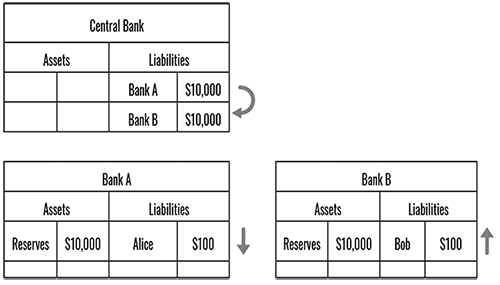

Before

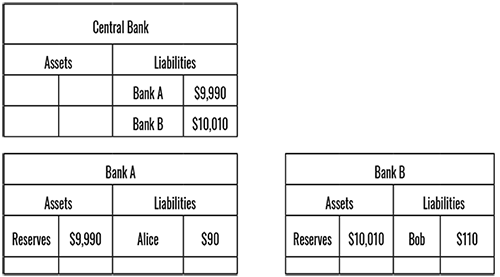

After

Interbank payment via RTGS.

So to recap, and remember, here we are dealing with a single currency only:

•If both customers bank with the same bank, then that bank itself clears the transaction.

•If two banks have a ‘correspondent banking’ relationship, then the receiving bank clears the transaction.

•If there is a central bank system—a RTGS or DNS—then the central bank clears the transaction.

Clearing

Unfortunately, the word clearing is used to mean different things in different contexts. As we have just seen, clearing in payments refers to the final -$10/+$10 transaction. It is not to be confused with clearing in securities trading, which means something else.

In securities trading (for example, shares), two parties strike a deal, say on a stock exchange: one buys from or sells to the other in return for electronic cash. But they do not exchange the cash and shares directly with each other: they settle against a central clearing party instead. So once a trade between parties A and B is agreed, A and B actually both settle up with C, the central clearing party.

C, the central clearing counterparty (CCP), acts as the legal trading counterparty to each side. So where, for example, A buys shares from B, A sends the cash or funds to C56, and B sends the shares to C57. Once C has received the right amount of funds and shares from the respective sides, it then reassigns the funds and the shares respectively, i.e., it gives the shares to A and the funds to B. This setup removes the credit risk between A and B: A and B no longer have credit risk with each other; instead, they both have credit risk with C, whom they both trust for this purpose, at least more than they trust each other.

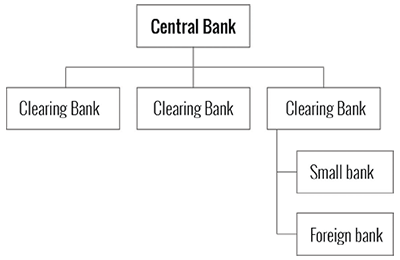

Clearing Banks

Back to payments, in some countries only certain banks get to have accounts with the central bank. These are called ‘clearing banks,’ because they can clear payments, as we have seen above, through the central bank. Smaller banks, or foreign banks with a local presence who are not able to access the central bank, need to open accounts with a clearing bank instead. The clearing banks get to make fees from their privileged position.

Thus, you get a pyramid, a hierarchy of relationships, with the central bank sitting at the top, the clearing banks sitting a layer below, and finally smaller banks, or non-clearers, who don’t have an account at the central bank. They use a clearing bank to make payments in the same way a clearing bank uses a central bank, knowing that the clearing bank can call upon the central bank to clear its own payments when it needs to.

Hierarchy of banks.

Different jurisdictions operate differently. The UK’s RTGS system, for example, known as CHAPS, is highly tiered. Only a small number of banks58 have accounts at the UK’s central bank, the Bank of England; whereas in Hong Kong all licensed banks operating in the jurisdiction are required to have an account at its central bank, the Hong Kong Monetary Authority59.

Although a central set of books run by a central bank is much more efficient than each bank maintaining lots of accounts (or ‘nostros’) with every other bank, the system works only within one jurisdiction and in one currency. So while most economically developed jurisdictions will have a centrally cleared RTGS or DNS system for clearing interbank payments within that country for their respective domestic currency, there is no ‘central bank’ of the world60, not even the World Bank, however grand and ambitious its name.

What do we mean by international payments? Well, there are two main types.

Firstly, there is the payment of a single currency across a border. The receiver receives units of the same currency that the sender sends. For example, someone sends USD across a border and someone else receives USD. This means the USD is either leaving its domestic currency zone (in this case the USA), or it is returning to its domestic currency zone, or it is moving between two countries outside its domestic currency zone (e.g., between the UK and Singapore).

Secondly, there is the transfer of value across borders, with foreign exchange, where the sender and receiver are working in different currencies. For example, the sender has GBP removed from her GBP account in the UK and the receiver has SGD added to her SGD account in Singapore.

By exploring these concepts separately we will see that money, in general, does not leave its domestic currency zone.

As we have seen, there is no central bank of the world to clear international commercial payments, so we have to fall back to the less efficient correspondent banking systems where banks maintain accounts with each other.

Single Currency Transfers Across a Border

Have you ever thought about how your bank can offer you a current account in a currency from a jurisdiction where your bank doesn’t have a banking licence? How does it do that? How does it receive and make payments?

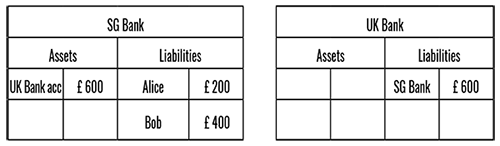

The answer, as you might have guessed by now, is that the bank has an account with a correspondent bank licensed in the country of the currency. For example, a Singapore bank may not have a banking licence in the UK. If it wishes to offer to hold GBP for its customers, it will maintain a GBP denominated account (a nostro) with a major bank in the UK, preferably a clearing bank, and it will then use that as a mega-account (called an ‘omnibus’ account) for all its customers’ GBP currency.

Foreign currency accounts.

So, a Singapore bank customer, Alice (a new Alice), might log in to her Singapore bank website and see that she has £200 in her GBP account, but the £200 is actually sitting in a UK bank under the name of the Singapore bank, alongside any other GBP which the Singapore bank is holding for its other customers. Alice thinks she has £200 in her Singapore bank, but really the money is sitting in a UK bank, and her Singapore bank just shows her her share of a larger account they are holding on behalf of all their GBP customers.

Sending GBP from UK to Singapore

So let’s see what happens when Bob (a new Bob), Alice’s British friend wants to send £10 to Alice’s sterling account in her Singapore bank. Let’s assume Bob banks in the UK with a different bank from the bank that Alice’s Singapore bank uses as its correspondent bank.