CHAPTER 4

Again, Buy Only Good Companies—and Know Where to Find Them

“Keep it simple.”

—Charlie Munger

I reiterate the title from Chapter 3 because if there is one thing you should remember from reading this book, it is to buy only good companies!

It isn't that other companies won't make you money. They may make you a lot of money. Donald Yacktman didn't buy Chrysler because the auto industry was not the place he wanted to be, not because Chrysler wouldn't make him money. If you buy only good companies, your chance of making money is much improved and the journey is far more pleasant.

Peter Lynch can make money anywhere; he knows about every industry and how to succeed in every investing situation, and he owns thousands of stocks. But you don't have to be like Lynch; as Charlie Munger said: “You don't have to know everything. A few really big ideas carry most of the freight.”1

A woman calls in a plumber when her washing machine breaks down. The plumber arrives, studies the machine, then takes out a hammer and gives it a hefty whack. The washing machine starts working again, and the plumber presents her with a bill for $200. “Two hundred dollars?” says the woman. “All you did was hit it with the hammer.” So, the plumber presents her with an itemized bill: Hitting washing machine with a hammer: $5. Knowing where to hit it: $195.

This joke has been used in many situations to enlighten people on how, and where, to focus their effort. When it comes to investing, buy only good companies! The advice seems simple, but it is not always easy to follow—numerous opportunities in the market pose appealing gains.

As mentioned in Chapter 1, Lynch categorized investment opportunities into six classes.2 I will examine them all and demonstrate whether the idea of buying only good companies applies to each.

Asset Plays

An asset play is the situation that occurs when a company is sitting on something valuable, but this is not reflected in its stock price. These days, the valuable assets are often understated real estate. This refers to the deep-bargain investing where the stock price is much lower compared to the asset value, net current asset value, or net-net working capital of the business, as I examined in Chapter 2. Unless the situation is extremely liquid and takes a short time to liquidate, or the business itself is decent and generates enough cash flow to be self-sustaining, investors should avoid investing in asset plays altogether.

Warren Buffett calls it “foolish.” Yacktman likens it to a factory that is idle but the machines can be cheaply bought. Remember Sears? As this writing progresses, Sears is still “unlocking value.” But, “It's taking much longer than we thought,” as Bruce Berkowitz admitted in his 2016 semiannual shareholder letter,3 published July 28, 2016, and which can be translated into “It is eroding more value than we thought.” Avoid asset plays.

Turnarounds

Turnarounds are the companies that “have been battered, depressed and often can barely drag themselves into Chapter 11.”4 Lynch made many multibaggers from turnarounds. Above all, the stock price was usually badly beaten down and the recovery could be strong from the rock-bottom levels. But Lynch also has a long list of turnarounds he wishes he'd never bought.

Avoid investing in turnarounds. The mere fact that the company could get itself into trouble precludes it from qualifying as a good company. And these problems rarely go away, as Buffett wrote in his 1979 shareholder letter, suffering from the pain of trying to turn the embattled textile business around:

We witnessed a high-profile turnaround effort at JC Penney a few years ago. Under the direction of corporate raider and activist investor Bill Ackman, former Apple store genius Ron Johnson was brought in to turn the business around. But Johnson couldn't replicate the magic he performed at Apple, and the turnaround effort failed spectacularly. Ackman lost 60 percent on his billion-dollar investment in JC Penney and gave up.

Still struggling to turn the textile business around, Buffett wrote in his 1980 shareholder letter:6

That is exactly what happened to the reputation of Ron Johnson, who succeeded at Apple but not at JC Penney. Above all, Apple is Apple—and JC Penney is just JC Penney.

But didn't Buffett make a killing with the turnaround of GEICO? He paid $45.7 million in 1976–1979 for one-third of the company, which was eventually worth $2.3 billion when he acquired the remaining shares of GEICO. In the early 1970s, the executives running GEICO made some serious errors in estimating their claims costs, a mistake that led the company to underprice its policies, which almost caused it to go bankrupt.

