12

Murder on the Orient Express: The Mystery of Underperformance

Evidence increasingly shows that a “crime” of extensive underperformance has been committed in mutual funds, pension funds, and endowments. In a pattern reminiscent of Agatha Christie's famous novel, Murder on the Orient Express, an investigation leads to a surprising, if inevitable, conclusion: The usual suspects—investment managers, fund executives, investment consultants, and investment committees—are all guilty.

Agatha Christie, for many years, the world's favorite mystery writer, perfected her guessing game by creating a “can you solve it?” puzzle in Murder on the Orient Express. Clues pointed in many directions but gave no certainty. As the plot thickened, Hercule Poirot, the wily Belgian investigator, deftly guided readers to an eventually obvious conclusion: No one suspect was guilty—all the suspects were guilty.

The same reality may explain the persistent failure of institutional investors to achieve their ubiquitous but evanescent investment goal of superior results, or “beating the market.” The results are consistently disappointing; clues to the causes and leads to suspects abound; and suspicions and evidence implicate a full array of possible culprits, any one of whom could be the perpetrator. However, unintentionally, the “failure to perform” problem is made even worse by many funds that aim very high, set inherently unrealistic expectations, and then take on higher-volatility managers because their recent investment performance looks “better.”

Despite the statistical impossibility of more than one in four funds achieving Top Quartile results, a majority of funds—more than twice the Top Quartile objective's capacity—solemnly declare this goal as their objective. (Lake Wobegon fans would not be surprised. Nor would behavioral economists whose research shows the famous 80/20 Rule at work in many self-evaluations. About 80% of people in group after group rate themselves “above average” as friends, conversationalists, drivers, or dancers and in having a good sense of humor and good judgment and being trustworthy.)

Maybe it is just human nature to be qualitatively optimistic about ourselves. But the investment results can always be quantified for objective analysis. Extensive and readily available data show that in a random 12-month period, about 60% of mutual fund managers underperform. Lengthen the period to 10 years and the proportion of managers who fall behind the market for this longer period is about 80%. At least as concerning, equity managers who underperform do so by roughly twice as much as the “outperforming” funds beat their chosen benchmarks. So, the underperformers' “slugging average” is doubly daunting. New research on the performance of institutional portfolios shows that after risk adjustment, 24% of funds fall significantly short of their chosen market benchmark and have a negative alpha, 75% of funds roughly match the market and have zero alpha, and well under 1% achieve superior results after costs—a number not statistically significantly different from zero.

If our profession fails to deliver on its promises, negative consequences could be in the offing for us as well as for our patient, long-suffering clients. So, let's look at the evidence to see why institutional funds have been underperforming.

The Evidence

Institutional funds underperform because their managers underperform—certainly not always and certainly not all managers, but by enough managers enough of the time to make the aggregate evidence undeniable.

Data from over 35 years of behavioral research on individual managers at institutional funds show that large numbers of new accounts go to managers who have produced superior recent results—mostly after their best-performance years—and away from underperforming managers after their worst-performance years. Another oft-repeated negative factor is moving into asset classes or subclasses after prices have risen and out of asset classes or subclasses after prices have fallen—moving assets in the wrong direction at the wrong time. This “buy high, sell low” pattern of behavior, so familiar to students of mutual fund ownership, also burdens institutional investors with billions of dollars in costs.

