Before I came to the United States, I'd never envisioned being caught up in a stock market mania that would drastically alter my career and completely change my life. I loved physics, which I had studied for many years, and assumed I would become a physics professor someday. I'd never had anything to do with the stock market.

The summer of 1998 was hot, even for Texas. I came to work for Texas A&M University in an equally “hot” field in the physics department: fiber optics and lasers. This was during the momentous expansion of the Internet and the telecommunication industry, and everything related to the technological boom was hot, everything related to fiber optics was hot!

By then, I already had my PhD in physics in the field of lasers and optics from Peking University. I was excited to be working in a field that seemed to hold unlimited potential, and I found that people like me were in strong demand. In less than two years I was recruited by a fiber optical communications company that would soon go public. Business was booming. The company had dramatically expanded its office space and hired hundreds of additional engineers. The benefit that most attracted people to work for this particular company was its stock option offering. I had no idea what stock options were—I just knew that they would be worth a lot of money!

Everyone was talking about stocks and stock options. It sounds like fun! And it can make me money! I need to buy stocks, I told myself. I need to buy fiber optics stocks!

I felt that I had an edge. After all, I had worked with lasers and fiber optics for many years. I had published many research papers and would ultimately be awarded 32 patents in the field. I knew exactly how fiber optics worked.

I also knew the fiber optics companies. I used their products in my work, and demand for them was tremendous. Internet traffic was booming and the need for Internet capacity and fiber optics networks was expected to grow 1,000 percent a year. Companies like Global Crossing were laying fiber across oceans. WorldCom was hosting an exciting Terabyte Challenge, which would squeeze a terabyte per second of bandwidth into a single optical fiber. The demand for fiber network capacity, it seemed, would grow exponentially, forever.

In a trillion-dollar market, no one could lose, analysts wrote. The stocks of these fiber optics companies would double in three months, and that was true for every fiber optics company that was going public.

I started my shopping spree. In 2000, I bought the stocks of fiber optics companies New Focus, Oplink, and Corning. Corning, the old dog that learned a new trick in fiber optics, was making the optical fiber cable used in fiber networks. It didn't disappoint me, quickly doubling and then some. Corning was doing so well in fact that the stock went on a 3:1 split. It was fun!

But, I would later realize, I was lucky I didn't have much money to buy stocks with back then.

The Bloodbath

The party didn't last very long—and I'd arrived late.

Without my realizing it, things were turning sour with my employer. By the end of 2000, the company was already quietly laying off contractors and temporary workers. It turned out that our biggest customers, WorldCom and Global Crossing, were having their own problems and had stopped buying equipment.

Then 9/11 hit and everything came to a grinding halt. My company had lost 80 percent of its sales from the previous year, and WorldCom was on the verge of bankruptcy. All new product development had ceased, and my company was now ruthlessly laying people off. In less than two years the company had lost more than 75 percent of its employees and was itself on life support. The people who were still there, including myself, felt lucky just to have a job. No one talked about stock options any longer. The company's initial public offering (IPO) plan had long since been shelved, permanently.

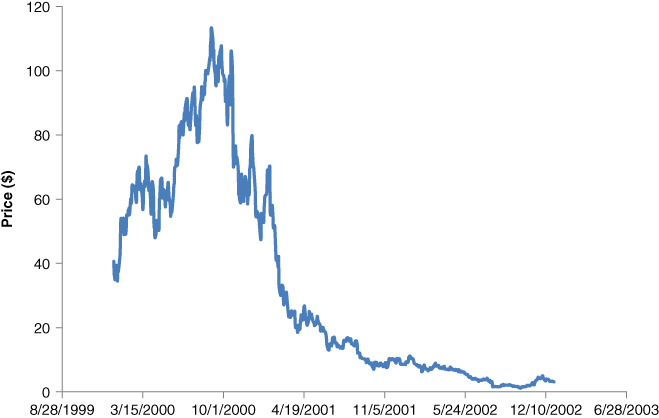

So, what happened to my fiber optics stocks? The chart below illustrates the stock prices of Corning from January 2000 to the end of 2002. I bought the stock in January 2000 at around $40 a share (split-adjusted). In about nine months, it almost tripled—going all the way up to $110. Then it started its decline. For a while I didn't budge, as I still had a sizable gain. Of course, it never went straight down. It fluctuated. And these fluctuations gave me hope. It will come back, I kept telling myself. Then, in 2001, as the bad news about the telecom industry flooded in, the falling accelerated. By mid-2001, I had lost half of my investment in the stock. I continued to ride the rollercoaster all the way to the bottom.

Figure I.1Price Chart of Corning

My Oplink stock fared worse. I bought at the IPO, thinking it would double in three months, as Wall Street predicted. It never did. The price of Oplink almost never went above its IPO price. Of course, it, too, fluctuated and gave me hope.

It was painful to look at the balance of my brokerage account, so I stopped checking. Instead, I started reading Peter Lynch's Beating the Street.1 I gradually realized that those fiber optics stocks were terrible investments for me to make, so in the fourth quarter of 2002, I threw in the towel and sold everything at more than a 90 percent loss—right when the prices bottomed and they actually became much better investments, as I will explain in Chapter 2.

