Cash—physical money—is wonderful. You can transfer (or spend or give away) as much of what you have as you want, when you want, without any third parties approving or censoring the transaction or taking a commission for the privilege. Cash doesn’t betray valuable identity information that can be stolen or misused. When you receive cash in your hand, you know that the payment can’t be ‘undone’ (or charged back, in industry jargon) at a later date, unlike digital transactions such as credit card payments and some bank transfers, which is a pain point for merchants. Under normal circumstances, once you have cash, it is yours, it is under your control, and you can transfer it again immediately to somebody else. The transfer of physical money immediately extinguishes a financial obligation and leaves nobody waiting for anything else.

But there is a big problem with traditional physical cash: it doesn’t work at a distance. Unless you carry it in person, you can’t transfer physical cash to someone on the other side of the room, let alone on the other side of the planet. This is where digital money becomes highly useful.

Digital money differs from physical money in that it relies on bookkeepers who are trusted by their customers to keep accurate accounts of balances they hold. To put it another way, you can’t own and directly control digital money yourself (well, you couldn’t until Bitcoin came along, but more on that later). To own digital money, you must open an account somewhere with someone else—a bank, PayPal, an e-wallet. The ‘someone else’ is a third party whom you trust to keep books and records of how much money you have with them—or, more specifically, how much they must pay you on demand or transfer to someone else at your request. Your account with a third party is a record of an agreement of trust between you: simultaneously how much you have with them, and how much they owe you.

Without the third party, you would need to keep bilateral records of debts with everyone, even people who you may not trust or who may not trust you, and this is not feasible. For example, if you bought something online, you could attempt to send the merchant an email saying ‘I owe you $50, so let’s both record this debt’. But the merchant probably wouldn’t accept this; firstly, because they probably have no reason to trust you, and secondly, because your email is not very useful to the merchant—they can’t use your email to pay their staff or suppliers.

Instead, you instruct your bank to pay the merchant, and your bank does this by reducing how much your bank owes you, and, at the other end, increasing how much the merchant’s bank owes them. From the merchant’s point of view, this extinguishes your debt to the merchant, and replaces it with a debt from their bank. The merchant is happy, as they trust their bank (well, more than they trust you), and they can use the balance in their bank account to do other useful things.

Unlike cash, which settles using the transfer of physical tokens, digital money settles by increasing and decreasing balances in accounts held by trusted intermediaries. This probably seems obvious, though you may not have thought of it this way. We’ll come back to this later, as bitcoins are a form of digital money which share some properties of physical cash.

There is a big difference between online card payments, where you type the numbers, and physical card payments, where you tap or swipe the physical card. In the industry, an online credit card payment is known as a ‘card not present’ transaction, and swiping your card at the cashier’s till in a shop counts as a ‘card present’ transaction. Online (card not present) transactions have higher rates of fraud, so in an effort to make fraud harder, you need to provide more details—such as your address and the three digits on the back of the card. Merchants are charged higher fees for these types of payments to offset the cost of fraud prevention and the losses from fraud.

Cash is an anonymous bearer asset which does not record or contain identity information, unlike many forms of digital money that by law require personal identification. To open an account with a bank, wallet, or other trusted third party, regulations require that the third party can identify you. This is why you often need to supply information about yourself, with independent evidence to back that up. Usually that means a photo ID to match name and face, and a utility bill or other ‘official’ registered communication (for example from a government department) to validate your address. Identity information is not just collected when opening accounts. It is also collected and used for validation purposes when some electronic payments are made: when you pay online using a credit or debit card you need to supply your name and address as a first gateway against fraud.

There are exceptions to this identity rule. There are some stored value cards that don’t require identity, for example public transport cards in many countries, or low-limit cash cards used in some countries.

Do payments need to be linked to identity? Of course not. Cash proves this. But should they? This is a big question that raises legal, philosophical and ethical issues that remain subject to ongoing debate. Credit card information is frequently stolen, along with personally identifying information (name, addresses, etc) which creates a cost to society.

Is it a fundamental right to be able to make payments which are shielded from the eyes of the state governments? And should people have the ability to make anonymous digital payments, as they do with physical cash? To what extent should our financial transactions be anonymous or, at the very least, private? And what, if any, are the reasonable limits to that privacy? Should the public sector or the private sector provide the means for electronic payments and financial privacy? Should a nation state be able to block an individual’s ability to make digital payments, and with what limits? How can we reconcile financial privacy with the prevention of support for illegal activities, including the funding of terrorism? I won’t provide answers to these big questions in this book, but the fundamental questions concerning financial privacy are inevitably raised when understanding the game-changing innovation that is Bitcoin.

We all know what money is, but how might we define it? The generally accepted academic definition of money usually says that money needs to fulfil three functions: A medium of exchange, a store of value, and a unit of account. But what does this really mean?

Medium of exchange means it is a payment mechanism—you can use it to pay someone for something, or to extinguish a debt or financial obligation. To be a good medium of exchange, it doesn’t need to be universally accepted (nothing is), but it should be widely accepted in the particular context for which it is being used.

Store of value means that in the near term (however you define this) your money will be worth the same as it is today. To be a good store of value, you need to be reasonably confident that your money will buy you more or less the same amount of goods and services tomorrow, next month, or next year. When this breaks down, the money’s value is quickly eroded, a process often referred to as hyperinflation. Individuals quickly develop alternative ways to denominate value and undertake transactions, for example bartering or using a ‘hard’ or more successful and stable currency.

Unit of account means it is something that you can use to compare the value of two items, or to count up the total value of your assets. If you record the value of all of your possessions, you need some unit to price them in, to get a total. Usually that is your home currency (GBP or USD or whatever), but you could in theory use any unit. The last time I counted, I had 0.2 Lamborghinis worth of gadgets in my study. To be a good unit of account, the money needs to have a well-accepted or understood price against assets, otherwise it is hard to figure out the total value across all your assets and, if you need to do so, to convince others of that value.

While some believe that ‘good money’ should fulfil all of these functions, others think that the three functions can be fulfilled by different instruments. For example, there is no real reason why something used as a medium of exchange (i.e., something that can be used to immediately settle a debt) must also be a long term store of value.

Is Today’s Money Good Money?

It is debatable how well the forms of money we generally regard as ‘good money’ stack up against these properties. The US dollar is arguably the most prominent form of money we have today, and can be considered the best, at least for the time being. But how good is it? The dollar is generally acceptable for payment, certainly in the USA, and even in other countries, so it is an excellent medium of exchange in those contexts (but less so in Singapore). And it is an excellent unit of account, because many assets are priced in dollars, including global commodities such as crude oil and gold.

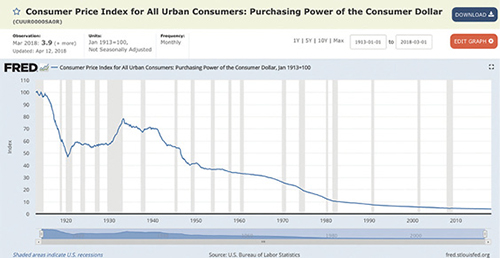

But how has it fared as a store of value? According to the St Louis Fed, the purchasing power of the USD from a consumer’s perspective has fallen by over 96% since the Federal Reserve System was created in 1913.

Source: St Louis Fed4.

Given that purchasing power of the USD over time has decreased significantly, it has been a poor store of value over the long term. Indeed, people don’t tend to keep banknotes under their mattress for decades, because they know cash is not a good store of value. And if they did, they would find that the purchasing power has decreased, or worse, that the banknotes have been pulled out of circulation and are no longer accepted in shops. In fact, the dollar, as with almost all government currencies, consistently loses value by design, driven by policy. We can predict, more or less, that the USD will lose its purchasing power by a few percentage points each year. This is known as price inflation (as opposed to currency inflation which is an increase in the number of dollars in circulation). Price inflation is measured by CPI (Consumer Price Inflation)—an index measuring the changes in the price of a theoretical basket of goods that are reportedly chosen to represent typical urban household spending5. The makeup of the basket changes over time, and policymakers are not beyond employing various tricks with that basket to bend the rate of inflation to figures they find more convenient6.

