Where do we start? There are so many cryptocurrencies, each working differently with different rules and mechanisms, that is it not particularly easy to make accurate generalisations: however you describe cryptocurrencies, there are bound to be exceptions. For example, Bitcoin uses a mechanism called ‘proof-of-work’ to ensure that anyone (in theory, at least) can add blocks to the blockchain at a certain cadence without a central actor coordinating access or providing permission. Proof-of-work creates a fair competition between block adders who compete to add blocks. This competition consumes electricity—a lot of it75—which is one reason some people describe Bitcoin as wasteful. However not all cryptocurrencies, and certainly not all blockchain technologies, work this way. So it is inaccurate and therefore unhelpful to generalise and say ‘cryptocurrencies’ or ‘blockchains’ are energy intensive. Just because Bitcoin works in a certain way, it doesn’t mean everything else does.

Bearing this in mind, we will nevertheless start by getting a good grounding in how Bitcoin works, and then later describe some of the differences between Bitcoin and other cryptocurrencies and their respective blockchain protocols (all to be explained—do not fear!).

People refer to Bitcoin as a digital currency, virtual currency, or cryptocurrency, but it may be easier to think of it as an electronic asset. The word currency often side-tracks people when they are trying to understand Bitcoin. They get caught up trying to understand aspects of conventional currencies which do not apply to Bitcoin, for example, what backs it (nothing) and who sets the interest rate (there is none). Bitcoin is also sometimes described as a digital token, and in some respects that is accurate; but, alas, the term token is now also used to mean something more specific, which we will cover later, so the ambiguity of this term too is best avoided.

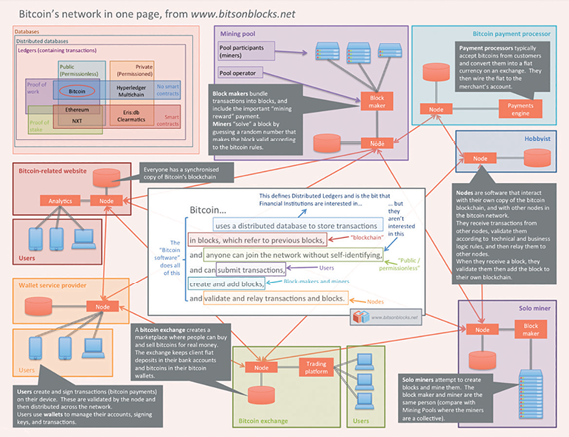

Bitcoins are digital assets (‘coins’) whose ownership is recorded on an electronic ledger that is updated (almost) simultaneously on about 10,000 independently operated computers around the world that connect and gossip with each other76. This ledger is called Bitcoin’s blockchain. Transactions that record transfer of ownership of those coins are created and validated according to a protocol—a list of rules that define how things work and which therefore govern updates to the ledger. The protocol is implemented by software—an app—that participants run on their computers. The machines running the apps are called ‘nodes’ of the network. Each node independently validates all pending transactions wherever they arise, and updates its own record of the ledger with validated blocks of confirmed transactions. Specialist nodes, called miners, bundle together valid transactions into blocks and distribute those blocks to nodes across the network.

Anyone can buy bitcoins, own them, and send them to other people. Every Bitcoin transaction is recorded and shared publicly in plain text on Bitcoin’s blockchain. Contrary to many media articles, Bitcoin’s blockchain is not encrypted. By design, everyone sees all details of all transactions. Anyone can, in theory, create bitcoins for themselves too. This is part of the block creation process, called mining, and is described later.

The purpose of Bitcoin is described in its whitepaper—a short document written by a pseudonymous Satoshi Nakamoto, published in October 2008. It describes why Bitcoin exists and how it should work. It is worth reading the whitepaper in full. It is only nine pages long and available online77. The abstract says:

A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution. Digital signatures provide part of the solution, but the main benefits are lost if a trusted third party is still required to prevent double spending. We propose a solution to the double spending problem using a peer-to-peer network. The network timestamps transactions by hashing them into an ongoing chain of hash-based proof-of-work, forming a record that cannot be changed without redoing the proof-of-work. The longest chain not only serves as proof of the sequence of events witnessed, but proof that it came from the largest pool of CPU power. As long as a majority of CPU power is controlled by nodes that are not cooperating to attack the network, they’ll generate the longest chain and outpace attackers. The network itself requires minimal structure. Messages are broadcast on a best effort basis, and nodes can leave and rejoin the network at will, accepting the longest proof-of-work chain as proof of what happened while they were gone.

That first sentence says it all. It sets out the purpose of Bitcoin, and how Bitcoin derives both value and utility. For the first time in history, we have a system that can send value from A to B, without the physical movement of items or using specific third-party intermediaries. It is difficult to overstate how important a milestone this is in the evolution of payments. I get shivers down my spine every time I think of Bitcoin like this78. As popularised by cryptocurrency industry commentator Tim Swanson79, Bitcoin is designed as censorship resistant digital cash.

There is no mention of a blockchain or ‘block chain’ at all in the original Bitcoin whitepaper, even though we are constantly reminded by the media that Bitcoin is built on blockchain or that blockchain is the underlying technology of Bitcoin. A chain of blocks was not the purpose of Bitcoin, it is just the design that was developed to achieve the objective—the solution to the business problem.

The Bitcoin blockchain is managed by software running on computers that communicate with each other forming a network. Although multiple compatible software implementations exist, the most commonly used software is called ‘Bitcoin Core’ and source code to this software is published on GitHub80. This software contains the full range of functionalities needed for the network to exist. It has the ability to perform the following tasks which will be explained in this section:

•Connect with other participants in the Bitcoin network

•Download the blockchain from other participants

•Store the blockchain

•Listen for new transactions

•Validate those transactions

•Store those transactions

•Relay valid transactions to other nodes

•Listen for new blocks

•Validate those blocks

•Store those blocks as part of its blockchain

•Relay valid blocks

•Create new blocks

•‘Mine’ new blocks

•Manage addresses

•Create and send transactions

However, in practice, the software is usually only used for its bookkeeping function, which will be explained in depth in this section.

To understand how Bitcoin works, and why it works the way it does, it is important to keep in mind the objective: to create an electronic payment system that cannot be censored, and to allow anyone the ability to send payments ‘directly from one party to another without going through a financial institution’.

Such a system cannot have a central administrator managing the ledger, as that administrator would be the financial institution that Bitcoin is set up to avoid. The system therefore needs to be able to be operated by anyone, without any need to identify themselves or gain permission from a gatekeeper. The moment that parties need to identify themselves, they lose privacy and are vulnerable to interference, coercion, prison, or worse. This goes for both administrators of the system and users themselves. So every single part of the solution needs to work with these constraints in mind.

How did Satoshi go about designing the solution? Let’s start with a classic centralised model and then try to decentralise it. In this way, we can build up the design of Bitcoin step by step.

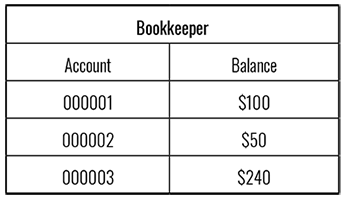

Classic Centralised Model

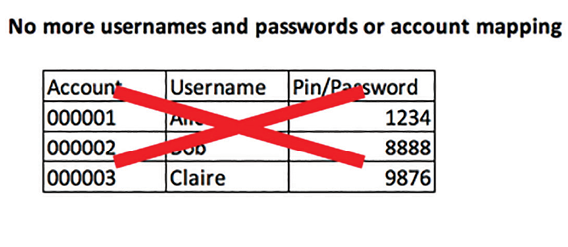

Let’s start with a ledger which keeps tracks of balances, managed by an administrator. You can think of it as a list with two columns: Account, Balance81.

Classic centralized model

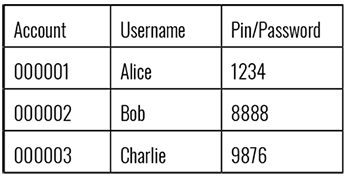

The administrator assigns account numbers to customers, and customers make payments by instructing the administrator. There is an authentication process where the customer proves that they are the account holder before the administrator will carry out the payment instruction. So each customer is named and, for security, has a password linked to their account.

Account mapping

The administrator maintains the central record of balances and makes all payments. They are responsible for ensuring that no one spends money they don’t have or spends the same money more than once, the ‘double spend’.

But if we want resistance to control and censorship, and to allow anyone to be able to transact with anyone else, we need to remove the administrator.

First, let’s remove the administrator from the account opening process, so that anyone can open an account without needing permission from the administrator.

Problem: Accounts Need Permission

Someone has to set up an account and assign it to you. It is the administrator’s job to assign you an unused account number then set you up with some sort of username (which may be your own name) and password so that when you ask the administrator to make a payment on your behalf, the administrator knows it is really you making the request. In setting up your account the administrator has granted permission for you to open the account, and may, equally, choose to refuse that permission. Any time you have an entity that can approve or deny something, you have a point of third party control. We are trying to eliminate third party control.

Is there a way you can open an account without having to ask permission? Well, cryptography provides a solution.

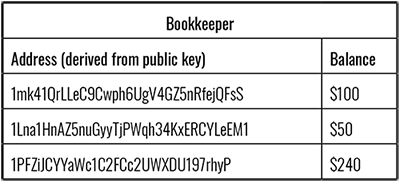

Solution: Use Public Keys as Account Numbers

Instead of names or account numbers and passwords, why not use public keys as the account number, and digital signatures instead of passwords?

By using public keys as account numbers, anyone can create their own accounts with their own computer without having to ask an administrator for an account number. Remember, a public key is derived from a private key, which is a number picked at random. So you create an account by picking a random number (your private key) and doing some maths on it to get your public key. In Bitcoin and most other cryptocurrencies, account numbers are mathematically derived from public keys (not public keys themselves), and are called addresses.

