Before

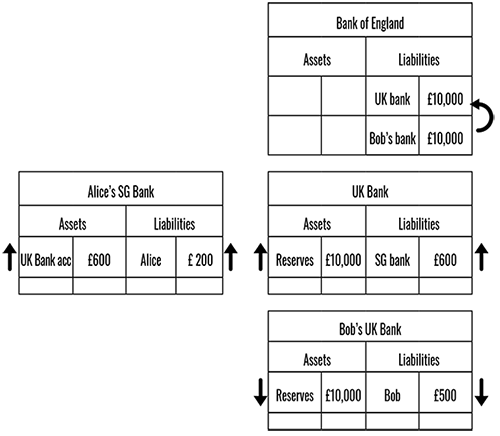

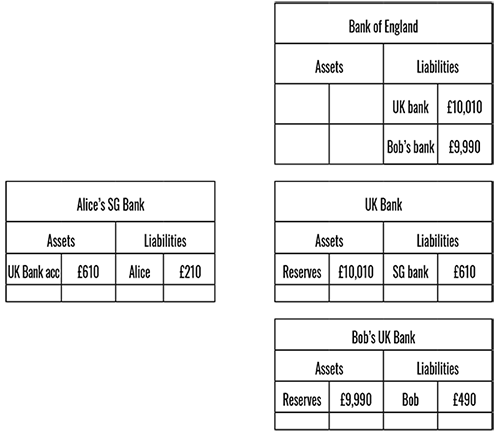

After

Bob sends £10 from his GBP account at his UK bank to Alice’s GBP account at her SG bank.

When Alice in Singapore receives GBP from Bob, the money is actually moving across the Bank of England’s RTGS system and arriving in the Singapore bank’s nostro at its correspondent bank in the UK. The GBP is not moving in or out of the country… it is simply changing ownership within the UK.

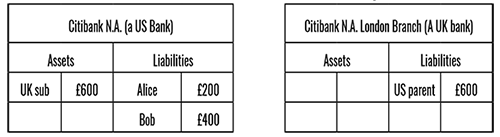

Where banks (often larger ones) have subsidiaries with banking licences in other jurisdictions, they will preferentially use their subsidiaries for their nostros. For example, a US bank, Citibank N.A., has a subsidiary bank in the UK called ‘Citibank N.A. London Branch’61 which is a clearing bank in the UK. So Citibank N.A. would use Citibank N.A. London Branch as its GBP nostro. So if Alice and Bob opened GBP accounts with Citibank N.A., the funds would really be held by Citibank N.A. London Branch:

Global banks often use their subsidaries as correspondents

That is what happens if one of the banks is in the country of the currency being moved.

Sending USD from UK to Singapore

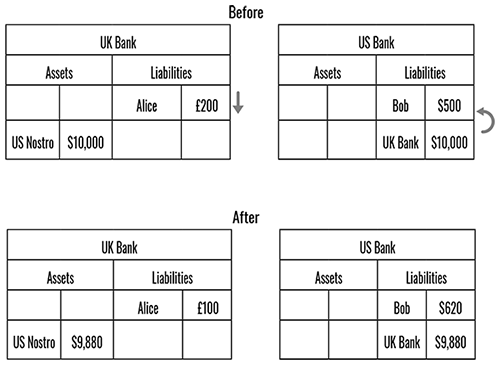

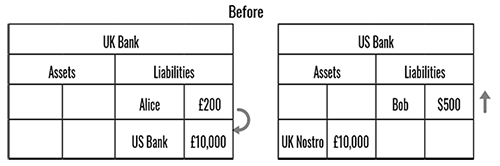

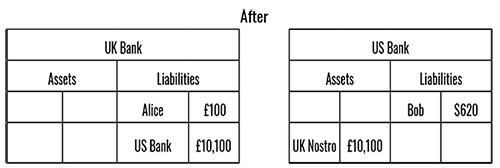

We have seen what happens if one of the banks is operating in the domestic zone of the currency being moved. But what if both banks are outside that zone? For example, what if Bob, in the UK, wants to pay Alice, in Singapore, USD $10?

