Howard Buffett was one of those rare people who prospered in the aftermath of the 1929 stock market crash.1 Now his son’s star was rising during the second great crash of the century. But the world had changed; stardom, even in business, now meant fame. Buffett had closed his partnership during a media explosion in the United States in which cable had transformed television, newspaper companies were going public, and advertising was still in a golden age of selling to a monolithic audience in which virtually the whole nation sat down together on Tuesday nights and watched Happy Days.

Buffett had entered the media world as an investor drawn to the business by a natural affinity. But as he embarked on a new, post-partnership phase of life, he began to enjoy the fruit of the discreet use of profile-raising press. Now he was a subject of media interest, not just a media investor; and no less a personage than Katharine Graham was paying him attention, which had brought him into the orbit of one of the most important newspapers in the United States.

As was her habit with powerful men, Graham reached out to him for help. Buffett needed little encouragement.

“The first time she was going to speak to the New York Society of Security Analysts, I went over there to her apartment in New York on a Sunday morning to help her write her speech. She was a basket case. She was terrified that all these men were going to be there and she was going to have to stand up in front of them. Public speaking was something that was very hard for her always. The funny thing is, she had a great sense of humor, she was smart, but she tended to freeze in front of a crowd. Particularly if she thought they were going to question her about numbers.”

As Robert Redford had said in an interview after first meeting her to discuss the Watergate movie All the President’s Men, Graham had a “tight-jawed, blue-blooded” quality that demanded that her privacy not be invaded. Why, therefore, Redford asked himself, “did she keep making speeches and accepting awards?”2—particularly since it terrified her to do it.

Buffett sat down in the living room of Graham’s apartment in the UN Plaza, overlooking New York City’s East River. Surrounded by Asian art and antiques from Agnes Meyer’s collection, they started to work.

“She kept imagining these questions they were going to ask, like how much are you paying for your newsprint per ton? She thought it was a quiz.… I kept trying to get her away from trying to remember facts. Just have a theme.” Graham wanted to say that good journalism makes good profits. Buffett snorted to himself over this notion and refocused her. “You know, good journalism is not inconsistent with good profits, or something like that. The hell with all the other stuff. I just tried to convince her that she was a hell of a lot smarter than all those dumb males that were out there. That’s what really sort of bonded us initially.”

In an ironic turnabout, Buffett became Kay Graham’s personal Dale Carnegie instructor. He, of all people, could sympathize with someone who tended to freeze in front of a crowd. Moreover, thanks to Susie’s gentle tutelage over the years, he had learned a subtler way of dealing with people. He knew how to anticipate their reactions and to phrase things in a nonthreatening way. His letters, which had always been self-conscious, were now more deftly worded and empathetic. He had learned to listen and show interest in other people. It helped that he was genuinely fascinated by Graham.

Buffett returned to Omaha having seen a new side of Graham. As he continued getting to know her on a personal level, he saw her as a bundle of paradoxes. “Fearful but willful. Patrician but democratic. Wounded by the people she cared most about.” He was surprised how much she still talked about her former husband a decade after his suicide.

“When you first met her, she would often get off on the subject of Phil very quickly, almost like Charlie getting off on a subject. And she described him in terms that were sort of hard to believe, considering how badly he treated her. But after I got to know her better, she told me everything about him and the relationship.…

She felt she was a fraud, almost, even pretending to be in the same room with him.… Anything he said was funny, anything he did was right. When he used to chop up the children right in front of her, she wouldn’t stop him.”

That he and Graham—who showed the aftereffects of an upbringing by a cruel, neglectful mother and years of abuse by a sadistic husband with untreated bipolar disorder—would be mutually attracted seems almost a foregone conclusion given Buffett’s own childhood experiences. By the spring of 1974, she began to switch her allegiance from her other advisers to him. He seized the chance to tutor the CEO of the Washington Post Company about business as if he had been waiting to play Pygmalion all his life: his very own Eliza Doolittle. More patient than Henry Higgins, he coached her gently and sent helpful, interesting articles to Kay and to her son Don.