Though in trouble, GEICO's fundamental competitive strength was unchanged, according to Buffett, and is the reason he bought GEICO. He explained in his 1980 letter:7

Therefore, the most important test to distinguish a true “turnaround” from the “localized excisable cancer” is if the business still has the “fundamental competitive strength” and “exceptional underlying economics” it once enjoyed. If we apply this to Sears and JC Penney, we can clearly see that they don't. So much for their turnarounds.

Investors should also distinguish a market manipulation from a true turnaround, as both can result in the collapse of stock prices. This happened to Fairfax Financial, a Canadian insurance company founded by value investor Prem Watsa, who got into the insurance business under the influence of Buffett. Watsa became a successful value investor after studying Benjamin Graham and John Templeton. Under his leadership, Fairfax had grown its book value by more than 20 percent a year since 1985. In 2004–2005, Fairfax was traded in both the United States and Canada at around $200 a share, when it became the target of influential short sellers. Fairfax was compared to the infamous accounting manipulator and then-bankrupt company Enron. Fairfax stock lost 50 percent of its market value and dropped to $100 a share. Fairfax then sued the short sellers and withdrew its stock from trading in the U.S. market. The dust finally settled and Fairfax continued to grow its book value at a 20 percent annual rate, and it made a killing during the financial crisis in 2008 by shorting the stock market. Now Fairfax is traded at around $700 as of October 2016.

Fairfax's trouble came from stock manipulations. The short sellers' attacks damaged its reputation, which may have temporarily affected its insurance business. But its business was doing fine, and the short sellers in fact created a great buying opportunity for long-term investors.

In conclusion, turnarounds seldom turn and shouldn't be considered good companies. An investor can, however, find many good opportunities; the key is to identify the companies that are in trouble but still have “fundamental competitive strength” and “exceptional underlying economics.” Avoid true turnarounds!

Cyclicals

A cyclical business sees the demand for its products expand and contract periodically every several years. The demand is often synchronized with the economic cycle. The business usually requires high capital investment and heavy fixed assets. Its production capacity cannot expand quickly when demand is high and cannot be eliminated when demand is low. The business tends to invest to expand its production capacity when demand is strong, but when the production capacity is ready, the demand has already dwindled, resulting in a dramatic decline in profit and heavy debt.

Highly cyclical industries include auto, airline, steel, oil and gas, chemicals, and many others. Sometimes a cyclical business can ride on a tailwind and expand for many years, disguising it as secular growth. For instance, the housing industry, which was driven by declining interest rates, expanded almost ten years before its collapse.

Cyclical industries are not the places in which to find good companies for a long-term hold. Yacktman didn't want to buy Chrysler because the auto industry is too cyclical. Investors should also stay away from cyclical industries.

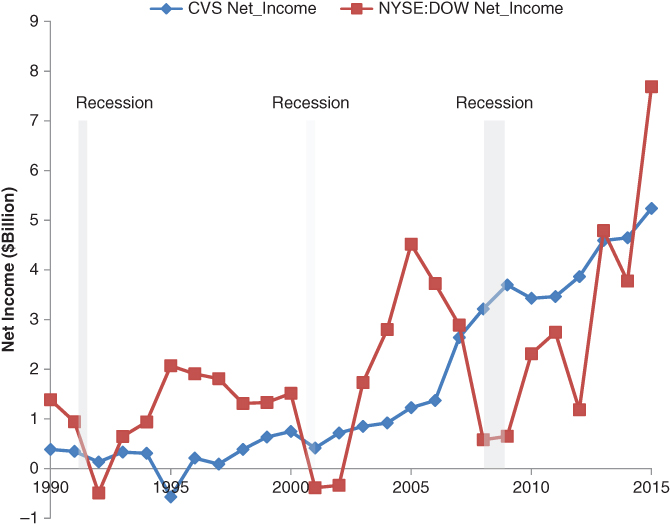

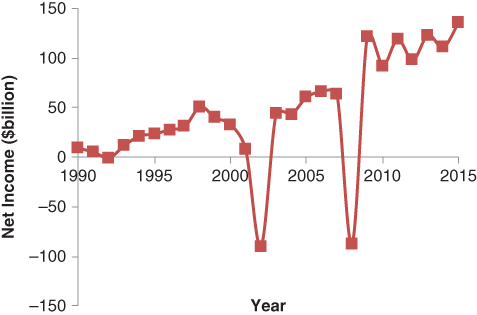

Although Howard Marks said, “most things will prove to be cyclical,”8 some industries are definitely more cyclical than others. A way to identify a cyclical industry is to see how its sales and profit did over at least ten years, and especially during recessions. An example is reflected in Figure 4.1.

