It is worth understanding how digital money is currently used to settle debts. In my career, I have spent time with people with a wide range of experience, from new graduates through to seasoned professionals who wear ties and work in banks and management consultancies, yet I rarely come across people who really understand how a payment is made, and who can articulate clearly how money moves around the financial system.

How Are Interbank Payments Made?

Banks need to pay each other all the time, sometimes because a customer has instructed the bank to make a payment on their behalf, sometimes because a bank needs to pay another bank as a result of its own trading or lending activity. Here we are going to look at the bank to bank payment that arises when a customer wishes to make a payment to someone else who banks elsewhere.

We easily understand physical payments that are made directly when you pay in cash for something without a third-party intermediary. This can be described as ‘peer-to-peer’ as you simply hand over cash to the other person. There’s no one in the middle, you don’t need to instruct or pay a third party, and no one can stop the payment. The cash payment is also resistant to censorship. If you are the recipient, you can be reasonably confident, upon inspection, that the banknote or coins are unique (i.e., not counterfeit copies), otherwise you should not accept them and there is no transaction. It is also obvious that the payer hasn’t spent that same cash already (else they wouldn’t have it to give to you), and furthermore, they can’t use the same cash to simultaneously pay you and someone else (because physical cash can’t exist in two places at once). Of course—this is all intuitive.

As soon as you move into the digital world, things become a little more complex. Digital assets are easy to copy. Unlike physical cash you can’t give a digital asset (e.g., a file) to someone as a currency payment. Well, you can, but they won’t value it because they can’t tell if it is unique. They can’t be sure that you will delete it once you have sent it to them, and they can’t tell if you have sent, or will send, a copy of the file to a different person53. This problem with digital assets is called the ‘double spend’ problem.

Wikipedia54 describes double spending as:

…a potential flaw in a digital cash scheme in which the same single digital token can be spent more than once. This is possible because a digital token consists of a digital file that can be duplicated or falsified.

The digital money world deals with this by using a bookkeeper who is an independent third party, who, because they are regulated, can be trusted to maintain accurate books and records and abide by certain rules. For example, you trust that PayPal is not creating PayPal dollars out of thin air because each PayPal balance must be backed by an equivalent balance in its bank, and you trust that the regulators will do their job and shut PayPal down if they are not behaving. You also trust that when you instruct your bank to make a payment, the amount of money leaving your account is the same as the amount that is entering the recipient’s account (less fees, of course).

So, with any form of digital asset, you need a trusted bookkeeper to maintain a list of who owns what and who plays by some well understood and trusted rules. They often have a licence from an authority that gives them some credibility and increases your confidence that they are carrying out their activities according to certain standards.

Now, let’s dive into how the movement of bits and bytes and debits and credits produces the effect of money moving instantly from one person to another.

How are Payments Made?

How does digital money move from one bank account to another? When Alice wants to pay $10 to Bob, does Alice’s bank simply subtract $10 from her account and tell Bob’s bank to add that $10 to Bob’s account? And then how do the banks settle that $10 up between them?

It can be complex. Let’s build this up by looking at the following scenarios:

1.Same bank

2.Different banks

3.Cross border (same currency)

4.Foreign exchange

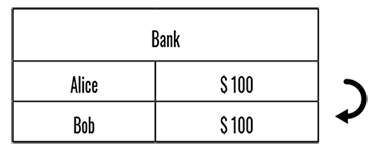

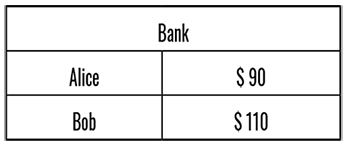

If Alice is trying to pay $10 to Bob and they both have accounts at the same bank, it is relatively straightforward. Alice instructs her bank to make the payment, and they bank then adjusts their records by subtracting $10 from Alice’s account and adding $10 Bob’s account. In banking jargon some banks call this a ‘book transfer’ as it is just a transfer from one account to another and no money moves into, or out of, the bank.

If you imagine a bank as managing a giant spreadsheet with a list of account holders in the first column and a list of balances in another column, the bank subtracts ten from Alice’s row and adds ten to Bob’s row. I refer to this book transfer as a ‘-10/+10’ transaction. Because this accounting entry has been entirely internal to the bank, we can say that the transaction ‘settles across the bank’s books’ or is ‘cleared by the bank’.

Before

After

A book transfer.

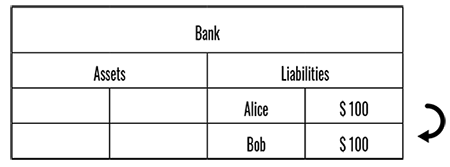

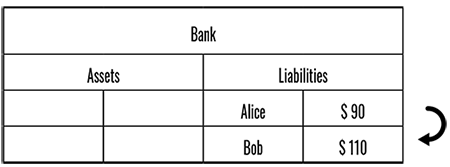

It is important to understand that the money in customer accounts is a liability of the banks: when you log into your online banking and see $100 in your account, this means the bank owes you $100 and should either pay you that money on demand (via a cashier or cash machine), or they need to pay someone else (a coffee shop, a supermarket, or your friend) when you instruct and authorise them to do so.

So while from your point of view the money in your account is an asset, from the bank’s point of view, the money in your account is an outstanding liability. So the transaction on the bank’s balance sheet (where assets and liabilities are recorded) looks more like this:

Before

After

Banks record customer accounts as liabilities.

Although we don’t touch the asset side of the balance sheet for transfers between customers of the same bank, we will need it later.