So perhaps ‘store of value’ is a not a good medium or long term function of money, and perhaps the economists and textbooks don’t have it quite right. We certainly need all three ‘functions of money,’ but perhaps not in the same instrument. Perhaps money fulfils one need (immediate settlement of obligations), whereas the longer-term store of value need can be better achieved through other assets. In terms of the ‘store of value’ function of money, it is more the short-term predictability of value, or spending power, that is relevant: I need to know that a dollar tomorrow or next month can buy me more or less the same thing as a dollar today and will settle immediate debts. But for long term preservation of value, perhaps housing or land or other assets may be more reliable.

How do cryptocurrencies fare against the standard definitions of money?

Bitcoin as a Medium of Exchange

As a medium of exchange, Bitcoin has some interesting characteristics. It is the very first digital asset of value that can be transferred over the internet without any specific third party having to approve the transaction or being able to deny it. It is also an asset that is transferred from one owner to another rather than moving via a series of third party debits and credits, for example, through one or more banks. In this respect it is genuinely novel.

This is worth repeating:

Bitcoin is the very first digital asset of value that can be transferred over the internet without any specific third party having to approve the transaction or being able to deny it.

Can you make payments with bitcoins? Yes, absolutely—anytime, anywhere. Is it fast? Sometimes—depending on a number of factors. At a settlement speed varying between seconds and hours, it is certainly faster than some traditional payment methods, but slower than others. Different cryptocurrencies settle transactions at different speeds.

Is Bitcoin widely accepted? Well, among its community it is widely accepted, and some prefer using it to traditional payment mechanisms7. But by a global standard, no, it is not widely accepted. Could this change? Could more and more people and businesses accept bitcoins or other cryptocurrencies? Perhaps not in large stable economies, but possibly in unstable smaller economies. There are a number of factors to consider when deciding if bitcoins should be used in preference to the domestic currency or existing alternatives.

What about merchant adoption? Every now and again, you might read that a merchant now accepts bitcoins or other cryptocurrencies as payment. What’s going on? Doesn’t this mean bitcoins are improving as a medium of exchange? Well, yes and no. In reality, most of the companies who say that they accept Bitcoin as payment don’t actually accept bitcoins or hold them on their balance sheets. Instead, they use cryptocurrency payment processors that act as an intermediary by quoting a price to the customer in bitcoins (based on current prices of bitcoins to dollars on various cryptocurrency exchanges), accepting the bitcoins from the customer, then wiring an equivalent amount of conventional currency (fiat in the jargon) the boring way into the merchant’s bank account.

Here is how it works:

1.The customer fills their shopping cart with items, then clicks ‘check out’.

2.They are presented with the total value of the goods in local currency. ‘How would you like to pay?’

3.Customer selects ‘Bitcoin’.

4.They are then shown the number of bitcoins that they need to pay. The payment processor calculates this number by using the current exchange rate between Bitcoin and local currency, found on one or more cryptocurrency exchanges.

5.The customer then has a short amount of time to accept the price before the price of Bitcoin changes and the payment processor has to re-price the basket. The pricing refresh time can be as short as 30 seconds due to Bitcoin’s volatility. 30 seconds!

Bitpay8 is a good example of this kind of cryptocurrency payment processor. In 2013-2015 a number of merchants announced that they now accepted Bitcoin. This was good cheap press for merchants, and many companies did this: Microsoft, Dell, and even—my favourite—Richard Branson for Virgin Galactic trips. Just think—in 2013 you could buy a trip into space and pay in bitcoins! However, since then, many merchants have quietly dropped Bitcoin as a method of payment.

So, in these cases where a merchant says they accept Bitcoin as payment, bitcoins are a medium of exchange from the customer’s perspective. But these cases are rare, and currently it is not a widely used medium of exchange. In July 2017, investment bank Morgan Stanley produced a report on Bitcoin merchant adoption9 that found that, in 2016, only five of the top 500 online merchants accepted Bitcoin and, in 2017, that number had dropped to three.

Bitcoin as a Store of Value

For now, let’s put aside the argument about whether ‘store of value’ is a valid property of money, or if it should be an attribute of an asset.

Instead, let’s ask the question, what do you want from your store of value? What is its job? Is its job to make you richer so you can buy more toys, or is its job to maintain its value so you can plan your life well? And if the job of the thing is to make you richer so you can buy more toys, how much volatility and downside risk are you willing to stomach? Are we talking about a short-term store of value, perhaps a speculative investment, or a long-term store of value, often a lower risk asset?

Bitcoin as a speculative investment has performed amazingly well. Anything that starts at a price of zero, and is not currently at a price of zero, is great. Bitcoin started at zero value in 2009 and now, less than ten years later, each Bitcoin is worth thousands of dollars. So it has certainly appreciated in value since its creation. But would you buy it now? Would you move all your savings into this asset in order to store value (as opposed to gamble and hope for a quick price appreciation)? Well, due to its price volatility, which is very high compared to most fiat currencies, the answer is probably no if you are looking for a stable store of value. As a long-term store of value I suppose you want, as a minimum, something that can be used to buy a basket of goods in twenty years’ time roughly identical to the basket you can buy with it now. So, if you had bought it at the right time, Bitcoin has certainly been a good investment, but its volatility makes it a nauseating store of value.

Does Bitcoin, or do other cryptocurrencies, have the potential to keep value over the long term, as some people expect from gold? Possibly. According to its current protocol rules, bitcoins are created at a known rate (12.5 BTC every 10 minutes or so)—and that rate will decrease over time. So the supply of it is understood and predictable, capped to almost 21 million BTC and not subject to arbitrary creation, unlike fiat currencies10. Limiting the supply of something can help maintain its value if demand is stable or increases, though the downside of a known, predictable, and completely inelastic supply unrelated to a fluctuating demand results in perpetual price volatility11, which is not good if you are looking for price stability.

Bitcoin as a Unit of Account

As a unit of account, Bitcoin fails miserably, due to its price volatility against USD and everything else in the world. The fact that there are almost no merchants who are willing to price items in bitcoins (not even merchants who sell cryptocurrency related paraphernalia) is evidence that bitcoins are not a good unit of account.

You wouldn’t keep your accounts in BTC. You wouldn’t record the price of your laptop in BTC. You certainly wouldn’t do your year-end bookkeeping in BTC12, and if you tried to file mandatory accounts in BTC you would fall foul of accounting standards in all jurisdictions. If you were a masochist, you could prepare an inventory and denominate everything in BTC, but first you’d figure out the price of things in USD (say, my laptop is worth about $200), then you’d convert that number to a Bitcoin number at a ‘what is the price of Bitcoin in dollars at this very second?’ ratio. So then, very briefly, you could say ‘all my worldly possessions are worth 3.0364 BTC’. Within minutes or hours, that BTC number would almost certainly be meaningless as the BTC to USD price fluctuates so rapidly.

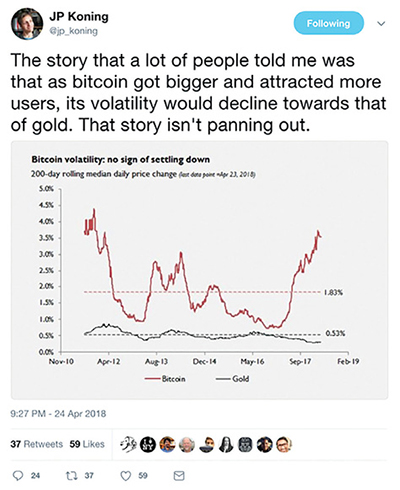

Monetary economist JP Koning compared the price volatility of Bitcoin to gold and made the following observation on Twitter13:

Will the price volatility of Bitcoin decrease? It is anyone’s guess, but I personally doubt it. One argument I used to hear was, ‘When the price of BTC gets really high, the price volatility will decrease because it will take a lot more money to bully the price up and down’. The argument is flawed. A price can be high, but if a market is illiquid, small amounts of money can still push the price around. Stability is determined more by the liquidity of a market (how many people are willing to buy and sell at any price point), than the price of an asset. But even liquid markets can move quickly if the market’s perception of the value of the asset changes suddenly. Also, this argument is predicated on the price of Bitcoin getting really high… There is no good reason why the price of Bitcoin should ever go ‘really high’. Furthermore, as discussed earlier, Bitcoin’s supply is inelastic. If there is a spike in demand, there is no impact on the rate at which bitcoins are generated, unlike normal goods and services, so there is no dampening effect on the price, and this holds true for any price point—even if volatility decreased, traders may just take bigger bets, often with leverage, which would then move the price again.