It took some 15 years for the Nasdaq index to return to where it had been at its 2000 peak. As of June 2016, and even after so many years, the Dow Jones U.S. Telecommunications Index is just above 50 percent of its 2000 apex.

An industry went from boom to bust. A bubble burst. As I would later learn, this kind of boom–bust cycle has been repeated many times throughout history.

The Bubbles

In his book, A Short History of Financial Euphoria,2 economics professor John Kenneth Galbraith discusses all the speculative bubbles since the early 1600s. He argues that financial memory is “notoriously short” and defines bubbles as created by human speculation when there is something new and there is an abundant amount of money from leverage.

Mark Twain said: “History does not repeat itself, but it rhymes.” It turns out that the fiber optics bubble was just another “rhyme” of bubbles that have come before.

The first recorded economic bubble was the Dutch tulip mania in the late 1630s. At its peak, any tulip bulb could fetch a price equivalent to many years of earnings of a skilled worker. People were selling land and houses to speculate in the tulip market. Another phenomenal historical bubble involves the stock of the South Sea Company. The company was established in the early eighteenth century and was granted a monopoly on trade in South Sea in exchange for assuming England's war debt. Investors loved the appeal of the monopoly, and the company's stock price began to rise. Just as with any bubble, high prices drove the price ever higher, and even Sir Isaac Newton wasn't immune to the speculation. In 1720, Newton invested a meager sum in South Sea; a few months later, he had tripled his investment and therefore sold his position. But the stock price continued to rise at an even faster pace. Newton came to regret the sale as he watched his friends quickly become rich, so he went all-in at three times the price he had sold for. The price did continue to increase for a time, but then it collapsed. Newton sold his position at a great loss at the end of 1720. The entire drama had lasted less than a year, and Newton lost £20,000, which constituted his life savings.

Even Newton, one of the smartest people in all of history, couldn't escape the destruction caused by the bubble. He created the entire theory of classical physics with the inspiration of being hit on the head by an apple, but he couldn't overcome the emotions of greed and fear. He later wrote: “I can calculate the movement of stars, but not the madness of men.”3

It was amusing to learn that the founding father of the field of my academic study had lost so much money in a stock bubble, just like me. Not that it made me feel any better.

The fiber optics bubble was like all past bubbles in terms of the associated greed for something new and the abundance of money and leverage. As in prior bubbles, speculation soared as a result of the Internet explosion, which made people expect that the demand for fiber optics networks would also explode and thus a significant amount of money could be made building fiber optical networks. Companies like WorldCom and Global Crossing were borrowing money to build optical networks and were laying fiber everywhere, which inflated the demand for optical network equipment. For equipment suppliers like Nortel and Alcatel, and my former employer, business was booming. They invested heavily in product development and manufacturing capacities, which further drove the demand for optical components. As a result, hundreds of optical component companies popped up in Silicon Valley.

Funds were unlimited. A PowerPoint presentation could land you tens of millions in investment dollars and get your startup going. When I attended the Optical Fiber Communication Conference in early 2001, mountains of free pens greeted me. You could grab as many as you wanted! Companies were giving out all kinds of fancy toys to anyone who passed their booth. This was in March 2001. The Nasdaq index had already lost more than 60 percent from its peak a year before, but the fiber optics companies were still going crazy.

Unlike the dot-com companies that had no revenue, fiber optics companies did. Oplink had $131 million in revenue for 2001, although it lost $25 million on that. But the demand for bandwidth didn't grow fast enough. The overinvestment and the innovations in telecom technology by people like me created far more capacity than the Internet traffic needed. The overcapacity and overbuilt infrastructure drove the cost of data transmission dramatically lower. We could now squeeze much more capacity into a single fiber, and there were too many fibers. The price of data traffic collapsed—97 percent of the fiber laid was dark. WorldCom and Global Crossing found that they couldn't service their debt and were forced into bankruptcy. The bottom fell out of the entire industry. By 2002, Oplink's revenue had dropped to $37 million, and $75 million was lost on that. My former employer lost more than 80 percent of its own revenue, and in the years that followed, many of the telecom equipment companies went belly up. The industry never recovered, much like the tulip bulb market.

You would think that humankind would learn from past bubbles, but the creation of bubbles never stopped. There are four recurring types of participants during the expansion phase of bubbles:

The average folks: These are the people who are excited about the new idea and are also relatively new to the market. They think they are onto something and because their friends and neighbors are getting rich, they, too, should jump in. I was one of them. So was Sir Isaac Newton. Widely recognized as the smartest person alive during his time, Newton was just an average guy when it came to the stock market.