As Buffett’s influence grew stronger, Graham noticed that the words “Warren says” brought shudders from some of her board members.3 And Buffett himself was hoping to be invited onto that board. When Tom Murphy had approached him to join the Cap Cities board, Buffett told him no, he was holding out for the Post.4 Murphy dutifully spilled this news to Graham, who “felt dense” for not having figured it out herself.5

Susie thought that instead of taking on more business responsibilities, her husband should use their wealth for a higher cause. Riding with him in a taxi in Washington, D.C., she pointed out philanthropist Stewart Mott, who was running the Stewart R. Mott Charitable Trust, which gave money to peace, arms control, and population and family-planning causes. The Buffetts were now richer than Mott, who had started with $25 million. “Why don’t you quit?” Susie said. “Stewart Mott is doing all these other things now and he doesn’t have to work every day.” But Warren was incapable of quitting; he fell back on his philosophy that $50 million today would be worth $500 million someday. Nonetheless, he had picked up some vibrations from Susie, a sense that she wanted more from her life. With Peter moving along in high school, Warren told her, “Susie, you’re like someone who has lost his job after twenty-three years. Now what are you going to do?”

The answer, she said, was sing. Her nephew Billy Rogers had made her some instrumental guitar tracks so that she could practice. Rogers had been playing jazz guitar at clubs in Omaha, and along with him, Susie was now a familiar face in the local music scene. But when she first started practicing, “I was scared, really scared,” she said. “I was bad.” She got coaching and worked on contemporary love songs and ballads. Susie first debuted as a chanteuse that July, before a friendly audience at a private party at Emerald Bay. It thrilled her husband to see his friends applauding his wife’s talent.

While the Buffetts were in Emerald Bay that summer, Warren invited Graham for a visit. Sensing that Graham was going to talk to him about joining the Post board, Buffett had been dancing around his office at Kiewit Plaza for days ahead of time, happy and excited as a kid on Christmas Eve.6

Apparently, he must have impressed upon his wife that they would have to make an unusual effort for Graham. The first morning after Kay arrived, Susie rose at an unheard-of hour and cooked a full breakfast, which both of the Buffetts pretended to eat. Her husband spent the rest of the day wrapped up in Graham, talking to her about newspapers, journalism, politics, and bringing up every opportunity for her to invite him on the board.

At some point, he donned a bathing suit purchased for the occasion, picked up a beach umbrella bought in Graham’s honor, and walked the hundred or so yards to the shore to join the family. Previously, his attitude toward the ocean had been: “I think having the ocean nearby is an attractive feature, and fun to listen to at night, and all that kind of stuff. But actually getting in it—I feel I’ll save that for my old age.” But now, after sitting on the sand for a bit, looking at the water, he waded gamely into the Pacific. By all reports, Susie and the Buffett kids “went into convulsions of laughter” at the odd sight.

What Susie thought about this extraordinary gesture is not known. But Warren’s explanation of it is on record: “Only for Kay,” he says. “Only for Kay.”

On Sunday morning, they dropped their company manners and Susie sleepwalked through cooking bacon and eggs for Graham, eating nothing herself, while Warren sat nearby spooning chocolate Ovaltine from a jar.7 After breakfast, he and Graham resumed their tête-à-tête. At some point, Graham told him that she wanted him to join her board but was waiting for the right time. She knew that some of her board members, such as André Meyer, would not welcome Buffett. But he asked, “When is the right time?” thus forcing her to make up her mind. And so in short order it was done; they agreed that Buffett would join the board of the Washington Post Company. He was elated.

That afternoon, Buffett left his family at Emerald Bay and drove Graham to the Los Angeles airport. “On the way, all of a sudden, she looked at me like a three-year-old kid. Her voice changed, and her eyes, and she said, basically pleading, ‘Just be gentle with me, please don’t ever assault me.’ I learned later that Phil and some people at the paper, to get their own ends or for sheer enjoyment, would push her buttons just to watch her fall apart.”