At the time of writing there is a quest for ‘stable coins’—cryptocurrencies whose prices are relatively stable compared to some other thing, for example a US dollar. Unless they are backed 1 to 1 with the relevant asset, stable coins are very hard to produce because essentially you are trying to peg the price of something dynamic to something else with a different dynamic, and as we will see in the next section about history of money, no one has ever been successful at this in the long term: Pegs always eventually break. If a successful stable coin were to emerge, things could become more interesting14.

There is one case where BTC may be used as a unit of account: when valuing baskets of other cryptocurrencies. If you are a normal trader trading normal assets like shares, it is a good idea to understand the current value of your assets in your home currency—for example USD, EUR, or GBP. If you are a cryptocurrency trader, you probably still want to understand your total asset value in your home currency, but in this very specific case, you may also want to understand your total balance in BTC as it is the market leader in the cryptocurrency world—you could say BTC is the USD of cryptocurrencies. Perhaps your investors let you manage some bitcoins with the hope that you will turn their bitcoins into more bitcoins. In this case, the value of your assets in BTC is more important than the value in USD. This is a niche case.

The Current State of Cryptocurrencies as Money

Mark Carney, Governor of the Bank of England, summarised the current state of the moneyness of Bitcoin during a Q&A session at Regent’s University London on 19 February 201815:

‘[Bitcoin] has pretty much failed thus far on…the traditional aspects of money. It is not a store of value because it is all over the map. Nobody uses it as a medium of exchange…’

Bitcoin may be suffering growing pains in its infancy, but this doesn’t mean that we should write it off and that the story must end here. According to the Bitcoin Obituary website,16 Bitcoin has been declared dead over 300 times! But it lives on—at the very least, it still trades on exchanges with a nonzero price. It seems that people try to fit Bitcoin into an existing bucket (‘It is a currency / asset / property / digital gold’), and when it exhibits some properties that do not match others in that bucket, it is declared a failure. Maybe the answer is to not try to fit it into any existing bucket, but to design or define a new bucket, and to judge Bitcoin and other cryptoassets on their own merits.

Also note that central bankers have a potential conflict of interest when commenting on new forms of money. Central bankers have a critical role to maintain monetary and economic stability, and their tools (quantity of money in the economy and the price of borrowing money) are applied to their respective fiat currencies. Any new form of money, if widely adopted and if not under the control of the central bank, could potentially undermine the ability of the central bank to fulfil its mandate. New forms of money could be disruptive and destabilise economies, which, from a central banker’s point of view is not a good thing. So you wouldn’t expect central bankers to warmly embrace new forms of money that are not under their control.

A Brief History of Money—Dispelling the Myths

So far, we have discussed cryptocurrencies and how they measure up as ‘money’ as we currently define it. But has money always been the same? In order to understand where cryptocurrencies might fit in, we should try to understand the history of money itself—its successes, failures, and technological innovations. It is a fascinating topic, as there are so many interesting tidbits and common misunderstandings to straighten out.

The definitive writing on the subject is A History of Money from Ancient Times to the Present Day by Glyn Davies17 who spent nine years researching the book as Emeritus Professor of Banking and Finance at the University of Wales. His work is summarised by his son Roy Davies on the Exeter University website18. Much of this section is based on the timeline outlined by Roy, used with his permission. Errors and omissions are mine. I hope you’ll find this section as fascinating as I did while researching this book.

The concepts and eras I want to touch on are:

•Barter (let’s exchange valuable things)

•Commodity money (the money is the valuable thing)

•Representative money (the money is a claim on the valuable thing)

•Fiat currency (the money is completely de-linked from any valuable thing)

Barter

It is common knowledge that before money existed transactions were carried by exchanging goods when both parties agreed on the deal. ‘Sir, your five ugly old sheep for my twenty bushels of fine corn’. But barter is difficult. It is very rare that you want something the other person has, and at the same time, they want something you have, and that you’re both prepared and able to make a trade. Economists call such a rare situation a ‘double coincidence of wants,’ and aside from market days in subsistence economies this situation almost never occurs. So, the argument goes, money was invented to lubricate the deal. Money is something that everyone is happy to accept in exchange for other things, so it serves as the intermediary asset for the times when you don’t have something that the other person wants. In summary, the inefficiency of barter gave rise to money.

This elegant argument seems intellectually neat. Unfortunately, however, there is not a shred of evidence for it. It is pure fantasy—the textbooks are wrong! When you hear someone talk about money being invented to replace barter, do please educate them or talk to someone else.

Money solving the inefficiencies of barter is a myth popularised in 1776 by Adam Smith in The Wealth of Nations. Ilana E Strauss discusses this in an amusing and eye-opening read, ‘The Myth of the Barter Economy’ published in The Atlantic19, in which she quotes Cambridge Anthropology Professor Caroline Humphrey in a 1985 paper, ‘Barter and Economic Disintegration’20:

‘No example of a barter economy, pure and simple, has ever been described, let alone the emergence from it of money, … All available ethnography suggests that there never has been such a thing’.

Economies developed based on mutual trust, gifts and debt or social obligations—‘Have a chicken now, but please remember this for later’. Early communities were small and stable, and individuals tended to grow up with each other and know each other well. Reputation within a community was crucially important, so people didn’t tend to renege on their word. But people still had to keep some sort of record of debts or favours owed. Trading (the simultaneous exchange of non-monetary goods) did exist, but mainly occurred where there was a lack of trust, for example with strangers or enemies, or where there was a strong possibility that debt wouldn’t be remembered or couldn’t easily be repaid, such as with travelling merchants.

The emergence of money to solve the problem of repaying a debt or favour makes more sense than the emergence of money as a solution to the double coincidence of wants. Indeed, David Graeber details the existence of debt and credit systems before money, which itself appeared before barter, in his fascinating and influential book Debt: The First 5,000 Years21.

Commodity Money

With commodity money the physical token that is transacted is itself valuable, for example grain, which has intrinsic value, or precious metals, which have extrinsic value.

Good forms of commodity money have a stable and known value and are relatively easy to keep and exchange, or ‘spend’. They also need to be consistent, and a standardised unit makes things easier. Examples are standardised quantities of grain or cattle, which have intrinsic value by being edible, and precious metals or shells, which have extrinsic value by being both scarce and beautiful.

Note: An argument that cryptocurrency proponents like to use is that the tokens should be valuable because they are scarce (‘There will only be 21 million bitcoins ever, so that is what makes them valuable!’). This is not a solid argument. Something may be scarce, but that doesn’t mean it is, or should be, valuable. There must be one or more underlying factors that make it desirable—beauty, utility, something else. And these underlying factors must create demand for the item. The two underlying factors in Bitcoin that create demand are:

1.It is the most recognised instrument of value that can be transmitted across the internet without needing permission from specific intermediaries.

2.It is censorship resistant.

Representative Money

Representative money is a form of money whose value is derived by being a claim on some underlying item, for example a receipt from a goldsmith for some gold they are safekeeping. The receipt may be passed to another party to transfer that value. You could say that the value of the token is backed by the value of the underlying asset. Warehouse accounts or receipts (or ‘tokens’) are backed by the value of the goods contained in the warehouse and are good examples of representative money.

Representative money differs from commodity money in that it relies on a third party (e.g., the manager of the warehouse or the goldsmith) to be able to supply the underlying item on redemption of the tokens, so there is some counterparty risk: What if the third party fails?

Representative money tokens were similar to bearer bonds, where the person holding a piece of paper was entitled to reclaim the value of the underlying asset (sometimes on demand, sometimes on a due date). These tokens were used as we use cash today to settle transactions, and were a stepping stone between use of commodity money (e.g., precious metal coins) and fiat currency.

