In this section, I describe some considerations to help you decide whether investing in cryptoassets is right for you. There are many risks, but the markets are exciting and people have made and lost fortunes in the these markets.

How do you put a value on cryptocurrencies or cryptoassets? For tokens that are a claim on an underlying asset such as 1 oz of gold, the price of the token should more or less track the price of the underlying asset. However, as previously discussed, cryptocurrencies are not a claim on any asset, nor are they backed by an entity. Is there a way to calculate a fair value for them?

We can ask three independent questions:

1.What is the current price of the cryptoasset?

2.What causes prices to change?

3.What should the price be?

What is the current price of the cryptoasset?

The current price of any asset is determined by the market. Cryptoassets trade on one or more exchanges, and both prices and liquidity can differ between exchanges. Exchanges that report the most trade volume provide a good measure of the price, as they are the most active and should have the most liquidity. Other exchanges may have higher or lower prices.

Coinmarketcap.com is one of many websites that provide data about the current price of tokens and which exchanges they trade on. If you click on the name of a token and then click on ‘Markets,’ you can see where that token trades and how much volume the exchange says it has traded. Note that some exchanges have been caught faking trade volume in order to generate business, and I am not confident this practice has been eliminated… beware!

What causes prices to change?

The prices of cryptocurrencies and tokens behave like any other financial asset, driven by buyers and sellers who make trading decisions based on various factors:

1.Sentiment (how traders feel about the asset)

2.Gossip and chatter on forums and social media sites

3.Technical successes (e.g., when blockchains successfully implement technical upgrades that make them more useful, or when an ICO makes progress on its roadmap)

4.Technical failures (e.g., if transactions slow down or a weakness is found in the way the blockchain operates)

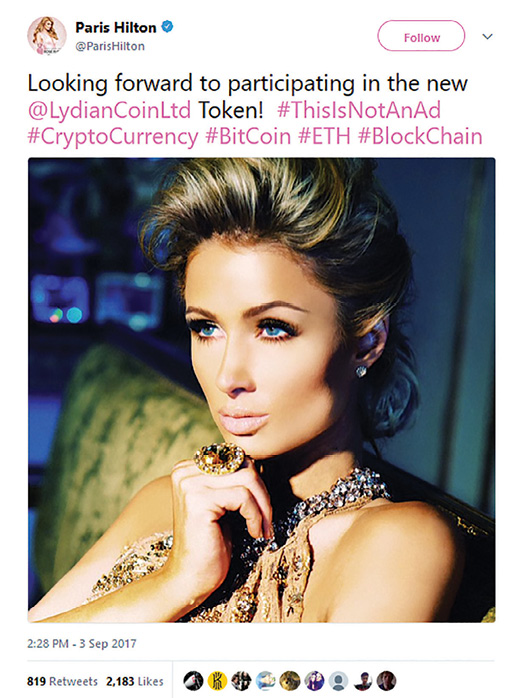

5.Celebrity endorsements (e.g., Paris Hilton’s endorsement of LydianCoin in Sept 2017, or John Mcafee’s occasional promotional tweets)

6.Founders getting arrested (e.g., when the founders of Centra token were arrested in the USA, and the price of the tokens fell by 60%237)

7.Orchestrated Pump & Dumps where people coordinate to all buy a coin together to make the price go up and persuade others to buy it at a higher price, then sell the coins to unsuspecting new buyers

8.Manipulation by large holders of any particular token

A celebrity endorsement238.

What should the price be?

There have been a number of attempts to create models to find a fair value for cryptocurrencies and tokens. A common but flawed model for putting a value on a Bitcoin is the ‘if the money in gold went into Bitcoin’ model:

‘If x% of the money in gold (or other asset class) moved into Bitcoin, a single Bitcoin should be worth $y’.