Bob and Alice both have USD ‘foreign currency’ accounts at their respective banks in their respective countries. Neither bank may have banking licences in the USA, so they must have correspondent bank accounts—their respective nostros—with a US correspondent bank. In the simplest case, if they both use the same correspondent, then the USD is cleared by that correspondent, who does a -$10/+$10 book entry between the banks’ nostros.

If the banks have USD nostros at different correspondent banks, then the USD is cleared by the central bank, the Federal Reserve, who, as we have seen above, records the -$10/+$10 movement between the accounts of the correspondent banks.

Note that the USD moves in the USA, not in the UK or in Singapore. Currencies (in electronic form) stay inside their domestic zone62!

And that is the happy scenario where Alice’s and Bob’s banks are lucky enough to have nostros at USD clearing banks (who in turn have accounts with the central bank). Sometimes smaller banks or banks licensed in less well-regulated environments might not be able to establish banking relationships in major banking jurisdictions abroad: the big clearing banks see the small banks as not worth the effort, risk, and paperwork required to establish and maintain a high-confidence working relationship. The banks perceived as more risky need to open accounts with local banks perceived as less risky, who could have correspondent accounts at small US banks who might in turn have correspondent accounts at major US clearing banks…

So payments take longer, there is more operational risk, there is less transparency, and fees accumulate. The effect of this, in practice, is a form of financial exclusion. Some small banks and financial institutions in less stable regions are practically excluded from the major financial system, and this is detrimental to their growth and the growth of their customers’ businesses and other economic activity within their local economies.

This form of financial exclusion is increasing. For example, the World Bank conducted a survey in 201563 of 110 banking authorities, 20 large banks and 170 smaller local and regional banks. It found that roughly half of those surveyed experienced a decline in correspondent banking relationships, directly reducing their ability to conduct foreign currency transactions. Money Transfer Operators (MTOs, non-banks) were also surveyed and it was found that of the MTOs surveyed, 28% of MTO principals and 45% of their agents could no longer access banking services. Of those, 25% were no longer able to operate and 75% had to find alternative channels for foreign currency transactions.

Large banks have been actively closing down the nostros of foreign banks, especially banks from those jurisdictions which are deemed higher risk. The large banks cite the risk of being fined or suffering reputational risk if the banks for whom they open nostros are found to be using those nostros for, or are otherwise associated with, illegal or unethical activities.

This has affected the cryptocurrency industry too. In 2015, there were rumours that the big US banks would threaten to cut off smaller banks if the smaller banks continued to bank Bitcoin exchanges. This ‘de-risking,’ as it is euphemistically known, is serving to cut off the parties who need their services the most, and is creating a moat around the larger economies, disabling smaller economies from flourishing. My favourite financial columnist, Matt Levine, made some comments about big banks threatening to cut off smaller banks who bank cryptocurrency exchanges in his Bloomberg column “Money Stuff”64:

The concern here is that JPMorgan might transfer money for another bank, and that other bank might transfer money for a Bitcoin exchange, and that Bitcoin exchange might transfer money for a drug dealer. Which, in the eyes of the law, means that JPMorgan might as well be dealing drugs itself.

I sometimes think about the analogy between banks and airlines: If a drug dealer uses a bank to move money, that bank is held responsible, but if he just gets on a plane with a bag of money, no one thinks to hold the airline responsible.

But this is much further removed. This is like, a taxi driver flies on United Airlines from New York to Miami, and in Miami he picks up a guy who owns a boat and drives him to the marina, and then the guy with boat transports bags of cash for a drug dealer, and you hold United responsible.

Vast swathes of legitimate financial transactions will be cut off if you punish banks for dealing with people who deal with people who deal with people who commit crimes.

Euro-currencies

Reality is always more complicated than theory, especially in banking. Currencies can actually be created and exist outside of their domestic zones or home jurisdictions. Examples are ‘Euro-currencies,’ e.g., Euro-dollar, Euro-euro, Euro-sterling. The Euro- prefix originated from Europe the region, and should not be confused with:

•the Euro currency (€) itself, or

•the terminology used in the foreign exchange (FX) trading, e.g., ‘Euro/dollar’ which refers to the exchange rate between euros and dollars.

In this context, the prefix ‘Euro’ indicates that the currency exists outside of its home zone. It was first used when the first USD loan was created outside of the USA, in Europe. So, Euro-dollar, Euro-sterling, and Euro-euro mean, respectively, a US dollar that exists outside the USA, a British pound that exists outside the UK, and a Euro that exists outside the Eurozone.