Fiat Currency

Commodity money was gradually replaced by representative money which in turn has now almost entirely been replaced by ‘fiat money’. All major recognisable sovereign currencies now are fiat. Fiat (pronounced fee-at, Latin for ‘let it be done’) is money because legislation says so, rather than because it has a fundamental or intrinsic value. Fiat money neither has intrinsic value nor is it convertible22. Statements on banknotes often say something along the lines of ‘I promise to pay the bearer on demand the sum of …’ but you won’t get very far if you go to the issuer of the fiat currency—usually the central bank—and say, ‘Hey, give me some of the underlying asset back for this’. At best you will get a new banknote.

So how and why are fiat currencies valuable? Two main reasons:

1.They are declared by law as legal tender, meaning that in that legal jurisdiction it must be accepted as valid payment for a debt. Therefore people use it.

2.Governments accept only their own fiat for tax payments. This gives fiat currencies a fundamental usefulness, as everyone needs to pay tax23.

The Economist newspaper has described cryptocurrencies as having fiat characteristics24 as it is simply declared so, but to date, cryptocurrencies have not been declared legal tender in any nation. We will discuss legal tender later in the book.

Here I have tried to pick out interesting events in the history of money that help to form a picture of how we got to where we are now.

9,000 BCE: Cattle—Commodity Money

The earliest forms of commodity money were livestock, particularly cattle, and plant products such as grain. Cattle have been used as commodity money from c.9,000 BCE. As such, the cow is probably the most enduring, if not successful, form of money. They are still used today in some parts of the world. For example, in March 2018, 100 cattle stolen in Kenya were believed to be used for paying a dowry25.

Would a cow pass the three ‘is it money’ questions that economists like to use? History tells us that cows are a medium of exchange, so it ticks that box. You would assume that if it is used for buying and selling things, people might have some sort of idea of the price of other objects in cows. If so, that would make a cow a decent unit of account. But is it a store of value? Hmm, there are some complexities—the price of cows varies by breed and age and individuals can drop down dead. On the other hand, cows have a kind of interest rate, in that they are able to reproduce. So, while any single cow may not be a very good store of value, a herd arguably is. Monetary economists enjoy arguing about things like this.

3,000 BCE: Banks

Between about 3,000 and 2,000 BCE, banks were created in Babylon, Mesopotamia, the land now roughly equating to Iraq, Kuwait, and Syria. Banks evolved from the warehouses that were places for the safekeeping of commodities such as grain, cattle, and precious metals.

2,200 BCE: Lumps of Silver

Around 2,250-2,150 BCE silver, ingots were standardised and guaranteed by the state in Cappadocia (in present day Turkey), and this helped their acceptance as money. Silver was the ‘gold standard’ of precious metal money. This notes an interesting shift from using commodities that clearly have an intrinsic value (cattle and grain that you can eat) to commodities that have an extrinsic value because of their scarcity and durability. During this shift, you can imagine people then having the same arguments as we do today with Bitcoin. ‘Yes, but silver doesn’t have intrinsic value—I can’t feed my family with it’. At the next dinner party if ‘intrinsic value’ is brought up, you can say ‘Come on guys, we’ve been having this argument since 2,200 BCE…’

1,800 BCE: Regulation!

If you want to blame someone for regulation, blame Hammurabi, sixth King of Babylon, who reigned between 1792 and 1,750 BCE and developed the Code of Hammurabi. This set of laws was once considered the earliest written legislation in human history, and the 282 case laws include economic provisions (prices, tariffs, trade, and commerce), family law (marriage and divorce), as well as criminal law (assault, theft), and civil law (slavery, debt). It included the very first laws for banking operations.

Hammurabi code on a clay tablet. Source: Wikimedia26.

Just think—those libertarians who proclaim that regulation is unnecessary, but then demand that something must be done when they lose money in cryptocurrency scams, are just discovering the value of regulations that have existed ever since laws were first written down!

1,200 BCE: Shell Money

In 1,200 BCE, cowry shells were used as money in China. Cowries are sea snails, most commonly found on the shores of the Indian Ocean and the waters of Southeast Asia. Wikipedia describes cowries as:

a group of small to large sea snails, marine gastropod molluscs in the family Cypraeidae, the cowries. The word cowry is also often used to refer only to the shells of these snails, which overall are often shaped more or less like an egg, except that they are rather flat on the underside.

A living cowry. Source: Wikipedia27

According to the World Register of Marine Species28 (WORMS), the zoological name for cowries is Monetaria Moneta (Linnaeus, 1758). This sea snail is so ‘money’ the scientists named it ‘money money!’

In fact, the Chinese named these creatures as ‘money’ well before the West did—the radical 貝(贝 in simplified Chinese and pronounced bèi), means shell or currency, and it even looks like one of the cowries. Chinese words and characters related to money, property, or wealth often use this radical.

Cowry shells. Source: Wikipedia29

As with cattle, the practice of using cowry shells as money survived until as recently as the 1950s in parts of Africa.

700-600 BCE: Mixed Metal Coins

In 640-630 BCE, we see the earliest examples of coins in Lydia (now Turkey), which was a trading hub with large gold supplies. The first coins were made of a naturally occurring mixture of gold and silver called electrum. It is no coincidence that one of the earliest popular Bitcoin wallets, created in 2011 by Thomas Voegtlin, is also called Electrum30!

Lydian coins. Source: britishmuseum.org31

According to the British Museum, these coins were not consistently round, but were created to various standard weights. It is thought that the coins were weighed rather than counted for many transactions.

600-300 BCE: Round Coins

The first round coins emerged in China, made of base (non-precious) metals. These were still commodity money, so their value was the value of the metal, which was low. Their low value meant that the coins were useful for daily transactions.

c. 550 BCE: Pure Precious Metal Coins

Lydia, which must have been the Silicon Valley of the Iron Age world, continued to innovate, producing separate silver and gold coins, and usage of these started to spread. I suppose this is one of the earliest examples of ‘FinTech’ (financial technology): using technology to invent new financial instruments. Next time a banker effuses that they are pioneers of FinTech, you can tell them that Lydians got there first in 550 BCE!

According to Amelia Dowler, curator at the British Museum,

Silver was more widely available than gold and with a lower value could be used for smaller transactions and was therefore better in the marketplace. So, it was silver coinage which gained rapidly in popularity and, during the sixth century BC, mints opened in Greek cities across the Mediterranean.

Source: bbc.co.uk32

405 BCE: First Example of Gresham’s Law

In 405 BCE, Aristophanes’ famous political satire The Frogs was produced. It tells of the adventures of Dionysus and his slave in their quest to bring witty poet Euripides back from the underworld to Athens, which had become boring. The play contains the first known example of Gresham’s Law, that bad money drives out good. What this means is that you’d rather hold on to good/more valuable money and spend the bad/less valuable money if others will accept it. So if you have the choice between spending a pure gold coin or a debased gold coin (with other base metals mixed in), and they both have the same face value, then you will of course spend the debased one, and the good money disappears from circulation.

Here is the Chorus lamenting that they now use new ugly copper coins instead of old gold coins—and with a bit of anti-immigrant sentiment thrown in for good measure:

The freedom of the city has often appeared to us to be similarly circumstanced with regard to the good and honourable citizens, as to the old coin and the new gold. For neither do we employ these at all, which are not adulterated, but the most excellent, as it appears, of all coins, and alone correctly struck, and proved by ringing every where, both among the Greeks and the barbarians, but this vile copper coin, struck but yesterday and lately with the vilest stamp; and we insult those of the citizens whom we know to be well-born, and discreet, and just, and good, and honourable men, and who have been trained in palæstras, and choruses, and music; while we use for every purpose the brazen, foreigners, and slaves, rascals, and sprung from rascals, who are the latest come; whom the city before this would not heedlessly and readily have used even as scape-goats.

Translation source: libertyfund.org33

345 BCE: Origins of the Words Mint and Money

In the centre of Rome a temple was built, dedicated to goddess Juno Moneta. Juno was the goddess of protection and Moneta is derived from the Latin monere, which means ‘to warn or advise’. It is said that Goddess Juno gave warnings or advice on at least a couple of occasions. First, when the Gauls sacked Rome in 390 BCE, Juno’s sacred geese gave Roman commander Marcus Manlius Capitolinus a heads up that the Gauls were coming, allowing him to protect the Capitol. Second, during an earthquake when a voice from the temple advised the Romans to sacrifice a pregnant sow34.

