THREE GIANT STEPS DOWN WALL STREET

Annual income twenty pounds, annual expenditure nineteen six, result happiness.

Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery.

— Charles Dickens, David Copperfield

THIS CHAPTER OFFERS rules for buying stocks and specific recommendations for the instruments you can use to follow the asset-allocation guidelines presented in chapter 14. By now you have made sensible decisions on taxes, housing, insurance, and getting the most out of your cash reserves. You have reviewed your objectives, your stage in the life cycle, and your attitude toward risk, and you have decided how much of your assets to put into the stock market. Now it is time for a quick prayer at Trinity Church and then some bold steps forward, taking great care to avoid the graveyard on either side. My rules can help you avoid costly mistakes and unnecessary sales charges, as well as increase your yield a mite without undue risk. I can’t offer anything spectacular, but I do know that often even a 1 percent increase in the yield on your assets can mean the difference between misery and happiness.

How do you go about buying stocks? Basically, there are three ways. I call them the No-Brainer Step, the Do-It-Yourself Step, and the Substitute-Player Step.

In the first case, you simply buy shares in various broad-based index funds or indexed ETFs designed to track the different classes of stocks that make up your portfolio. This method also has the virtue of being absolutely simple. Even if you have trouble chewing gum while walking randomly, you can master it. The market, in effect, pulls you along with it. For most investors, especially those who prefer an easy, lower-risk solution to investing, I recommend bowing to the wisdom of the market and using domestic and international index funds for the entire investment portfolio. For all investors, however, I recommend that the core of the investment portfolio—especially the retirement portion—be invested in index funds or ETFs.

Under the second system, you jog down Wall Street, picking your own stocks and perhaps overweighting certain industries or countries. I recommend that your serious money set aside to provide for a comfortable retirement be invested in a diversified portfolio of index funds. But if you would like to take some extra money you can afford to risk and if you enjoy the game of picking stocks, I’ve provided a series of rules to help tilt the odds of success a bit more in your favor.

Third, you can sit on a curb and choose a professional investment manager to do the walking down Wall Street for you. Professional advisers can choose the mix of investments best suited for your capacity and willingness to accept risk and ensure that you have the benefits of broad diversification. Unfortunately, most investment advisers are expensive and they often have conflicts of interest. Fortunately, a new breed of low-cost advisers is now available. These advisers often use automated technologies to manage diversified portfolios of index funds and they charge rock-bottom fees. I will describe these advisers later in the chapter.

Earlier editions of my book described a strategy I called the Malkiel Step: buying closed-end investment company shares at a discount from the value of the shares held by the fund. When the first edition of this book was published, discounts on U.S. stock funds were as high as 40 percent. Discounts are far smaller or nonexistent now, as these funds are more efficiently priced. But attractive discounts can arise, especially on international funds and municipal bond funds, and savvy investors can sometimes take advantage. In the Random Walker’s Address Book, I list a few closed-end funds that sometimes sell at attractive discounts.

THE NO-BRAINER STEP: INVESTING IN INDEX FUNDS

The Standard & Poor’s 500-Stock Index, a composite that represents about three-quarters of the value of all U.S.-traded common stocks, beats most of the experts over the long pull. Buying a portfolio of all companies in this index would be an easy way to own stocks. I argued back in 1973 (in the first edition of this book) that the means to adopt this approach was sorely needed for the small investor:

What we need is a no-load, minimum-management-fee mutual fund that simply buys the hundreds of stocks making up the broad stock-market averages and does no trading from security to security in an attempt to catch the winners. Whenever below-average performance on the part of any mutual fund is noticed, fund spokesmen are quick to point out, “You can’t buy the averages.” It’s time the public could.

Shortly after my book was published, the “index fund” idea caught on. One of the great virtues of capitalism is that when there is a need for a product, someone usually finds the will to produce it. In 1976, a mutual fund was created that allowed the public to get into the act as well. The Vanguard 500 Index Trust purchased the 500 stocks of the S&P 500 in the same proportions as their weight in the index. Each investor shared proportionately in the dividends and in the capital gains and losses of the fund’s portfolio. Today, S&P 500 index funds are available from several mutual-fund complexes with expense ratios below ¹⁄₂₀ of 1 percent of assets or less, much lower than the expenses incurred by actively managed funds. Some index funds are available at zero fees. You can now buy the market conveniently and inexpensively. You can buy exchange-traded 500 index funds from State Street Global Advisors, BlackRock, and Vanguard.