At summer’s end, on September 11, 1974, Buffett officially joined the board, which catapulted him from a star investment manager from Omaha to official adviser at one of the most important media companies in the world. Even at that first meeting he could see that Graham had a habit of pleading with the board for help. Buffett thought, This won’t do. You can’t put yourself in that position as a CEO. But he didn’t yet know her well enough to say anything. Instead, he educated himself about the Post board, which was full of many prominent and influential people, and began to tiptoe his way through the powerful, jockeying men who were used to dominating Graham. He was a quiet board member, however, and used his skills behind the scenes.

Buffett at the time was preoccupied with far more than just Kay Graham and the Washington Post. The market, expected to rally in 1974, instead was in the full throes of collapse. Pension fund managers had cut back their stock purchases by more than eighty percent. Berkshire’s portfolio looked as though someone had given it a severe hedge trimming, shearing off nearly one-third in the second Great Crash, the kind that comes along only a few times in a century.

Munger had kept his partnership open after Buffett had shuttered his. Now its value was plunging, his partners losing nearly half of their money.8 Like Ben Graham half a century earlier, he felt obliged to make their money back.

“Certainly the quoted value of my capital went down,” says Munger. “I didn’t like it, but just think about how many years could go by—what difference does it make at the end whether I have X dollars, or X minus Y? The only thing that bothered me was that I knew how hard it was on the partners. That was what killed me—the fiduciary aspect of my position.”9

To earn back losses of half his capital, Munger would have to more than double the remaining stake. The value of Blue Chip Stamps would have a significant bearing on whether he could accomplish that.

Bill Ruane’s Sequoia Fund was also in trouble. It had started with $50 million from Buffett’s former partners and invested its money well by taking large positions in undervalued stocks like Tom Murphy’s Capital Cities Communications.

“In this business,” Ruane said, “you have the innovators, the imitators, and the swarming incompetents.” The swarming incompetents were now at the wheel, and the stocks that Ruane and his partner Rick Cunniff had bought in 1970 had been cut in half. The fund’s worst year yet was 1973 and it was on its way to another terrible year in 1974. The timing of Sequoia’s opening was obviously inauspicious—Ruane had agreed to start up just as Buffett was shutting down due to lack of opportunities. Sequoia had underperformed the market every year—cumulatively by a dramatic amount.10 Ruane’s largest backer, Bob Malott, was incensed. He was already known as a “ballbuster” around the halls of Ruane, Cunniff for his habit of calling to complain about minor discrepancies in his family’s accounts. Now he berated Ruane for buying a seat on the exchange before the crash, and for his poor performance with such persistence that Ruane feared he would pull his capital out of the firm.11 Buffett, however, remained serene in the knowledge that Mr. Market’s opinion of a stock’s price at any time had no bearing on its intrinsic value.

If not exactly an ego booster, because of the snooty staff, Buffett’s 1969 meeting of the Grahamites at the Colony Club had at least provided mutual support in a challenging market. Since then Buffett had named them the Graham Group; in 1971, Buffett made the meetings biennial. Out of loyalty, he let Ruane invite Malott—a favor normally verboten—for the meeting in Sun Valley in 1973.

Malott, mightily impressed by the whole affair, stayed in Ruane’s fold, even though his complaints continued at a frequency and volume that still made Ruane fear his defection. By the end of 1974, however, the Sequoia Fund had at least managed to produce a smaller loss than the market’s.

Nonetheless, the market’s cumulative toll on the Sequoia Fund was such that Henry Brandt and John Loomis, Carol’s husband, both of whom had gone to work there, feared the worst and cast off from what seemed a sinking ship.12

Forbes captured Buffett’s attitude in an interview that November, which opened with a juicy quote: Asked how he felt about the market, “Like an oversexed man in a harem,” Buffett replied. “This is the time to start investing.”13 He went on to say, “This is the first time I can remember that you could buy Phil Fisher [growth] stocks at Ben Graham [cigar butt] prices.” He felt this was the most significant statement that he could make, but Forbes didn’t include it; a general audience wouldn’t understand the references to Fisher and Graham.14

But despite his enthusiasm for the market so far in 1974, he had invested at a trickle, and mostly moved money around. He had also bought 100,000 shares of Blue Chip from Rick Guerin. “He sold me at five bucks because he was getting squeezed,” Buffett says. “That was a brutal period.”