From 269 BCE, the Roman mint was located at this temple, and lasted some centuries. The English words ‘mint’ and ‘money’ are derived from Juno Moneta.

336–323 BCE: Gold to Silver Peg

Alexander the Great simplified the silver to gold exchange rate by declaring a fixed exchange rate of ten units of silver equal to one unit of gold. This peg eventually failed.

The Americans effectively tried the same thing in the eighteenth century at rates of 15:1 and 16:1. Later, we will discuss what currency pegs are, how they are managed, and how difficult they are to maintain. This is relevant today because there are a number of attempts to create a ‘stable coin’ cryptocurrency, some of which rely on an entity or automated smart contract to defend a peg by buying when the price is too low and selling when the price is too high.

323–30 BCE: Warehouse Receipts—Representative Money

Ptolemy, a Greek bodyguard of Alexander the Great, established himself as ruler of Egypt. He created a dynasty which ruled Egypt until the demise of Cleopatra with the Roman conquest of 30 BCE. The Ptolemies, as the rulers were known, established a system of warehouse accounts where debts could be repaid by transferring the title to grain from one owner to another without physically moving the grain stored within.

118 BCE: Leather Banknotes

Square white deerskin leather with colourful borders was used as money in China. This is possibly the first documented type of banknote. China would later experiment with paper-based banknotes, then stop using them for a few hundred years before reintroducing them.

30 BCE–14 CE: Tax reform!

Augustus Caesar, adopted son of Julius Caesar, expanded Rome’s taxation of the provinces, regularising tax levies which, until then, had been decentralised to the provinces. He introduced sales, land, and poll taxes. These taxes weren’t universally unpopular, especially in the provinces, where taxes until then had been somewhat arbitrary. If you hate paying taxes, you probably hate paying arbitrary taxes at arbitrary frequencies even more. Augustus Caesar also issued new, almost pure, gold, silver, brass, and copper coins.

To 270 CE: Debasement and Inflation

Over the next 300 years, the silver content of Roman coins fell from 100% to 4%. Talk about debasement! But as we saw earlier, the US dollar has fallen in value by 96% in a third of the time35. Attempts by leaders such as Emperor Aurelian to purify coinage failed, as Gresham’s Law kicked in and people circulated their debased coins and hoarded the pure ones.

306–337 CE: Gold for the Rich, Debased Coins for the Poor

Constantine, the first Christian Roman emperor, issued a new gold coin, the Solidus, which was used successfully and without debasement for the next 700 years. That is quite some achievement. However he also produced debased silver and copper coins. So the rich got to use nice shiny gold coins that retained value while the poor got coins that steadily decreased in value. Is that surprising?

c. 435 CE: No More Coins for Brits for 200 Years

Anglo-Saxons invaded Britain and coins were no longer used as money for 200 years! Money, it turns out, can come in and out of fashion, depending on the politics at the time. Just because we grow up with one form of money, it doesn’t mean it will last forever.

806–821 CE: Fiat Money in China

Due to a shortage of copper, Chinese emperor Hien Tsung issued paper money notes for merchants who wanted to make large payments without the inconvenience of heavy coins. Over the next few hundred years there was much overprinting and inflation, causing paper money to depreciate against metals. This is a theme we hear over and over again.

Paper money spread to Europe via Marco Polo, a Venetian who travelled extensively and learnt of paper money from his travels in China from 1275–1292.

Paper money was only used in China for a few hundred years, during which time inflation soared due to uncontrolled printing of paper money. In the 1400s, they seem to have stopped using paper money for a few hundred years.

1300s: British Pennies Shrink Twice

In 1344 and 1351, on two separate occasions, King Edward III reduced the size and quality of the penny. The King owned the mints, so a smaller and less fine penny meant that the King could issue more pennies from the same amount of metal, meaning more profits or seigniorage for the King.

The debasement of all forms of money that is not commodity money seems to be a common theme in the history of money.

1560: Gresham’s Law!

Another year, another currency reform: this time Queen Elizabeth I recalled and melted coins, separating the base metals from the precious metals. Thomas Gresham became an advisor to the Queen and noticed that bad money drives out good.

1600s: The Rise of the Goldsmiths

Goldsmiths in Britain became bankers, as their vaults were used for coin storage, and their notes and receipts became a convenient method of payment.

1660s: Central Banking

The world’s oldest central bank, Sveriges Riksbank, was created in Sweden. Initially, the Bank was forbidden to issue banknotes due to lessons learnt from Stockholms Banco, Sweden’s first bank. Stockholms Banco issued Europe’s first banknotes but got carried away and issued more than could be redeemed, a money creation technique known as fractional reserve banking. Stockholms Banco failed when banknote holders wanted the underlying metal coins back. In 1668, Sveriges Riksbank was founded and later, in 1701, it was allowed to issue banknotes, then called credit notes. It gained exclusivity over banknote printing 200 years later in 1897 with the first Riksbank Act.

The home of the Riksbank at Järntorget in the old town of Stockholm. Source: Riksbank36

The Riksbank is noted for its attitude towards innovation: in July 2009, it was the first central bank to charge money from commercial banks to maintain overnight deposits, rather than paying interest, pushing the overnight deposit rate down to -0.25% (annualised). It deepened this interest rate, as well as other associated rates, in 2014 and 2015. This was an effort to stimulate the economy by encouraging the lending and spending of money rather than hoarding, when quantitative easing was not having the desired effect.

1727: Overdrafts!

The Royal Bank of Scotland was founded, introducing an overdraft facility where certain applicants were able to borrow money up to a certain limit and were charged interest only on the amount drawn, rather than on the full amount. This was a form of FinTech.

1800-1860: Cowrie Depreciation

Here is a powerful example of how the supply of money causes price inflation: When cowrie shells were first introduced to Uganda around 1800, a woman could typically be bought for two shells. Over the next 60 years, as more shells were imported at scale, prices rose, and by 1860 a woman commanded a price of one thousand shells.

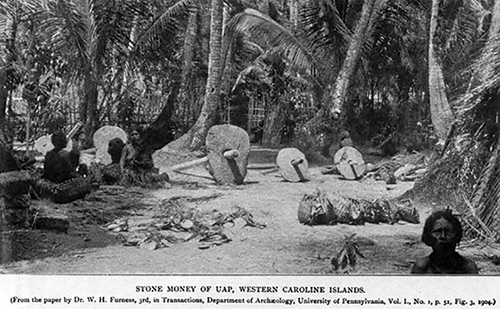

Rai Stones

No history of money would be complete without mentioning the Rai (sometimes called Fei) stones still in use on the island of Yap.

Yap is a small island in the Federated States of Micronesia, approximately 2,000km east of Manila, Philippines. It is known for its superb SCUBA diving and its Rai stones. Rai stones are large, circular stone discs with holes in the middle, to help transportation. They are made with stone quarried from Palau island, about 400 km away, brought back by canoe with some effort, and still are used as money today.

John Tharngan, Historical Preservation Officer of Yap, in an interview with the BBC37, explains the origin of the Rai stones:

Several hundred years ago, some people from Yap went on a fishing trip and got lost and arrived accidentally in Palau. They saw the limestone structures that occur naturally on that island and thought they looked great. They broke off a piece of stone and did a bit of carving on it with shell tools. They brought home a stone that was shaped like a whale, which is called ‘Rai’ in Yapese and that is where the word comes from.

Rai stones come in all sorts of sizes, from a few hand spans to over 3 metres in diameter, and have a value mainly based on their history, but also on their size and finish. According to monetary economist JP Koning’s excellent blog Moneyness38, W.H. Furness, who spent a year on the island, wrote in his 1910 book The Island of Stone Money, Uap of the Carolines:

A rai spanning a length of three hands and of good whiteness and shape ought to purchase fifty ‘baskets’; of food—a basket is about eighteen inches long and ten inches deep, and the food is taro roots, husked coconuts, yams, and bananas;- or, it is worth an eighty or a hundred pound pig, or a thousand coconuts, or a pearl shell measuring the length of the hand plus the width of three fingers up the wrist. I exchanged a small short handled axe for a good white rai, fifty centimeters in diameter. For another Rai, a little larger, I gave a fifty pound bag of rise… I was told that a well-finished rai, about four feet in diameter, is the price usually paid either to the parents or to the headman of the village as a compensation of the theft of a mispil [a woman].