The logic behind this strategy is the logic of the efficient-market hypothesis. But even if markets were not efficient, indexing would still be a very useful investment strategy. Since all the stocks in the market must be owned by someone, it follows that all the investors in the market will earn, on average, the market return. The index fund achieves the market return with minimal expenses. The average actively managed fund incurs an expense ratio of nearly 1 percent per year. Thus, the average actively managed fund must underperform the market as a whole by the amount of the expenses that are deducted from the gross return achieved. This would be true even if the market were not efficient.

The above-average long-run performance of the S&P 500 compared with that of mutual funds and major institutional investors has been confirmed by numerous studies described in previous chapters of this book. Yes, there are exceptions. But you can count on the fingers of your hands the number of mutual funds that have beaten index funds by any significant margin.

The Index-Fund Solution: A Summary

Let’s now summarize the advantages of using index funds as your primary investment vehicle. Index funds have regularly produced rates of return exceeding those of active managers. There are two fundamental reasons for this excess performance: management fees and trading costs. Public index funds and exchange-traded funds are run at fees very close to zero. Actively managed public mutual funds charge annual management expenses close to 1 percentage point per year. Moreover, index funds trade only when necessary, whereas many active funds have a turnover rate close to 100 percent. Using very modest estimates of trading costs, such turnover is undoubtedly an additional drag on performance. Even if stock markets were less than perfectly efficient, active management as a whole could not achieve gross returns exceeding the market. Therefore active managers must, on average, underperform the indexes by the amount of these expense and transactions costs disadvantages. Unfortunately, active managers as a group cannot be like the radio personality Garrison Keillor’s fictional hometown of Lake Wobegon, where “all the children are above average.”

Index funds are also tax-friendly. Index funds allow investors to defer the realization of capital gains or avoid them completely if the shares are later bequeathed. To the extent that the long-run uptrend in stock prices continues, switching from security to security involves realizing capital gains that are subject to tax. Taxes are a crucially important financial consideration because the earlier realization of capital gains will substantially reduce net returns. Index funds do not trade from security to security and, thus, tend to avoid capital gains taxes.

Index funds are also relatively predictable. When you buy an actively managed fund, you can never be sure how it will do relative to its peers. When you buy an index fund, you can be reasonably certain that it will track its index and that it is likely to beat the average manager handily. Moreover, the index fund is always fully invested. You should not believe the active manager who claims that her fund will move into cash at the correct times. We have seen that market timing does not work. Finally, index funds are easier to evaluate. There are now over 5,000 stock mutual funds out there, and there is no reliable way to predict which ones are likely to outperform in the future. With index funds, you know exactly what you are getting, and the investment process is made incredibly simple.

“Leaping tall buildings in a single bound is nice, but can you outperform the S&P 500 Index?”

© 2002 by Thomas Cheney: Reprinted with permission.

Despite all the evidence to the contrary, suppose an investor still believed that superior investment management really does exist. Two issues remain: First, it is clear that such skill is very rare; and second, there appears to be no effective way to find such skill before it has been demonstrated. As I indicated in chapter 7, the best-performing funds in one period of time are not the best performers in the next period. The top performers of one decade are not the best performers in the next. Paul Samuelson summed up the difficulty in the following parable. Suppose it was demonstrated that one out of twenty alcoholics could learn to become a moderate social drinker. The experienced clinician would answer, “Even if true, act as if it were false, for you will never identify that one in twenty, and in the attempt five in twenty will be ruined.” Samuelson concluded that investors should forsake the search for such tiny needles in huge haystacks.

Stock trading among institutional investors is like an isometric exercise: lots of energy is expended, but between one investment manager and another it all balances out, and the trading costs the managers incur detract from performance. Like greyhounds at the dog track, professional money managers seem destined to lose their race with the mechanical rabbit. Small wonder that many institutional investors have put substantial portions of their assets into index funds.

How about you? When you buy an index fund, you give up the chance of boasting at the golf club about the fantastic gains you’ve made by picking stock-market winners. Broad diversification rules out extraordinary losses relative to the whole market. It also, by definition, rules out extraordinary gains. Thus, many Wall Street critics refer to index-fund investing as “guaranteed mediocrity.” But experience shows conclusively that index-fund buyers are likely to obtain results exceeding those of the typical fund manager, whose large advisory fees and substantial portfolio turnover tend to reduce investment yields. Many people will find the guarantee of playing the stock-market game at par every round a very attractive one. Of course, this strategy does not rule out risk: If the market goes down, your portfolio is guaranteed to follow suit.