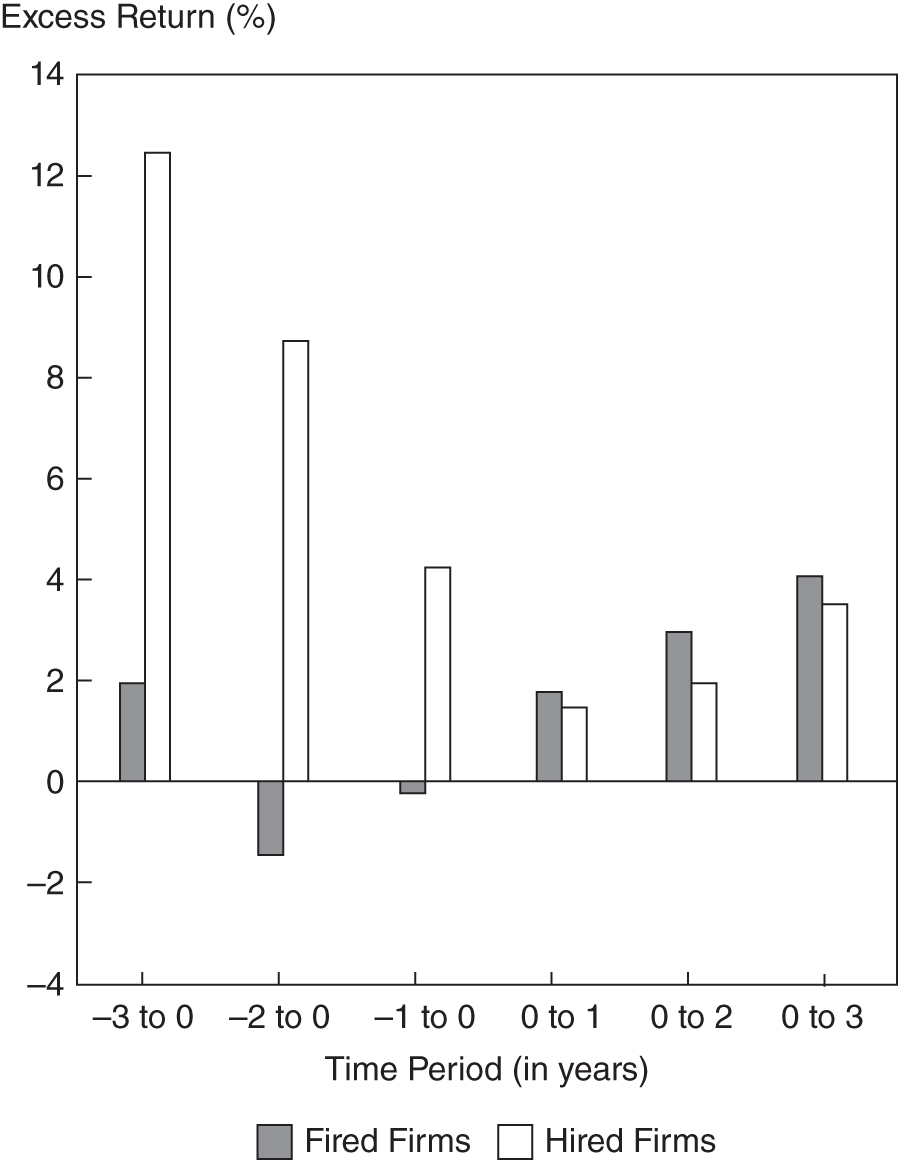

Forensic evidence in Figure 12.1 shows that institutional investors (pension funds, endowments, etc.)—despite their many “competitive advantages,” including full-time staff, consultants, and the ability to change managers and select those they consider the very best managers—typically under-perform their chosen benchmarks. In a recent study of more than 1,000 institutional funds, the managers who were hired had achieved over the three years before their hiring significantly higher returns than the managers who were fired. (The to-be-hired managers produced substantial excess returns on domestic equities over the prior three years.) However, for the three years after the new managers were hired, the fired managers achieved slightly higher returns than the new managers. This difference—repeated over and over—incurs two kinds of costs that accumulate through repetition. What matters most is not the cost of the trivial underperformance of the new managers versus the fired managers after the change, but the substantial underperformance of the soon-to-be-fired managers over the years before the change.

Figure 12.1 Excess Returns for Fired and Hired Investment Managers Notes: All the differences between fired and hired managers before the firing are significant. The differences between fired and hired managers after the change are clearly indicative but not statistically significant. All data are for U.S. funds.

Source: Amit Goyal and Sunil Wahal, “The Selection and Termination of Investment Management Firms by Plan Sponsors,” Journal of Finance, vol. 63, no. 4 (August 2008): 1805–1847.

Ironically, once the hiring is done, almost nobody involved studies the process of hiring managers who later disappoint. Managers tell themselves that their poor runs were just “anomalies” and look forward, often with remarkable optimism, to better times ahead—and better results. Meanwhile, clients tell themselves that they got rid of the bad managers. As Emerson so wisely observed, “The unexamined life is not worth living.” Social scientists have observed that people with motivations to believe in their efficacy repeatedly “see what they believe in”—the illusion of validity—and so do not recognize even persistent shortfalls or failures. Although everybody knows that patrons of gambling casinos are, as a group, significant losers, the tables and slots stay busy. So, if neither clients nor managers examine or learn from their actual experience, the problem will continue.