How are Euro-currencies created? When a bank writes a loan in the currency outside its domestic currency zone (e.g., a British bank issuing a loan in USD), it creates money that exists outside its currency zone (i.e., USD deposits existing outside the USA). This is allowed and is normal business practice, fairly common in fact, but complicates the financial world, especially when countries are trying to count how much of their own currency exists in the world. So it is not the case that all currency is directly controlled by its respective central bank.

At this stage, it is worth busting a common myth. It is commonly believed that banks take money from one customer and lend it to another. This is a sloppy way of thinking about banking and leads to incorrect conclusions. Banks create money, in the form of deposits, when they write loans. These new deposits are new money, sometimes called ‘fountain pen money’ because bankers used to approve loans by signing a document with a fountain pen. If you take out an unsecured loan from a bank, the bank adds deposits to your account (increasing their total liabilities) and adds a loan to their balance sheet (increasing their total assets). New money has been created; it hasn’t been ‘borrowed’ from another depositor. The Bank of England explains this in a research piece entitled ‘Money creation in the modern economy’65.

Foreign Exchange

Now that we’ve dealt with single currency payments (that is, the movement across borders of value denominated in a single currency), what about foreign exchange? What about Alice wanting to send GBP from her sterling account for it to arrive as USD in Bob’s US dollar account?

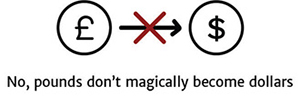

Money doesn’t simply ‘become’ other money, just because of ‘banks’. Pounds sterling cannot become US dollars any more than a pint of milk can become a litre of beer, or a lump of silver can become a lump of gold. 1 pound is not 1.2 dollars. 1 pound is not even ‘the same as’ 1.2 dollars. Sterling is a completely different asset from US dollars, and assets and currencies cannot, and do not, magically morph from one type to another. You always need a third party who is prepared to accept one currency and give you the other.

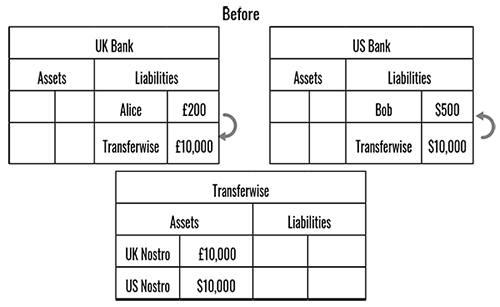

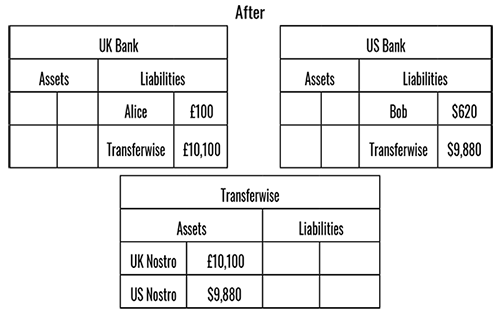

In a payment involving two currencies, someone somewhere is acting as a third party willing to accept some of your currency in return for some of the other currency. When Alice pays GBP to end up as USD in Bob’s account, the role of exchanger may be fulfilled by Alice’s bank, who will deduct GBP from Alice’s account, and credit USD to Bob’s bank, or by Bob’s bank, who will accept GBP from Alice’s bank, and credit USD into Bob’s account. Or Alice could use a specific third party, an MTO such as Transferwise. Transferwise, and other similar MTOs, have local currency accounts in banks in many countries, and they will receive GBP from Alice into their GBP account in London, and they will instruct their USD bank in New York to send some USD from their USD account to Bob’s account. Transferwise has therefore changed the balance of currencies it holds by holding more GBP and less USD. This in turn changes its risk arising from foreign exchange fluctuations—that is, movements in the value of those currencies relative to each other. To maintain its original risk profile, Transferwise will then hope that someone will want to send money the other way, helping to square up its books, or it may try to sell those extra GBP to another agent for USD.