The index method of investment has other attractions for the small investor. It enables you to obtain very broad diversification with only a small investment. It also allows you to reduce transactions charges. The index fund does all the work of collecting the dividends from all of the stocks it owns and sending you each quarter one check for all of your earnings (earnings that, incidentally, can be reinvested in the fund if you desire). In short, the index fund is a sensible, serviceable method for obtaining the market’s rate of return with absolutely no effort and minimal expense. Moreover, index funds are far more tax efficient than actively-managed funds.

A Broader Definition of Indexing

The indexing strategy is one that I have recommended since the first edition in 1973—even before index funds existed. It was clearly an idea whose time had come. By far the most popular index used is the Standard & Poor’s 500-Stock Index, an index that well represents the major corporations in the U.S. market. But now, although I still recommend indexing, or so-called passive investing, there are valid criticisms of too narrow a definition of indexing. Many people incorrectly equate indexing with a strategy of simply buying the S&P 500 Index. That is no longer the only game in town. The S&P 500 omits the thousands of small companies that are among the most dynamic in the economy. Thus, I believe that if an investor is to buy only one U.S. index fund, the best general U.S. index to emulate is one of the broader indexes such as the Russell 3000, the Wilshire Total Market Index, the CRSP Index, or the MSCI U.S. Broad Market Index—not the S&P 500.

Ninety years of market history confirms that, in the aggregate, smaller stocks have tended to outperform larger ones. Over long periods of history, a portfolio of smaller stocks produced a rate of return of about 12 percent annually, whereas the returns from larger stocks (such as those in the S&P 500) were about 10 percent. Although the smaller stocks were riskier than the major blue chips, the point is that a well-diversified portfolio of small companies is likely to produce enhanced returns. For this reason, I favor investing in an index that contains a much broader representation of U.S. companies, including large numbers of the small dynamic companies that are likely to be in early stages of their growth cycles.

Recall that the S&P 500 represents 75 to 80 percent of the market value of all outstanding U.S. common stocks. Literally thousands of companies represent the remaining 20 to 25 percent of the total U.S. market value. These are in many cases the emerging growth companies that offer higher investment rewards (as well as higher risks). The CRSP U.S. Total Stock Market Index contains all publicly traded U.S. common stocks. The Russell 3000 and MSCI Index contain all but the smallest (and much less liquid) stocks in the market. A number of funds are now based on these broader indexes and go by the name Total Stock Market Portfolio. Total stock market index funds have consistently provided higher returns than the average equity mutual-fund manager.

Moreover, unlike charity, indexing need not begin (and end) at home. As I argued in chapter 8, investors can reduce risk by diversifying internationally, by including asset classes such as real estate in the portfolio, and by placing some portion of their portfolio in bonds and bondlike securities, including Treasury inflation-protected securities. This is the basic lesson of modern portfolio theory. Thus, investors should not buy a U.S. stock-market index fund and hold no other securities. But this is not an argument against indexing because index funds currently exist that mimic the performance of various international indexes such as the Morgan Stanley Capital International (MSCI) index of European, Australasian, and Far Eastern (EAFE) securities, and the MSCI emerging-markets index. In addition, there are index funds holding real estate investment trusts (REITs) as well as corporate and government bonds.

One of the biggest mistakes that investors make is to fail to obtain sufficient international diversification. The United States represents only about one-third of the world economy. To be sure, a U.S. total stock market fund does provide some global diversification because many of the multinational U.S. companies do a great deal of their business abroad. But the emerging markets of the world (such as China and India) have been growing much faster than the developed economies and are expected to continue to do so. Hence, in the recommendations that follow, I suggest that a substantial part of every portfolio be invested in emerging markets.

Emerging markets other than China tend to have younger populations than the developed world. Economies with younger populations tend to grow faster. Moreover, in 2022, they had more attractive valuations than those in the United States. We have pointed out that cyclically adjusted P/E ratios (CAPEs) tend to have predictable power in forecasting longer-run equity returns in developed markets. The relationship also holds in emerging markets. Emerging market CAPEs were less than half the level in the United States in 2022. Future long-run returns have tended to be generous when stocks could be bought at those valuations.