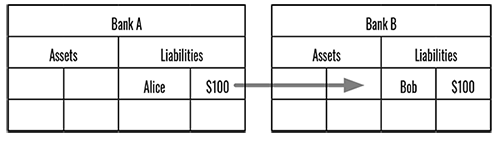

Now consider when Alice wants to pay $10 to Bob, but they bank at different banks, albeit in the same country and currency. Alice instructs her bank, Bank A, to remove $10 from her account and pay it to Bob’s account at Bank B. In banking jargon, Alice is the payer and Bob is the beneficiary.

So Bank A reduces Alice’s balance, and Bank B increases Bob’s balance.

Before

After

Alice pays Bob.

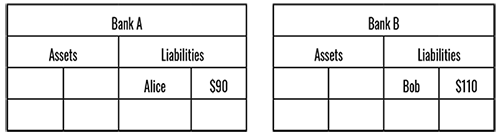

The Problem

While the customers are happy, can you see the problem from the perspective of the banks?

Bank A now owes Alice $10 less than before and so it is better off, but Bank B now owes Bob $10 more and so is worse off. So that can’t be the whole picture. Bank B would be furious!

The Solution

This payment instruction must be balanced by a bank to bank transfer: Bank A needs to pay Bank B $10 to balance out the customer account movements and complete the end to end payment.

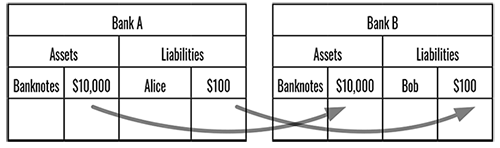

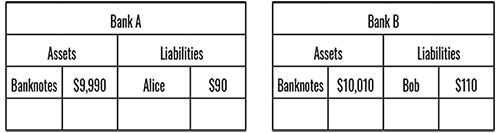

How does an interbank payment happen? Bank A could put a bunch of banknotes in a van and send them to Bank B. This would make both banks square:

•Bank A owes Alice $10 less but pays $10 in banknotes to Bank B

•Bank B owes Bob $10 more but receives $10 in banknotes from Bank A

Before

After

The ‘banknotes in a van’ solution.

But in most countries, when banks want to transfer money to each other, they don’t put bundles of banknotes in vans—they pay each other digitally.

The Digital Solutions

There are two main ways a bank can digitally pay another bank: by using correspondent bank accounts; or by using a central bank payment system.

If you set up a new business, the first thing you would want to do is open a bank account to let you receive and make payments.

Banks are no different. If you set up a new bank, you still need bank accounts in order to participate in digital payments.

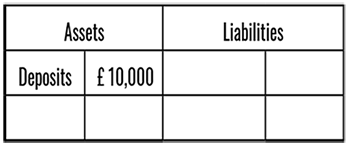

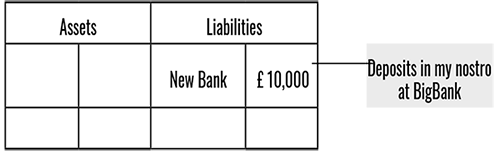

Correspondent bank accounts are industry jargon for the bank accounts that banks open with other banks. These are also called ‘nostros’ (nostro is a Latin word meaning ‘our,’ as in ‘our account’). Correspondent banking describes activities related to the use of these accounts.

In your new bank’s balance sheet, the deposits you hold in your nostros would appear as assets, in the same way as you (as an individual) consider the deposits you hold in your bank to be your assets. The bank that you opened the account with, your correspondent bank, shows those funds as their liability, in the same way as your own consumer bank regards your individual deposits as its liability.

New Bank

Big Bank

Correspondent banking is just banks holding accounts with each other.

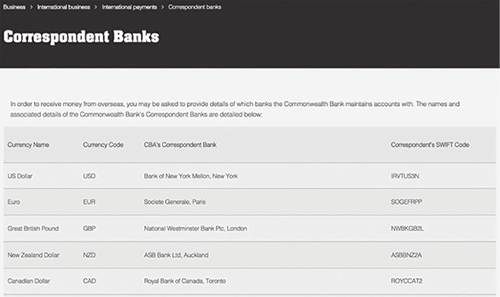

If you google for your bank’s name and ‘correspondent banks,’ you might find a list of accounts where they hold their foreign currency. Here is an example from the Commonwealth Bank of Australia (CBA)55:

You can see that CBA has opened a US dollar account at the Bank of New York Mellon and a Euro account at Societe Generale. The SWIFT codes are identifiers for those specific banks.

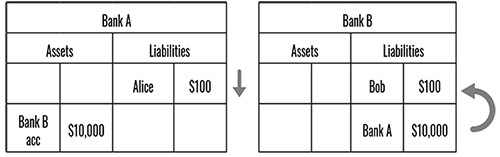

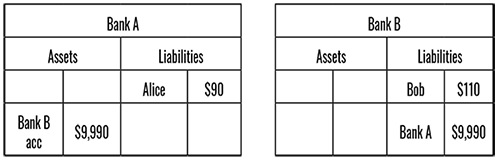

So, back to our example. If Bank A had an account at Bank B, it could instruct Bank B to transfer the $10 from its account to Bob’s account:

Before

After

Bank A pays from its nostro.

In this way, the banks are neatly squared off:

•Bank A owes Alice $10 less but has $10 less in its account with Bank B

•Bank B owes Bob $10 more but owes Bank A $10 less

The Problem with Correspondent Bank Accounts

Although correspondent bank accounts allow payments to flow, they can also present difficulties for the banks themselves. Imagine running a bank and having to maintain accounts at every single other bank that your customers might want to transfer money to. You’d need to open accounts at every single bank in the world, just in case you have a customer who wants to transfer to someone who banks there. This would be an operational nightmare.