Figure 4.1 CVS DOW Net Income

This chart shows the net income of CVS Health Corp. and Dow Chemical. The gray areas in the chart denote the periods in which the U.S. economy was in recession. Dow Chemical's net income dropped drastically during these recessions. In the 2002 recession, Dow Chemical fell into loss; in the 2008 recession, its net income dropped from above $4 billion a year to less than $1 billion—meanwhile, CVS's net income was barely affected by the recessions.

Clearly Dow Chemical is a cyclical business while CVS is not. Holding cyclicals long term is not very rewarding. Holding leveraged cyclicals can be extremely dangerous. Many cyclicals can't outlast recessions, and they go bankrupt. Think of how many bankruptcies we have heard about for carmakers, airlines, mining companies, and oil explorers. By definition, they cannot meet the requirement of long-term and consistent profitability that we have established for good companies. Avoid cyclicals.

Slow Growers

Slow growers are mature companies that have lost their growth steam. Their revenue base is too expansive for them to find new markets for growth. Therefore, their revenue is not growing much faster than the economy. Think of Wal-Mart, Microsoft, Procter & Gamble, and Johnson & Johnson. These companies are usually hugely profitable and have high returns. For the three questions on profitability, return on invested capital, and growth we ask about good companies in the last chapter, we have acceptable answers for Question 1 (long-term, consistent profitability) and Question 2 (high return on invested capital), but not for Question 3 (double-digit growth).

The investment returns from the stock of slow growers can be satisfactory if bought at lower valuations relative to their historical mean. Slow growers are a good choice for steady and high dividends when building an income portfolio. I will discuss more about this in Chapter 8.

The Stalwarts

The stalwarts are typically midsized companies that are growing at a low double-digit rate and still have exceptional potential ahead of them. They represent the ideal field in which to find good companies that have long-term profitability, high return, and double-digit growth. The companies are growing at decent rates and have proven track records. Holding these stocks can be unexciting, but holding high-quality companies over the long term has little investment risk, which can be very rewarding.

A stalwart company may grow slower in one year and faster in another. We look at the long-term average of the business performance in the areas of growth, profitability, and business returns. We need to analyze what caused the company to grow slower than in the past and see if the slower growth will become the norm for the future. Sometimes industry transformation destroys the economic moat the business once enjoyed, or the business itself deviates from its past track under existing or new management. Investors need to continue to watch the growth and profitability of these companies. No business is perfect or hiccup-free.

I have created a good companies screen in GuruFocus's All-In-One Screener for readers to find these companies. Simply go to GuruFocus.com → All-In-One Screener → GuruFocus Screens → The Good Companies. I have also created a portfolio that monitors the performance of the stocks that appear on the screener as of August 2016.

With this screener, we find companies such as AutoZone, AMETEK Inc., and Jack Henry & Associates Inc. These are steady and profitable growers with high return on invested capital and the potential for more growth. Their stocks also did extremely well during the past decade.

Lynch sells the stalwarts after a gain of 50 percent in a year or two. But they can also be long-term steady growers. It is often worthwhile to hold them for the long term, as selling will result in capital gain tax and missed opportunities to buy these high-quality companies again. Consider AutoZone. There has never been a good time to sell AutoZone. The company has been growing its revenue at about 15 percent a year, year in and year out, and even during recessions. Holding it for the long term has been extremely rewarding.

Fast Growers

Fast growers are the companies that grow at above 20 percent. They are usually small and aggressive new companies. This is Lynch's favorite land, where he found many ideas that eventually gained 10 times, 20 times, and more.

