Get Control of Your Finances With Small Business Cash Flow Made Simple

Step Six Will Help You Solve These Problems:

- You aren’t sure where your personal finances and the business finances begin and end.

- You consistently worry you are going to run out of cash.

- You get profit-and-loss statements from your accountant but they seem confusing and don’t help you make decisions.

- You aren’t sure how much profit the company really makes.

- You want the small business to help you make outside investments that build personal wealth.

- You want extra money to reinvest back into the business for hiring, new technology, advertising, and more.

- You need real-time optics into how your small business is doing financially.

• • •

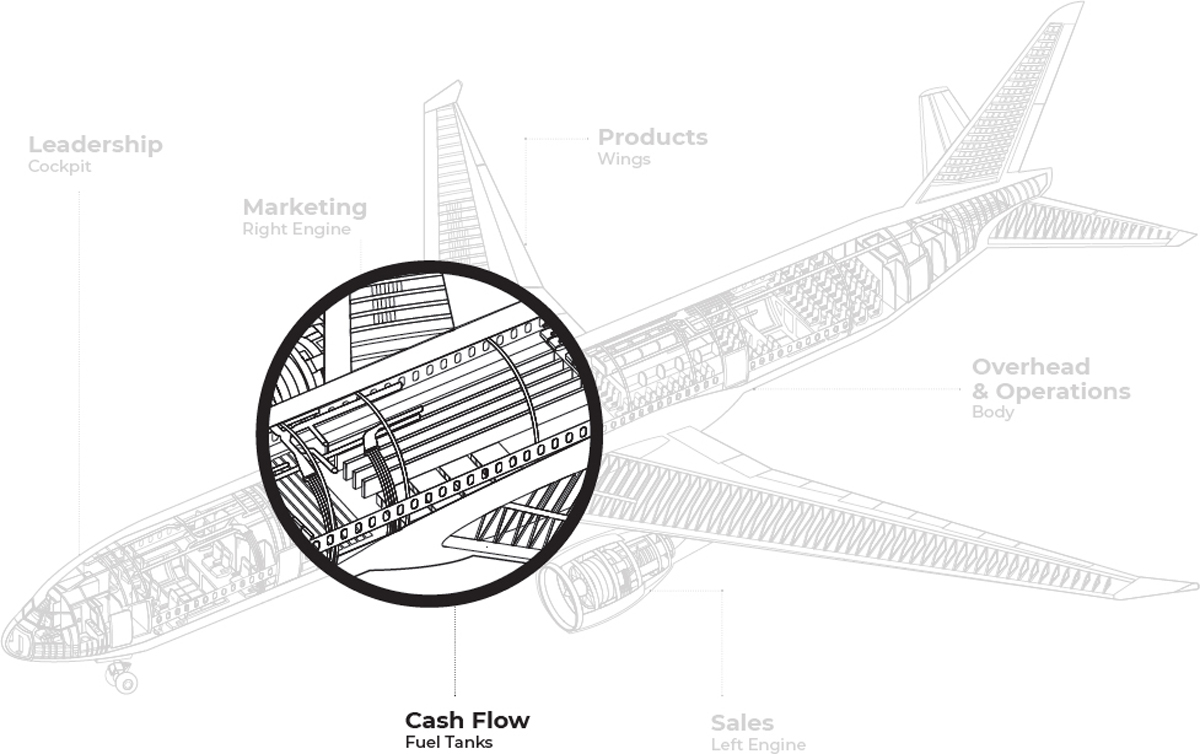

If you manage the six parts of your business well, it should grow, and you’ll start making more money. This brings us to the final step in our list: Small Business Cash Flow. Even if your business is engineered like the perfect airplane, it is shockingly easy to run out of money and crash your plane.

As it concerns our airplane metaphor, the way you manage the money coming in and out of your business is represented by the fuel tanks. If you have plenty of fuel, you can fly your airplane far and fast. More than that, you can circle the airport when there is trouble and secure yourselves plenty of time to fix whatever is wrong.

Stories have been told about pilots who have circled airports addressing a problem with their plane only to crash because they ran out of fuel. No matter how big and beautiful your airplane is, without fuel, it’s going down.