Indexing also is an extremely effective strategy in emerging markets. Even though emerging markets are not likely to be as efficient as developed markets, they are costly to access and to trade. Expense ratios of active funds are far higher than is the case in developed markets. Moreover, liquidity is lower and trading costs are higher. Therefore, after all expenses are accounted for, indexing turns out to be an excellent investment strategy. Standard and Poor’s reported in 2021 that over 92 percent of all actively-managed emerging market equity funds were outperformed by the S&P/IFCI EM index over the preceding 20-year period.

A Specific Index-Fund Portfolio

The table on page 386 presents specific index-fund selections that investors can use to build their portfolios. The table shows the recommended percentages for those in their mid-fifties. Others can use exactly the same selections and simply change the weights to those appropriate for their specific age group. You may want to alter the percentages somewhat depending on your personal capacity for and attitude toward risk. Those willing to accept somewhat more risk in the hope of greater reward could increase the proportion of equities. Those who need a steady income for living expenses could increase their holdings of real estate equities and dividend growth stocks, because they provide somewhat larger current income.

A SPECIFIC INDEX-FUND PORTFOLIO FOR INVESTORS IN THEIR MID-FIFTIES

Cash (5%)* |

|

|

|

Fidelity Government Money Market Fund (SPAXX)or Vanguard Federal Money Market Fund (VMFXX) |

|

Bonds and Bond Substitutes (27½%)† |

||

7½% |

U.S. Vanguard Long-term Corporate Bond Fund ETF (VCLT) or iShares Corporate Bond ETF (LQD) |

|

7½% |

Vanguard Emerging Markets Government Bond Fund (VGAVX) |

|

12½% |

Wisdom Tree Quality Dividend Fund (DGRW) or Vanguard Dividend Growth Fund (VDIGX)† |

|

Real Estate Equities (12½%) |

||

|

Vanguard REIT Index Fund (VGSLX) or Fidelity Real Estate Index Fund (FSRNX) |

|

Stocks (55%) |

||

27% |

U.S. Stocks Schwab Total Stock Market Index Fund (SWTSX) or Vanguard Total Stock Market Index Fund (VTSAX) |

|

14% |

Developed International Markets Schwab International Index Fund (SWISX) or Vanguard Developed Market Index Fund (VTMGX) |

|

14% |

Emerging International Markets Vanguard Emerging Markets Index Fund (VEMBX) or Fidelity Spartan Emerging Markets Index Fund (FPADX) |

|

*A short-term bond fund may be substituted for one of the money-market funds listed.

†Although it doesn’t fit under the rubric of an index-fund portfolio, investors should consider putting part or all of the U.S. bond portfolio in Treasury inflation-protected securities. The U.S. Treasury I Savings Bonds were an excellent choice in 2022. The dividend growth and corporate bond funds are also exceptions since they are not standard index funds.

Remember also that I am assuming here that you hold most, if not all, of your securities in tax-advantaged retirement plans. Certainly all bonds should be held in such accounts. If bonds are held outside of retirement accounts, you may well prefer tax-exempt bonds rather than the taxable securities. Moreover, if your common stocks will be held in taxable accounts, you might consider tax-loss harvesting, covered below. Finally, note that I have given you a choice of index funds from different mutual-fund complexes. Because of my long association with the Vanguard Group, I wanted also to suggest a number of non-Vanguard funds. All the funds listed have moderate expense ratios and are no-load. More information on these funds, including telephone numbers and websites, can be found in the Random Walker’s Address Book, which follows this chapter. ETFs may be used in lieu of mutual funds.

One of the advantages, noted above, of passive portfolio management (that is, simply buying and holding an index fund) is that such a strategy minimizes transactions costs as well as taxes. Taxes are a crucially important financial consideration, as two Stanford University economists, Joel Dickson and John Shoven, have shown. Utilizing a sample of sixty-two mutual funds with long-term records, they found that, pre-tax, $1 invested in 1962 would have grown to $21.89 in 1992. After paying taxes on income dividends and capital gains distributions, however, that same $1 invested in mutual funds by a high-income investor would have grown to only $9.87.