As Lynch pointed out, the fast growers don't have to be in a fast-growing industry. Ideally, they are the companies that grab market shares from existing players. While the reward can be great, the risk in investing in fast growers can also be high. The fast growers may grow too fast and get into too much debt. The high expectations of Wall Street usually elevate their valuations to fragile levels. Any hiccup in growth will result in severe punishment to their stocks.

Enter Chipotle Mexican Grill. The fast-food chain grew its revenue by more than 20 percent per year on average for the past decade. Its stock was trading at P/E of above 50 in 2014, as the company seemed unstoppable, opening more stores and enjoying double-digit same-store sales growth. Then, in 2015 the restaurant chain was hit by a virus and facing federal investigation. The same-store sales are now in decline, and the stock has lost close to 50 percent from its peak in 2015.

It is hard to find good companies that have proven themselves over the long term in the land of fast growers, as these companies usually don't have enough history. Some of them, however, over time can develop into the good companies we are looking for.

In summary, as investors are looking to buy only good companies, we will not consider asset plays, cyclicals, and turnarounds from among Lynch's six categories. We may barely find qualified companies among slow growers and fast growers—the best ones are the stalwarts. The stalwarts are more likely to meet the good companies' requirements. Again, these requirements are:

- Long-term and consistent profitability

- High business returns as measured by high return on invested capital and high return on equity

- Above-average growth

If you are a plumber, know where to hit.

The Cyclicity of Businesses

The cyclicity of businesses deserves further consideration. It is one of the first things Yacktman looks at in a business. He prefers businesses with a long product cycle and short consumer purchase cycle, which means businesses that are not cyclical. As pointed out by Marks, most things are cyclical, as illustrated in the net income of different sectors in the following. At the bottoms of the cycles, demand for the products slows. A small decline in sales can translate into huge drops in the profits of the business because the cost cannot be reduced as quickly as the demand, and the reduction of the cost itself costs money.

Because of the nature of business, some industries can never produce consistently good returns for their shareholders. Buying good companies means avoiding these industries altogether. I have mentioned cyclical industries such as autos, airlines, chemicals, steel, and energy. I now want to examine in further detail the cyclicity of certain businesses.

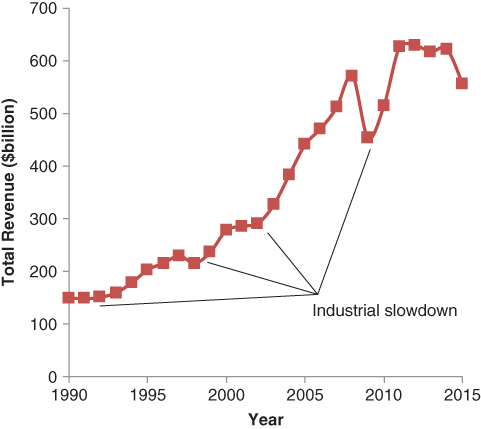

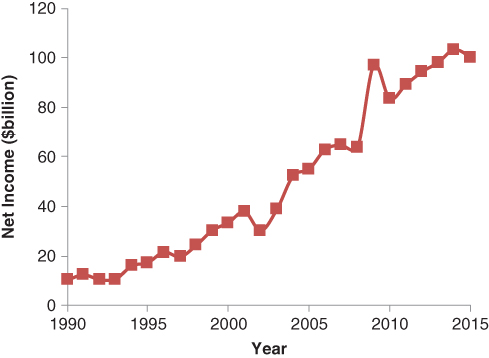

The basic materials sector is one of those. Figure 4.2 illustrates the history of the total revenue of the 732 U.S. companies that are currently traded in the basic materials sector. These include companies in the industries of agriculture, building materials, chemicals, coal, forest products, metals, and mining.