Option 1: Alice’s (sending) bank does the FX by deducting pounds from Alice and crediting Bob with their dollars

Option 2: Bob’s (receiving) bank does the FX by receiving pounds and crediting Bob with dollars

Option 3: 3rd party e.g., Transferwise does the FX by receiving Alice’s pounds and sending their dollars to Bob

Cross border transactions with foreign exchange.

In recent years, digital wallets have become more popular, and the industry landscape continues to evolve quickly. Digital wallets are usually smartphone apps that allow customers to open accounts. Customers fund their wallets using a credit or debit card, a bank payment, or by paying physical cash to an agent, usually in a convenience store. Once money has been transferred from the customer to the wallet operator, the customer sees a balance in their wallet, which can then be used. Depending on the services provided by the wallet, it can be used to temporarily store value or to send money to other customers, pay bills, buy tickets, shop at various merchants, pay for taxis, pay for groceries at the checkout, and even pay speeding tickets. Many providers offer a ‘virtual’ credit or debit card number that is connected to the customer’s digital wallet. This allows customers who may not have otherwise be able to get a credit or debit card to make payments anywhere that those cards are accepted, and sometimes even make ATM cash withdrawals.

PayPal, Venmo (owned by PayPal), and Starbucks are popular digital wallets in the USA. In India, Paytm and Oxigen are the leading providers. GoPay, owned by Indonesian ride-sharing app GoJek, is popular in Indonesia and is gaining traction in the rest of Southeast Asia, where the dominant ride-sharing app Grab also has a wallet. In China, Alipay and WeChat Pay are used extensively to store value and make payments. The rate of customer growth of these wallets is astonishing: Alipay alone has over 500 million registered users and 100 million daily active users.

Early wallets were provided by telecommunications companies (telcos), who were already dealing in pre-paid airtime, a different type of digital currency. It was a small step to allow customers to move money into a wallet denominated in fiat currency rather than in ‘minutes,’ especially as the wallet would exist on a device that the customer had likely bought from the telco (do you remember when handsets were branded with the telco’s logo?). However, telcos were unable to maintain their early lead due to their ‘walled-garden’ approach, so this first wave of digital wallets was not, on the whole, successful.

Today’s wallets have either developed from private companies who could navigate the airtime-to-wallet path well (PayTM), or ridesharing companies who, due to their popularity, have gigantic scale (Grab, GoJek), or companies that started as social messaging apps and added payments (WeChat).

These businesses operate under different licences in different jurisdictions. The names of the regulatory licences used by these wallet businesses differ by jurisdiction. Examples include: e-Money; Money Transmitter; Stored Value Card; Remittance; Wallet; Money Transfer, and so on. These licences tend to be easier to obtain than banking licences, but the permitted activities are more limited. In most jurisdictions, licensees are usually forbidden to write loans or create money, a privilege granted to lenders and banks. Every dollar or unit of currency that a customer sees in their app must be backed by an equivalent dollar in the company’s bank account.

E-Money wallets are easy to understand from a payments perspective. Each operator has a bank account that is ring-fenced to contain only customer money. This account must not be used for company operations such as receiving income or paying salaries. When customers fund their wallets, transfers are made into this bank account. When customers of one operator move money between each other, there is no change to the money in the bank account, but the wallet operator records a debit to one customer and a credit to another—a -$10/+$10 in its books. If a customer withdraws money from their account, then the wallet operator makes a corresponding bank transfer to the customer’s bank account. Customers are not limited to individuals. Merchants, minicab drivers, utilities companies, and public-sector entities are often customers of wallets, and wallets are becoming a convenient and common way to pay bills in some countries.

The rise of wallets, due in part to their focus on delivering a superior user experience, has caused some concern from banks. In some jurisdictions banks are losing relevance with their customers and losing data and revenue from payments. Wallets are increasingly sitting between the customers and their respective banks.

In Europe, one of the most successful ‘challenger banks,’ Revolut, uses an e-money wallet licence, so is not technically a bank. Despite this, it offers a full suite of payments, savings, insurance, pensions, loans and investments. Revolut is the customer-facing front-end through which licensed providers offer their services. This dynamic raises interesting questions as to the future of licensed banks.

Banks need to make a tough decision: They should either try to re-engage with their customers and become more relevant by providing better user experiences, or they should focus on becoming extremely efficient financial pipes in the background. Both models are viable if executed well.