If participants did examine their experience, they would see that one serious cost is the negative performance incurred by funds before they are finally provoked into taking action. This cost comes from the risks taken when trying to identify managers that might achieve superior future performance and actually increase the odds of future disappointment because recent past performance, however compelling it may appear, seldom predicts future performance.

Costs also matter far more than most investors realize. Investment management fees are not “low.” Viewed correctly, such fees are actually very high. Over the past several decades, fees for institutional investors have risen from less than 1/10 of 1% to nearly ½ of 1% of assets for equity investments (less for fixed income and more for such “alternatives” as private equity and hedge funds). Because the client already has the assets and is thus looking only for returns, those same fees are actually more than 5% of likely returns—a more accurate recognition of reality.

But now, a new reality is stalking active managers. The very small commodity fees charged for index funds that consistently provide market-matching returns at market-matching risk. This means that active managers can only hope to deliver real value when they actually beat the market—which, we now know, most do not do, particularly over the long term. As a consequence, for active management, true fees—incremental fees as a percentage of incremental added value—are more than 50% of the value delivered by the more successful active managers and are far higher, even infinitely higher, for the many less successful active managers. Here's why: The real marginal cost of active management is the incremental fee that active managers charge versus the incremental returns they deliver after fees and costs of operations.

Seen correctly, active management may be the only service ever offered—and widely accepted—that costs more than the value delivered. (Students of real versus apparent cost will remind us that the true cost of a puppy is not the cost of a dog nor is the payment to the boat broker the true cost of a yacht. On the latter, J.P. Morgan famously observed, “If you have to ask what it costs, you cannot afford it.”) Increasingly, clients are realizing that costs are at least a major part of the problem of underperformance—particularly in today's intensely professionalized market. The cruel irony is that so many active managers are so skillful, hard-working, and capable that they collectively dominate the market and so very few, if any, can beat the crowd. Judging by overall investment performance, the record is not comforting.

So, institutional underperformance—in addition to the high fees and the costs of manager switching—involves three “murder weapons”: hiring managers late, firing managers late, and investing with managers and in asset classes that underperform. We are still left with the question that Agatha Christie fans must try to figure out: who dunnit?

The Suspects

The investment profession is not lacking in possible suspects for the crime of systematic underperformance.

Investment Managers

After almost three decades of working on business strategy with major investment management firms in Europe, Asia, Australia, New Zealand, and North America, it became clear that the main culprit had to be investment managers. Managers—knowing they are talented, hard-working, well trained, and dedicated—still sometimes believe deeply in the value of their work (behavioral economists call this familiarity bias). The circumstantial evidence was substantial. During new-business presentations and in quarterly review meetings, virtually all managers gave in to the understandable temptation to present their performance records in the most favorable light. Their records were almost always “enhanced.” For example, the years included in historical “performance” charts were often chosen mainly to make the best impression. In addition, the benchmarks against which the managers' results were compared were often selected for similar reasons. Looking back, both the inconsistency of “relevant time periods” and the variety of benchmarks used were impressive. Even more disturbing is how many institutional managers still present their results before deducting fees.

Another “clue”: Investment philosophies and decision-making processes—no matter how complex they might be to implement—were all too often oversimplified, documented with selected data, and then crisply articulated as convincing universal truths. Both prospects and clients were led to believe that each manager had developed a compelling conceptual competitive advantage in the “battle for performance.” One aspect of client-manager meetings had an intriguing reality: Virtually every such meeting was actually a sales meeting. Of course, new-business presentations were also sales meetings. But so were the quarterly review meetings. The managers' unstated objective at every meeting was less about building a shared understanding of the uncertainties and difficulties of investing and more about “winning”—winning the account in a new-business competition or winning additional business when performance had been strong or winning a reprieve and retaining the account for a few more quarters when performance had been disappointing. No manager talked candidly with clients about how difficult investment management had become as company information and rigorous analyses proliferated, competitors multiplied, and information that had once been seen as a competitive advantage become increasingly “commoditized.”

Realists would suspect that as much as investment managers might want to build their firms on the basis on superior performance, the more compelling motivation had become economic: to win new accounts and to keep old accounts while worrying about performance tomorrow. After nearly three decades of “behind the scenes” experience with over 100 investment organizations of various sizes in several nations, I was increasingly drawn toward the suspicions of the realists.