Figure 4.2 Basic Materials Revenue

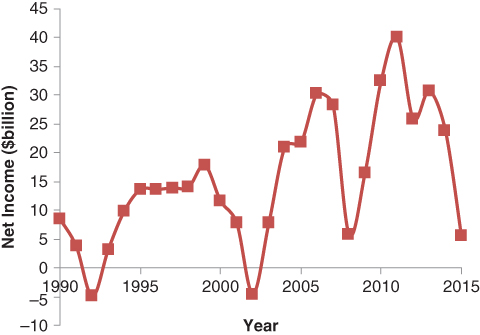

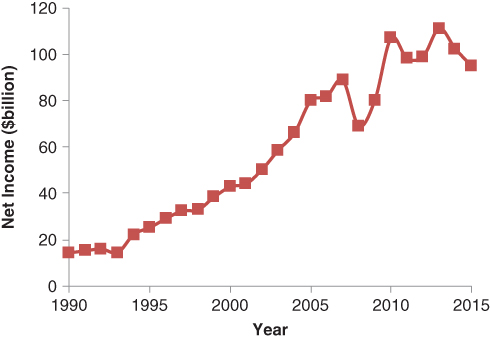

We can see that during the years 1992, 1998, 2002, 2008, and 2015, the revenue for basic materials declined. Among those years, 1992, 2002, and 2008 are associated with recessions. The total revenue of these companies shrank from previous years by a few percent most of the time because even in the good years, 1999, 2006, and 2010, the sector had an average profit margin of just above 6 percent. The insignificant few percent of decline in revenue resulted in dramatic collapses in the total profit of the sector, as is evident in Figure 4.3.

Figure 4.3 Basic Materials Net Income

During the years 1992 and 2002, the basic materials sector fell into deep loss. In the years 2008 and 2015, the sector gave up more than 80 percent of profits in relation to previous years and was barely profitable as a whole. The capital- and asset-intensive nature of the sector makes it hard to quickly adjust cost as demand slows. The products in the business are usually commodities, making it hard for businesses to raise prices to compensate for the loss in demand. These factors make the basic materials businesses highly cyclical.

Shareholders in this sector usually find that their companies swing wildly between profit and loss every several years. Many companies cannot pass the test of bad times and go bankrupt. As Buffett said, “In a business selling a commodity-type product, it's impossible to be a lot smarter than your dumbest competitor.”9 So companies must compete on prices, and they have similar patterns of profit and loss. They just cannot generate consistent earnings over a long period.

Therefore, companies producing agricultural products, building materials, chemicals, coal, forest products, and metals are not good businesses. Lynch once said that companies selling commodity-like products should come with a warning label: “Competition may prove hazardous to human wealth.” Avoid them!

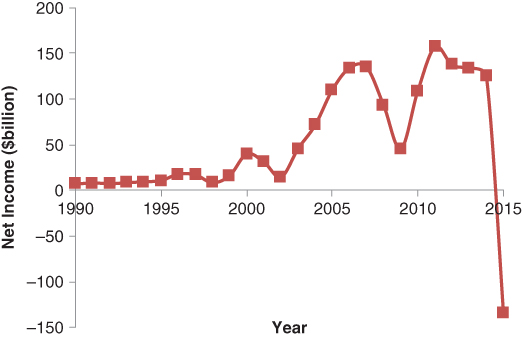

Similar behavior is observed in the energy and consumer cyclical sectors. Their profits are reflected in Figures 4.4 and 4.5. As we can see, the consumer cyclicals sector is indeed cyclical. This sector includes industries such as auto, entertainment, manufacturing, travel and leisure, and luxury goods. These always experience deep losses during recessions. It is hard to build consistently profitable companies in these industries.

Figure 4.4 Energy Net Income

Figure 4.5 Consumer Cyclical Net Income

For the technology sector, the behaviors of hardware and software businesses are quite different. The hardware producers, such as telecom equipment and computer companies, are more asset-heavy and capital-intensive. Thus, these are more susceptible to economic cycles. Because of the continuous changes in technology, it is difficult for a hardware business to stay competitive over the long term.