Using user-generated addresses instead of accounts

You can tell the world this Bitcoin address to allow people to pay to it82. No one can spend anything from it unless they have the private key, which only you have. You can also create as many addresses as you want and your wallet software will manage all of them for you.

Could someone else already be using an address that you randomly picked? Possible, but unlikely. We saw in the cryptography section that Bitcoin’s scheme uses a random number between 0 and 115,792,089,237,316,195,423,570,985,008,687,907,853,269,984,665,640,564,039,457,584,007,913,129,639,935 as a private key. There are so many private keys available that the possibility of stumbling across someone else’s account is virtually nil. As one commentator put it, ‘Go back to bed and don’t worry about this ever happening’. 83

Public/private keypairs also solve the authentication problem. You don’t have to log in to prove that you are the account holder. When sending a payment instruction you digitally sign the transaction with your private key, and this signature proves to the administrator that the instruction is indeed coming from you, the account holder. You can create and sign the transaction offline without being connected to any network. When you broadcast the signed transaction to the administrator, all the administrator has to do is check that the digital signature is valid for the respective account number, rather than maintain a list of usernames and passwords for you and all transacting parties.

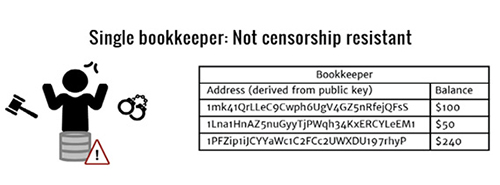

Problem: Single Central Bookkeeper

We have now eliminated the role of the third-party administrator in creating accounts. But we still have the third-party administrator in the role of central bookkeeper—the coordinator who maintains the list of transactions and balances and who both validates and orders the transactions you request against some business and technical rules. This single point of control ultimately decides what is reflected in your account, whether your transaction goes through or not. As a single point of control, it is classified as a financial institution, and has the regulatory burden of having to identify you and all other customers, a process known as Know Your Customer or KYC. It can also be coerced to censor transactions.

So, for a digital cash system resistant to third party influence, including control and censorship, we need to remove that single point of control84.

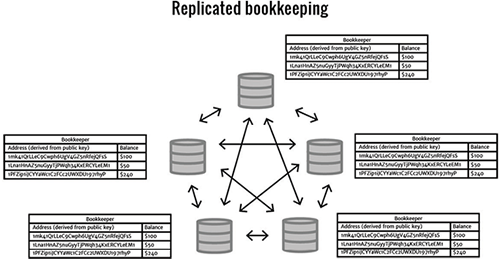

Solution: Replicate the Books

The more people you have sharing a secure system and its information, the less vulnerable that information is to manipulation. However, a group of ‘trusted bookkeepers’ would inevitably require their own gatekeeper, so we would be back to the central point of control problem again. The solution is for anyone anywhere to be able to be a bookkeeper without asking permission from anyone else and without hierarchy. And all bookkeepers, wherever they are, maintain the same complete books of record and are peers of equal seniority, with checks and balances such that if any single bookkeeper were forced to try to censor a transaction or manipulate the database, the others would ignore or exclude them.

As long as all bookkeepers maintain identical records of which transactions are included and which excluded, we have a more resilient system. If any individual bookkeeper is forced to stop work, the others can continue. Anyone is able to join this network of bookkeepers without needing permission from anyone else. So the network is resilient to anyone joining or leaving at any time.

In Bitcoin, any individual with a computer, adequate storage, and access to internet bandwidth can download some software (or write their own), connect to a few neighbours, and become a bookkeeper.

New transactions are broadcast to all bookkeepers via a gossip network, and each bookkeeper relays new transactions to as many others as they are connected to. This ensures eventual propagation of transactions to all bookkeepers.

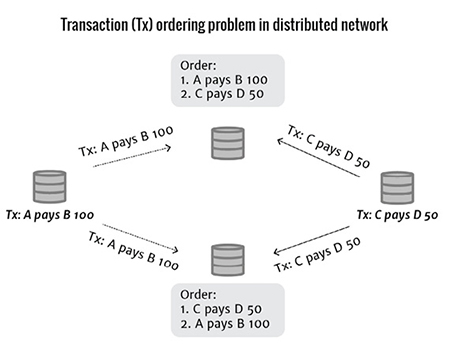

Problem: Transaction Ordering

How do multiple bookkeepers stay in sync with each other? Every bookkeeper will have a different idea of the order of transactions. Given that there could be hundreds of transactions being created anywhere in the world, and given that it takes some time for these to fully propagate across the network, if every bookkeeper tried to put these transactions in order, there would be many conflicting versions of the ‘correct’ order of transactions. What happens if a bookkeeper in China receives transaction A then transaction B, whereas a bookkeeper in the USA receives transaction B first, then A?

Geography, technology, connectivity, internet traffic, servers, and bandwidth all influence the speed and order in which transactions originating anywhere in the world manifest themselves everywhere else. Your ordered list of transactions as manifest, say, in London is going to be very different from someone else’s list, even next door, let alone in, say, Lagos, New York, Auckland, or Nairobi.

How do we get an agreed ordering of transactions?

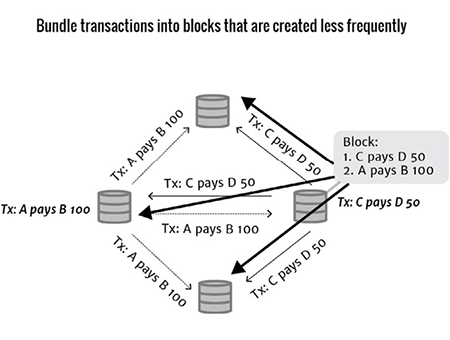

Solution: Blocks

We can’t control how many transactions can be created per second, but we can control the data entry into the ledgers. We can do this by recording transactions in batches, page by page instead of transaction by transaction. Individual transactions, validated as ‘pending’ transactions, can be passed around the network, then entered into the books in less frequent batches. We call these batches blocks!

Blocks are created much less frequently than transactions, so it is more likely that a block reaches all bookkeepers in the network before another one is created. This means that a bookkeeper now performs two functions:

1.Validating and propagating ‘pending’ transactions

2.Validating, storing, and propagating blocks of transactions

By slowing down the ‘data entry’ process of the bookkeeping system, bookkeepers around the world have more time to agree on the ordering of blocks of transactions. So rather than all bookkeepers needing to agree on the order of transactions, they need to agree on the order of blocks which are generated less frequently. Because there is more time to agree on the order of blocks, there are fewer differences in opinion about block ordering, and so a greater chance of network-wide consensus. Later we will see how the network deals with conflicting blocks.

Once your transaction is bundled along with other transactions into a valid block, and that block is passed around the network, the transaction is said to be ‘confirmed’ with one confirmation. When the next block is added, on top of the block with your transaction, your transaction is confirmed with two confirmations. As new blocks arrive on top of the initial block, your transaction is deeper in the ledger and becomes more and more confirmed. This is important because there are situations where the very top of the chain, i.e., the newest blocks, may be replaced by other blocks, kicking out transactions which looked like they have already been confirmed85. We will look into the ‘longest chain rule’ later.

There is a trade-off between the ease with which bookkeepers can agree on the ordering of transactions and the speed at which valid transactions are written into the blockchain. Having blocks created, say, once per day would make it very easy for all bookkeepers to agree on the ordering of those blocks, but this is longer than people want to wait for their transactions to be confirmed.

In Bitcoin, blocks are created every 10 minutes on average. Different cryptocurrencies have different block creation target times.

Problem: Who Can Create Blocks, and How Often?

We have seen that it makes sense to batch pending transactions into blocks that are propagated around the network. Bookkeepers add those blocks to their own ledgers. As we will see later, if there are discrepancies or competing blocks, they use the ‘longest chain rule’ to decide which block wins.

Firstly, we need to manage the creation and frequency of blocks. How can we do this? If one party gathers up all the pending transactions, puts them into blocks, and sends the blocks to all the bookkeepers then we are back to a single, centralised control point, which we have set out to avoid.

So anyone, without permission, needs to be able to create blocks and send them around the network. But then how do we control the speed at which blocks are created? How do we get a bunch of anonymous block-creators to take it in turns and ensure that they don’t create blocks too quickly or too slowly?

Could the bookkeepers themselves have a rule to accept blocks only a minimum ten minutes after the last block they saw, to make it pointless for someone to try to create blocks at more frequent intervals? Due to the latency of the internet, this may create some unfair advantages (we don’t know the precise time when any individual bookkeeper received the latest block, and we can’t trust timestamps on blocks because these can be easily faked), and we also can’t trust the individual bookkeepers who might alter this rule, or their computer’s clock, and accept their own blocks sooner than 10 minutes.

Perhaps, we could have a conductor, an entity whose job is to randomly assign the next block-creator, who allows the next block to be created only 10 minutes after the previous one? No, that would not work either, as the conductor would be a central point of control over the network, and we don’t want a central point of control.

So perhaps each block-creator could be randomly assigned, like rolling some virtual dice so whoever gets a ‘double six’ is the next block maker. But that wouldn’t work—how could anyone prove they have or haven’t cheated? Who would roll the dice? How do we randomise the next block-creator and ensure that everyone agrees that it was a fair process?

Solution: Proof-of-Work

The solution is extremely elegant. The solution is that all block-creators have to play and win at a game of chance, a game that in aggregate, over the whole network, takes some specific amount of time to play (say 10 minutes on average).

The game must give all block-creators an equal chance of winning. The game must not have a barrier to entry, else the gatekeeper would be a central point of control. The game must not have shortcuts, and the game needs to have a publicly displayable proof so that the winner can prove they have won. The game must not be cheatable.

The prize? Being allowed to create the next block.