A close examination of the competitive rankings of investment managers makes a compelling case: Over and over again—even when they had to know that continuing to produce such superior results would be terribly hard—managers made special efforts to go out and sell their services and win new accounts when their recent annual performance numbers were particularly favorable. Well, they would, wouldn't they? Realists recognized that those managers who worked hard to get new accounts when their results looked best won more business, and those who temporized skillfully during patches of underperformance kept more business. So, if investors were asked, “Who dunnit?,” the evidence would point to the investment managers as being guilty of causing institutional underperformance.

Investment Consultants

On reflection, however, another group of suspects had to be considered: investment consultants. They are paid fees, usually on retainer, to monitor an institution's current managers and to help select new managers after, of course, first helping clients decide to terminate underperforming managers. In the view of most institutions' busy investment committees, it has made sense to use an outside consultant who specializes in evaluating hundreds of potential investment managers, systematically evaluating their “performance” numbers, regularly interviewing their key people, and rigorously comparing actual behavior with projections and promises. The outside expert, ostensibly dedicated solely to the client's best interest, is independent and also able to do a more extensive and intensive evaluation. Moreover, the stated cost of retaining a consultant is low compared with having internal staff do the work.

A realist would note that investment consulting is a business. Although consultants would like to achieve great results for their clients, business economics almost inevitably dominate aspirations toward professionalism. Once the research costs of evaluating managers and compiling the database at an investment consulting firm are covered, the annual profitability of an incremental account is over 90%. And because well-managed relationships continue for many years into the future, their economic value is not just this year's fee but, rather, the net present value of many future years' fees. Equally, over 90% of the net present value of any lost account's fees is lost to the firm's profits. So, the owners of consulting firms pay close attention to their firms' business relationships, and the main priority of relationship managers is clear: Never lose an account. Eventually, as consulting firms get larger, this business priority naturally dominates compensation and promotion for every on-the-line consultant.

Given the great difficulty of the task, it would be naive to assume that any investment consulting firm could somehow consistently identify managers with superior future capabilities and skillfully terminate those about to disappoint. It would be far better for the consulting firm to build a strong defensive position by encouraging each institutional client to diversify its fund across various asset classes and to have multiple managers in each category. On both dimensions, “the more, the merrier” diversification protects the consultant's business by diversifying against the risk of any particular manager's performance difficulties doing harm to the consultant's relationship with his clients and future fees.

Of course, this hyperdiversification portfolio strategy has led to client institutions paying higher fees and having a large number of different managers, which increased the chances of one or more managers producing disappointing results. It also made the institution's fund executive and its investment committee all the more dependent on the consultant monitoring those numerous managers—plus the alternative managers who might be brought in when some of the current managers faltered or failed. Monitoring all those managers not only made the institution dependent on the consultant for information, but it also meant that no one manager was all that important to the total fund. The traditionally limited time of investment committee meetings—typically three hours once a quarter—was fully booked with reviewing the overall performance of the portfolio and reporting on a long list of specific managers, particularly those who were seriously underperforming. Keeping to the agenda left too little time for thorough evaluation of both the committee's own management of the manager selection process and the consultant's true added value.

Many consultants learned long ago the wisdom of following two practices with each client's investment committee. First, develop a particularly close, personal service relationship with the chair of the committee. This is easily done by increasing the frequency of research reports, report updates, e-mails, and phone calls to render impressively caring service. (A supplemental objective might be to develop nearly as close a relationship with the most likely next committee chair.) Second, investment consultants learned to present at selection finals only those managers who had compelling recent annual performance records and not to lose points by defending a “disappointing” investment manager. (Has any consultant ever presented a manager by saying, “While this manager's recent performance record certainly does not look favorable, our professional opinion is that this manager has weathered storms in a market that was not hospitable to its style and has a particularly strong team that we believe will achieve superior results in the future”?.)

Consultants' agency interests—compensation for both consulting firm owners and individual consultants—are economically focused on keeping the largest number of accounts for as many years as possible. These agency interests are not well aligned with the long-term principal interests of the client institution. Although neither consultant nor committee really wants it to be that way, a separation of agency versus principal behavior should have been anticipated.

