CHAPTER 2

Deep-Value Investing and Its Inherent Problems

“Don't let the tall weeds cast a shadow on the beautiful flowers in your garden.”

—Steve Maraboli1

After the bursting of the tech bubble, many of the once high-flying tech stocks were sold off without regard to the price. By October 2002, the stock of Oplink, the fiber optics company I'd bought, dropped from its two-year-prior price of $250 to $4.5 a share (split adjusted). Concurrently, the company had the net cash per share of over $8, which means that if the company had ceased its operations, eliminated all its other assets, and distributed the cash to its shareholders, these shareholders would have almost immediately doubled their money. Therefore, at some point, even an originally poor investment can become a pretty good one if the price is right.

This is an example of deep-value investing, a strategy that focuses on buying the stocks of the company at a deep discount against the value of its assets. The approach was theorized by the founding father of value investing and the mentor of Warren Buffett, Benjamin Graham.2

Deep-Value Investing

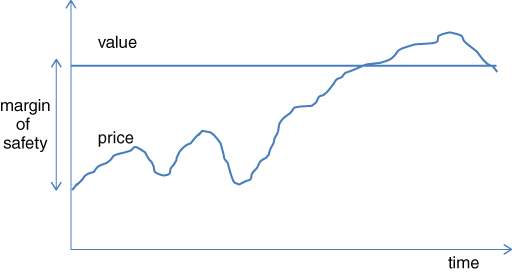

The idea of deep-value investing is straightforward; it is simply “buying dollar bills for 40 cents,” as explained by Buffett, who in his early years experienced tremendous success practicing deep-value investing.3 Deep-value investors try to buy the stock of a company for a price that is discounted from the assessed value of the assets, then wait for the gap between the price and the value to close. Deep-value investors require a minimum gap between the price and the assessed value in order to buy. This minimum gap is called the margin of safety, which is important to protect investors from errors occurring during the assessment of the value.

The idea is illustrated in Figure 2.1.

Figure 2.1 Value Investing and Margin of Safety

Over time, the gap between the price and the value may shrink, and deep-value investors can profit from selling the stock at a higher price, which might be closer to the value of the stock.

Benjamin Graham and Walter Schloss were deep-value investors.4 Graham said in his classic book, The Intelligent Investor, that to avoid errors and ignorance, it is safer to have a diversified portfolio, which may consist of more than a hundred companies.5 In assessing what the stock is worth, or its value, deep-value investors focus on the balance sheet of the company and have no interest in its operations. There are four ways to estimate the company's value, depending on how conservatively investors want to go with the valuation.

Tangible Book Value

In this approach, the company is only worth the value of its tangible assets, such as cash, receivables, inventories, buildings, and equipment after paying all the debt and other liabilities. Its intangible assets, such as goodwill, patents, trademarks, brands, and business operations are considered worth nothing. Therefore, the value of per share is calculated as:

This approach is seemingly a conservative way of estimating a company's value, but the investor can go even more conservatively.

Net Current Asset Value

To be more conservative and careful in the valuation, we assign no value to the business's long-term assets such as buildings, land, and equipment. Only its current assets are taken into account for the calculation because all the liabilities are actual and must be paid, so the net current asset value (NCAV) of a company is calculated as:

Risk still exists with this approach because not every current asset is worth its listed value. An even more conservative evaluation is the net-net working capital.

Net-Net Working Capital

In this approach, the inventory and the receivables are discounted to their book value and any prepaid expenses are considered worth nothing, but the liabilities are still real. It is defined as:

In the net-net working capital valuation, cash is counted as 100 percent, accounts receivable as 75 percent of book value, and inventories as 50 percent of their value. Everything else is worth nothing and the liabilities are paid in full. This is assuming that in a fire-sale the value of the company is what is left for shareholders.

Net Cash

In the net cash valuation, only the cash and short-term investments of the company are used for the calculation. Everything else is considered worth nothing:

It seems inconceivable that anyone would sell a portion of a company at a price that is far below its liquidation value, but this does happen, especially during market panics. Even as of July 2016, the stock market has reached an all-time high, yet some stocks are still sold at a price far below their liquidation value. In the table below, I list some of them. All numbers are per-share numbers for July 19, 2016.

| Tangible Book Value | NCAV | Net-Net Working Capital | Net-Cash | Price | |

| Emerson Radio Corp. | $ 1.99 | $ 1.93 | $ 1.75 | $ 1.75 | $ 0.68 |

| Adverum Biotechnologies Inc. | $ 8.92 | $ 8.78 | $ 8.73 | $ 8.70 | $ 3.07 |

| Carbylan Therapeutics Inc. | $ 1.64 | $ 1.63 | $ 1.59 | $ 1.59 | $ 0.59 |

The numbers are decreasing from tangible book to NCAV to net-net working capital to net cash, as they are more conservative in calculation in that order.