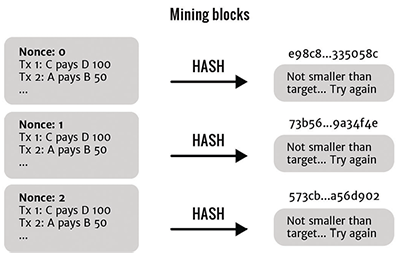

The game of chance that Bitcoin uses is called ‘proof-of-work’. Each block-creator takes a bunch of transactions that they know about, but which have not yet been included in any previous blocks, and builds a block out of them, in a specific format. The creator then calculates a cryptographic hash from the block’s data86. Remember that a hash is just a number. The rule of Bitcoin’s proof-of-work game of chance says, if the hash of the block is smaller than a target number, then this block is considered a valid block which all bookkeepers should accept87.

What if the hash of the block is bigger than this number? Does the specific block-creator bow out for this turn? No. The block-creator needs to alter the data going in to the hash function and try hashing the block again. They could do this by removing a transaction from the block, or adding a new transaction, or changing the order of transactions in the block, but these are not elegant and eventually you might run out of permutations. You don’t really want to mess around with the transactions in a block.

The solution in Bitcoin is that in every Bitcoin block there is a special part of the block that block-creators can populate with an arbitrary number. Its only purpose is to allow block-creators to fill it with a number, and change the number if the hash block doesn’t meet the ‘hash is smaller than a target number’ rule. So, if the first hash attempt doesn’t result in a winning hash, then they can just change the number in this part of the block. This number is called the ‘nonce’ (number once) and is completely separate from the financial transactions in the block. Its only job is to change the input data for the hash function.

So each block-creator puts together a block and fills the nonce field with the number and hashes the block. If the result meets the ‘hash is less than a target number’ rule for valid blocks, then they have created a valid block, and can send it to the bookkeepers, and get to work on the next block. If the result doesn’t fit the rule, then they change the nonce (e.g., by adding 1) and hash again. They do this repeatedly until they find a valid block. This is a process known as mining.

This is elegantly described as a scratch-off puzzle in a paper by Miller et al entitled “Nonoutsourceable Scratch-Off Puzzles to Discourage Bitcoin Mining Coalitions”88. Like scratch-off lottery cards, each miner has to expend a bit of effort scratching off a puzzle to see if they have a winning ticket.

So the authority to create a valid block is not given by a third party but is self-assigned by repeating some tedious mathematical algorithms, which all computers can do89. Note that mining is a tedious, repetitive job. Take some transactions with the nonce, hash it, see if the hash is smaller than a certain number, and if not, repeat with a different nonce. It is not ‘solving complex mathematical problems’ as is widely described in the media. Hashing is easy but boring! You can even do it by hand using pencil and paper if you have the patience, though you would be unlikely to win a block with only these tools to power you. Ken Shiriff did a round of hashing by hand with pencil and paper without a calculator, and you can watch him do it on his blog90.

In this way, anyone can be a block-creator and create valid blocks. They then send the valid blocks to the bookkeepers. The only thing that the bookkeepers have to do is to take the block, including the nonce, and hash it once to verify for themselves that the hash of the block is less than the target number.

Proof-of-work also avoids another kind of attack, a Sybil attack. A Sybil91 attack is when a network is overwhelmed by multiple forged identities all under the control of a single actor. Think Facebook or Twitter bots… loads of usernames but all under control of a small number of bad actors.

In Bitcoin, your chance of winning a block is proportional to how much hashing power you control. In the Bitcoin whitepaper this described as ‘one-CPU-one-vote’. If Bitcoin had given each node (each block-adder) an equal chance of winning a block (one node, one vote), the Sybil attack would be to create unlimited numbers of block adders and try to win all the blocks. Creating multiple identities is very cheap for attackers to do. So proof-of-work works well as a solution to this kind of Sybil attack because proof-of-work is computationally expensive, and this in turn means expensive in terms of electricity and hardware (i.e., cash), which means it is expensive to try to overwhelm the network with hashing power, which in turn increases the attack costs to a bad actor. If you have all of this hashing power available, you might as well put it to work finding blocks and making money (well, bitcoins) instead of trying to subvert the network, so the theory goes.

Problem: Incentivising Block-Creators

But all of this tedious hashing needs resources: computers, electricity, bandwidth… and this all costs money. Why should anyone bother creating blocks? What’s in it for them? How can we incentivise the block-creators to create blocks and keep the system running?

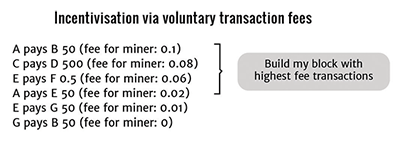

Solution: Transaction Fees

The solution is to pay the block-creators for their time and resources! But who is going to pay them and in what currency? An external payment or incentivisation mechanism, i.e., a third party paying the block-creators, would centralise and gate the process, defeating the purpose of censorship resistance, so that will not work. US dollars or any fiat currency would not work either, as fiat is held in bank accounts and banks can be instructed to freeze accounts.

An internal or intrinsic incentivisation scheme avoids third party control. This is implemented as a per transaction fee, so the block-creator gets a commission, a small amount of value, from each transaction. This could be specified as a percentage or a flat rate for all transactions and encoded into the rules of the system—a bit like the ‘10 minutes per block’ rule. But it is difficult to establish the right fee. Bitcoin’s solution is a market-based approach where people creating transactions add their own voluntary transaction fees, and the block-creators can prioritise those transactions with higher fees over those with lower fees.

When Alice creates her Bitcoin transaction she can optionally add a fee that is collected by the lucky miner who mines her transaction92. This fee allows miners to prioritise her transaction over others, who are all competing to get in a block. Blocks are limited by network rules, as to how much data can squeeze into a block. In Bitcoin, this limit is nominally 1 MB93. Fees tend to go up in times where there are many transactions queuing up to get into blocks, and down again in times with fewer transactions.

Problem: How to Bootstrap?

How were block-creators incentivised to keep creating blocks in the early days or, indeed, now during slack periods when there may be periods where there are no transactions for some hours? The hashing work consumes electricity and costs miners’ money.

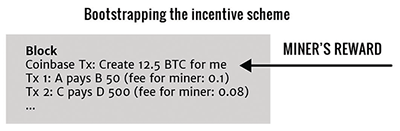

Solution: Block Rewards

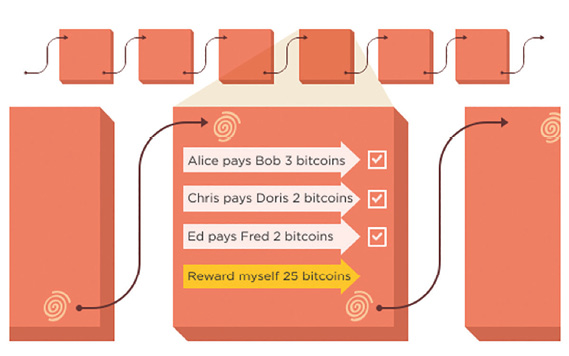

The second, and currently much larger, incentive for block-creators to create blocks is the ‘block reward’. In effect, the block-creator can write a cheque to themselves once per block, for up to a certain amount. The idea is that block rewards can kick start the system, and then be phased out gradually, with transaction fees to replace them.

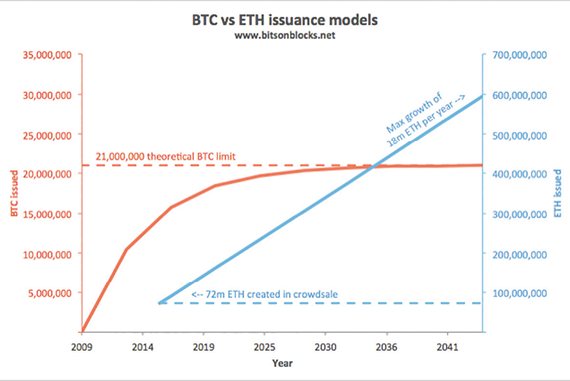

The very first transaction in a block is called the coinbase transaction94. This coinbase transaction is special because it is the only transaction that creates bitcoins. All other transactions move bitcoins between addresses. The block-creator can create a transaction that pays any address (usually themselves) any number of bitcoins, up to a limit specified by the Bitcoin protocol. This limit was 50 BTC per block in 2009 and reduces by half every 210,000 blocks, which at 10 minutes per block, is about every 4 years. Currently (mid-2018) the maximum block reward is 12.5 BTC, with the next reduction to occur on block 630,000, estimated to occur in May 202095. These block rewards have created around 17 million bitcoins to date, and owing to the repeated halving of the block reward, the maximum number of bitcoins created ever will be a sliver under 21 million, the last of which should be created a little before the year 2140. Unless the rules change.

This block reward is the mechanism that keeps block-creators creating blocks. They receive valuable BTC in return for spending resources doing the tedious hashing to create valid blocks. Note that block-creators are under no obligation to include any transactions in their blocks, but they choose to because the transactions themselves contain transaction fees and these also accrue to the block-creator.

The beauty of this system is that the payment for creating blocks comes from the protocol itself rather than from an external third party.

Problem: More Hashing, Faster Blocks, More Monetary Supply

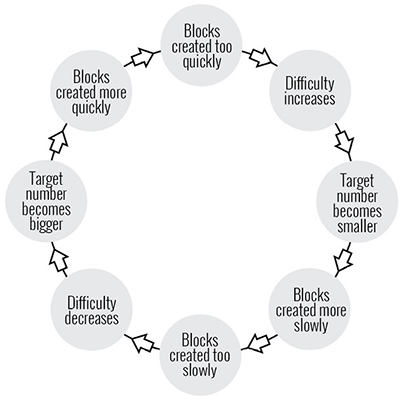

If anyone can create valid blocks by finding the nonce that makes the hash of the block meet a certain criterion and get paid for it, then surely by throwing more computers at the hashing they can create valid blocks more quickly and get paid more! By doubling the amount of hashing power, they can, on average, double the speed at which they can create valid blocks.

