Nightmare

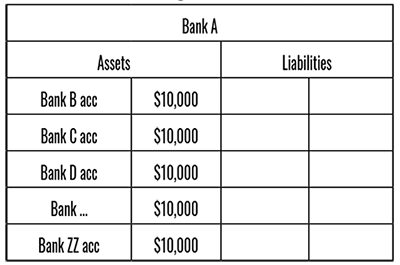

The correspondent banking problem.

And it would be expensive, as you’d need to have a positive balance at each of these banks in anticipation of payment instructions, and as we all know, money sitting in current accounts doesn’t earn much interest. You’d prefer to put that capital to work elsewhere. And it is risky, too! What if any of your correspondent banks went bankrupt? You’d lose your money.

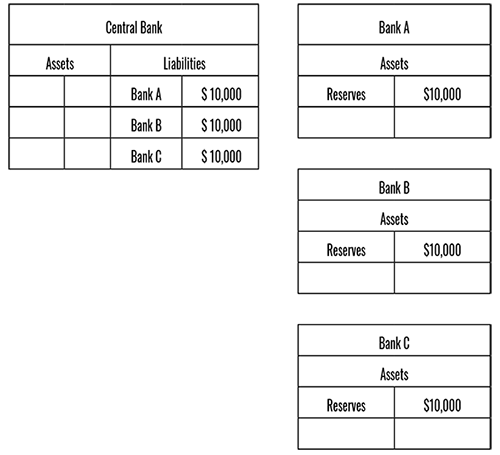

Central bank accounts provide a more efficient way.

One of the roles of a central bank is to enable banks in its jurisdiction to pay each other electronically without each of them having to maintain accounts with one another. The idea is that the central bank acts as a bank for the banks in its currency zone. This allows payments to be made between any of the banks in the jurisdiction, each needs to only maintain one account at the central bank instead of accounts with all the others in the jurisdiction. Money held at the central bank is called reserves.

Central Bank: A banker’s bank

Each bank holds an account with the central bank.

Banks can have multiple accounts with central banks each for different purposes, in the same way that you can have multiple savings pots—a deposit for the home you hope to buy, a holiday, a new car, a wedding, provision for a rainy day, etc. Here, we care about the accounts that are used for interbank payments.

We call the systems that manage these records interbank settlement systems. There are broadly two types:

•Deferred Net Settlement (DNS) systems

•Real Time Gross Settlement (RTGS) systems

DNS Systems

DNS systems are systems that queue up payments due between banks then make a single payment at the end of a given period of time, for example at the end of every day. Payments in both directions are ‘netted off,’ and one single payment of the outstanding balance, in whichever direction it is due, is made at the end of the period. For example, throughout the day Bank A will accumulate payments to make to Bank B, and Bank B will accumulate payments to Bank A. At the end of each day, these payments will be added up against each other and only one single payment will be made representing the net total owed, either by Bank A to Bank B or by Bank B to Bank A, depending on the day’s transactions.

DNS systems are capital efficient. Banks need to set aside only the forecast net amount of outflow in a given period, taking into account the expected inflow. You do the same when you set aside money for next month’s expenses but ‘net off’ your expected income (e.g., your salary) in that period.

But there is a credit risk that builds up during each period, which describes the risk that the forecast inflow doesn’t come in or, in the worst case, a bank becomes bankrupt mid-period. This risk can have a systemic impact, as one failed obligation can impact the recipient’s ability to make their payments. There needs to be a mechanism to ensure least disruption to the remaining participants.

RTGS Systems

With RTGS systems the -$10/+$10 adjustments on the central bank’s books are made in ‘real time’ during the day as soon as a payment instruction is made by a customer. Each payment instruction is settled independently and not grouped, batched, or netted off against any other instructions. This is known as ‘gross settlement,’ the opposite of ‘net settlement’.

DNS systems used to be popular, but nowadays most central banks also operate some kind of RTGS system to settle immediate payment instructions, and customers increasingly expect payments to be made in real time. These RTGS systems operate at least during office hours, and many systems now operate 24x7, at least for small transactions. The trade-off is that banks need to set aside more capital to make sure all payments can be made immediately.

So, back to the example. How does Alice pay Bob if both of their banks are on a RTGS system?

As both Bank A and Bank B are on the central bank’s RTGS system, the central bank performs the -$10/+$10 to remove money from Bank A’s account and add it to Bank B’s account. This is the settlement between the two banks, and in industry terminology, it is said that the central bank ‘clears’ the transaction. The account which each bank holds with the central bank for this purpose is sometimes called their clearing account.