The argument is as follows: The total value of gold in circulation is estimated at 8 trillion US dollars. If some small proportion of the people holding gold, say 5% (but you can use any number from 0-100% here), sold their gold for dollars, it would release a large amount of money, in this case $400 billion. If the dollar proceeds were used to buy bitcoins, the total value of bitcoins in circulation, commonly referred to as ‘market capitalisation’ or ‘market cap,’ would increase by the same amount, $400 billion. As we know, the total number of bitcoins in circulation, 17 million or so, then this must increase the price of each Bitcoin by $23.5k ($400bn / 17m).

But this logic is wrong. That is not how financial markets work at all. The ‘money going into Bitcoin’ doesn’t simply drop into the ‘market cap’. The reason is simple: When you buy $10,000 worth of Bitcoin, someone else is selling those bitcoins for $10,000. So any money ‘pumped in’ is also exactly equal to money ‘pumped out’ (excluding exchange fees, to keep things simple). The only thing that happens when you buy a Bitcoin is that the Bitcoin changes ownership and some cash changes ownership. There is no mathematical relationship between how much money you spend buying bitcoins from someone else and the market cap of Bitcoin.

Let’s put numbers to this and demonstrate the flawed logic with a counterexample… Let’s say the last price paid for BTC was $10,000. So the ‘market cap’ of Bitcoin, assuming 17 million Bitcoin outstanding, is: $10,000 x 17m = $170,000,000,000 ($170bn)

Now, let’s say you want to buy a tiny amount of BTC (say $10 worth), and the best price that you can see is $10,002. So you pay $10 and buy 0.0009998 BTC ($10 divided by $10,002 per Bitcoin). What has happened to the ‘market cap?’ It is now: $10,002 x 17m = $170,034,000,000.

The market cap has increased by $34 million just because of your measly $10 trade! You didn’t ‘pump in’ $34 million, but the market cap increased by that amount. So clearly the earlier argument is wrong.

Having said that…of course if there are more buyers with a greater desire to buy and pay whatever it takes to accumulate BTC, then the prices will increase. Likewise, if there are sellers who will sell bitcoins at any price, then prices will fall.

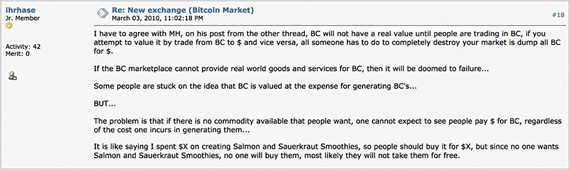

I also hear variations on, ‘cost of creation’ argument: The price of Bitcoin should be at least the cost of mining them, so the cost of mining puts a floor under the price of Bitcoin, and as difficulty increases, it costs more to mine bitcoins, so the price should rise. Alas, this is also false. The cost incurred by a miner (or even all the miners in aggregate) bears no relation to the market price of Bitcoin. The price of Bitcoin affects the profitability of miners, but there is no rule dictating that miners need to be profitable. If a miner is unprofitable, they will eventually stop mining, but this doesn’t affect the price of bitcoins. If it costs me $5,000 to dig up 1 oz of gold, this doesn’t mean the price of gold should be at least $5,000/oz. User ihrhase explains this with salmon and sauerkraut smoothies in a forum post239 in 2010:

Unfortunately, I have not yet come across a reasonable fair value model for cryptocurrencies.

ICO tokens should be easier to price. These tokens are redeemable for a certain good or service in the future, so putting a price on the token should be a case of figuring out what that good or service is worth. Right?

Alas, it is never that easy. The fact is that ICOs who issue tokens want the price of their tokens to go up, as do their investors. Redemption is always described generically and not quantified. For example, they say, ‘Tokens will allow you access to cloud storage,’ rather than, ‘One token will give you 10 GB of cloud storage for 1 year starting in 2020’. This is a deliberate strategy. If the issuers quantified the goods or services, you could figure out an appropriate ballpark price for the token. But this would constrain the price, preventing the price of the token from massively increasing (which is really what ICO issuers and investors really want). I have never seen an ICO whitepaper quantify exactly what a token will be redeemable for.

Who Controls the Price of Utility Tokens?