The smart ones: These are the people who recognize that something is wrong, yet think they can figure out when the bubble will burst—they will ride all the way to the peak, but get out before everyone else. As Warren Buffett joked in his 2007 shareholder letter, after the burst of the dot-com bubble in the early 2000s, Silicon Valley had a popular bumper sticker that read: Please, God, Just One More Bubble. Before long, they got one. This time in housing, and we all know how that ended.4

The short sellers: These are the people who recognize that things are wrong and that what is happening is not sustainable. Stocks are overpriced. So they short the stocks by borrowing the shares and selling them, hoping to buy the shares back at a much lower price or not to buy back at all if the company goes bankrupt. But then their pain begins. The stocks continue to go up and short sellers are losing more and more money. Just as economist John Keynes pointed out, “Markets can remain irrational a lot longer than you and I can remain solvent.” This happened to one of the most celebrated investors, George Soros, the man who broke the Bank of England. During the beginning of 1999, Soros's fund was betting big against Internet stocks. He saw the bubble taking shape and knew that the Internet craze would end badly. But as the craze kept gathering force, his fund lost 20 percent by the middle of 1999. Though he knew that the Internet bubble would burst, he bought the borrowed shares back and closed his short positions. That wasn't enough. Under performance pressure, he turned against what he knew—which was the right thing to do—and became the next type of bubble participant: the forced buyer.

The forced buyers: These are the professional investors who are forced to participate in a bubble, mostly under pressure to deliver short-term gains. Not getting involved in the Next Big Thing would make them look outdated, and they face losing jobs or clients. After closing his short positions in Internet stocks, and feeling he couldn't buy those stocks himself, George Soros hired someone to do it for him. His portfolio was then filled with the Internet stocks he hated. Not only that, but the new guy was now selling short the old-economy stocks. It worked. By the end of 1999, Soros saw his fund come all the way back to finish 1999 up 35 percent. The problem was that in another few months, Soros's prediction of the burst of the Internet bubble came true, and he found himself turned in the wrong direction again.

Those people who recognized the bubble and decided to stay out and instead wait for opportunities were (and are) the truly smart investors. But their lives weren't necessarily any easier, especially if they were managing someone else's money. Warren Buffett was considered “to have lost his magic touch.”5 Hedge fund legend Julian Robertson saw his fund in a downward spiral as investors withdrew in response to his shunning of Internet stocks; he closed his fund just as the bubble started to burst. Donald Yacktman, one of the most rational value investors, lost more than 90 percent of the fund's assets to redemptions. The fund's board of directors wanted him out, and only a proxy fight helped him remain in the fund that bears his name. Steven Romick, the excellent young manager of FPA Crescent Fund, was luckier. Though 85 percent of the fund was redeemed, the remaining 15 percent of shareholders “forgot they had invested in the fund,” he assumed, and he kept his job.6

Those who stick to what they believe through the tough times are my true investment Gurus. In the years that followed the Internet and fiber optics bubbles, I read everything these stock market masters wrote. Their teachings have completely changed the way I think about business and investing and have made me a better investor.

GuruFocus.com

I don't recall how I found out about Peter Lynch, but it was through Lynch's books7 that I learned about Warren Buffett and his mentor, Ben Graham. I then read all of Buffett's shareholder and partnership letters from the past 40 years. Upon finishing these letters, I was exhausted. I felt like a hungry man who had enjoyed the first complete meal of his life. I thought, This is the right way to invest!

I realized that successful investing is about knowledge and hard work. It is a lifelong learning process—there is no other secret. Only through learning can you build confidence in your investment decision making. Knowledge and confidence help you to think rationally and independently, especially during market panics and euphoria—when rational and independent thinking is most needed. The good news is that if you learn, you will get better.

I started GuruFocus during the Christmas holiday of 2004 to share what I'd learned. Over the course of its existence, I have probably learned more from GuruFocus users than they have from me. I cannot sufficiently describe my enjoyment. I certainly worked hard. I would get up at 4 a.m., after only three hours of sleep, work four hours until 8 a.m., eat some breakfast, then go to my full-time job in fiber optics. I would come back home at 6 p.m. and immediately go back to work on GuruFocus. I loved weekends and holidays because I could work without stopping.

In 2007, I quit my full-time job and put all my time and effort into the website. I also gradually built a team of software developers, editors, and data analysts to work on GuruFocus. We developed many screening tools and added a lot of data in the areas of Guru portfolios, insiders, industry profile, and company financials. I built these screeners and valuation tools initially for my own investing. We continue to improve them in response to feedback from our knowledgeable users. These tools are now the only ones I use in my investment decision-making process.

In the meantime, I continue to invest in the stock market with my own money, making mistakes and learning from them along the way. I believe that I have become a much better investor. I feel that I have many lessons and much experience to share with my children; I hope that they don't make similar mistakes. Though they may not work in the investing field in the future, I want to guide them in the right direction when managing their own money—which is why I wrote this book. I hope that even people without much prior knowledge in investing can benefit from it.

This book is divided into three sections. The first focuses on where to find the companies that may generate higher returns with smaller risk. The second deals with how to evaluate these companies, how to find possible problems with them, and how to avoid mistakes. The third further discusses stock valuations, general market valuations, and returns. Many easy-to-follow case studies and real examples are used throughout the book.