So, how do we manage money in such a way that we can pay our bills, enjoy a great salary, put some profit away for a rainy day, pay our taxes, leverage our success into a diversity of outside investments, and, most importantly, never run out of money?

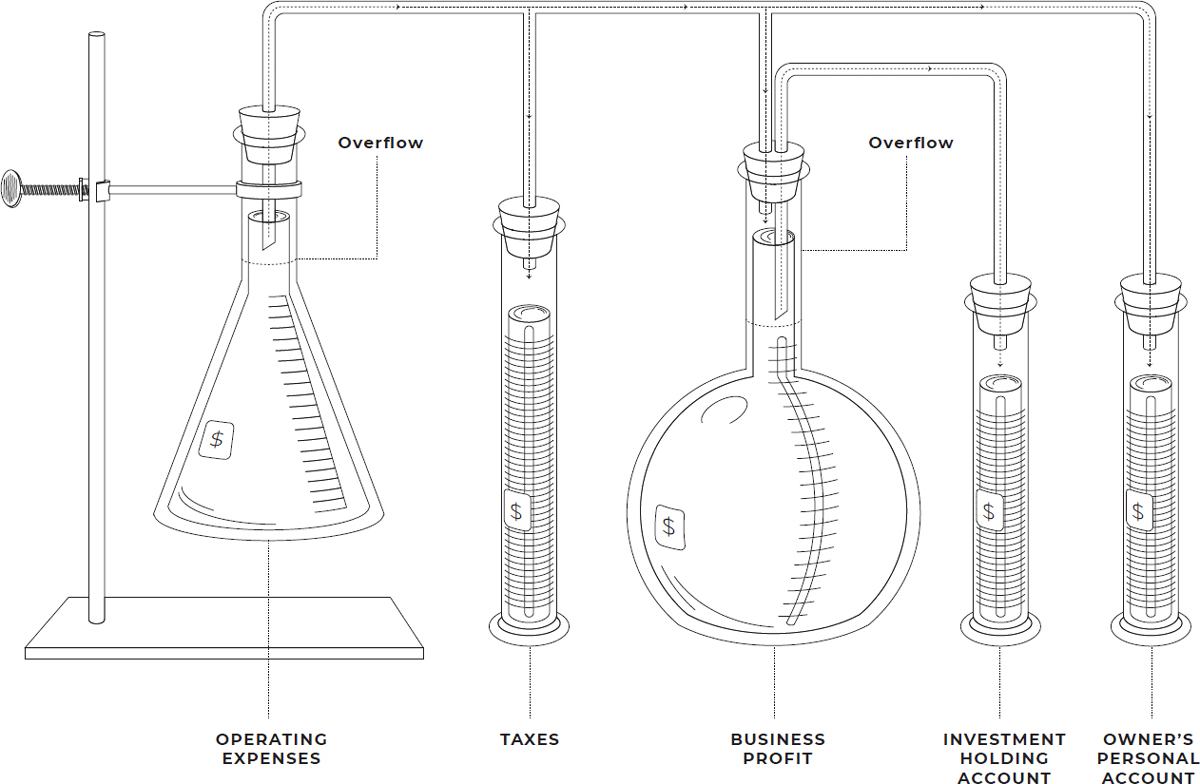

The answer: Manage your small business cash flow using five checking accounts.

You Don’t Have to Sweat the Finances

I created the Small Business Cash Flow Made Simple Playbook by accident. Like many small-business owners, when I started my business, I operated with only two accounts: my personal account and my savings account. My business expenses, along with my personal expenses, all came out of my personal account. This was a huge mistake not only because it made filing taxes difficult, but it blurred the line between my business and my personal life. At the time, I had no employees and really didn’t see a difference between what I spent to make money and what I spent to eat and live. Because my company was being run out of my personal checking account, though, I found it hard to know where the company was succeeding and where I was bleeding it dry.

Slowly, I began to add more accounts to my banking system. I added an operating expense account, so I could keep track of the money going in and out of the company. A couple of years later, after I got tired of not having enough money for taxes, I opened an account to set aside tax money in advance. From there I added an account for a rainy-day fund, and so on. I’ll explain each account and how I use them a little later.