But some software companies have developed products and services in areas that don't change as fast. For example, Microsoft and Google have built their economic moats and have become great companies with consistent earnings power and a high return on invested capital and growth. A company called Ansys Inc. makes simulation software that is widely used in industries from aerospace, defense, auto, and construction to healthcare, energy, and almost everything else. The software needs to be tested and verified repeatedly in the real production world. Once the software is found reliable, no customer will want to risk changing to new software from another company; thus, Ansys has established its moat.

Banking didn't display much sensitivity to cycles and recessions for almost two decades as the industry rode on the tailwind of housing expansion, until the housing crisis started in 2007. A bank can be a simple business like a small community bank focusing on conservative home mortgages; it can also be a complex business with who knows what on its book. Buffett didn't like banks in general. He didn't buy bank stocks until 1990, when he bought Wells Fargo. He wrote in his 1990 shareholder letter:10

This is exactly what led Citigroup into trouble under its former CEO Charles Prince, who famously said about Citigroup's continued commitment to leveraged buyout deals, despite fears of reduced liquidity because of the subprime meltdown: “As long as the music is playing, you've got to get up and dance.”

I once heard this joke:

During the housing craze of the 2000s, most bankers just remembered the third rule.

Buffett considers management the key to a bank. He continued in his 1990 letter:

This is also what Munger echoed in the 2016 shareholder meeting of Daily Journal Inc., for which he serves as chairman:11

Lynch loves community banks and savings and loans. The business for these small banks is much simpler and conservative bankers can be found within them.

Healthcare and consumer defensive sectors are relatively insensitive to economic cycles. After all, people still go to doctors when they get sick. The consumer defensive sectors include food, drinks, tobaccos, and other low-priced, daily-consumed products. Consumers are not sensitive to the price changes of these products and cannot withhold their purchases even if the prices increase, which gives the pricing power to the companies. These are the products that are consumed daily and therefore have a short consumer purchase cycle, as preferred by Yacktman. On the other hand, the products are usually simple and have a very long life cycle. For example, since Berkshire Hathaway purchased See's Candy in 1972, the company has been making the same kinds of candies. Therefore, the required invested capital is light. This is a field in which many great businesses are built. We as investors can participate in the growth of these businesses and can be rewarded by buying their stocks and holding them for the long term. (See Figures 4.6 and 4.7.)

Figure 4.6 Healthcare Net Income

Figure 4.7 Consumer Defensive Net Income

This is also what renowned value investor Tom Russo has been doing for more than three decades. He put more than 60 percent of his portfolio into food and drink companies like Nestle, Heineken, Anheuser-Busch, and Pernod Ricard, and cigarette companies such as Philip Morris International and its sister company Altria. Buying these high-return and consistently profitable companies bears little risk and imposes no need to sell. His quarterly portfolio turnover is less than 2 percent, and he has achieved an excellent long-term track record.

Investors need to be wary of retailing businesses, though they belong to consumer defensive. This is what Buffett wrote about retailing in his 1995 shareholder letter:12

In summary, the dedication to buy only good companies means that investors should avoid the companies in the highly cyclical sectors such as basic materials, computer hardware, telecom, and semiconductor companies, no matter how attractive the opportunities appear. The nature of these businesses is simply prohibitive for anyone to build consistently profitable companies. The sectors of consumer defensive and healthcare are almost noncyclical. They represent better places to find great companies with high returns and consistent profitability.

Shooting for the Stars versus Shooting Fish in a Barrel

Sticking to buying good companies also means that we are going to miss some of the best-performing stocks. When I sort the 3,577 companies that were continuously trading for the past ten years by their performances, the best-performing 50 stocks delivered an annualized gain of just under 25 percent or higher. Among the 50 stocks, 6 were in biotech and 5 were in software. These two industries produced most of the star performers in the past ten years. We are not likely to catch any of them because we choose to invest in good companies with great long-term performance records. None of these companies qualified as a good company ten years ago. Even today, very few of them qualify.