These numbers are taken from GuruFocus.com, where you can find all these numbers, for every stock, as both current and historical values. You can also screen stocks that are sold below their liquidation values with GuruFocus's All-In-One Screener6 and Ben Graham's Net-Net Screener.7

It seems obvious that investors are not in a position to lose money if they buy stocks at far below their liquidation values, which is what Graham did. He wrote in The Intelligent Investor:8

He continued:

Graham looked for companies whose market values were less than two-thirds of their net-current-asset values. GuruFocus has created the Graham Bargain Screener to screen for these net-current-asset bargains, which can also be found at: http://www.gurufocus.com/grahamncav.php.

The risk in investing in these companies is that most of them are not well-run and may be continuously losing money. To reduce the risk, GuruFocus added the option that users can filter for companies that have positive operating cash flow. In this way, the companies will likely be able to maintain their operations without burning through their cash.

According to Graham, some of these companies may well become insolvent as economic conditions worsen, so it is important to hold a diversified basket of them.

Though the strategy worked well for Graham, these bargains are no longer around for modern value investors seeking to build a diversified portfolio. During the drastic decline of the stock market in 2008, this screener had a long list, but it has gradually dwindled.

My experience with Ben Graham Net Current Asset Bargains has been mixed. Just as Graham described, when you can locate many of them, the strategy works well. But if you cannot, the ones you do find will likely not bring success.

For instance, following are the top-20 stocks generated by the screener on December 26, 2008. S&P 500 was 872 and had lost more than 40 percent from its peak in 2007. It is, as of this writing, 2163. The performances of the 20 stocks through July 2011 are displayed here:

December 2008 Net-Net Working Capital Portfolio (S&P 500 = 872)

| Symbol | Price on Dec. 26, 2008 | Prices as of July 13, 2011 | Change % | Comment |

| Heelys Inc. | 2.52 | 2.24 | –11% | |

| Valpey Fisher Corp. | 1.45 | 2.7 | 86% | |

| Solta Medical, Inc. | 1.35 | 2.6 | 93% | |

| Emerson Radio Corp. | 0.51 | 1.97 | 286% | |

| Orbotech Ltd. | 4.06 | 12.35 | 204% | |

| Silicon Graphics International Corp. | 3.76 | 15.87 | 322% | |

| NUCRYST Pharmaceuticals Corporation | 0.85 | 1.77 | 108% | Acquired |

| PECO II Inc. | 2.1 | 5.86 | 179% | Acquired |

| Dataram Corp. | 1.15 | 1.59 | 38% | |

| Mattson Technology Inc. | 1.2 | 1.94 | 62% | |

| ACS Motion Control Ltd. | 0.91 | 1.4 | 54% | |

| Avanex Corp. | 1.04 | 3.256 | 213% | Acquired |

| LinkTone | 1.13 | 0.9701 | –14% | |

| PDI Inc. | 3.39 | 7.72 | 128% | |

| Actions Semiconductor Co. Ltd. | 1.6 | 2.15 | 34% | |

| Soapstone Networks Inc. | 2.46 | 0.01 | –100% | |

| Transcept Pharmaceuticals Inc. | 5.45 | 8.59 | 58% | |

| ValueVision Media Inc. | 0.29 | 8.29 | 2759% | |

| Allianz SE | 10.14 | 12.82 | 26% | |

| GSI Group Inc. | 1.65 | 11.99 | 627% | |

| Average | 257.6% |

Among these stocks, a complete loss occurred with only one company, Soapstone Networks Inc. Three companies were acquired at premiums and gains were all more than 100 percent. As a group, these 20 stocks have averaged a gain of 257 percent. By comparison, for the same period, the S&P 500 gained 48.5 percent and the Nasdaq index gained 82 percent. Seventeen of the 20 stocks had positive returns, the greatest being ValueVision Media Inc., which gained more than 2,700 percent over a period of two-and-a-half years. GSI Group Inc. gained more than 600 percent; Silicon Graphics International Corp. gained more than 300 percent; Emerson Radio Corp. gained more than 280 percent. (All numbers exclude dividends.) The net-current-asset value bargains did extremely well, especially during the 12 months when the gain was more than 150 percent.