But this, unchecked, would cause havoc. With more people throwing more hashing power (i.e., computers) at the block creation process, blocks would be created faster and faster. Remember, we want blocks to be created slowly, so that the bookkeepers have a better chance of staying in consensus. And BTC would be created faster and faster, creating a huge supply and possibly decreasing the value of each unit.

Solution: Difficulty

The network needs to self-correct and slow down if blocks are created more quickly than the target of one block every ten minutes. The answer lies in changing the target number for the hash calculation. Variations in this target number can make it easier or harder for the network, in aggregate, to find hashes that fall below this number. As an analogy, if you have to roll two dice and get a sum total below eight, that is quite easy, but if you have to get a sum total below four then that will take you more rolls. So making the target number smaller slows down the rate at which valid blocks are created.

In Bitcoin, the target number is mathematically calculated from a number called the ‘difficulty’. The difficulty changes every 2016 blocks (which takes about two weeks at ten minutes per block), according to a formula that uses the elapsed time it took to mine the previous 2016 blocks. The faster the previous 2016 blocks were created, the more the difficulty increased. The difficulty and the hashing target number are inversely related, so as difficulty increases, the target number becomes smaller, making it harder and therefore slower to find valid blocks.

The network is beautifully self-balancing. If more hashing or mining power is added, then blocks get created faster for a period of time until the next difficulty change, after which it becomes harder to find valid blocks, slowing block creation down. If mining power leaves the network, then blocks take longer to be found, until the next time the difficulty changes, then difficulty decreases, and blocks become easier to find. And this is all done without a central coordinator.

Problem: Block Ordering

Transactions are bundled into blocks which are like pages in a ledger. These blocks are passed around the network at a slower rate than individual pending transactions would be. But how do you know what order the blocks should be? In a book, each page has a unique page number, and you know that the pages follow in ascending order. If the pages fall out, you can put the book back together again in the right order.

Could the same be done for blocks where each block gets a unique ‘block number’? In principle, yes, but remember that block-creators are competing to mine blocks by hashing their contents and seeing if the hash is smaller than a target number determined by the current difficulty. Imagine that the block 1,000 has just been mined and passed to all the nodes. The miners start mining block 1,001. Someone super sneaky might get to work mining block 1,002 and to try to get ahead of competitors, so that as soon as someone else has found block 1,001, they can submit block 1,002 and claim the block reward. Remember, the miner doesn’t need to populate any transactions in the block, they can just hash an empty block 1,002 that refers to block 1,001 with a coinbase reward transaction and no other transactions. Hmm, that wouldn’t be a good idea, there’d be all sorts of gamesmanship.

What restricts miners to ensure they mine only the very next block? How is ‘mining ahead’ prevented?

Solution: A Block Chain!

Instead of having each block have a ‘block number,’ each block refers to the previous block by its hash. Miners must include the previous block’s hash in the block they are creating.

This means that to mine block 1,002, miners need to know the hash of block 1,001. Until 1,001 has been mined, 1,002 can’t be mined. This forces miners to focus on block 1,001, which in turn includes the hash of block 1,000, and no miner can skip ahead. Thus a chain of blocks is created, held together not by block numbers (which can be predicted) but by block hashes (which can’t). Each block refers to a previous block by the previous block’s hash, rather than by a number that goes up sequentially.

This is the chain of blocks, or blockchain.

A block chain96 where each block includes the hash of the previous block, rather than a sequential block number.

An additional benefit of blocks linking through their hashes is that of internal consistency, sometimes described as immutability. Let’s say the latest block that has been passed around the network is block 1,000. If a rogue bookkeeper attempts to tamper with a previous block, say, block 990, and attempts to republish that block to other bookkeepers, they could:

1.Publish block 990 with new data but using the old hash; or

2.publish block 990 with new data and a new valid hash (i.e., ‘re-mine’ the block).

In the first case, the block will be considered invalid by all other bookkeepers, because it is internally inconsistent (the block’s hash doesn’t match the data inside it), and in the second case, the hash of block 990 won’t match the reference found in block 991. Thus, it is very hard to get away with tampering with any records that already form part of the blockchain—it will be immediately obvious to anyone who you try to convince. This is what is meant when blockchains are described as immutable. Of course, nothing is immutable (can’t be changed), but blockchains are tamper-evident—that is, it is easy for others to tell if data has been modified, accidentally or otherwise.

Problem: Block Clashes / Consensus

There is still a chance that blocks are created by different block-creators at the same time, due to the random process of hashing. If a bookkeeper receives two valid blocks from two different block-creators (miners) and they both reference the hash of the same previous block, how does the bookkeeper know which one to use and which one to throw away? How does the network come to consensus about which block to use? And if a miner receives two valid but competing blocks, how do they know which block to build the next block on?

Solution: Longest Chain Rule

There is another protocol rule called the longest chain rule97. If a miner sees two valid blocks at the same block height then they can mine on either block (usually the first seen) and would keep the other one ‘in mind’. Others will also make their decisions and eventually one of the blocks will have another block mined on it, then another, and another. So the rule is that the longest chain is the chain that should be considered the chain of record, and the block that is discarded is called an orphan.

What happens to the transactions in the orphaned block? They are considered as if they have never been part of a valid block and therefore are ‘unconfirmed’. They will just be included in later blocks along with other unconfirmed transactions, assuming they don’t conflict with the transactions that have already been confirmed in the blockchain.

Problem: Double Spend

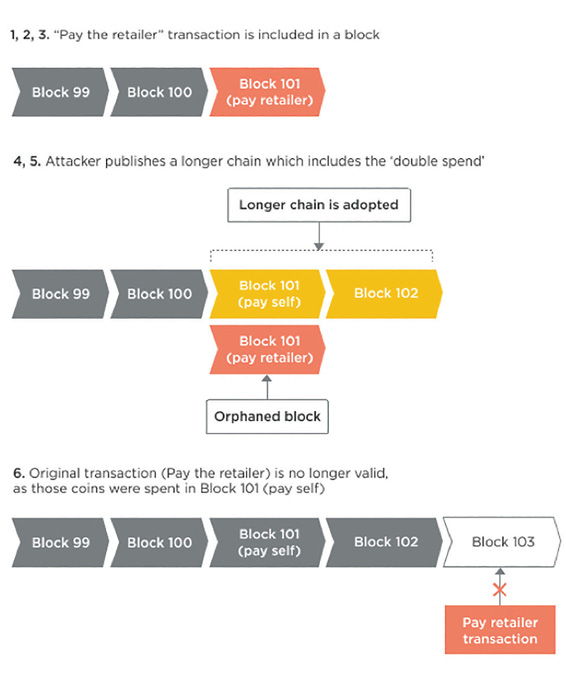

Although the longest chain rule seems sensible, it can be used to create mischief in a deliberate double spend. Here is how you could do it:

1.Create two transactions using the same bitcoins: one payment to an online retailer, the other to yourself (i.e., to another address you control).

2.Only broadcast the transaction that is the payment to the retailer.

3.When the payment gets added in an ‘honest’ block the retailer sees this and sends you goods.

4.Secretly create a longer chain of blocks which excludes the payment to the retailer, and replaces it with the payment to yourself.

5.Publish the longer chain. If the other nodes are playing by the ‘longest chain rule,’ then they will reorganise their blockchains, discarding the honest block containing the payment to the retailer, replacing it with the longer chain you published. The honest block is said to be ‘orphaned’ and, to all intents and purposes, does not exist.

6.The original payment to the retailer will be deemed invalid by the honest nodes because those bitcoins have already been spent in your longer, substituted, chain. You will have received your goods but the payment to the retailer will be rejected by the network.

How to double spend.

Solution: Wait About Six Blocks

Therefore, common advice for people receiving bitcoins is to wait for the transaction to be a few blocks deep (i.e., to have a few blocks mined on top of it). This gives comfort that the transaction is settled and can’t easily be unwound98. At this point the amount of mining that has to be done to create a competing chain longer than the existing chain is enormous,99 so rational miners would prefer to dedicate their hash power towards creating legitimate blocks, receiving the block reward and transaction fees, rather than trying to subvert the network.

To put it another way, it is deliberately hard to generate a valid block. Therefore, if someone wants to replace blocks, they have to create blocks quickly and overtake the rest of the (presumably honest) network. This is another reason why people say Bitcoin’s blockchain is immutable and cannot be changed. However, if more than 50% of the total hash power of the network is used to re-write blocks, then it will be able to do so, because it will create blocks faster than the other, less powerful, half. This is called a 51% attack. Smaller amounts of hash power can also be used to re-write the blockchain, but with a lower probability of success100. 51% attacks have been successfully performed on unpopular coins with few miners.

Which Coins?

Earlier, I used the phrase ‘using the same bitcoins’. What does this mean? With physical cash, each coin or banknote is a unique object. You can’t pay the same coin or banknote to two people. However, digital money doesn’t work that way. In a traditional bank account, all your money is mixed up or co-mingled in a ‘total balance’ figure. Your income goes into the bank account and is immediately jumbled up with all the other money that is in there, like adding water to a half-full bath. When you make a payment your total balance is reduced, like removing water from the bath. You cannot specify which dollar you are spending. For example, when you pay $8 for a coffee, you don’t say, ‘Use $8 from my salary payment that came in on 25 Jan,’ you just say, ‘Use $8 from the pool of money that is my account balance’. This non-specificity promotes the fungibility of digital money, that is, one dollar in an account is exactly the same as another.