In terms of recording the of ownership changes of these unwieldy pieces, Tharngan comments:

There’s no problem in knowing who owns which piece because all the pieces next to a dwelling tend to belong to that house. All those which are found on dancing grounds—their ownership does shift from time to time, but the shift is always done publicly in front of chiefs or elders, so everyone remembers what belongs to whom.

There is also the case of a large stone that was lost at sea, recorded by Furness who heard the legend recounted by a local fortune teller and exorcist. The fortune teller told Furness that a few generations ago a large stone was lost at sea, and even though it is not physically present and no one can see it, claims on the stone continue to have value.

This particular Rai stone is used by some economists as an example of fiat money existing in primitive societies. However, Dror Goldberg argues in a 2005 paper, Famous Myths of Fiat Money39 that this is not fiat. There was no evidence of this stone being used in trade, as ownership remained in the family, and the value of the lost stone was agreed by the community, not by any legal decree. Goldberg argues that Rai stones have legal, historical, religious, aesthetic, and sentimental value, and are therefore not fiat, and furthermore, there are no good examples of fiat money existing in primitive societies.

1913: Birth of the US Federal Reserve System

In 1913, the Federal Reserve Act was passed into law in the USA. This created the Federal Reserve System, the central banking system of the USA. The act was drafted by influential commercial bankers and gave the central bank the monopoly on the price and quantity of money, and had the mandate to maximise employment and ensure price stability. The system has public and private sector components, and the regional Federal Reserve Banks are owned by large US private banks. The Federal Reserve is discussed in greater detail in the Appendix.

The US dollar remained on a gold standard for a period of time under the Federal Reserve System, as we will see in the section about gold standards.

1999: The Euro

On 1 Jan 1999, the Euro officially became the currency of the member states of the European Union: Belgium, Germany, Spain, France, Ireland, Italy, Luxembourg, the Netherlands, Austria, Portugal, and Finland. Euro notes and coins came into circulation in 2002. The currency is now the official currency of nineteen of the current twenty-eight EU states, six non-EU jurisdictions, and a number of other non-sovereign entities.

2009: Bitcoin!

On 3 January 2009, the first Bitcoin was brought, or ‘mined,’ into existence. How does Bitcoin relate to money? We’ll discuss Bitcoin in a lot more depth later on, but it was first commonly described as a ‘cryptocurrency’. And simply because of the word ‘currency’ people start thinking… Is it money? Does it fulfil the traditional three functions of money? What is money anyway? Does Bitcoin count?

Defining Bitcoin is a popular activity for regulators and policymakers who need to determine if bitcoins fall under their purview or not. I suspect things would have worked out differently had Bitcoin been originally described as a ‘cryptocommodity’ or a ‘cryptoasset’. It turns out that Bitcoin is hard to shoehorn into existing categories, so perhaps it, along with other crypto-things, belongs in a new asset class.

That fact is, for our purposes, the definition of Bitcoin doesn’t matter. It doesn’t matter how you define money, it doesn’t matter it Bitcoin fits the bill or not. Bitcoin has some properties that make it appear from one angle like money, and from another angle like a commodity such as gold.

Money is in the eye of the beholder. Nowadays, we have so many different forms of money, all with slightly different characteristics and trade-offs, that Bitcoin and its siblings can, and will, sit alongside the other forms.

Good Enough Money

I like to use the concept of ‘good enough money’. If the money you want to use is good enough for your purposes, then that is ok. For example, when I borrow cash from my colleagues to buy my lunch, sometimes I pay them back in Grab credits.

Grab is a ride-hailing app similar to Uber, but localized for Asia, and it also has a wallet function which you top up with your credit or debit card. The credits are denominated in local currency and can be used to pay for journeys, sent to other users, or used to pay for goods in some shops. Some of my colleagues use Grab for their taxis, so paying them back in Grab credits is fine for me and fine for them. So, Grab credits are ‘good enough money’ as far as we are concerned for that particular small denomination use. But I wouldn’t buy a house with Grab credits, nor would a company settle a large invoice with it. It wouldn’t be ‘good enough money’ in those situations.

It seems that people and companies will accept a wide range of forms of money so long as they can do the next thing with it—whether that is paying for a taxi, settling invoices, or saving it for long term value appreciation.

Some people talk about The Gold Standard. In fact, there is no such thing as the gold standard. There are a few types of gold standard:

1.Gold specie standard. Coins are made of gold and are a certain weight and purity in convenient standard units instead of random shapes, sizes, and weights. This is called a gold specie standard. Specie is a Latin word for ‘the actual form’. This is commodity money.

2.Gold bullion standard. Notes (bits of paper) are redeemable or convertible at the issuer (usually the central bank) for gold—usually in the form of gold bullion (this means bars of gold of certain standard weights and purities). This is called a gold bullion standard. This is representative money.

3.Non-convertible gold bullion standard. This is where the issuer declares that their currency is worth a certain amount of gold, but doesn’t allow you to redeem your money for gold. This is starting to blur the lines between representative and fiat money.

When people talk about the gold standard, they usually mean a gold bullion standard where a note represents some defined amount of gold and can be redeemed for it. The issuer of the currency, usually a central bank, pegs their currency to a fixed weight in pure or fine gold and tells the world that they will exchange one unit of currency for a certain amount of gold stored in their vaults. This is a currency peg, which we discussed earlier, and means they need to have the gold in their vaults in order to remain credible and promise to let people redeem their notes for gold. The amount of gold you have in your vaults is largely irrelevant if you don’t let people redeem their notes.

When a few countries adopt a gold standard, the exchange rates between their respective currencies become effectively pegged. In theory, you can always sell one currency for gold, and then buy a known amount of another ‘gold standard’ currency with it. So the gold peg rates also determine the currency-to-currency exchange rates. Before the First World War, the effective exchange rate between the US dollar and the pound sterling was $4.8665 to £1 because both currencies were on a gold standard. Of course, there are costs and risks involved in the transactions and the storage and transport of the gold, so that is why it is an effective peg with some wiggle room, rather than an absolute peg.

Before we look at an example of a gold standard, let’s clear up some terminology. Gold and silver are measured by weight (or mass, to be pedantic). The units are grains and troy ounces. There are 480 grains to one troy ounce, and twelve troy ounces to one troy pound. In standard terms, this means one troy ounce is 31.10 grams, which is about 10% heavier than one ‘normal’ (or avoirdupois) ounce of 28.35 grams. Old habits die hard—the troy ounce is still the measure used today when pricing gold and other precious metals.

The small golden disk close to the 5 cm marker is a piece of pure gold weighing one troy grain. Source: Wikipedia40

Gold Standards in the USA

Although many countries have attempted to peg their currencies to gold, the USA has had an interesting history. According to Brief History of the Gold Standard in the United States41 published by the Congressional Research Service, the USA went through a number of periods with multiple attempts at pegging the US dollar to gold. They all eventually failed. Let’s look at what happened.

1792–1834—Bimetallic specie standard: Standardised gold coins ($10 eagles, and $2.50 quarter-eagles) and silver coins existed, minted by the government. The definition of one dollar was based on a certain weight of silver or a certain weight of gold which valued the metals in the ratio 15:1. World markets valued gold a little more than implied by the USA’s peg, so gold coins left the USA, leaving the USA mainly using silver coins.

1834–1862—Silver flees the USA: The USA changed their ratio to 16:1 by minting the gold coins with slightly less gold. World markets now value silver a little more than implied by this new ratio. Thus, the silver coins left the USA, leaving the USA mainly using the new, less-goldy gold coins. It is hard to peg things that trade in markets abroad!

1862—Civil War chaos and fiat paper money: The USA government issued notes called ‘greenbacks’. Greenbacks were notes that were declared as legal tender, but were not convertible into gold or silver. This took the USA off any metallic standard and onto fiat paper money. The dollar lost value in the marketplace, and people preferred to hold 23.22 grains of gold more than one dollar.