Soon, I realized I’d created a terrific money-management system for a guy who hates managing money. I love to make money, but I’m not the type to sit and count every dollar and review the budget and pore over profit-and-loss statements for hours.

The Small Business Cash Flow Made Simple Playbook is perfect for business owners and leaders who identify more as moneymakers than as money managers. That’s not an excuse; we all need to steward our money well. It’s just that most entrepreneurs like making it more than managing it.

Here is what running my money with five checking accounts has allowed me to do:

- I can log onto my online banking portal and see the overall health of my company in an instant.

- When I log onto my banking portal, I know how much money my wife and I have and how much money my business has. I know that I only have access to one of those piles of money. I never dip into the company for personal gain.

- I am never short of cash when the tax man comes. I can pay taxes, and it never bothers me (okay, maybe a little) because I’ve already psychologically separated myself from the money I will pay the government.

- I know the business can suffer a loss and/or survive a crisis and we will not have to lay anybody off because I have plenty of money put away for a rainy day.

- When I log onto my online banking portal, I can see how much money my wife and I are putting away to create personal wealth for ourselves and our family. My business exists to generate money I can use to buy financial products and investments that will make my family even more money generations into the future.

If all of this sounds too good to be true—especially for somebody who likes making money more than managing money—you’re going to enjoy the Small Business Cash Flow Made Simple Playbook. You no longer have to sweat the finances.

The Small Business Cash Flow Made Simple Playbook

The five checking accounts you will use to manage your small-business finances flow in and out of each other to create a fluid system that will give you optics, and control, over your money.

Here is a detailed description of each of the five checking accounts and a breakdown of how to use them.

Operating Account

All of the money that flows into and out of your business will flow into and out of this account. This is the main account you will use to pay all your bills, including your personal salary. Yes, you have to establish a personal salary. It’s critical to the health of your business.

Personal Account

Your Personal Account will receive an automated bimonthly or monthly transfer from the business account that will make up your personal salary. How much money you pay yourself depends, and it’s largely up to you. If your new business is a side hustle, you might pay yourself very little so you can get the machine going. If your business is established, you can and should pay yourself much more. You deserve it. You will figure out how much you can pay yourself as you go along. The key principle, though, is this: You must live off of a fixed salary so the business can establish a predictable rhythm, allowing you to manage and grow the business. As the business grows, you can give yourself raises. Don’t forget: Your salary, unlike everybody else’s salary, is taxable income. I’ll show you how to put tax money aside in a minute.

Business Profit

Your Business Profit Account is where you store the money your business makes that does not need to go back into the company in order to keep it alive. You will establish a high-water mark for your Operating Account. When you have excess money in the Operating Account, you will transfer money into your Business Profit Account. The high-water mark will be different for everybody and will change as your business grows. This account will also serve as your rainy-day fund you can dip into if the business suddenly encounters a headwind and starts burning more fuel.

Tax Account

Your Tax Account is where you will put the money you’ll use to pay or pre-pay taxes. This account will serve you in two ways: First, it will give you peace of mind that you will always be able to pay your taxes (while stopping you from spending the money elsewhere) and second, it will act, in some ways, as a secondary safety account. I’ll explain a little more about that later.

Investment Holding

Your Business Profit Account is the place where you put money and keep it for a rainy day, but if that account grows so large that it doesn’t make sense to keep all of it as an emergency fund, you’ll move that money into an Investment Holding Account and decide from there what to do with it. As the name suggests, I recommend using this money to buy outside investments that will make you even more money without you having to work for it. You can invest in real estate, stocks, insurance products, CDs, cryptocurrency, whatever you want. If you want to buy a second home or a bass boat or a family vacation in Europe, you can do that from this account too. Your Investment Holding Account holds the money the company made for you. It’s your money. Still, if you invest your money rather than spend it, your money will start making even more money and that’s the money the uber-wealthy like to live off of. Making money off of money is how many of the ultra-wealthy get and stay wealthy. In other words, your business is a machine that makes you money so you can buy another machine that makes you money. The difference between the first and second machine is that you have to work in the first machine and the second machine makes money without you working at all.

Should You Take Out Your Profit First?