The “harem” comment had a double meaning: Buffett, for the most part, could look but not touch. One of National Indemnity’s business partners, an aviation broker, had run amok, selling money-losing aviation-insurance policies. The company had tried to stop the agent by revoking its authority but for several months was unable to shut it down.15 The accounting records were a shambles and the losses were unclear. National Indemnity had no idea how high the bill for the “Omni affair” would run, but worst-case estimates ran as high as tens of millions of dollars. The hope was that they were much less, because National Indemnity did not have tens of millions. Buffett was sweating.16

Within a couple of months—by early 1975—his problems compounded monumentally. Chuck Rickershauser, a partner from Munger’s law firm, now renamed Munger, Tolles & Rickershauser, called him and Munger to say that the Securities and Exchange Commission was considering pressing charges against them for violating securities laws. What had seemed like a brewing but manageable problem had now exploded into a full-scale emergency.

Rickershauser had first started doing legal work for Buffett during the See’s transaction. More recently he had been fighting a rear-guard action, ever since an SEC staff lawyer had called him with some questions. Assuming the matter was routine, Rickershauser had directed the man to Verne McKenzie, Berkshire’s controller.

When McKenzie’s phone rang in Nebraska, he picked it up to find the head of the SEC’s Enforcement Division, Stanley Sporkin, the much-feared “tough cop” of the business world, on the other end of the line. Sporkin looked as though he spent his evenings hunched droopy-eyed under a desk lamp, personally drafting the charges against large corporations that for the first time in American history had frightened a remarkable number of them into settling with the SEC without ever setting foot in court.17 In a practical sense he had more power than his boss, the chairman of the SEC. Sporkin interrogated McKenzie on a wide range of subjects, from Wesco to Blue Chip to Berkshire and beyond. His tone was not friendly, but this, McKenzie had assumed, was simply his modus operandi. On the other hand, McKenzie did get the impression that Sporkin thought if you were rich, you must have done something wrong.18

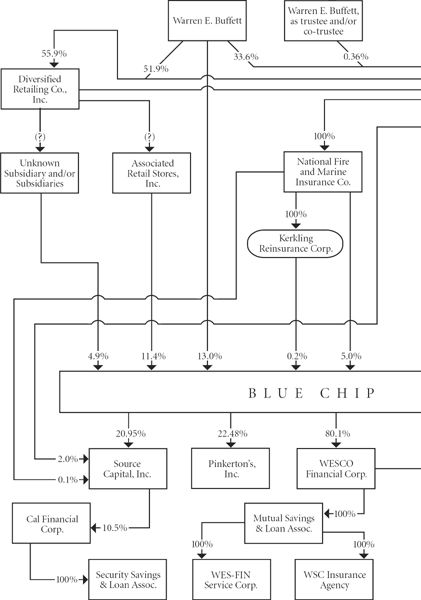

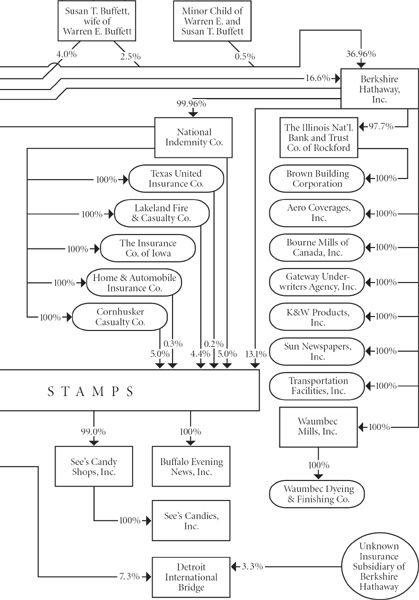

What seemed to have drawn the SEC’s attention was a project of nearly two years in which Buffett and Munger were trying to delicately untangle the many strands of spaghetti that connected the several companies they owned. Their first step had been to try to merge Diversified, the least essential piece, into Berkshire Hathaway. By 1973, Diversified had become little more than a vehicle for buying Berkshire and Blue Chip stock. But the Securities and Exchange Commission—whose approval was required—had delayed the Diversified deal. Munger had told Buffett that this was not anything serious.

