25

A New Paradigm of Investment Management

The managerial disciplines required to achieve organizational success—recruiting and rigorously training the most capable people, developing a strong culture centered on serving clients unusually well, etc.—have, in recent decades, been increasingly subordinated to the discipline of a specific kind of investing—growth versus value, etc. serving one kind of client: institutions vs individuals. Actually, organizational excellence can accommodate more than one investment specialty and enables an investment organization to serve major clients better over the long term.

A new paradigm is developing in investment management—a new organizational and “management” paradigm—that has the competitive strength to dominate the investment management business and the practice of the investment profession. The new paradigm is remarkably different from the paradigm that has, over the last quarter century, became the accepted and dominant norm in the field.

The presently dominant paradigm is a specialist manager with one investment “product” serving one market, usually pension funds. The developing new paradigm is a multimarket, multiproduct organization.

My thesis is that because the new multimarket, multiproduct organization—when properly led and managed—is more consistently capable of meeting the long-term needs of clients and investment professionals, it will be increasingly accepted and will become the norm. In fact, the evidence suggests the Darwinian process of one species displacing another—because it is even better matched to the situation—is progressing very rapidly now.

The Past

To put the current situation in perspective, recall the situation 50 years ago. It was simple: Insurance companies and insured plans dominated pension fund investing through the 1940s.

In the 1950s, with the proliferation of corporate pension funds symbolized by General Motors' agreements with the UAW to set up a separate fund and to provide “fringe” benefits during the Korean War price freeze, a new paradigm moved into ascendance—the large bank trust departments offering a narrow product line: balanced accounts. But their offering included a crucial difference: Equities could be 30% or even 40% of total assets, far greater than the 5% limit of the insurance companies. And in the postwar bull market, being in equities made all the difference.

By the mid-1960s, two key changes in the situation were increasingly significant. Pension fund assets had become quite large and having so much money with one manager was questionable. In addition, performance was being measured and compared, and some of the largest bank trust departments were seen to be underperforming another type of manager—investment counselors that explicitly sought “performance.”

Five more changes were increasingly evident through the 1970s and into the 1980s. First, plan sponsors split up their funds among more and more investment managers in part because they sought specialist managers and in part because many of the most promising specialist managers were small, relatively new firms. The multimanager concept of pension fund investing further encouraged the formation of specialist managers.

Second, plan sponsors were clearly willing to pay higher fees to get the “performance” managers they believed could obtain higher rates of return that would more than cover the cost of higher fees. Third, investment managers learned that they could win substantially more business by engaging boldly in vigorous direct selling—and so they did. Fourth, the institutional brokerage industry developed considerable capabilities in research and the execution of block trades to meet the needs of “performance” managers. Finally, assets continued to grow, and more and more pension plans and endowments organized themselves to “manage the managers”—particularly, to be buyers that could meet the sellers of investment services and make a market.

And what a market it was, particularly for the specialist investment managers. They became so notoriously successful that the trust departments and the insurance companies abandoned their traditional organizational structures so they could try to replicate the new paradigm that is so familiar to us all—a group of experienced portfolio managers in their forties with strong analytical backgrounds, engaging personalities, high energy levels and considerable skill, who strive to achieve superior performance as a creative team, manage portfolios actively, seek to develop close professional relationships with clients, and are skillful in both direct selling and in working with consultants. They earn substantial compensation as individuals, charge high fees as firms, are exciting to be with, and have fun. They met the market on its own terms—and have proliferated.

The 1980s extended the developments of the 1970s. Asset classification became increasingly important. Manager classification became increasingly important. You were either a value manager or you were not; you were a growth manager or you were not; you were a sector rotator or you were not. You had to pick one and stay there. Product proliferation began, and the different kinds of specialization that investment managers might undertake multiplied.

One solution to the problem of proliferating managers was the emergence of a completely new industry: “consulting.” At least 50 consultants now intermediate between plan sponsors and investment managers, trying to solve the problem of proliferating asset classification, proliferating managers, and product proliferation.

The Future

Managers are classified according to an ever-expanding set of specific categories. A manager is either a value manager or a growth manager and, within each of those categories, a large-capitalization, or a small-capitalization manager. He is a passive, quantitative or an active manager. He may operate with or without “technology.” A global or international manager can concentrate on the Pacific Rim, on Europe or Latin America, on the emerging markets globally, or on any specific part of the world with or without currency overlays.

On the bond side of the business, a manager is immunized or dedicated, structured, or indexed or index-plussed. He could have GICs or BICs; be in the high-yield sector, with or without credit evaluations; deal with private placements or the extended market; avoid or concentrate in mortgages and asset-backed securities of all kinds. A bond manager could be international or global, with or without currency overrides; have a STIF or a medium-term note portfolio; be involved in bank loan packaging or convertibles, sector switching, arbitrage, constant yield, constant duration, and so on.