If you’re familiar with Mike Michalowicz and his book Profit First, you’ll see a resemblance between my playbook and his. I promise, I didn’t steal Mike’s ideas. On a long drive one summer I listened to Mike’s book and realized, for the first time in my life, I was not a complete idiot when it came to managing the company money.

For years I’d used this playbook and had never run into financial trouble, but I always wondered if it was just a band aid. I thought real businesspeople likely do it differently or had a better system, but Mike’s book taught me that I was getting a lot more right than I was getting wrong.

Since I listened to his book, Mike and I have become friends. In fact, I will never write a book about my small-business cash flow system because Mike has already written it. If you want to take a deep dive into how to run your business using five checking accounts, read or listen to Profit First.

That said, there are two things I do differently than Mike. The main point of Mike’s book is that you should take a fixed percentage of revenue out of the company at the beginning of each month. The money you take out first is the profit you are projected to make that month. This forces you to reverse engineer a business that makes you a profit. I, on the other hand, take profit out of the company sporadically based on whether or not the Operating Account has a surplus of cash. In other words, I take the profit that “boils over” a high-water mark in my Operating Expense Account. If I took our projected profit out at the beginning of the month like Mike, I’d likely take less, not more money, out of the company for profit. My business often closes very large deals every other month or so, which means revenue spikes sporadically. When that happens, I scoop the profit out of and away from the business. If I took the profit out first, based on a fixed percentage, I’d constantly have to transfer money back into the company to keep it afloat or, in reverse, have way too much money in my Operating Expense Account and be too tempted to spend it.

Mike also recommends that the account I call Investment Holding should be opened at a separate bank that does not show up in your online banking portal. He truly wants that money out of sight. This is smart, but I prefer having all my accounts visible in one online banking portal.

Am I wrong to pull the profit out sporadically? Is Mike right to pull his out as a fixed percentage at the beginning of the month and place it in a blind account? I think both systems are a considerable improvement on the ways that many of us are managing our money.

Now that we understand the basic philosophy of the playbook, let’s break down the process of installing the playbook.

How to Install the Small Business Cash Flow Made Simple Playbook

Step One

Go to your bank and open five checking accounts. Those accounts should be your Operating Account, your Personal Checking Account, your Tax Account, your Business Profit Account, and your Investment Holding Account. You may already have some accounts like this; if you do, you’ll want to rename them to reflect their appropriate functions. In addition, make sure they all show up in your online banking portal so you can see the amounts in each account comparatively and at a glance. This is the key to having a clear picture of where your business stands financially.

Step Two

Make sure all the money for your business flows in and out of your Operating Account. All revenue from the business should flow into this account, and all bills should be paid out of this account (except for taxes, which are paid out of the Tax Account).

Step Three

Your bimonthly or monthly salary should flow out of your Operating Account, and that salary should be fixed, just like all your employees’. You should not take more money out of the Operating Account if you want to buy a car, an expensive watch, or an albino tiger. The key here is to decide how much you want to make and live off of that amount for a long time. The benefit of paying yourself a salary is mostly for mental clarity. This way you know what money belongs to you versus what money belongs to the machine that exists to make you more money.