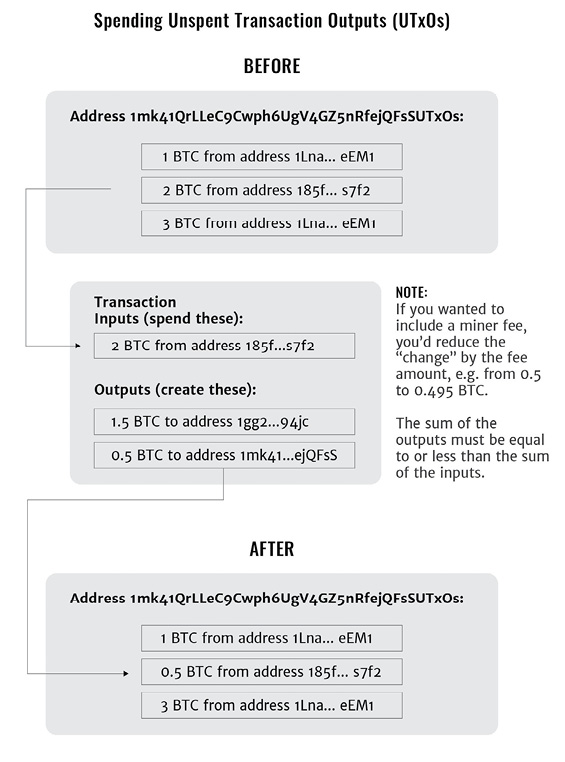

Bitcoin is digital, but it works more like physical cash. With cash you open your wallet and take this specific $10 note which you received earlier and pay $8 for your coffee and expect $2 change. Bitcoin is similar: for every payment you make, you have to specify exactly which coins you are spending—that is, which specific bitcoins that you received earlier. You refer to these received bitcoins by the transaction hash101 that sent the coins to you. In the same way that blocks build on each other by referring to the previous block’s hash, transactions also refer to each other using a previous transaction’s hash. When you make a Bitcoin payment, you say, ‘Take this bundle of money that came in to my account in this transaction, and pay some of it to this account and return the change to me’.

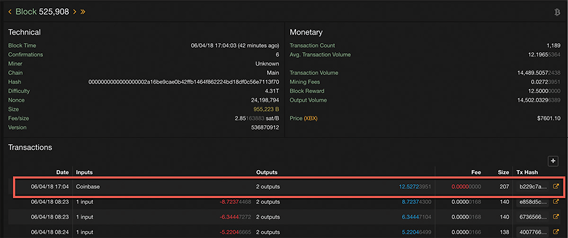

Here is a Bitcoin transaction102. You can see that it takes 1.427 bitcoins from address 17tVxts…QM and sends 0.5999 bitcoins into 1Ce2Qzz…wK and returns 0.827 bitcoins back to 17tVxts…QM. But wait… The two payments add up to less than the amount spent. 0.5999 + 0.8270 = 1.4269 which is less than the 1.427 spent. The 0.0001 Bitcoin difference is the mining fee. The miner can add that 0.0001 to the coinbase transaction in the block and pay it to themselves.

If we look at the block the transaction is included in,103 we can see that the miner paid themselves 12.52723951 bitcoins in the coinbase transaction, which is the 12.5 BTC block reward plus the sum of the transaction fees from the transactions in the block:

Hence all bitcoins are traceable. You can see the exact composition of every lump of Bitcoin that comes into your account—what it is composed of and where it came from—and you can trace every part of that money via the previous accounts, all the way back to when it was first created in a coinbase transaction.

I say each ‘lump of money’ specifically, rather than ‘each Bitcoin,’ because you don’t send bitcoins coin by coin, you just send a total amount. Let’s see how this works with an example.

Let’s start with an empty address and assume that you are friends with a Bitcoin miner who has just created a ‘lump’ of 12.5 BTC in a coinbase transaction when they successfully mined a block. The 12.5 BTC is like a single banknote in a physical wallet and needs to be spent in its entirety. The miner takes pity on you because you have no bitcoins and wants to give you 1 BTC. So the miner creates a transaction spending those 12.5 BTC to two recipients: 1 BTC to you, and 11.5 BTC back to herself. You now have a 1 BTC ‘lump’ in your account.

Now it is your lucky day and a few other people give you BTC. In further separate transactions, you receive ‘lumps’ of 2 BTC and 3 BTC. So now you have 6 BTC in your wallet, in three lumps: 1 BTC, 2 BTC, and 3 BTC.

If you want to give 1.5 BTC to another friend, how would you do that? You could do it in a few different ways:

Option 1: Spend the 2 BTC lump

You’d create a transaction that looks like this:

Spend: 2 BTC lump

Pay: 1.5 BTC to your friend, 0.5 BTC lump as change back to yourself

Option 2: Spend the 3 BTC lump

You’d create a transaction that looks like this:

Spend: 3 BTC lump

Pay: 1.5 BTC to your friend, 1.5 BTC lump as change back to yourself

Option 3: Spend the 1 BTC and 2 BTC lumps

You’d create a transaction that looks like this:

Spend: 1 BTC and 2 BTC lumps

Pay: 1.5 BTC to your friend, 1.5 BTC lump as change back to yourself

Option 4: Spend the 1 BTC and 3 BTC lumps

You’d create a transaction that looks like this:

Spend: 1 BTC and 3 BTC lumps

Pay: 1.5 BTC to your friend, 2.5 BTC lump as change back to yourself

Option 5: Spend the 1 BTC and 2 BTC and 3 BTC lumps

You’d create a transaction that looks like this:

Spend: 1 BTC and 2 BTC and 3 BTC lumps

Pay: 1.5 BTC to your friend, 4.5 BTC lump as change back to yourself

Although Option 1 feels like the most obvious and is probably what you would do if you were spending banknotes in a physical wallet, you could in theory choose any of those options. These are all different transactions but all achieve the same thing. The lumps of money that sit in your account are called ‘UTXO’s which stands for Unspent Transaction Outputs. Most people think in terms of ‘account balances’ (i.e., my account goes up and down) whereas Bitcoin ‘thinks’ in transactions (the transaction spends this money and puts it there). The lumps are the result or output of a transaction, and they are unspent because you haven’t spent them yet. Bitcoin would describe Option 1 as follows:

Option 1: Spend the 2 BTC lump

Transaction inputs: (this is money that is being spent)

1.2 BTC lump

Transaction outputs: (this is money that is not yet spent)

1.1.5 BTC to your friend

2.0.5 BTC lump as change back to yourself

This whole transaction is hashed, giving it a Transaction ID which can then be used by future transactions. If you later want to spend the 0.5 BTC you returned to yourself, you would say ‘take output (2) from this transaction, and spend it like this…’

Now, assuming you did Option 1 described above, what is left in your account? You started with lumps of 1, 2, and 3 BTC. You spent the 2 BTC lump and got 0.5 BTC back. So you’re left with three lumps: 1 BTC, 3 BTC, and the new 0.5 BTC lump. The blockchain records that the 0.5 BTC lump came from yourself, so anyone can trace the 0.5 BTC lump back to its original 2 BTC lump, and then further trace it to the account which it came from originally.

What next?

The transaction is created and signed by the sender using their private keys. This signed transaction is then sent to a node (bookkeeper) who validates it according to business rules (e.g., Does this UTXO exist? Has it been spent before?) and technical rules (e.g., How much data does the transaction contain? Is the digital signature valid?), and if found to be valid, the bookkeeper keeps this transaction in a pool of ‘unconfirmed transactions’ that they have heard about, called a mempool or memory pool. They then propagate this transaction to their neighbours in the network. Each neighbour follows the same process. Eventually a miner or block-creator picks up this transaction and decides whether they want to pack it into a block, and if so, they start mining the block. If the miner is successful in mining the block, they propagate the block to other miners and bookkeepers and each node records this transaction as confirmed in a block.

Peer-to-Peer

When people say Bitcoin is ‘peer-to-peer’ what do they mean?

Firstly, data is sent between bookkeepers in a peer-to-peer way, i.e., directly and not via a central server. Transactions and blocks are sent between bookkeepers who are each as important in status as each other—that is, they are peers. They use the internet to send data between themselves, instead of a 3rd party infrastructure like the SWIFT network used by major banks.

Second, Bitcoin payments are often described as peer-to-peer (i.e., with no middle man). But is this really true? Up to a point. A physical cash transaction is definitely peer-to-peer as there are no other actors other than the payer and the recipient. But Bitcoin also has intermediaries such as miners and bookkeepers. The difference between Bitcoin payments and bank payments is that, with Bitcoin payments, the intermediaries are non-specific and can act in lieu of each other, whereas traditional banks and centralised payment services are specific intermediaries. For example, if you have an account with HSBC you can’t instruct another bank such as Citibank to move your money, but in Bitcoin any miner can add your transaction to a block they are mining.

Peer-to-peer models of data distribution are like a gossip network where each peer shares updates. Peer-to-peer is in many ways less efficient than client-server, as data is replicated and validated many times, once per machine, and each change to the data creates a lot of noisy gossip. However, each peer is independent and the network can continue operating if some nodes temporarily lose connectivity. And because there is no central server that can be controlled, peer-to-peer networks are more robust and resistant to shutdown, whether accidental or deliberate.

In anonymous, and therefore untrusted, peer-to-peer networks, each peer needs to operate on the basis that any other peer could be a bad actor. So every peer needs to do their own homework and validate transactions and blocks, rather than trusting other peers. The network as a whole acts honestly, if populated by a majority of honest nodes. Next, we examine the limits of bad behaviour and the related costs and incentives.

Miscreants

What can and can’t miscreants do?

The impact of a malicious bookkeeper is very limited. They can withhold transactions and refuse to pass them to other bookkeepers, or they can present a false view of the state of the blockchain to anyone asking them. A quick check with other bookkeepers will reveal any discrepancies.

Malicious miners can cause a little more impact. They can:

•Attempt to create blocks that include or exclude specific transactions of their choosing.

•Create a double spend by attempting to create a ‘longer chain’ of blocks that make previously accepted blocks become ‘orphans’ and not part of the main chain. They can realistically only do this if they command a significant proportion of the entire network’s hashing power.

But they can’t:

•Steal bitcoins from your account, because they can’t fake your digital signatures.

•Create bitcoins out of thin air, because no other miners or bookkeepers would accept this transaction.