As the market ticked higher, the number of these bargains decreased. By October 2009, the S&P 500 recovered some of the losses caused by the financial crisis in 2008 and moved back above 1000; we found 12 of these bargains, which are reflected here:

October 2009 Net-Net Working Capital Portfolio (S&P 500 = 1020)

| Company | Price($) |

| The9 Ltd. | 7.57 |

| Orsus Xelent Technologies Inc. | 9.36 |

| Heelys Inc. | 2.15 |

| eLong Inc. | 9.74 |

| TSR Inc. | 4.1 |

| Netlist Inc. | 0.69 |

| Forward Industries Inc. | 1.72 |

| United American Healthcare Corp. | 0.99 |

| Optibase Ltd. | 6.35 |

| magicJack VocalTec Ltd. | 4.88 |

| American Learning Corp. | 0.52 |

| MGT Capital Investments Inc. | 15 |

Following are the performances of the portfolio over the next four years:

| Year | Bargain Portfolio | SP 500 | Nasdaq |

| Oct. 2009–Sept. 2010 | 50.00% | 9.75% | 13.38% |

| Oct. 2010–Sept. 2011 | –17.00% | –1.29% | 1.88% |

| Oct. 2011–Sept. 2012 | –2.00% | 24.68% | 25.69% |

| Oct. 2012–Sept. 2013 | –28.00% | 17.43% | 24.23% |

In the first year, this bargain portfolio delivered a very strong performance and investors would have benefited tremendously from selling it after 12 months, but if the holding time grew longer, the gain would have gradually diminished.

However, as we continued to watch the performance of these net-current-asset bargains, the portfolios we generated after 2011 did not perform well. As a group, they often underperformed the S&P 500 by significant margins.

Listed here is an NCAV bargain portfolio generated in April 2011, when the S&P 500 was above 1300.

April 2011 Net-Net Working Capital Portfolio (S&P 500 = 1332)

| Company | Price($) |

| China TechFaith Wireless Comm Tech Ltd. | 21.6 |

| Blucora Inc. | 8.79 |

| China-biotics Inc. | 8.38 |

| Jiangbo Pharmaceuticals Inc. | 4.43 |

| Noah Education Holdings Ltd. | 2.16 |

| eLong Inc. | 14.25 |

| Gencor Industries Inc. | 7.85 |

| Vicon Industries Inc. | 4.75 |

| TSR Inc. | 4.99 |

| Maxygen Inc. | 5.21 |

| Comarco Inc. | 0.31 |

| Actions Semiconductor Co Ltd. | 2.44 |

| Meade Instruments Corp. | 3.66 |

| BroadVision Inc. | 14.45 |

| Qualstar Corp. | 10.74 |

| Merus Labs International Inc. | 1.62 |

| Peerless Systems Corp. | 3.16 |

| Cytokinetics Inc. | 9.06 |

Reflected here is the performance of April 2011's NCAV bargain portfolio during the 12-month periods afterward:

| Bargain Portfolio April 2011 | Bargain Portfolio | S&P 500 | Nasdaq |

| April 2011–March 2012 | –10% | 7.21% | 12.70% |

| April 2012–March 2013 | –20% | 11.41% | 5.69% |

| April 2013–March 2014 | 11% | 18.38% | 27.18 |

| April 2014–March 2015 | –30% | 10.51% | 18.5 |

This net-assets-bargain portfolio underperformed the indices from the very beginning and would continue to generate deep losses in all the periods following, even as the broad market continued to gain.

As we continued to observe the performance of deep-bargain portfolios, we initially didn't have many to include in the portfolio with enough margin of safety. If we invested in the ones that appeared, the performance was typically poor and significantly lagged the market.

Compared with Graham's time, finding companies that have large displaced prices relative to their liquidation values is much easier due to the advances of technology. As a result, the market is getting crowded and not many deep bargains exist. Especially true in recent years, when the interest rate has been low, the valuations for all assets have been lifted to much higher levels, and it therefore becomes difficult to find deep bargains relative to the net assets on a company's balance sheet.

The best time to invest in these deep bargains is when you can find plenty of them, especially when panic and forced selling are prevalent in the market due to a market crash. During such a period, many stocks that deserve higher valuations are also beaten down on prices, especially those with relatively poor business fundamentals. When the overall market valuation is high and everything else is rising, those dropping and appearing in the deep-bargain screener probably deserved to be traded by low valuations. Their stock prices were likely low for the right reasons, and buying these would likely have resulted in steep losses, as I observed in the years after 2011. Therefore, when it comes to deep-value investing, investors need to be cautious and aware of this approach's inherent problems.