Step Four

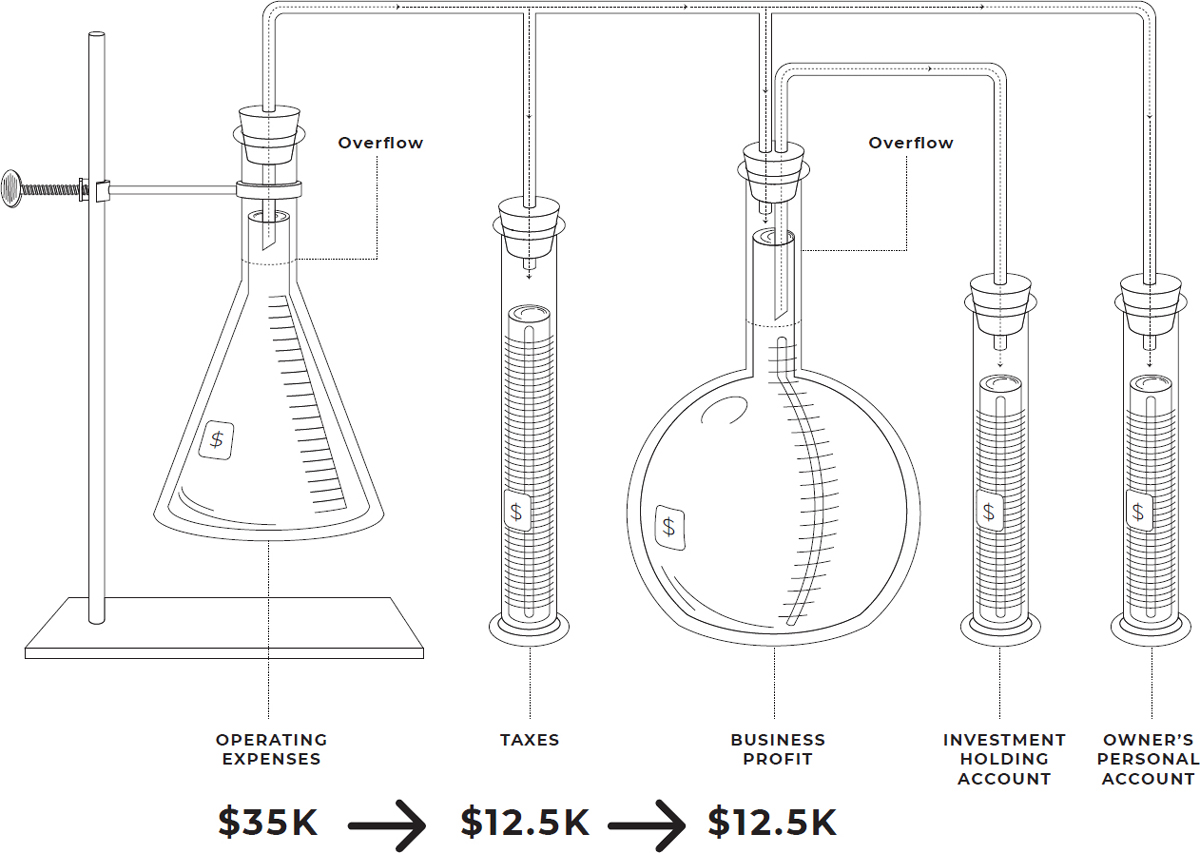

Establish a high-water mark for your Operating Account. By this I mean an amount of money high enough to cover the largest hit you might experience that month. For instance, if your payroll is $25K every two weeks, you never want your account to go below $35K or so. If you get hit by payroll, you’d be down to $10K, but you’d have two weeks to make it up before you get hit again. Let’s say your high-water mark, then, is $35K. That’s pretty good; this amount keeps you safe yet doesn’t allow a ton of excess money to sit around in your Operating Account (where people tend to spend it, and fast). Let’s say you look at your account one day and you had $60K in cold, hard cash. That means you’ve got $25K over your high-water mark sitting there doing nothing. What you’re going to do is take the excess $25K and split it between your Business Profit Account and your Tax Account. Simply log on to your online banking portal and transfer $12.5K to your Business Profit Account and $12.5K to your Tax Account. What results is your Operating Account is at $35K while your Business Profit Account increases by $12.5K and you’ve also put away $12.5K for taxes.

What’s great about this playbook is you can easily look at your Business Profit Account and know how much money is yours (on top of your salary) and feel good about how your business is doing. You can also look at your Tax Account and feel great about the fact that you have plenty of money to pay your quarterly business and salary taxes. In fact, you’ll probably be transferring into your Tax Account so that, at the end of the year, you’ll have an excess of money in your Tax Account that can be moved into your Business Profit Account. That dynamic is the exact opposite of what most small-business owners experience come Tax Day, so that day will feel great for you.

Step Five

Just like your Operating Account, you will also establish a high-water mark for your Business Profit Account. You will want to work up to and keep your Business Profit Account at or above that high-water mark because your Business Profit Account is also your rainy-day fund. I believe your Business Profit Account should be about six times your Operating Account’s high-water mark. If your Operating Account’s high-water mark is $35K, your Business Profit Account’s high-water mark should be $210K. I realize that’s a lot of money sitting there not earning much interest, but that money is going to buy you one of the most valuable things a small-business owner can have: peace of mind.