So the impact of a malicious miner is also actually quite limited. Furthermore, a miner discovered to be enabling double spends could quickly find themselves cut off from the rest of the network if the rest of the network informally agrees to take action. Honest miners might agree not to build on blocks generated by a malicious miner.

Summary

Transactions are payment instructions of specific amounts of Bitcoin (UTXOs) from one user-generated account (address) to another. The transactions are created using wallet software, authenticated with unique digital signatures, then sent to bookkeepers (nodes) who individually validate them according to some well-known business and technical rules. The bookkeepers then add valid transactions to their mempool and distribute them to other bookkeepers that they are connected to.

Miners gather these individual transactions into blocks and compete with each other to mine their blocks by tweaking the block contents, specifically the nonce field, until the hash of the block is smaller than some target number. The target number is based on the difficulty setting at the time, which is derived from the time taken to mine the previous set of blocks to achieve a network-wide target frequency of one new mined block every 10 minutes. Miners receive a financial incentive in the form of new BTC and transaction fees which they may credit themselves, to compensate for spending resources to perform the competitive, repetitive hashing needed to create valid blocks.

The blocks link to each other in a unique sequence to form a ledger, the Bitcoin blockchain, that is recorded identically almost simultaneously on thousands of computers around the world that run Bitcoin software. If a Bitcoin transaction is not recorded on this blockchain, it is not a Bitcoin transaction. It doesn’t exist. A Bitcoin transaction recorded outside this file does not form part of the ledger.

There is no central authority who controls the ledger or who can censor specific transactions.

Different blockchain platforms or systems work differently. If you relax or change the aims or constraints, the design of the solution can also change. The solution may be simpler, as we will see later with private blockchains where censorship resistance is not a critical factor.

Putting this all together, we can see that the Bitcoin ecosystem consists of parties who perform different roles. Miners and bookkeepers focus on building and maintaining the blockchain itself. Wallets make it easy for people to use cryptocurrencies. Exchanges and cryptocurrency payment processors bridge between the fiat and crypto worlds.

While the theory sounds good, Bitcoin in practice is not as decentralised as people might have you believe. By some metrics it is not performing as well as some proponents might lead you to believe.

Bookkeeping Nodes

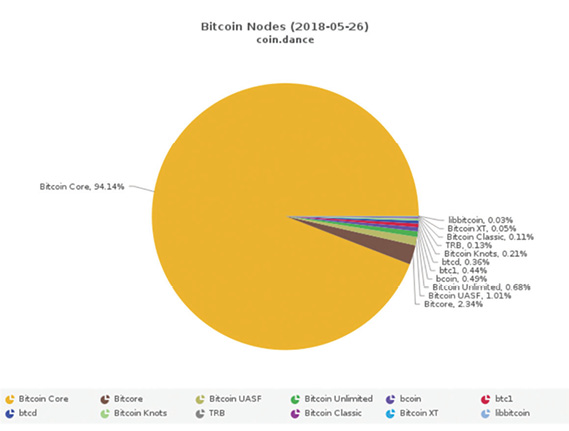

While there are around 10,000 nodes who perform bookkeeping tasks and who relay transactions and blocks, they are mostly running the same software written, and therefore controlled, by a very small number of people. They are known as the ‘Bitcoin Core’ developers and the software is known as ‘Bitcoin Core’.

Source: coin.dance104

The various versions, or implementations, that are not Bitcoin Core all have slightly different rules but are not different enough to create incompatibilities. Some, for example, may have additional flags to signal that the bookkeepers would be prepared to adopt a rule change if enough participants also signal the same intention.

Mining

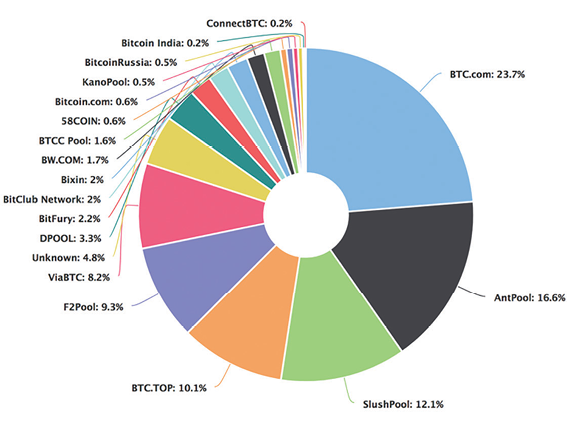

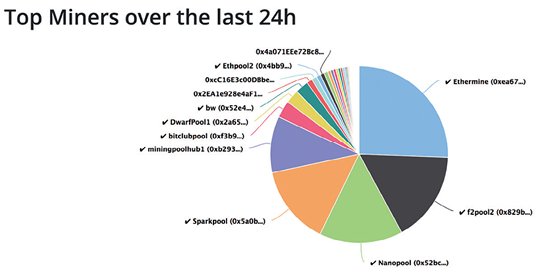

Although anyone can mine, the process has become so intensive that new hardware and chips are created which are designed to be exceedingly efficient at performing the SHA-256 hashing. ASICs (Application Specific Integrated Chips) became the norm for mining in 2014 and outcompete all other forms of hardware in terms of energy efficiency for Bitcoin mining. Dave Hudson explores the effects of ASICs in his excellent blog Hashing It105. In the popular media, the computational power of these specially designed chips is often compared to the computational power of supercomputers, but ASICs cannot operate as general-purpose computers, so comparisons with supercomputers are meaningless. Only a few entities can mine profitably, usually using special purpose ‘mining farms’ clustered in areas of cheap electricity. The chart below shows miners and what proportion of blocks they have recently mined. The proportion of blocks they have mined is roughly equivalent to their hashing power as a proportion of the total hashing power of the network.

Bitcoin mining is not that decentralised! Source: blockchain.info106

Some of these are single mining entities. Others are syndicates that anyone can join, contribute hash power, and receive rewards in proportion to their contributions. At an estimate, around 80% of the hash power is controlled by Chinese entities. BTC.com, Antpool, BTC.TOP, F2Pool, viaBTC are all Chinese groups107, and a company called Bitmain owns both BTC.com and Antpool. Hence, if only the top three mining pools collaborate, they can reorganise blocks and arrange double spends, and no one would be able to stop them as they represent more than 50% of the total hashing power. So this is not a well-decentralised system.

It is often argued that miners wouldn’t do this because it would cause a loss of confidence in Bitcoin and thus cause the price to fall, and their stock of bitcoins would be worth less. However, an enterprising group of miners who carried this out could build a temporary large short trading position just before executing a double spend and profit on the fall in price of BTC.

Mining Hardware

As discussed, miners use special purpose chips called ASICs that are specifically designed and built to be efficient at SHA256 hashing. Commercial chip manufacturers have been slow to design chips that are specifically built to be efficient at SHA256 hashing, so demand has created an alternative specialised industry for supplying Bitcoin ASICs. The main provider of this is Bitmain, the same Chinese company who controls the top two mining pools. It has been estimated that Bitmain produces hardware that mines 70-80% of the total blocks in Bitcoin108. Bitcoin hardware manufacturing is not well decentralised.

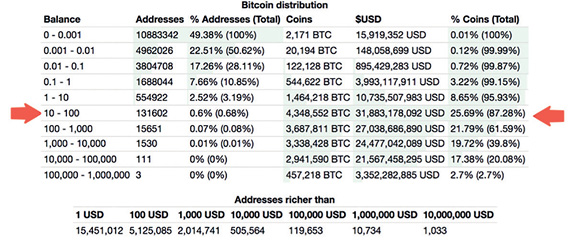

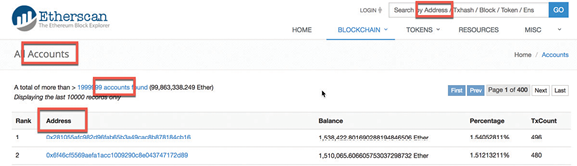

BTC ownership

The ownership of BTC too shows a concentration in a small number of hands:

Source: bitinfocharts.com109

According to this analysis, almost 90% of value is owned by fewer than 0.7% of the addresses. Of course, we have to treat this kind of analysis with some caution. Some large wallets are controlled by exchanges who take custody of coins on behalf of a large number of users. So the table might be overstating the centralisation of Bitcoin ownership. Against that, some people might spread out their bitcoins across a large number of wallets in order to not attract attention. This is very easy to do. So the table might be understating the centralisation of Bitcoin ownership. However, it remains highly likely that, just as in the non-crypto world, very few people probably own the vast proportion of the value. Now, there’s a surprise.

Upgrades to the Bitcoin Protocol

Upgrades to the Bitcoin network and protocols are also fairly centralised. Changes are suggested in ‘Bitcoin Improvement Proposals’ (BIPs). These are documents that anyone may write but, but they all end up on a single website: https://github.com/bitcoin/bips. If it gets written into the Bitcoin Core software on Github, https://github.com/bitcoin/Bitcoin, it forms part of an upgrade, the next version of ‘Bitcoin Core’ which is the most commonly used software, or ‘reference implementation,’ of the protocol. As we have seen, this is run by the vast majority of participants.

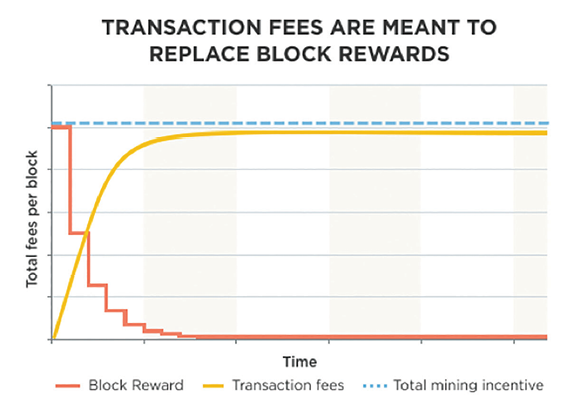

Transaction Fees

In theory, the transaction fees collected per block is meant to compensate for the decrease in block reward as the network gets more popular over time. The reality is that this doesn’t seem to be working out.