1879–1933—A true gold standard: A dollar was re-defined in terms of the pre-war weight of gold (but not silver) at $20.67 per troy ounce. The treasury issued gold coins and convertible (redeemable) gold notes, and greenbacks were once again redeemable in gold. The Federal Reserve System was created in 1913.

Allow me to digress just for a bit of fun. This was a difficult political period that coincided with the birth of populism in the US. Indeed, L. Frank Baum’s book The Wonderful Wizard of Oz is regarded by some as a clever political satire, a parable on populism, and a commentary on monetary policy. References are numerous. Yellow brick road? Gold. Ruby slippers? In the book, they were silver, and a reference to a populist demand for ‘free and unlimited coinage of silver and gold’ at the 16:1 ratio. Scarecrow? Farmers who weren’t as dim as first thought. Tin Man? Industrial workers. Flying monkeys? Plains Indians. The Cowardly Lion? William Jennings Bryan, Nebraska representative in Congress and later the democratic presidential candidate. Emerald City, where the Wizard lives? Washington DC. The Wizard, an old man whose power is achieved through acts of deception? Well, pick any politician in Washington. Now can you guess what ‘Oz’ is a reference to? Yes, the unit for precious metals. These parallels are discussed in more detail by Quentin P. Taylor, Professor of History, Rogers State College in a fascinating essay “Money and Politics in the Land of Oz.”42

1934–1973: The New Deal and the end of the true gold standard. The 1934 Gold Reserve Act devalued the dollar from $20.67 to $35 per troy ounce, and ended convertibility for citizens. ‘The free circulation of gold coins is unnecessary,’ President Franklin Roosevelt told Congress, insisting that the transfer of gold ‘is essential only for the payment of international trade balances’. The Gold Reserve Act outlawed most private possession of gold, forcing individuals to sell it to the treasury. Those found hoarding gold in coin or bullion could be punished by a fine of up to $10,000 and/or jail time. According to Wikipedia43:

A year earlier, in 1933, Executive Order 6102 had made it a criminal offense for U.S. citizens to own or trade gold anywhere in the world, with exceptions for some jewellery and collector’s coins. These prohibitions were relaxed starting in 1964—gold certificates were again allowed for private investors on April 24, 1964, although the obligation to pay the certificate holder on demand in gold specie would not be honored. By 1975 Americans could again freely own and trade gold.

This quasi-gold standard was maintained under the Bretton Woods international monetary agreement of 1944. The Bretton Woods agreement is explained in greater detail later.

1971: The Nixon administration stopped freely converting dollars at their official exchange rate of $35 per troy ounce. This effectively ended the Bretton Woods agreement.

1972: The dollar was devalued from $35 to $38 per troy ounce.

1973: The dollar was devalued from $38 to $42.22 per troy ounce.

1974: President Gerald Ford permitted private gold ownership again in the USA.

1976: The gold standard was abandoned in the USA: The US dollar became pure fiat money.

So people talk about the gold standard, but let’s be realistic: It is not really a gold standard if (a) people can’t redeem their dollars for gold, and (b) you keep changing the rate. It turns out that implementing a gold standard is difficult, even if you can put people in prison for owning gold!

Fiat Currency and Intrinsic Value

‘Yes, but Bitcoin has no intrinsic value,’ is a comment I hear a lot from people trying to understand why Bitcoin has a price. However, it is not a very good argument against Bitcoin. Fiat currencies—USD, GBP, EUR, etc—have no intrinsic value either. In fact, fiat currencies are defined by not having intrinsic value.

That is worth repeating. Fiat currency has no intrinsic value.

But that is ok! On the European Central Bank’s (ECB) website44 you can read:

Euro banknotes and coins are money but so is the balance on a bank account. What actually is money? How is it created and what is the ECB’s role?

The changing essence of money

The nature of money has evolved over time. Early money was usually commodity money—an object made of something that had a market value, such as a gold coin. Later on, representative money consisted of banknotes that could be swapped against a certain amount of gold or silver. Modern economies, including the Euro area, are based on fiat money. This is money that is declared legal tender and issued by a central bank but, unlike representative money, cannot be converted into, for example, a fixed weight of gold. It has no intrinsic value—the paper used for banknotes is in principle worthless—yet is still accepted in exchange for goods and services because people trust the central bank to keep the value of money stable over time. If central banks were to fail in this endeavour, fiat money would lose its general acceptability as a medium of exchange and its attractiveness as a store of value.

The St Louis Fed, in episode nine of a podcast series called Functions of Money—The Economic Lowdown Podcast Series, says:

Fiat money is money that does not have intrinsic value and does not represent an asset in a vault somewhere. Its value comes from being declared ‘legal tender’—an acceptable form of payment—by the government of the issuing country.

So next time someone brings up intrinsic value, try to be patient and explain that intrinsic value doesn’t really matter. What matters is if there is utility in the asset. How useful is it? Well, fiat currency is useful, at the very least because it is the settlement instrument with which you pay your taxes to the state, and more broadly because it is legal tender and must be accepted by merchants.

If you don’t pay your taxes you go to prison, or worse. So some people argue that fiat currency is backed by the threat of state violence. Other people say that fiat currency is backed by the trust and confidence in state institutions—which is a little bit vague, don’t you think? But at least it sort of makes sense, unlike the cryptocurrency favourite: ‘Bitcoin is backed by math’—which is entirely nonsensical. Although at first it sounds kind of profound, don’t stop to think about what that means. Mathematics is used to determine which transactions are valid or not, and is used to control the speed at which bitcoins are created, but this is not a ‘backing’ in the sense that a bond is backed by the issuing company, or a US dollar is backed by the assets on the Federal Reserve’s balance sheet, or a startup is backed by a venture capitalist.

Legal Tender

When a currency is declared legal tender, it means that by statute (law), people must accept it as a settlement mechanism to meet a financial obligation, and that you can pay your tax bills with it45.

Not all notes and coins are legal tender in all circumstances. Currencies are, in general, not legal tender outside of their home jurisdiction. For example, someone in the UK can refuse to accept Russian roubles as repayment of a debt. This doesn’t stop a recipient accepting roubles if they want; it just stops someone being able to force a recipient to accept them.

Also, in many countries you can’t force a recipient to accept payment in an antisocial amount of loose change: there are specific rules as to what counts as legal tender. In Singapore, according to the 2002 Currency Act46, you can’t force someone to accept more than $2 in any combination of 5c, 10c, 20c coins, and you can’t force someone to accept more than $10 in 50c coins. Currently there are no limits for payment in one dollar coins, but after a series of high profile incidents in 2014 where people and merchants made payments in large amounts of loose change47, the Currency Act is being reconsidered to a more memorable uniform legal tender limit of ten coins per denomination, across all denominations, per transaction. This means that a payer would legally be able to use up to ten pieces each of 5-cent, 10c, 20c, 50c, and one dollar coins, but no more, per transaction.

Also in Singapore, under the 1967 Currency Interchangeability Agreement, the Brunei dollar is acceptable as ‘customary tender’ on a 1:1 basis. You can pay for a coffee in Singapore by handing over the same amount in Brunei dollars. Banks in each country will accept the other currency at par48.

Zimbabwe uses USD as the main currency for pricing goods and for government transactions, but lists the following currencies as legal tender: Euro, United States dollar, Pound sterling, South African rand, Botswana pula, Australian dollar, Chinese yuan, and Japanese yen. Its own currency, the Zimbabwe dollar, is not on that list. There are also multiple versions of the Zimbabwe dollar (with different pricing) and the country is a fascinating case study for how not to do currency. It is a mess for shopkeepers, but a delight for monetary economists!

A currency peg is when someone in charge declares that one currency is worth a fixed amount of another currency and then attempts to maintain that exchange rate by matching the supply of either currency with the demand. If people think that you have got your peg wrong, a black market can emerge where people trade the currencies at what they perceive to be a more accurate exchange rate.

How do you maintain a peg? Firstly, you threaten. You announce the pegged rate, and then declare penalties for people found deviating from it. This may mean fines, prison, or perhaps something worse. But you also need to be credible and try to prevent black markets from emerging. Credibility comes from having enough of both currencies to match whatever a trader might want to exchange.