Finally, after tracking which managers win accounts and which lose accounts each year—and then subdividing the records by consulting firm—the behavioral record indicates that consulting firms' clients have been hiring managers after their best years and firing managers after their worst years. So, the evidence points to this conclusion: The consultants did it! They are guilty of—or at least complicit in—the crime of causing institutional investors to underperform.

Fund Executives

Suspicion points in yet another direction—the institutions' own fund executives. One cause for suspicion is a curiosity: Fund executives frequently insist on having a separate account rather than investing in a pooled fund at a significantly lower fee—even though managed by the same firm using the same research and usually the same or similar portfolio managers. Separate accounts often make sense when investing in illiquid “alternatives,” but the preference for separate accounts for “long-only” stock investing is a mystery. Although there are much-admired exceptions—in particular, several endowment CIOs with extensive experience and strong professional staffs—many fund executives are disadvantaged. Often not deeply experienced in the complexities of investing, they are not highly paid, especially when compared with the front-line “socially dominating” representatives of investment managers.

Investment managers learned long ago to be represented always by socially dominant people—hunters—who are highly skilled at closing transactions and are paid many multiples of what fund executives are paid. Disparagingly called “gatekeepers,” fund executives are almost always staff-minded processing people who must often feel “caught in the middle” between investment committees with too little time and investment managers with too much skill and experience at selling—and an absolute determination to win. Through no fault of their own, fund executives and their staffs are set up to be overwhelmed. Rather than carefully buying investment services, they are sold those services. And the easiest time is at the peak of an investment firms' performance. So, a realist would be drawn, however reluctantly, to the grim conclusion that it is the fund executives who dunnit.

Investment Committees

During the past decade, a new kind of experience has provided me with another, better perspective on why institutional funds underperform. Having served on a dozen investment committees—in Asia, North America, and the Middle East—with funds ranging in size from $10 million to $300 billion, I can confidently state that the evidence points with remarkable consistency to yet another surprising culprit. With all their best intentions—both individually and collectively—the perpetrators of the crime of underperformance must be the funds' investment committees.

Consider the evidence. First, many investment committees are operating in ways that do not reflect the substantial changes in investment markets that have made obsolete many of the traditional beliefs about investing—particularly those outdated beliefs still often held by senior people who serve on investment committees. However unintentionally, many investment committees have misdefined their objectives and are organized in ways that are counterproductive. As Shakespeare put it, “The fault, dear Brutus, lies not in the stars, but in ourselves.”

Certain internal factors that inhibit fund committees “come with the territory.” Many are not helpful. Most investment committees devote up to 10% of their limited time to administrative matters: reviewing minutes of past meetings, setting dates for future meetings, and so on. Some 15–20% of their time is devoted to discussing the economic outlook and covering regulatory issues. Another 15–20% is spent reviewing managers' “performance” and comparing their fund's results with those of a peer group of funds. Usually, another 20% of the meeting time is devoted to presentations by two or three current managers who discuss the economy, the markets' outlook, their organizations' various perspectives on performance, their more interesting recent investments, and their look-ahead portfolio strategies. Always interesting and thoroughly documented, in combination, a series of these presentations by different managers can blend together in the memories of most committee members into one large “disassembled jigsaw puzzle” of data, concepts, opinions, and projections. What had seemed quite persuasive when first articulated can, in retrospect, seem confusingly jumbled together.

The committee then turns to the “real” work, often with the guidance of an investment consultant: considering the firing of one or two poorly performing managers among the dozens employed and then hiring one or more among the three or four “finalist” managers evaluated and selected by the consulting firm from the dozens of managers monitored. Usually, the selected managers have had the most apparently compelling recent performance and have made the most persuasive presentations. Each finalist manager's team enters the room; its members thank everyone, often individually, for “this important opportunity.” They pass out binders of 40–60 pages loaded with “gee whiz” charts of past performance, extensive statistics on the economy and the major investment markets, several sheets of “bullets” outlining the managers' core beliefs and investment concepts, a few compelling examples of their recent investment triumphs, and short “credential” biographies of several key professionals. Although sardonic humorists might point out that it is like trying to select a spouse via speed dating, committee members dutifully strive to do their best to keep up with the main themes of the presentations, try to remember specific points made, and then make a judicious appraisal of the capabilities of the complex organizations being presented, all before the meeting time has run out.