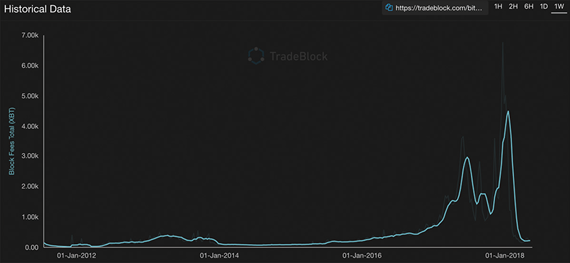

Source: tradeblock.com110

The chart shows that except for a brief spike at the end of 2017, the total transaction fees have stayed stubbornly low at approximately 200 BTC per week. Compare this with the new 12,600 BTC generated from coinbase rewards per week (12.5 BTC per block x 6 blocks/hour x 24 hours/day x 7 days/week = 12,600 BTC, a figure which reduced by half in 2016, and is estimated to half again in 2020). Without significant increase in transaction fees to compensate, clearly the economics of Bitcoin mining will change.

Bitcoin, like most innovative innovations, was not created in a vacuum. Bitcoin was built by drawing from previous experiences and piecing together various tried-and-tested concepts in an innovative way to come up with new characteristics for decentralised digital cash.

Below are some technologies and ideas that may have directly or indirectly inspired Bitcoin:

Digicash

It is hard to overstate the impact that David Chaum had on the movement towards electronic cash, by which he meant a privacy preserving digital asset that could settle financial obligations. Chaum, an early cypherpunk, described this concept in 1983 in a paper entitled ‘Blind signatures for untraceable payments’ in the journal Advances in Cryptology Proceedings. He wanted a bank to be able to create digitally signed digital lumps of cash for their customers. The customers could spend the digital cash at shops, who would then redeem the digital cash with the bank. When the merchant redeemed the digital cash, the bank would see that the digital cash was good, but it did not know which of its customers the digital cash had originally been assigned to. The individual transactions were therefore anonymous as far as the bank was concerned. Digicash was the Amsterdam based company incorporated to commercialise this technology. The system was called eCash, sometimes Chaumian eCash, with the tokens themselves called CyberBucks. Although a few banks did some trials with CyberBucks, Digitcash filed for bankruptcy in 1998, unable to secure a deal to keep it afloat.

b-money

In November 1998, Wei Dai, an American-educated cryptography researcher and cypherpunk, published a short paper111 describing b-money under two protocols. b-money would operate on an untraceable network where senders and receivers would be identified only by digital pseudonyms (i.e., public keys). Every message would be signed by its sender and encrypted to its receiver. Transactions would be broadcast to a network of servers who would keep track of account balances and update them when they received signed transaction messages. Money creation would be agreed by the participants in a periodic auction.

Hashcash

In 1992, Cynthia Dwork and Moni Naor described a technique for reducing spam (junk email) in their paper,112 ‘Pricing via Processing or Combatting Junk Mail,’ by creating a hoop that email senders would have to jump through before sending emails. Email senders would have to attach a kind of proof or receipt to their outbound emails demonstrating that they had incurred a very small ‘cost’. Recipients would reject inbound emails without these receipts. The ‘costs’ incurred by the senders would be tiny at normal email volumes, but add up and discourage spammers who send out millions of emails. The ‘cost’ wasn’t a payment to a third party, but it would be incurred as ‘work’ in the form of repeated calculations that had to be made, to ensure an email would be accepted. So the receipt would be a ‘proof’ that repeated calculations, or ‘work’ had been done, leading to the phrase ‘proof-of-work’.

In 1997, Adam Back proposed a similar idea113 and described a ‘partial hash collision-based postage scheme’ which he named ‘Hashcash’. Bitcoin mining uses this concept of forcing someone to do some work, and proving they have done it, before allowing them access to a resource. He followed up in 2002 with a paper,114 ‘Hashcash—A Denial of Service Counter-Measure,’ describing improvements and applications of proof-of-work, including hashcash as a minting mechanism for Wei Dai’s b-money electronic cash proposal.

e-gold

E-gold was a website opened in 1996 and operated by Gold & Silver Reserve Inc. (G&SR) under the name ‘e-gold Ltd’ that allowed customers to open accounts and trade units of gold between each other. The digital units were backed by gold stored in a bank safe deposit box in Florida, USA. E-gold didn’t ask users to prove their identity, and this made it attractive for the underworld. It became very successful. It was reported to have up to 3.5 million accounts in 165 countries in 2005 with 1,000 new accounts opening every day115, but the website was eventually shut down due to fraud and allegations of facilitation of crime116. Unlike Bitcoin, it had a centralised ledger.

Liberty Reserve

Like e-gold, Liberty Reserve, based in Costa Rica, allowed customers to open accounts with few personal details, nothing more than a name, email address, and birth date. Liberty Reserve made no attempts to verify these, even for obviously false accounts named ‘Mickey Mouse’ and so on. During an investigation117, a US agent opened a functional account with a username ‘ToStealEverything’ in the name of ‘Joe Bogus’ who lived at ‘123 Fake Main Street’ in ‘Completely Made Up City, New York’ and wrote that it would be used for ‘shady things’. As a result of its relaxed controls, Liberty Reserve was used extensively for money laundering and other criminal proceeds, more than $6 billion according to ABC News118. It served over 1 million customers before it was shut down in 2013 by the US Government under the Patriot Act.

Napster

Napster was a peer-to-peer filesharing system that was live between 1999 and 2001. It was created by Shawn Fanning and Sean Parker, and was popular with people who liked to share music, particularly in mp3 format, and who didn’t like to pay for it. The idea was to allow anyone to copy and share content saved on users’ hard drives. At its peak the service had about 80 million registered users. It was eventually shut down because its relaxed approach to the sharing of copyright material wasn’t appreciated by those with interests vested in that material.

Napster’s technical weakness was that it had central servers. When a user searched for a song, their machine would send the search request to Napster’s central servers, which would return a list of computers storing that song and would allow the user to connect to one of them (this is the peer-to-peer bit) to download the song. Although Napster itself didn’t host the material, it made it easy for users to discover others who did. Centralised services and entities running those services are easy to shut down, and so it was, to have its role replaced by BitTorrent, a decentralised peer-to-peer file sharing system.

Mojo Nation

According to CEO Jim McCoy, Mojo Nation was an open source project that was a cross between Napster and eBay. Launched in or around 2000119, it combined filesharing with microtransactions of a token called Mojo, so that file sharers could be compensated for sharing content. It split files into encrypted chunks and distributed them such that no single computer would host an entire file. Mojo Nation failed to gain traction, but Zooko Wilcox-O’Hearn, who worked on Mojo Nation later founded Zcash, a cryptocurrency focused on transaction privacy.

BitTorrent

BitTorrent is a successful peer-to-peer filesharing protocol that is still in wide use today. It was developed by BitTorrent Inc, a company cofounded by Bram Cohen who worked on Mojo Nation. BitTorrent is popular with those sharing music and movies, users who may once have used Napster. It is decentralised: each search request is made from user to user rather than via a central search server. As there is no central point of administration, it is hard to censor and shut down.

As a theme, whether we consider money (e-Gold, Liberty Reserve, Bitcoin etc), or data (Napster, BitTorrent, etc), the evidence shows that decentralised protocols are more resilient to being shut down than services with a central point of control or failure. I expect the trend of decentralisation to continue in the future, driven in part by concerns that authorities are overextending their reach into private social matters.

Bitcoin’s history is colourful, more colourful than some received wisdom might have it. Some Bitcoin proponents say ‘Bitcoin (the protocol) has never been hacked,’ but they are wrong. Bitcoin has been hacked. Here is a selection of events from historyofBitcoin.org120 and the Bitcoin Wiki121 with my personal comments about these events.

2007

A pseudonymous Satoshi Nakamoto began working on Bitcoin.

18 Aug 2008

The website bitcoin.org was registered using anonymousspeech.com, a broker that registers domains on behalf of customers who can choose to remain anonymous. This shows how important privacy was to the person or group involved in Bitcoin.

31 Oct 2008

The Bitcoin whitepaper, written under the pseudonym Satoshi Nakamoto, was released on an obscure but fascinating mailing list metzdowd.com that is much loved by cypherpunks. Wikipedia has this to say about cypherpunks:

A cypherpunk is any activist advocating widespread use of strong cryptography and privacy-enhancing technologies as a route to social and political change. Originally communicating through the cypherpunks electronic mailing list, informal groups aimed to achieve privacy and security through proactive use of cryptography. Cypherpunks have been engaged in an active movement since the late 1980s.

This short whitepaper is regarded by Bitcoin believers as sort of bible.

3 Jan 2009

The genesis (first) block was mined. At that moment, the first bitcoins, fifty of them, were created out of thin air and recorded on Bitcoin’s blockchain in the first block—block zero. The transaction that contains the mining reward, the so called ‘coinbase’ transaction, contains the text:

‘The Times 03/Jan/2009 Chancellor on brink of second bailout for banks’

The text refers to a headline of the UK newspaper The Times. This is regarded as proof that the block cannot have been mined significantly earlier than that date, and the headline was presumably chosen deliberately for its implication: When banks fail, their losses are socialized; here is Bitcoin—it doesn’t need banks.

Source: thrivemovement.com122

So beware of people who say they were ‘in Bitcoin’ before 2009! I have been on a number of panels where other panellists try to establish credibility by saying just how early they were involved in Bitcoin. Sometimes, in their enthusiasm, they try to convince eager listeners that they were there before 2009…

An interesting aside: The 50 BTC mined in the first block are unspendable. They sit in address 1A1zP1eP5QGefi2DMPTfTL5SLmv7DivfNa, but the account holder, presumably Satoshi, whoever he, she, or they may be, is unable to transfer them to anyone else due to some quirk in the code.