Instead, over the next eighteen months, the SEC staff seemed to have nosed around looking at Blue Chip Stamps and other investments; it concluded that Buffett and Munger had smashed up the Wesco–Santa Barbara deal deliberately by offering a high price for a quarter of the stock for the purpose of taking over the rest. At least, that must have been how it looked to Santa Barbara, for it had apparently turned in Blue Chip to the SEC.19

For the first time they all realized that Blue Chip was in trouble.20 No sooner had Buffett achieved the glory of joining the Post board than his and Munger’s need for legal services was about to grow with stunning rapidity. Rickershauser, who already knew what it was like to work with Buffett, had once explained to a colleague that “the sun is nice and warm, but you don’t want to get too close to it.”21 He would spend the next couple of years testing what could be called Rickershauser’s Law of Thermodynamics.

In February 1975, the SEC issued subpoenas and launched a full-blown fraud investigation of Blue Chip’s purchase of Wesco: “In the Matter of Blue Chip Stamps, Berkshire Hathaway Incorporated, Warren Buffet [sic], HO-784.” The commission staff speculated that Buffett and Munger had committed fraud: “Blue Chip, Berkshire, Buffet [sic], singly or in concert with others … may have engaged in acts which have, directly or indirectly, operated as a device, scheme, or artifice to defraud; or included an untrue statement of a material fact or omitted …”

The commission’s lawyers zeroed in on a theory that Blue Chip had secretly planned from the beginning to take over Wesco Financial but had not disclosed that fact, and that Blue Chip’s purchases of stock after the Santa Barbara deal dissolved were “tender offers” that were never registered with the SEC.22 This latter charge was most serious—the SEC might even file, with great fanfare and publicity, civil fraud charges not only against Blue Chip but also against Buffett and Munger personally.

In considering action against a target, Sporkin had a choice. He could prosecute or settle. A settlement let the target say sorry and accept a penalty without officially admitting guilt. And in agreeing to a settlement, the SEC could also make a deal with the company itself without naming anybody. Being named in a settlement might not be the literal end of someone’s career, but there would be no elephant-bumping afterward. Having so recently been elevated into the high and mighty through Supermoney and Forbes and the board of the Washington Post, Buffett began to fight desperately to save his reputation.

Instead, the investigation widened. Under subpoena, Buffett had to open his files—which, naturally, represented a huge and comprehensive collection of documents, just as huge and comprehensive as everything he had ever collected. Lawyers from Munger, Tolles sifted out trade tickets for recent stock purchases, memos to bankers, letters to See’s Candies, notes to Verne McKenzie at the textile mill, and the like and shipped them off to investigators in Washington, D.C. Buffett felt persecuted. He and Munger were being chased in a nightmare by a huge, lumbering giant. To survive, they would have to outrun it.

Letters flew back and forth like shuttlecocks between Munger, Tolles and the SEC. Buffett maintained a veneer of calm, but his back problems were plaguing him. Munger did not hide his agitation.

By March 1975, the investigation had wound its way to a command performance at the SEC. Betty Peters was hauled in and came without a lawyer, surprising the SEC staff. “Don’t you just want to know what happened?” she asked. They interviewed Peters without a lawyer.