The simple answer might seem to be ‘the market’ or ‘buyers and sellers,’ but this is not the full picture as we have an issuer who can pull some tricks to affect the value of a token. Initially, the quantity of goods/services that the tokens can buy is unspecified, so the price of the token is subject to normal cryptocurrency market forces, and there is no way to do fundamental analysis on what a fair market price should be (you can’t price ‘cloud storage’ without quantifying how much, for how long). During this period, some ICOs exert some influence on the price of their tokens by buying them up when the price falls. Some ICOs even discuss this strategy in their whitepapers. ICOs often retain a significant amount of tokens in their treasury, so they can sell some if the price rallies too aggressively. Essentially, they may act like a central bank of their tokens, managing the price.

Later, there comes a point when the project has to make a decision: Do they set prices in fiat or in tokens? Should 1 GB of cloud storage for 1-year cost $10, payable in tokens at market rate, or should 1 GB of cloud storage for 1-year cost one token?

Let’s explore the options.

1) Priced in fiat, paid in tokens

If this is the case, then at first you’d think that the price of tokens should be irrelevant. Customers hold fiat, then when they want to use the service, they buy the tokens then quickly redeem them. This process could be automated so the customer doesn’t know it is going on in the background. This is the same argument that remittance-by-Bitcoin companies use when they say that the price of Bitcoin is irrelevant to their business.

In this case, are tokens a good investment? Perhaps. As tokens are redeemed against the issuer, fewer and fewer of them exist in circulation, so long as the project does not re-issue them and sell them for fiat to pay their staff. Fewer tokens may mean a higher price due to scarcity. So a project in good financial health, not reliant on reselling redeemed tokens to pay their costs, can allow tokens to become more scarce over time, perhaps putting upwards pressure on their price. Perhaps. But a project in poor financial health will need to keep reselling their tokens to cover their costs. So actually, the financial health of the company may impact the pricing pressures on the token.

2) Priced in tokens, paid in tokens

This is wonderful: if the company sets the price of the goods or services in tokens, the company will have control over the value of their tokens, just as an airline controls the value of the air miles they issue. How does this work? Unless the product or service is unique, customers will have some idea about how much they are willing to pay for it. Imagine that a competitor sells a similar product for $10. If the project wants their tokens to be worth $10, then they set their product at a price of one token. If they want their tokens to be worth $20, then they set their product at a price of 0.5 tokens! The competitor’s pricing helps to peg the token’s price and as long as the products are somewhat substitutable, the project can make their tokens worth whatever they want. They should understand that as they do this, their liabilities change. Their liabilities are the outstanding tokens in circulation, and by changing the price of one product from one token to 0.5 tokens, existing tokenholders can redeem tokens for twice as many products.

If the company decides to price their product in tokens, are tokens a good investment? Probably. The founders of the project, provided they haven’t done a quick exit scam, also hold tokens and are financially incentivised to keep the price of tokens high and relatively stable.

So, projects have more control over their token price if they price their services in tokens, and I would expect that, as projects come to maturity, we will see projects priced in tokens, providing that the projects haven’t been shut down for violating securities regulations first.

Anshuman Mehta attempted to price a fictional utility token on his blog240 and concluded that, ‘In a fiat currency world, the market or traded price of the token is completely de-linked with the usage and velocity of the token’.

Cryptoasset prices are volatile and many have fallen to zero. At time of writing, deadcoins.com241 lists over 800 coins whose price has fallen to zero. I expect this number to increase. The price of any cryptoasset can potentially fall to zero or near zero. This scenario may seem less likely for popular cryptocurrencies; time, a significant hack, or exploited vulnerability could cause a fatal loss of confidence in the asset at any time.

Liquidity risk is the risk that the market cannot support your transaction at the price you expect. Liquidity comes and goes, as with all markets. Less popular coins are less liquid, meaning that a large buy or sell can move the market against you more than expected.