The Problem with Deep-Value Investing

Buffett coined the term “cigar-butt investing” for the strategy of buying mediocre businesses at prices that are much lower than the companies' net-asset values. He said the approach is like “a cigar butt found on the street that has only one puff left in it [and] may not offer much of a smoke, but the ‘bargain purchase’ will make that puff all profit.”9

There are several problems with this approach:

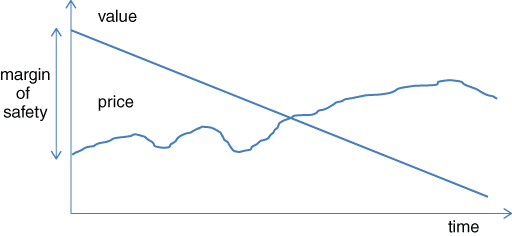

Erosion of Value Over Time

Mediocre businesses do not create value for their shareholders; instead, they destroy business value over time. So, the relationship between value and price is not what it looks like in Figure 2.1 and is closer to what is represented in Figure 2.2.

Figure 2.2 Price vs. Value for Mediocre Business

Therefore, the value of the business can decline and the initial margin of safety may gradually shrink, even if the stock price doesn't go up. Investors need to be lucky enough to have the stock prices rise in time and sell before prices drop again following the intrinsic value of the business.

Just as Buffett wrote in his 1989 shareholder letter: “Time is the friend of the wonderful business, the enemy of the mediocre.”10

Because he paid dear prices for buying unpromising businesses, Buffett learned his lessons. He considered his buying of the control of Berkshire Hathaway his biggest mistake, which eventually cost Buffett and his partners $100 billion.11 The stock was sold at a discount to its net-net working capital and less than half of its book value, but because of Berkshire Hathaway's operating loss and share repurchasing of stocks, its net worth had fallen from $55 million in 1964 to $22 million in 1967. At the time, Buffett also bought a well-managed retailer at a substantial discount from book value, but three years later he “was lucky” to sell it at the same price.12

This can also be seen from the October 2009 net-net working capital bargain portfolio shown above. In the first 12 months, the portfolio had substantially higher returns than the market. But in the three years that followed, it gave up all its gains while the stock market continued to march higher.

Timing and Pain

Buy these bargain portfolios when you can find plenty of them, but if the broad market is in quick decline, like in 2008, the bargain portfolio will be very likely to lose much more than the general market. If the decline lasts longer, many of the companies in the portfolio may suffer steeper operating losses and may even go out of business. It is much more painful to hold such a portfolio in bad times, as anyone who owns these stocks during bear markets or recessions will attest—and lose much sleep over!

In addition, because of the quick erosion of business value, selling the deep-asset bargains quickly is key, even if stock prices do not appreciate. The biggest profits are usually achieved within the first 12 months. That is why Charlie Munger said, “If you buy something because it's undervalued, then you have to think about selling it when it approaches your calculation of its intrinsic value. That's hard.”13

Buffett likens buying mediocre businesses at deep bargain prices for a quick profit to dating without the intent of getting married. In that situation, it is essential to end the courtship at the right time and before the relationship turns sour.

Not Enough Stocks Qualify

To avoid errors and disasters caused by single stocks in the deep-bargain portfolio, it is important to have a diversified group of them. But when the market valuation is high, it is just not possible to find enough stocks to satisfy the diversification requirement. This is the situation that emerged in 2012. GuruFocus's Net-Current-Asset-Bargain is only able to generate a handful of stocks in the U.S. market; they simply dried up as the market continued to tick higher. This situation may last a long time, as the close-to-zero interest rate has lifted the valuations of all assets.

Tax Inefficiency

Because of the short holding time, any gain from the portfolio is subject to the same tax rate as the investor's income tax for U.S. investors, unless it is in a retirement account. For those in the highest tax bracket, close to 40 percent of gains will have to be paid every year. This drastically reduces the overall return over the long term.

Though buying deep-asset bargains can be very profitable, this strategy comes with a much higher mental cost to investors. More importantly, business deterioration and the erosion of value put investors in a riskier position. As a result, they need to strictly follow the rules of maintaining a diversified portfolio and selling within 12 months whether investments worked out or not.

The approach should be to focus on small companies with liquid balance sheets. If a lot of hard assets such as equipment and buildings are involved, the liquidation process can be long and costly, which may eat up all the value the assets have. Buffett had first-hand experience with this. When Berkshire Hathaway finally shut down its textile business and was liquidating, the equipment that originally cost $13 million was still in usable condition and had a current book value of $866,000. The gross proceed from the sale of the equipment was $163,122. After the pre- and post-sale costs, the net proceed was less than zero.14

It is very dangerous and costly to hold onto the companies that have complex businesses and illiquid assets. You will get stuck with them while hoping the business will turn around, just as Buffett did with the original textile business of Berkshire Hathaway. If buying mediocre businesses at deep bargain prices for a quick profit is like a date without the intent of getting married, buying them and getting involved long term is like a marriage without love. A lot of other things need to be right to work things out, and it will never be a happy marriage.

One such case, ongoing for the past several years, involves Bruce Berkowitz of Fairholme Fund, one of the best-performing mutual fund managers in the first decade of this century. It has cost both him and his shareholders dearly.

Berkowitz has owned a large position in Sears Holdings, the struggling retailer, for more than a decade. The stock was trading at above $160 before spinoffs, and although he was well aware of the problems with the company's deteriorating retail business, he has long believed that Sears has tremendous values in its real-estate portfolio and its businesses, and these values can be realized by selling the businesses and real estate. By February 2014, the stock had lost more than 70 percent and was traded at $38, and Berkowitz believed that Sears' net assets exceeded $150 in value. He wrote in February 2014: “If our research is accurate, Sears' market price of $38 [is expected] to increase to this value over time.”15 Two-and-a-half years later, the stock is traded at below $10. Even if we added back the value from the spinoff of Lands' End and the right to buy Seritage at a discount, the stock has lost more than another 70 percent. Berkowitz is continuing to buy more Sears.

In the meantime, Sears has been doing everything to unlock value under the leadership of another supposedly capable value investor and financier, Eddie Lampert. Sears spun off Orchard Supply Hardware in January 2012 at above $20 and it now trades at 20 cents. The company couldn't compete with Home Depot and Lowe's, whether it was on its own or under Sears, and is now bankrupt. Another spinoff, Sears Canada, was never profitable after the spinoff at $18.5 a share in October 2012; the stock has since lost more than 80 percent and is on its own way to bankruptcy. The Seritage spinoff has been doing relatively well so far, but what the original shareholders received was the right to buy shares at $29.5 instead of simply getting the shares outright as with other spinoffs. Sears itself has been losing money every year for the past five. Most of the $2.7 billion proceeds from selling its primary properties to Seritage was used to cover the cash drain from its operating loss in 2015 alone. What value does it really unlock?

Sears also bought back a lot of shares over the years to “return” capital to shareholders. But for a company that kept losing money, the remaining shareholders only saw their share of loss get bigger and their share of business value drained faster.

One may argue that Sears shareholders could have sold the shares of Orchard Supply and Sears Canada after the spinoffs and benefited by doing so. I would argue that Sears shareholders should have long ago sold their shares altogether. The same is true for Berkowitz. His Fairholme shareholders would have been much better served ten years ago if he had sold Sears at above $160, or six years ago at above $70, or four years ago at above $40, or two years ago at above $30. The stock is now traded at below $10 and he is still not giving up. Instead, he is buying more because the stock is even more “undervalued.” The cost to Fairholme shareholders has been steep. The fund underperformed the S&P 500 by a total of more than 35 percent in the last three years and more than 50 percent in the last five years. Should I also talk about the lost opportunities?

The drama continues. Sears is spending heavily trying to turn around its beleaguered money-losing retail business and is hoping to compete against the likes of Amazon and Wal-Mart. Berkowitz has now joined the board of Sears. Such a move will definitely add more to his mental and psychological cost. The surprises just kept coming. Sears' pension fund burned $2 billion in the last several years, which as of today is more than double of the entire market cap of the company. The unlocking of value took longer than expected, which means more value is about to be eroded. In May 2016, Berkowitz thought that the problem with the pension obligation should improve, as the Fed's interest rate hike seemed imminent,16 only to see the interest rate continue to drop. Now he is expecting the retail losses to stop in 2016, which is unlikely as the company's loss keeps getting bigger each quarter. In the meantime, the company burned through another $700 million in the first quarter of 2016 and issued about the same amount of debt to maintain its cash balance.

Doesn't this sound like a hole that keeps getting deeper? Why would I, as an investor, want to get involved in this mess and witness things deteriorating, hoping the situation will improve? Even if it works out eventually, which to me is very unlikely, the mental and psychological drain is simply not worth it.

Buffett said it best:17

There are better ways to make money.