Munger was summoned. For two days—also unaccompanied, for what additional legal counsel could Charles T. Munger possibly need?—he tried to defend Blue Chip against the charges. Yes, Blue Chip had thought about getting control, he said, but those plans were only “remote and contingent” until the Santa Barbara merger blew up. This discussion became somewhat circular given his and Buffett’s role in talking to Vincenti and their admitted “wooing” of Betty Peters and the Casper family’s votes. Munger had a regrettable tendency to interrupt and lecture the SEC staff lawyer, Larry Seidman. “We wanted to look very fair and equitable to Lou Vincenti and Betty Peters,” he said.23 What about your Blue Chip shareholders? Seidman asked. Seidman saw no reason for Blue Chip to be so generous to Wesco shareholders; Wesco’s stock by then was largely in the hands of arbitrageurs.

These people had bought Wesco’s stock knowing that once the deal closed it would rise to the price that Santa Barbara had offered. They hedged their bets by shorting Santa Barbara’s stock. When the Wesco deal blew up, Wesco’s price collapsed.24 Why do the arbs a favor by propping up the price?

Munger reached for his ultimate weapon—Benjamin Franklin. “We didn’t feel our obligation to the shareholders was inconsistent with leaning over backward to be fair. We have that Ben Franklin idea that the honest policy is the best policy. It had a sort of shoddy mental image to us to try to reduce the price.”25

Seidman seemed a little baffled by this argument, and even Munger admitted that the details of what had been done did not look good. He begged Seidman to look at the big picture. “As you look at the overall records, we go way beyond any legal requirement in trying to be fair with people to observe the niceties of fair-dealing.… If there’s any defect at all, it’s not intentional.”

When Buffett appeared, they asked him why he and Munger hadn’t let Wesco go into the tank so they could buy it cheap. “I think the general business reputation of Blue Chip would not have been as good,” Buffett said. “I think someone might have been sore about it.” But why should he care? Because, said Buffett, “Lou Vincenti doesn’t really need to work for us.… If he felt that we were, you know, slobs or something, it just wouldn’t work.”

Now Buffett—who, like Munger, startled the enforcement lawyers by showing up alone—made himself helpful, venturing back to Washington several times, patiently explaining how Blue Chip worked, expounding on his investment philosophies, and talking about his childhood years in Washington. He made a favorable impression on Seidman, but not on the senior SEC staff lawyer who was in charge of the investigation, a “tiger” of a prosecutor whose motto was “They shall not pass.” He found these arguments unconvincing.26 The senior investigator’s attitude was that nobody who did anything close to the line would ever get by him.27

The SEC staff seemed fascinated by the intricacies and complications of Buffett’s empire. It even started looking into whether he had traded on inside information about San Jose Water Works.28 The staff started kicking around Source Capital, the closed-end investment fund that Munger had bought a twenty percent interest in as a cigar butt. By then, the stock market had recovered. Ruane’s Sequoia Fund had made a huge comeback in 1975. Munger had just about made back his partners’ money, with a seventy-three percent gain in 1975. He took no fees for himself, and was winding his partnership down. Explaining why their convoluted empire made sense based on the cheap prices paid for stocks at the time grew harder as the market recovered.

Rickershauser had been studying a chart that showed Buffett and Munger’s complex financial interests. Buffett sat at the center, buying Blue Chip, Diversified, and Berkshire, Wattling them into so many pockets that it made Rickershauser shudder.29 Everyone knew Buffett, the great white shark, was virtually helpless to stop himself from acquiring these stocks. After he and Munger had bought the first twenty-five percent of Wesco, Rickershauser had finally advised Buffett to buy stock only through formal tender offers to avoid the appearance of impropriety.30 The complex cross-holdings that Buffett had created looked suspicious. Rickershauser stared at the crazy diagram and fretted, “There’s got to be an indictment in there somewhere.”31 He didn’t think the SEC would have enough evidence to convict, but it would be awfully easy to accuse.

Munger was a two-bit player, his financial stake minute compared with Buffett’s. He had been snared as a petty accomplice. But Blue Chip was his territory, he was a principal in the Wesco saga, and thus central to the SEC’s questioning.32 He told Seidman, “We do have a very complicated set of business affairs, and I think we have learned, to our regret, that that may not be too smart.”