When you have six times your Operating Expense Account’s high-water mark, you have a reserve fuel tank that will allow you six months’ worth of circling the airport in the event of a crisis. With such a rainy-day fund, you can slowly adapt and even pivot in harsh weather or malfunctions in the plane. No more losing sleep over whether or not you will have to lay people off or crash-land the plane.

As your business grows, it will likely start to bother you to have so much money sitting in a basic checking account. If inflation starts to increase, that money really is being devalued by the day. If this becomes true for you, congratulations. You’re sitting on a pile of cash. Feel free to take some of the money in your Business Profit Account and put it into a better investment that gets a higher interest or return rate, but the key is to make sure that money is liquid. There will be times each year when you’ve miscalculated and will need to move money back from your Business Profit Account to your Operating Expense Account. Hopefully those instances will be rare as you adjust high-water marks and get a sense for when to transfer money into profit and taxes, but everybody experiences cash flow fluctuations. Regardless, the Business Profit Account mitigates the pain of those disruptions.

Remember this as well: Whenever you move money backward from Business Profit, you can move the same amount backward from taxes because that money is no longer taxable income. In other words, if you suddenly need $10K, you can move $5K back from Business Profit and $5K back from Taxes.

So, what do you do when your Business Profit Account has a glut of cash? Let’s say you check your account and transfer some money so that you have $250K in your Business Profit Account when your high-water mark was $210K. That means your business is now a true, profit-producing machine. This money is all yours. You can do with it what you want. However, before you buy the nautical brass collapsing telescope used in the filming of Pirates of the Caribbean 4, do take time to move that money into your Investment Holding Account. Why? Because the very name of that account is going to pressure you to invest that money rather than buy the telescope (even though there are only nineteen left). The money that ends up in Investment Holding is the money that can seriously contribute to your personal wealth.

Betsy and I used money from our Investment Holding Account to build our home with cash and fund our retirement accounts. We also purchased life insurance, put money in the stock market, bought rental property, and contribute to organizations we love. Betsy chairs the board of an anti-human trafficking organization and we use money out of Investment Holding to donate to the organization and host a large dinner every year in which we raise even more money. The great thing is we do all of this from a position of stability because the machine we built has allowed us to be strategically and predictably generous.

If you want to splurge using money from Investment Holding, feel free. But if you wait and buy your albino tiger from the money you make off your investments, you can have the tiger as well as future revenue that your investments continue to produce.

As I said at the beginning of this chapter, I am more wired to make money than manage it, yet I never feel the frustration of that fact. We always have the money to move the company forward, pay our taxes, live off of, and invest.

Should Your High-Water Marks Change as the Business Grows?

If you implement your Small Business Flight Plan, your business will grow. I remember years ago being kind of shocked scrolling through my Instagram feed when a friend publicly celebrated that their small business made two million dollars. I sat there and thought of that kind of success as impossible. But I kept running my business using the playbooks and frameworks you’ve just read about and within two years my company was bringing in more than three million dollars and continued to grow at double-digit percentages for years and years after and continues to grow today.

Don’t be surprised if your small business grows a great deal bigger than you imagined. If this happens, though, the high-water marks in your Operating Expense and Business Profit Accounts should change as your business expenses increase. Your high-water mark may need to change from $35K to $55K depending on how much money your business is bringing in and spending. How do you know when your high-water marks need to change? You will know when the hits to your Operating Expense Account start to get so large, they bring your balance closer and closer to zero. When that starts happening, congrats! It just means all the numbers are getting bigger, including your Investment Holding balance!

Of course, it may be true that you have partners in your business or other complications, such as investors. Not to worry. The key is to split up the Investment Holding Account according to a cadence agreed upon by all parties. The playbook works fine even with outside investors.

The great thing about the Small Business Cash Flow Made Simple Playbook is that it will grow with your business. Whether you’re managing a side hustle that makes $20K per year or have grown your business north of $100 million, the playbook works to help you make even more money and to preserve your sanity.