From the investment manager's point of view, the world is not particularly simple either. The large, medium, and small institutional funds have fundamentally different characteristics. Public funds are tremendously different from corporate funds, and endowment funds are different from both. The 401(k) plans are growing rapidly and have fundamentally changed the terms of the competition. Nuclear decommissioning could be an important market. Insurance companies are becoming interesting and, of course, there are large numbers of different kinds of offshore funds. The United Kingdom, Japan, Germany and Canada—each an important market opportunity for American managers—are very different from each other and from the American market.

All the complexity on the investment manager's side and all the complexity on the client's side are beyond the capacity of most of us. Some new way of being organized is needed, one that has the capacity to deal in many different markets. It must be effective for the client, and it must be productive for the investment manager. It must be capable of dealing successfully with multiple products. And it must be a multimarket organization, so it can access business from many sources.

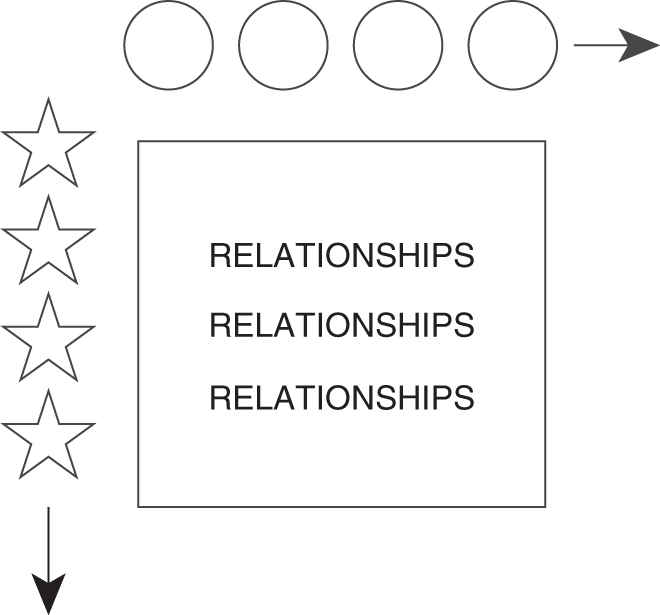

The new form of organization must be reliable and sustainable both for the client and for the manager. It must allow individuals of considerable talent and pools of capital of large size to make long-term commitments such as the structure shown in Figure 25.1. The stars represent investment management capabilities, which can be defined as “products.” Each is carefully, rigorously defined as to concept, specifications, and performance. The circles represent markets to which the organization sells its product capabilities. The interior space between products and markets will be dominated by superior capabilities in relationship management and development with particularly strong professional investment counseling—problem delineation and problem solving—servicing the specific needs of specific clients.

Figure 25.1 The New Paradigm

This multimarket, multiproduct investment management organization meets several needs of major clients: product specification and product conformance, product innovation to meet new needs or exploit new opportunities, the confidence and convenience that go with long-term professional relationships, possibly lower costs, and relationships that are “client-driven” rather than “product- driven.” And this organization better meets the needs of many investment managers, for professional growth and creativity and financial security at high pay levels without betting their business careers as well as their professional reputations on a single way of investing in a single asset class.

These organizations can afford to invest in acquiring increasingly costly and essential systems, developing new products, and developing new markets—and they will. And as product specialization and market segmentation proliferate, an increasingly large share of new products and new markets will be developed by the organizations that master the new paradigm. In fact, these new organizations are already dominating new product development and new market development.

Three concluding observations seem important. First, the new paradigm will not overwhelm all the boutiques. The best specialist firms will continue to prosper—but it will be more and more important to be very, very good. Second, not all of the multiproduct, multimarket organizations will be assured of success. Only those that produce consistent product quality and service quality will succeed.

Finally, the new paradigm is certainly not “just” a return to the old “balanced manager.” The old paradigm trust department or insured plan couldn't come close to competing with the new paradigm organization. The new paradigm organization is profoundly different on every important variable: leading-edge investment innovation, strong client-centered relationships, devotion to product excellence in design and conformance in execution, strong business development, and exceptionally rewarding careers for gifted, motivated professionals, with business strength the foundation for professional excellence.

Source: Charles D. Ellis (1992) A New Paradigm of Investment Management Financial Analysts Journal, 31: 2, 16–18, copyright © CFA Institute reprinted by permission of Taylor & Francis Ltd, http://www.tandfonline.com on behalf of CFA Institute.