Despite the pair’s protestations and the fact that it could find nothing wrong with the San Jose Water Works or Source Capital deals, the tiger of a prosecutor now recommended to Sporkin that the SEC charge Buffett and Munger personally. He was unswayed by their testimony and believed they had intentionally quashed the Santa Barbara merger by overpaying for the stock. He was unsympathetic to the “Who was harmed?” explanation for paying more than necessary for Wesco’s stock. He thought the pair was splitting hairs too fine in its explanations of events.33

Rickershauser wrote Sporkin directly. He pleaded with him not to prosecute Buffett and Munger, “individuals who value their good names and reputations as their most priceless possessions,” because “many people, probably most people, assume evil conduct on the part of anyone civilly prosecuted by the commission.” Even if Buffett and Munger consented to a settlement without admitting or denying the charges, merely filing them would cause “terrible, irreversible damage” because “the good reputation of the commission automatically and inexorably destroys the good reputation” of the defendants. “A giant’s strength should be used with great discretion,” he urged. “The risk from inadvertent oversights in business should not become so onerous that people who value their reputations are deterred from participation.”34 He offered to consent to an order on minor, technical disclosure violations on behalf of Blue Chip only, as long as the consent decree did not name any individuals.

The panic inside Buffett’s mind can only be imagined. Within the office, he did his best to maintain an imperturbable facade so as not to alarm his staff, any of whom might be interviewed by the SEC.

Rickershauser worked like a stevedore to portray his clients as upstanding citizens from the perfect model families. He sent in biographies of Munger and Buffett to the SEC, stressing their charitable work, the many boards on which they served, Howard Buffett’s tenure as a Congressman, and the millions of dollars of taxes that Buffett had paid to the government since filing his first tax return at age fourteen. Buffett obviously had been grinding away at this document as if his life depended on it.

Munger was resigned. “If a policeman follows you down the road for five hundred miles,” he said to Buffett, “you’re going to get a ticket.”

Then Rickershauser made a further proffer to Sporkin, put delicately: “The complex financial interests of Mr. Buffett and Mr. Munger … have apparently raised the impression that compliance with various legal requirements is becoming difficult,” he wrote, noting the pair had tried to comply with both the spirit and the letter of the law. “They now wish to simplify their holdings as rapidly as they can.”35

In their interviews, the SEC lawyers had already explored what simplifying would mean. Buffett had acknowledged that he might merge Blue Chip with Berkshire, but until Blue Chip’s legal problems were resolved, it would be hard to put a fair value on the company. “I don’t really like these complications,” he said. “It may look like I like these complications. I don’t have a great staff to handle it all. It seemed fairly simple while we were doing it,” he said, “but not simple now.”36

Asked by an SEC investigator if Buffett had “contingency plans” to simplify things, “Oh, does he ever,” said Munger. “He has about twice as big a contingency plan as before this investigation started.”37

In considering the proffer, says Sporkin today, much depended on Rickershauser. He “was one of those few lawyers that I’ve met in life that, whatever he told you, you could go to the bank on.” Rickershauser told Sporkin that Buffett was “going to be the greatest person that Wall Street has ever seen” and that “he was the most decent, honorable person you would ever meet.” Coming from almost anyone else, Sporkin says he would have dismissed this as rhetoric, but coming from Rickershauser, he took these statements to be both sincere and probably well-judged.38 Sporkin felt he had as great a duty to absolve as to convict. He thought that a prosecutor had to differentiate between a fundamentally honest person who had made a misstep and a crook. His view of Buffett and Munger was that they had certainly misstepped, but that they were not crooks.39

And so the giant tapped Blue Chip gently on the wrist.40

The company consented to an SEC finding that named no individuals.41 The publicity over the event had been trivial and would fade. Buffett’s and Munger’s records and reputations stayed clean.

Two weeks later, the SEC named Buffett to a blue-ribbon panel to study corporate disclosure practices. It was forgiveness and, above all, a fresh start.42