For example, let’s say you are the king of a country and you declare a peg of one apple = one orange. If one year for whatever reason people really want apples, the demand for apples will exceed the demand for oranges. So people might be prepared to pay two oranges for one apple. But you’ve declared a peg, so everyone will come to you with the oranges that they don’t want and demand one apple for each orange they bring you. So to keep the peg, you better have a lot of apples to give out. If you don’t have them, then a black market will emerge that excludes you, and people will start trading one apple for more than one orange, making a mockery of your peg. So you need to have at least as many apples in reserve as there are oranges in circulation.

And vice versa. If, on the other hand, people really want oranges, you’re going to need a lot of oranges to hand out, and you’ll be receiving apples (which no one wants) in return.

So to maintain a peg to the very end, you need as many apples in reserve as there are oranges in circulation, and you need as many oranges in reserve as there are apples in circulation. Or in the fiat world, you need to back your fiat currency 100% with the currency you are pegging to, at the peg rate—an arrangement known as a ‘currency board’.

While central banks can prevent their currencies from going up in value by creating as much fiat currency as they want and therefore capping the value of their currency, it is harder for them to prevent their currencies from going down in value, because they need other currencies with which to buy their own currency back in order to prop its price up.

This is essentially how George Soros broke the Bank of England: He had more ammo than the Bank.

George Soros and the Bank of England

Rohin Dhar details the story on priceonomics.com49: in October 1990, the Bank of England joined the European Exchange Rate Mechanism (ERM) and committed to keep the exchange rate of Deutsche marks and pounds sterling to between 2.78 and 3.13 marks per pound. By 1992, it had become obvious to the market that sterling was valued too highly, even at the floor of 2.78 marks per pound, and the real price of sterling should have been lower.

In the months leading up to September 1992, Soros, via his Quantum hedge fund, borrowed pounds from anyone he could, and sold them to anyone who would buy them. Borrowing something to sell it with an intention to buy it back later as a lower price is known as ‘going short’. According to an article in The Atlantic50, Soros built up a short position of $1.5bn worth of pounds. On the night of Tuesday, 15 September, the fund accelerated its bet and sold more, extending the fund’s short position from $1.5bn worth to $10bn worth, and pushing the price of sterling lower and lower overnight while the Bank of England was absent from the markets.

The following morning, the Bank of England had to buy sterling in order to prop up the value of the pound and maintain the peg they committed to. But what can the Bank of England buy pounds with? Their reserves—other currencies or borrowed money. The Bank of England announced that they would borrow up to $15bn in order to buy pounds. And Soros was prepared to sell that amount to neutralise the demand created by the Bank of England… it was a game of brinkmanship. So, the Bank bought £1bn of sterling over several batches, and raised short term interest rates by two percentage points to make Soros’ loans expensive (remember, Soros was borrowing sterling in order to sell it, and had to pay interest on the pounds he was borrowing). But it was too late. The markets didn’t react, and the price of sterling didn’t rise. At 7.30pm that evening the Bank of England was forced to exit from the ERM and let sterling float. Over the next month the price of sterling fell from 2.78 marks to 2.40 marks per pound. That critical Wednesday was known as Black Wednesday, and Soros became known as the man who broke the Bank of England.

Bretton Woods

The Bretton Woods meeting was all about currency pegs. On 1 July 1944, during World War II, delegates from forty-four countries met in Bretton Woods, New Hampshire, USA, for twenty-one days of discussion to normalise commercial and financial relations.

The outcome was a kind of international gold standard agreement where the US dollar was pegged to gold at $35 per troy ounce and other currencies were pegged to the dollar (with 1% wiggle room) and could be redeemed for gold at the US Treasury. The International Monetary Fund was established, as was the International Bank for Reconstruction and Development (IBRD, which would eventually become part of the World Bank). At that time, ordinary Americans were still banned from owning non-jewellery gold.

Prior to this, in 1931 Britain, most of the Commonwealth, except Canada, and many other countries had abandoned the gold standard. Bretton Woods therefore marked a return to some kind of gold standard.

The Bretton Woods Agreement didn’t work very well. Countries frequently devalued their currencies with respect to the dollar and gold. For example, in 1949, Britain devalued the pound by about 30% from $4.30 to $2.80, and many other countries followed suit.

In 1971 the Bretton Woods agreement broke down after the US stopped honouring the convertibility of dollars to gold. This coincided with a big drop in US gold reserves and increase in foreign claims on US dollars.

Quantitative Easing (QE) often comes up in conversations about fiat currencies, and people describe it as ‘printing money,’ but it is not that simple. QE is a euphemism for an issuing authority (generally a central bank) increasing the amount of fiat money in circulation in order to stimulate a flagging economy. So people worry that this additional money ‘dilutes’ the value of existing money, and this makes people worry about the sustainability of the fiat system.

‘Printing money’ is a poor description for QE. Think about it—if the central bank really ‘printed money’ whether physically or digitally, who would it give it to, and how?

So how does QE work? The central bank buys assets, usually bonds, from the private sector (commercial banks, asset managers, hedge funds, etc) in the secondary market. These are bonds that have already been issued and are now traded by financial market participants. Central banks broadly think of the private sector as having a balance of two things: money, and non-money (other financial assets). And central banks can, to some extent, control that balance by buying financial assets from the private sector to add money, or by selling financial assets to the private sector to remove money.

Why bonds? Because we take comfort that our central banks only own safe assets, and bonds are generally regarded as safe—or at least safer than other financial instruments. Their value is also affected by interest rates, something that a central bank has some degree of control over.

Who can central banks buy bonds from? Certainly not you or me directly because we don’t have that kind of relationship with central banks. As we will see in the next section, central banks have financial relationships with certain commercial banks called clearing banks, who have accounts called reserve accounts with the central bank. So central banks buy bonds from clearing banks, and they pay by crediting the banks’ reserve account with new money. Clearing banks can also act as an agent for other bondholders who wish to sell bonds to the central bank through the clearing banks.

Central banks start the QE journey by buying government bonds (US treasuries, etc) because they are considered the least risky bonds. When they run out of those to buy, they then move to more risky bonds, such as those issued by corporations. The problem is that the central bank ends up with a bunch of risky bonds on its balance sheet—and remember that, from a balance sheet perspective, it is the bonds that ‘back’ the currency.

There are two worries with QE:

1.With excessive QE, the value of money will go down as there is more of it sloshing around in the private sector, which is not great for savers, and could also cause price inflation (though we haven’t seen this yet).

2.A central bank owns risky financial assets that could go down in value, damaging the central bank’s balance sheet when the value of the assets it owns falls.

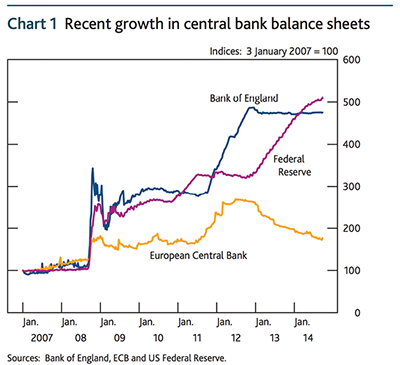

We can see the impact that QE has had on central bank balance sheets since the most recent global financial crisis:

Source: Bank of England51

The history of money is characterised by its failures. Inflation, dilution, debasement, clipping, re-coining, and creation of new tokens worth less and less all appear frequently. The theme with money seems to be that whatever form it takes, it gets watered down either through debasement or by excessive creation until a certain limit, then there is a reform.

The rate of monetary debasement seems to have increased, and the latest experiment in debasing is that of QE. Currency pegs are difficult to manage unless backed 100% with reserves, and although they can be successful for some time, they mostly eventually fail.

Is fiat currency the best solution to money? Will fiat money, backed by the full faith and confidence that people have in today’s governments, continue to survive? Who knows. Some believe that we have some new challengers in the form of cryptocurrencies. The narrative from policymakers has shifted from ignoring cryptocurrencies, to stating that they are not a threat to economic stability, to discussing a potential threat. A chapter in the BIS Annual Economic Report52 published by the Bank of International Settlements in Jun 2018 reads: