33

Too Much Liquidity Will Cost You

Fifty years of personal investing experience and observing other investors, particularly those managing their own investments, have led me to conclude that too much liquidity has, in fact, done individual investors more harm than good. The benefits of liquidity are often overstated while the costs are all too often under-recognized.

When it comes to investing, the general belief is that liquidity is a good thing. But is liquidity always a positive? The answer is No.

Liquidity with a specific purpose in mind is usually positive. For example, there is a clear benefit to having ready access to cash in an emergency fund to cover unexpected medical costs or your expenses between jobs. Stock markets rise over the long term, and therefore getting out of the market is betting against this powerful upward trend. The record for market timing is clear: Nobody has been consistently right about when to get out of the market and when to get back in.

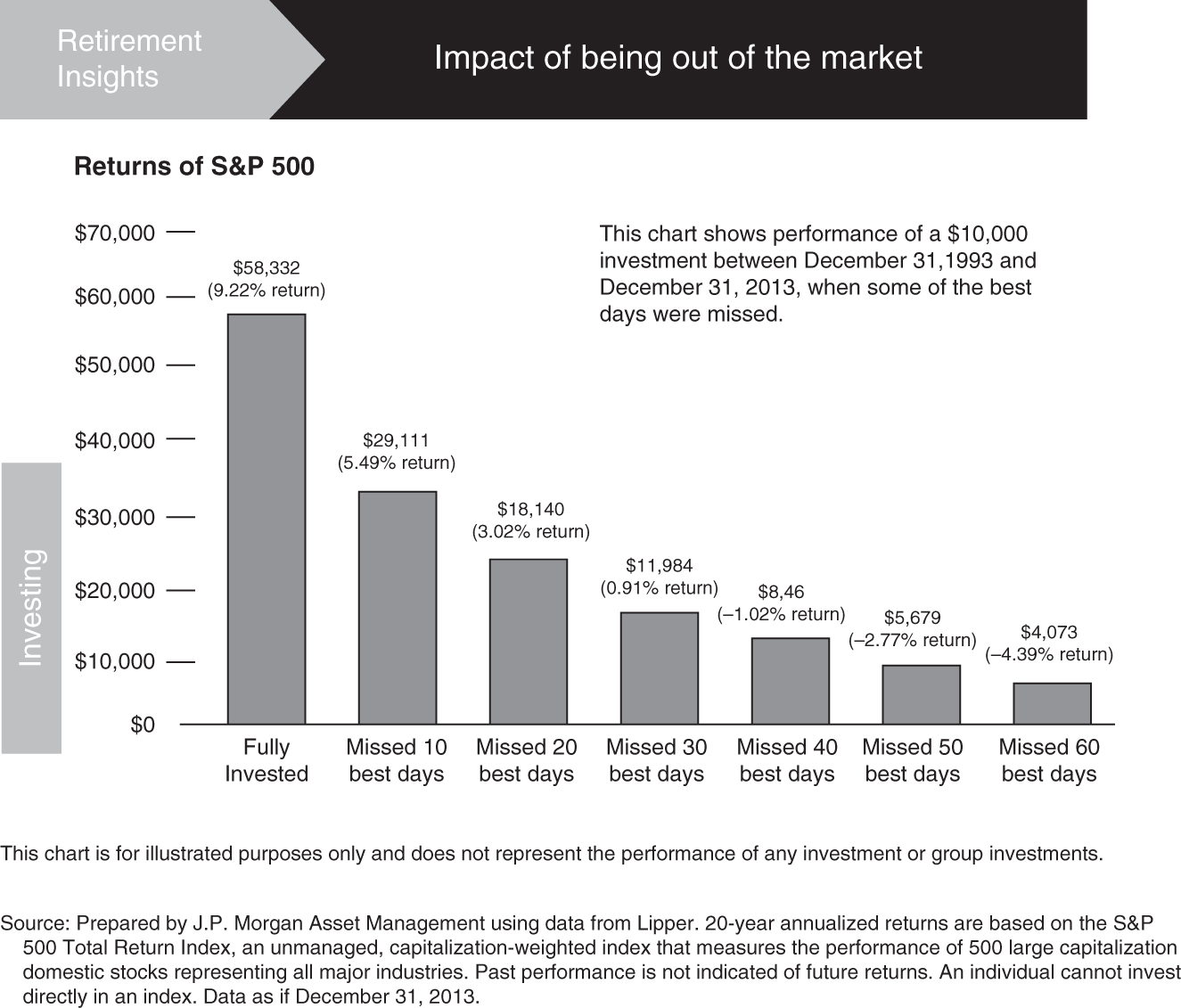

To reinforce this idea, let's look at some extreme, but illustrative, examples of how much it could have cost an investor to miss some key days of surging prices.

Let's take the 20 years from December 31, 1993 to December 31, 2013. The markets were open for more than 5,000 days. If an investor stayed invested through all those days, a $10,000 investment would have multiplied to $58,332. Now, take out just the best 10 days—less than 1/500 of the total time—and the total value of that portfolio drops to $29,111, wiping out almost exactly half of the returns over 20 long years. If an investor missed just 40 days, less than 1% of the 20-year time period, that 9.2% average annual gain would get converted into a loss of $854 (Figure 33.1). So patience and staying in for the long term are crucial for investment services. The same reality applies to individual stocks but even more forcefully.

Figure 33.1 Impact of Being Out of the Market

For most individuals, excess liquidity means more time out of the market, which history has shown can be a costly mistake. Cash drag is another way of looking at the same issue. For example, if you have $10,000 more than you need in a money market account where returns are about 5% less than what you might earn from a long-term investment, then, on average, you lose $500 every year you keep it there!

A more subtle and serious problem with liquidity is the temptation of what's known as easy action. In other words, if you have the money sitting there and what may appear to be the next big thing comes along you are more likely to buy it—impulsively.

America's favorite investor, Warren Buffett, illustrates the discipline that can substantially improve your decisions on investments with a “decision ticket.” Imagine you have a lifetime ticket that provides you with only 10 decisions to invest. Each time you make an investment decision, one of those 10 numbers gets punched. After 10 punches, you must turn in your card, and for you, it's game over! You can make no more investment decisions. So, you'd be particularly diligent and make each of your decisions with great care and self-discipline.

Source: Wealthfront, Summer, 2014.