With less popular coins or coins of regulatory uncertainty, there is also a risk that they are de-listed by exchanges, which reduces their liquidity. For example, in May 2018, Poloniex announced that they were de-listing seventeen tokens:

It is convenient to keep assets on exchanges because you don’t have to deal with private keys, and you can quickly trade between assets. However exchanges have had an extremely poor track record of keeping customer assets secure. Nearly all exchanges have been hacked in the past. Michael Matthews published a list242 of a selection of cryptocurrency exchange hacks between 2012 and 2016:

|

Date |

Bitcoin Service Targeted |

Attack Details |

BTC Stolen |

USD Value |

|

2016 Aug |

Bitfinex (exchange) |

user wallets/inside job |

119,756 |

$66,000,000 |

|

2016 May |

Gatecoin (exchange) |

hot wallet |

multicurrency |

$2,000,000 |

|

2016 Mar |

ShapeShift (exchange) |

inside job |

multicurrency |

$230,000 |

|

2016 Mar |

Cointrader |

hot wallet |

81 BTC |

$33,600 |

|

2016 Jan |

Bitstamp (exchange) |

hot wallet |

18,866 |

$5,263,614 |

|

2015 Feb |

Bter (exchange) |

cold wallet/inside job |

7,000 |

$1,750,000 |

|

2015 Feb |

Exco.in (exchange) |

cold wallet/inside job |

n/a |

n/a |

|

2015 Feb |

Kipcoin (exchange) |

cold wallet/inside job |

3,000 |

$690,000 |

|

2015 Feb |

796 (exchange) |

cold wallet/inside job |

1,000 |

$230,000 |

|

2015 Jan |

Bitstamp (exchange) |

hot wallet |

19,000 |

$5,100,000 |

|

2015 Jan |

Cavirtex (exchange) |

user database stolen |

n/a |

n/a |

|

2014 Dec |

Blockchain.info (wallet) |

user wallets (bug, R values) |

267 |

$101,000 |

|

2014 Dec |

Mintpal (exchange) |

inside job |

3,700 |

$3,208,412 |

|

2014 Aug |

Cryptsy (exchange) |

inside job |

multicurrency |

$6,000,000 |

|

2014 Mar |

Flexcoin (wallet) |

hot wallet |

1,000 |

$738,240 |

|

2014 Mar |

CryptoRush (exchange) |

cold wallet/inside job |

950 |

$782,641 |

|

2014 Jan |

Mt.gox (exchange) |

hot & cold wallets/inside job |

850,000 |

$700,258,171 |

|

2013 Dec |

Blockchain.info (wallet) |

2-factor authentication breach |

800 |

$800,000 |

|

2013 Nov |

Inputs.io (wallet) |

cold wallet/inside job |

4,100 |

$4,370,000 |

|

2013 Nov |

BIPS (wallet) |

cold wallet/inside job |

1,200 |

$1,200,000 |

|

2013 Nov |

PicoStocks (exchange) |

cold wallet/inside job |

6,000 |

$6,009,397 |

|

2012 Mar |

Linode (webhosting) |

inside job |

46,703 |

$228,845 |

From this analysis, we can see not only that exchanges have been successfully hacked by external parties, but it is not unknown for staff at exchanges to steal cryptocurrencies from their customers.

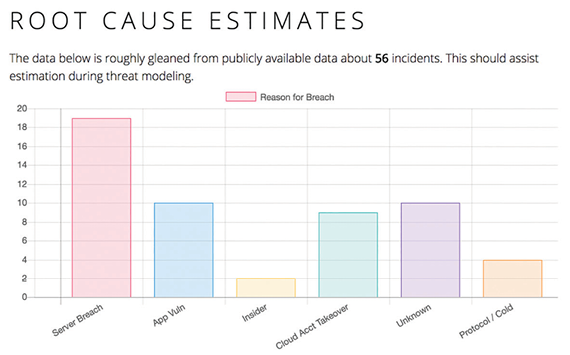

On his website, Blockchain Graveyard243, Ryan McGeehan manages a list of security breaches and thefts with their causes, based on public information. The root cause analysis shows that there are multiple ways for exchanges to be hacked:

Being hacked is an existential threat to exchanges. So the top exchanges take security extremely seriously. Nevertheless, prudence suggests that you should use exchanges only when necessary, and to withdraw funds as soon as possible after trading. Only keep as much on an exchange as you are willing to lose.