Committees tend to differ somewhat from one type of institution to another. For example, most endowment investment committees comprise experienced seniors who devote their time without compensation to impart their wisdom and experience because they care deeply about their institutions. Often, although they are important patriots of the institution and feel honored to serve, they are not always experts in contemporary investing. As distinguished seniors, participants are reserved in demeanor, strive to avoid disagreement or confrontation, and, to ensure harmony, usually place their spoken views near the center of an emerging consensus. In addition to these challenging qualitative characteristics, endowment committees are often similar in such quantitative factors as meeting four times a year for three or four hours per meeting with little contact between meetings. Committee members are aware of the reality that the meeting time is fixed, the agenda is at least “full,” and the chair is determined to complete all items by a pre-agreed time for adjournment.

Corporate pension committees tend to differ in several ways: Most are staffed entirely by internal executives representing such important parts of the sponsoring corporation as human resources, benefits administration, finance, and treasury. One or two investment staffers—typically young and serving on rotation for a few years for training purposes, but not extensively experienced in the complexities of investing—often hope to rotate to a divisional controller's or assistant treasurer's position. Usually chaired by the vice president for finance, meetings are disciplined, and the protocols of corporate deference to hierarchy are well understood. Committee meetings are shorter and more frequent than those for endowments. Open discussions on such theoretical subjects as how to evaluate investment managers or the reasons for skepticism about performance data are rare. Each agenda item has an explicit time limit, and the pace of meetings is expeditiously business-like.

Public pension fund committees have their own set of characteristics. They are large—often very large—to accommodate union representatives of such disparate employee groups as teachers, firefighters, police, and sanitation workers, as well as representatives of the government's budget office and treasury and of the mayor or governor. Many committee members are new to investing and its many complexities and to the importance of managing risk as well as returns. Some also have two or three “public” representatives or are required by law to be open to the public, and some even broadcast their meetings on radio or television.

Almost all investment committees labor under an array of handicaps, including the following:

- Believing performance data can provide useful information for evaluating active investment managers even though studies of past performance show that past results have no predictive power—except for the bottom decile. (High fees and limited capabilities tend to persist, so seriously disappointing results tend to repeat.)

- Believing the primary mission of their investment committee is to select top quartile managers who will significantly outperform even though the evidence shows that a majority of managers fall short of the market and almost none have outperformed by very much for very long.

- Staying with historically valid policies when circumstances have changed fundamentally.

- Being prone to the constraints of both “groupthink” and such aspects of behavioral economics as overreacting to recent events, being confirmation biased, and tending to ignore long-term norms.

- Being guided by an investment consultant whose advice may suffer from the very real agency problems discussed earlier.

- Making the double error of attempting to do too much of what they shouldn't do (making investment management decisions) and thus having too little time for the important work they should do (providing good governance).

Governance should include the following: evaluating the supervisory capabilities of the fund's internal management, understanding the real costs of actively managing investments, clarifying long-term objectives and short-term risk tolerance, developing realistic investment policies, determining the consistency with which actions fulfill agreed policies, and asking searching questions about the process followed by the fund's operating management and its investment committee. The best committees help bring stabilizing, rational consistency to the emotionally draining work of managing long-term investments in volatile markets and staying with chosen policies through periods of turbulence.

Conclusion

No matter how tempted investment committees may be—after objectively examining the accumulated evidence—to confess to causing underperformance, they are not entirely responsible. Investment committees are guilty, but they are not alone. They have accomplices. Investment managers, investment consultants, and fund executives are also guilty. No one suspect is guilty; they are all guilty.

But, in the “end-of-story” ironic twist so often enjoyed by Agatha Christie's many readers, none of the four guilty parties is ready to recognize its own role in the crime. Each participant knows that it is working conscientiously, knows it is working hard, and believes sincerely in its own innocence. Indeed, nobody seems to even recognize that a crime has been committed—nor to realize that until they examine the evidence and recognize their own active roles, however unintentionally performed, the crime of underperformance will continue to be committed.

Source: Charles D. Ellis (2012) Murder on the Orient Express: The Mystery of Underperformance, Financial Analysts Journal, 68:4, 13–19, copyright © CFA Institute reprinted by permission of Taylor & Francis Ltd, http://www.tandfonline.com on behalf of CFA Institute.