Let's first look at the star performers in the biotech industry. The best-performing stock is Medivation Inc. It gained an average of almost 50 percent a year over the past ten years. Ten years ago, the company had no revenue and was losing tens of millions a year. The market cap was already more than $100 million. Why would the market value a company with no revenue at hundreds of millions of dollars? Any sensible investor would not buy the stock. The company went another year without revenue while its market cap grew to more than $400 million. The company did make it, and now it has close to $1 billion in annual revenue and more than $250 million in net income. But it didn't turn a profit until 2014, when its market cap had grown to more than $7 billion. Today the market values the company at more than $10 billion.

How could anyone have spotted such an opportunity ten years ago? How could anyone foresee that the company could grow from no revenue to close $1 billion in ten years? Even with deep knowledge and industry insight, it seems impossible to do. Searching for such an opportunity ten years ago was indeed like shooting for the stars.

Now let's take a look at the second-best biotech stock, BioSpecifics Technologies Corp. Over the past ten years, the company's stock gained 43 percent a year annualized. A decade ago, the company had a tiny market cap of about $5 million. Its revenue shrank from $5.5 million in 2005 to $1.9 million in 2006 and was losing $3.3 million on that. Even today the revenue of the company is a mere $23 million a year. It is making a net profit of $10 million. The market cap is now $284 million. While the gain is attractive, a market cap of only $5 million ten years ago is too small for even many individual investors, and the company was in deep loss in its operations.

In the software industry, the two best-performing stocks were EBIX Inc. and Tyler Technologies. EBIX, an insurance software provider, delivered an average gain of 40 percent. Tyler provides management software for local governments and gained 30 percent a year for the past ten years. EBIX had revenue of under $30 million while Tyler had less than $200 million. They would not be considered good companies in 2006 because both only recently turned profitable. They could not pass the test of long-term consistent profitability found in good companies.

We would also miss other best-performing stocks of the past decade like Amazon.com, Apple, and Priceline for the same reasons. These companies haven't proven themselves for consistent profitability. Does it sound terrible? No, because we also have dodged a much higher probability of loss with many other companies.

Let's consider all the biotech stocks that were traded in the market in 2006. At the beginning of 2006, there were 210 U.S.-based biotech companies that had less than $100 million in annual sales. This includes companies that were later delisted for being acquired or going bankrupt. Sixty-seven, or 32 percent, of these companies went bankrupt in the following years. Another 40 percent of the stocks are still negative, even after a holding period of ten years. These 210 companies have a median gain of negative 80 percent. If we consider the 90 companies that had sales profiles similar to the star performers, such as Medivation and BioSpecifics, 70 percent later went bankrupt; 87 percent of the stocks lost more than 90 percent.

The software industry did somewhat better, although the odds of picking losers still ran extremely high. Among all 357 U.S.-based software companies that had less than $100 million in revenue and were traded in 2006, around 20 percent went bankrupt later. Investors are still losing money—more than 57 percent of them, even after a holding period of ten years. These 357 companies had a median gain of negative 28 percent. What is the chance of picking the star performers among these companies? If you didn't pick the winners, the losers cost you big.

If we look at the companies that would qualify as good companies in 2006, they would have been profitable over the previous ten years and have had a median return on invested capital of more than 20 percent. We found 205 companies at the beginning of 2006. If we held them for ten years, 5 percent of them went bankrupt later. We would have lost money on 31 percent of the companies after ten years. These 205 companies have a much higher median gain of 34 percent. Overall, the chance of losing money is much smaller.

If betting on picking the best performers is like shooting for the stars, buying good companies at fair prices is like shooting fish in a barrel. You may not get the star performers, but you get a lot of decent ones such as retail chain Dollar Tree and baking soda and condom maker Church & Dwight. More importantly, you avoid a lot of deep losses.

Therefore, by buying only good companies, we are focusing on a much better neighborhood of the investing universe. We are trying to eliminate the chance of losing money by buying those that have already proven themselves. We have a much smaller universe than Lynch in picking stocks. We want to stay in the proximity of good companies. We don't want to get into situations where we have high odds of losing money.

Didn't Munger once say: “All I want to know is where I'm going to die so I'll never go there”?

I want to finish this chapter with the wisdom of Buffett:13