Exchanges and users of exchanges may also engage in illegal or unethical activity. Tricks, borrowed from the wholesale financial markets industry, include:

•Painting the tape: Artificially increasing trading activity by having parties controlled by the exchange repeatedly trade with each other. This ‘fake volume’ encourages other customers to trade.

•Spoofing: Submitting orders with the intention of cancelling them before they are matched. This trick can be used to drive prices up or down.

•Front-running: An exchange can see a customer order and use the information to trade before the customer’s order is accepted.

•Running stops: A certain type of customer order, called a ‘stop loss,’ is not visible to other customers of the exchange but is visible to the exchange. Insiders who can see customer stop loss orders can use this information to trade against their own customers. This is a popular trick in FX markets.

•Fake liquidity: Exchanges can publish ‘unfillable’ orders that disappear, or only partially fill, when a customer tries to match them. This makes it look like there is more liquidity on the exchange than there actually is.

There are many other tricks that may be used either by exchanges or by customers of exchanges while the management of the exchange looks the other way. Different exchanges behave with different levels of professionalism. Many exchanges are dodgy. Do your own research!

With wallets, there is a trade-off between security and convenience. Wallets that run online on computers or smartphones are convenient because it is easy to make cryptocurrency payments. However, storing private keys on a device exposed to the internet is not advised. Some people keep a small amount of cryptocurrency on their phone wallet so they can make payments instantly, but the advice, again, is to keep only as much in them as you are willing to lose244.

In the past, it was common for people to print private keys onto bits of paper, a technique known as cold storage, discussed previously, but this is troublesome for making payments. Now, hardware wallets are the best compromise between security and convenience. But the risk remains with any wallet type that the software contains bugs or vulnerabilities that can be exploited. Many wallets open source their code to allow developers and security professionals to understand exactly how the wallet works, and to take comfort that there are no weaknesses, but this also provides transparency to hackers.

Regulation around cryptocurrencies and tokens is evolving. It is worth understanding as fully as possible the nature of the assets you are considering. ICOs are operating in a legal grey area in many jurisdictions, and there is a risk that some are deemed to have been illegally performing regulated activities.

Depending on the jurisdiction and classification of cryptoassets, and what you are doing with them, tax also needs to be considered. You are not excused from complying with tax regulations just because the assets are recorded on blockchains!

Finally, due to the nature of the cryptocurrency industry, many scams operate. Hype, technical complexity, regulatory uncertainty, and naïve investors hoping to make a quick buck all make for an environment ripe for fraudsters. Some popular scams are:

•Ponzi schemes: Investors are promised good returns and old investors are paid with new investors’ money.

•Exit scams: Founders of a project, wallet, exchange or investment scheme run off with customer money.

•Fake hacks: Project gets hacked by an associate who shares profit with the project team.

•Pump & Dumps: Illiquid coins are bought cheaply by fraudsters then hyped on social media and sold at a higher price to new investors.

•Scam ICOs: ICO raises money with no intention of delivering a product. Sometimes they will list well known industry experts as advisors or as part of the team to get credibility, without the knowledge or approval of the expert.

•Spoof ICOs: Clones of real ICO websites made with the scammer’s deposit address instead of the legitimate deposit address.

•Scam mining schemes: Claims that investors will earn lots of cryptocurrency but key information such as difficulty increases is not disclosed.

•Fake wallets: Wallet software that allows the scammer to access private keys, so the coins can be stolen from the user.

And so on. There are many variations to these, and scammers are proving increasingly innovative!

I hope this chapter has given you some food for thought. People have made and lost fortunes trading cryptocurrencies and investing in ICOs, but there are many risks. If you do decide to get involved, be careful and do a lot of research before committing your money.