9 Jan 2009

Version 0.1 of the Bitcoin software was released by Satoshi Nakamoto, along with its source code. This allowed people to review the code, and download and run the software, becoming both bookkeepers and miners. Bitcoin was thus accessible to anyone who wanted to download and use it. Developers were able to scrutinise the code and build on it if they wanted to contribute.

12 Jan 2009

The first Bitcoin payment was made from Satoshi’s address to Hal Finney’s address in block 170123, the first recorded movement of bitcoins. Hal Finney was a cryptographer, cypherpunk, and coder, and some people believe he was partly behind the Satoshi pseudonym.

6 Feb 2010

The first Bitcoin exchange, ‘The Bitcoin Market,’ was created by bitcointalk.org forum user ‘dwdollar’124.

Previously, people traded bitcoins, but in a relatively unstructured way in chat rooms and message boards. An exchange is the first step towards making it easier for people to buy or sell bitcoins and increasing price transparency.

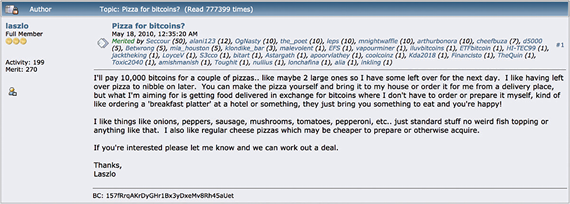

22 May 2010

Pizza day! This was the first documented time bitcoins were used to pay for something in the real world. Laszlo Hanyecz, a programmer in Florida, USA, offered to pay 10,000 BTC for a pizza on the bitcointalk forum125.

Another developer Jeremy Sturdivant (‘jercos’) took up the offer and called Domino’s Pizza (not Papa Johns as frequently reported) and had two pizzas delivered to Laszlo. He received 10,000 BTC126 from Laszlo.

Here is the transaction127:

Laszlo kept the offer open and, over the next month, received a number of pizzas for 10,000 BTC each time, before cancelling the offer:

This is the first transaction where bitcoins were used for economic activity other than a straight buy or sell.

17 Jul 2010

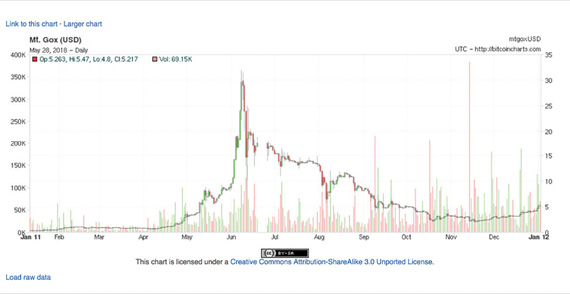

Jed McCaleb (who has more recently founded Stellar, a cryptocurrency platform based on Ripple), converted his card trading exchange into a Bitcoin trading exchange. ‘Mt Gox,’ usually pronounced ‘mount gox,’ stands for ‘Magic: The Gathering Online eXchange’. Magic: The Gathering is a collectable card game, and the website was used initially to trade cards before it was converted to a Bitcoin exchange. Initially, you could fund your Mt Gox account using PayPal, but in October, they switched to Liberty Reserve. Mt Gox would eventually collapse in Nov 2013–Feb 2014, but in its heyday, it was the largest and most well-known and well-used exchange.

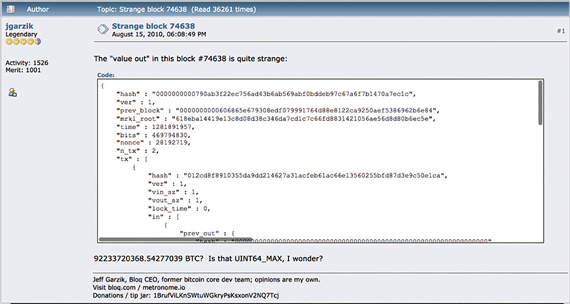

15 Aug 2010

Bitcoin’s protocol got hacked. Beware the popular narrative that says, ‘Bitcoin itself has never been hacked’. A potential vulnerability was discovered, and someone exploited this vulnerability in block 74,638 to create 184 billion bitcoins for themselves. This strange transaction was quickly discovered and, with the consent of the majority of the community, the whole blockchain was ‘forked,’ reverting it to a previous state (we will discuss forks later).

So much for the immutability of Bitcoin’s blockchain: there are always exceptions.

The bug was fixed. Bruno Skvorc has written a good explanation of how it happened on his blog bitfalls.com128, and the bitcointalk forum has a thread129 where key developers discussed the bug.

If anyone says Bitcoin hasn’t been hacked, ask them ‘What about the integer overflow bug in August 2010 where someone sent themselves 184 billion bitcoins?’

18 Sep 2010

The first mining pool, Slush’s pool, mined its first block. A mining pool is an organisation where multiple participants combine their hash power to give themselves a better chance of winning a block. The participants split the rewards between them in proportion to their hash power contributions, a bit like a lottery syndicate. Mining pools have grown in significance over time.

7 Jan 2011

12 BTC were exchanged for $300,000,000,000,000. This is probably the highest exchange rate Bitcoin has ever achieved. The dollars in question, however, were Zimbabwean dollars. The Zimbabwean dollar is a good example of what can go wrong in a failing economy, and a reminder that fiat currencies need to be well managed.

9 Feb 2011

On the Mt Gox Bitcoin exchange, Bitcoin reached parity with the US dollar (1 BTC = 1 USD).

6 Mar 2011

Jed McCaleb sold the Mt Gox website and exchange to a French entrepreneur Mark Karpeles who was living in Tokyo. Jed sold it on the premise that Mark would do a better job expanding it. Alas Mark did not live up to these hopes. Mt Gox filed for bankruptcy in 2014 and Mark eventually landed up in jail.

27 Apr 2011

VirWoX, a website that allowed customers to convert between fiat currencies and Linden Dollars (the virtual currency for use within the computer game Second Life), integrated Bitcoin. People could now exchange directly between bitcoins and Linden Dollars. This was possibly the first virtual currency to virtual currency exchange.

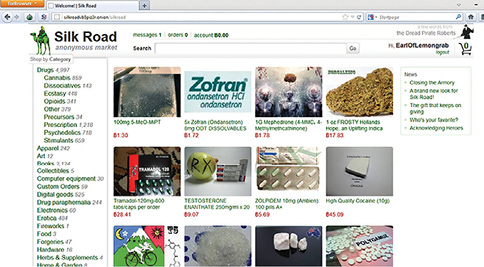

1 Jun 2011

WIRED magazine published a famous article, ‘Underground website lets you buy any drug imaginable,’130 written by Adrian Chen. It described a website called The Silk Road, launched in Feb 2011 and run by twenty-seven-year old Ross William Ulbricht under the nickname ‘Dread Pirate Roberts,’131. The Silk Road was described as a kind of ‘eBay for drugs’—a darknet market, only accessible through the special browser Tor132, which matched buyers and sellers of drugs and other illegal or questionable paraphernalia. Bitcoins were used as the payment mechanism.

Source: stopad.io133.

Here is how the article describes Bitcoin:

As for transactions, Silk Road doesn’t accept credit cards, PayPal or any other form of payment that can be traced or blocked. The only money good here is Bitcoins.

Bitcoins have been called a ‘cryptocurrency,’ the online equivalent of a brown paper bag of cash. Bitcoins are a peer-to-peer currency, not issued by banks or governments, but created and regulated by a network of other Bitcoin holders’ computers. (The name ‘Bitcoin’ is derived from the pioneering file sharing technology BitTorrent.) They are purportedly untraceable and have been championed by cyberpunks, libertarians and anarchists who dream of a distributed digital economy outside the law, one where money flows across borders as free as bits.

To purchase something on Silk Road, you need first to buy some bitcoins using a service like Mt. Gox Bitcoin Exchange. Then, create an account on Silk Road, deposit some bitcoins, and start buying drugs. One Bitcoin is worth about $8.67, though the exchange rate fluctuates wildly every day.

This was the first time Bitcoin came to the attention of a wide audience. The Silk Road was eventually taken down by US authorities in October 2013, though many copycats have taken its place.

14 Jun 2011

Wikileaks and other organisations began to accept bitcoins for donations. Bitcoin is attractive for these organisations owing to its censorship resistance. While it is relatively easy for a government to lean on traditional payment systems (banks, PayPal, etc) to monitor transactions, block assets and freeze accounts, cryptocurrencies provide an alternative funding mechanism. Whether this is good or bad, of course, is a matter of opinion…

20 Jun 2011

Possibly the first documented evidence134 of a physical brick-and-mortar merchant accepting Bitcoin as a means of payment. Room 77, a restaurant based in Berlin, Germany sold fast food for bitcoins.

2 Sep 2011

Mike Caldwell started creating physical bitcoins which he called Casacius coins. They are physical discs of metal, each with a unique private key embedded behind a hologram sticker. Each coin’s private key is linked to an address that is funded with a specified amount of bitcoins, as depicted on the coin.

Source: Bitcoin wiki135.

These Casascius coins are the physical representations used in many stock photos used for media articles about bitcoins. They are also prized as collector’s items and cost much more than the value of the bitcoins contained in them, especially the first edition, which had a spelling mistake.

8 May 2012

Satoshi Dice was a gambling website launched on 24 April 2012. Users could send bitcoins to specific addresses with a chance of winning up to 64,000 times their original stake. Each address had a different payout and a different chance of winning. On 8 May, it became responsible for over half the transaction volume on the Bitcoin blockchain. Satoshi Dice was created by libertarian Eric Voorhees and was extremely popular. Early adopters seemed to have a penchant for gambling, and there wasn’t much else they could do with their bitcoins.

It was an interesting gambling system. Unlike other online casinos where users have to trust that the house is not cheating, Satoshi Dice was provably fair, using deterministic cryptographic hashes as the random number generators. Of course, the house had an edge, but the edge was small, known (1.9%), and was demonstrably adhered to.