To a considerable extent, index mutual funds help solve the tax problem. Because they do not trade from security to security, they tend to avoid capital gains taxes. Nevertheless, even index funds can realize some capital gains that are taxable to the holders. These gains generally arise involuntarily, either because of a buyout of one of the companies in the index, or because sales are forced on the mutual fund. The latter occurs when mutual-fund shareholders decide on balance to redeem their shares and the fund must sell securities to raise cash. Thus, even regular index funds are not a perfect solution for the problem of minimizing tax liabilities.

Exchange-traded index funds (ETFs) such as “spiders” (an S&P 500 Fund) and “vipers” (a total stock market fund) can be more tax-efficient than regular index funds because they are able to make “in-kind” redemptions. In-kind redemptions proceed by delivering low-cost shares against redemption requests. This is not a taxable transaction for the fund, so there is no realization of gain that must be distributed. Moreover, the redeeming ETF shareholder pays taxes based on his or her original cost of the shares—not the fund’s basis in the basket of stocks that is delivered. ETFs also have rock-bottom expenses. A wide variety of ETFs are available not only for U.S. stocks but for international ones as well. ETFs are an excellent vehicle for the investment of lump sums that are to be allocated to index funds.

ETFs may involve transactions costs, however, including possible brokerage fees* and bid-asked spreads. No-load index mutual funds may better serve investors who will be accumulating index shares over time in small amounts. Avoid the temptation to buy or sell ETFs at any hour of the day. I agree with John Bogle, founder of the Vanguard Group: “Investors cut their own throats when they trade ETFs.” If you are tempted, follow the practice of Little Miss Muffet and run far away from the spiders and their siblings.

In the table on page 389, I list the ETFs that can be used to build your portfolio. Note that for investors who want to make their stock buying as easy as possible, there are total world index funds and ETFs that provide total international diversification with one-stop shopping.

If you want an easy, time-tested method to achieve superior investment results, you can stop reading here. The indexed mutual funds or ETFs that I have listed will provide broad diversification, tax efficiency, and low expenses. Even if you want to buy individual stocks or funds that concentrate on different sectors of the market, do what institutional investors are increasingly doing: Index the core of your portfolio along the lines suggested and then take active bets with extra funds. With a strong core of index funds, you can take these bets with much less risk than if the whole portfolio were actively managed. And even if you make some errors, they won’t prove fatal.

EXCHANGE TRADED FUNDS (ETFS)

|

Ticker |

Expense Ratio |

Total U.S. Stock Market |

|

|

Vanguard Total Stock Market |

VTI |

0.03% |

SPDR Total Stock Market |

SPTM |

0.03% |

Developed Markets (EAFE) |

|

|

Vanguard Europe Pacific |

VEA |

0.03% |

iShares Core MSCI Intl Developed Markets |

IDEV |

0.07% |

SPDR Developed World ex-US |

SPDW |

0.04% |

Emerging Markets |

|

|

Vanguard Emerging Markets |

VWO |

0.10% |

SPDR Emerging Markets |

SPEM |

0.11% |

iShares Core MSCI Emerging Markets |

IEMG |

0.11% |

Total World Ex-U.S. |

|

|

Vanguard FTSE All World ex-US |

VEU |

0.08% |

SPDR MSCI ACWI ex-US |

CWI |

0.30% |

iShares Core MSCI Total International Stock |

IXUS |

0.09% |

Total World Including U.S. |

|

|

Vanguard Total World |

VT |

0.04% |

iShares MSCI ACWI |

ACWI |

0.32% |

Bond Market U.S.* |

|

|

Vanguard Total Corporate Bond Fund |

VTC |

0.03% |

iShares Investment Grade Corporate Bond |

LQD |

0.14% |

Schwab US Aggregate Bond |

SCHZ |

0.04% |

*Taxable investors should consider the closed-end municipal bond funds listed on page 419.

THE DO-IT-YOURSELF STEP: POTENTIALLY USEFUL STOCK-PICKING RULES

Indexing is the strategy I recommend for individuals and institutions for their serious investment money such as retirement savings. I do recognize, however, that indexing the entire portfolio may be considered by many to be a very dull strategy. And if you do have some extra money you can afford to put at risk, you might want to use your own steps (and wits) to pick winners. For those who insist on playing the game themselves, the Do-It-Yourself Step may be appealing.

Having been smitten with the gambling urge since childhood, I can well understand why many investors have a compulsion to try to pick the big winners on their own and a total lack of interest in a system that promises results merely equivalent to those in the market as a whole. The problem is that it takes a lot of work to do it yourself, and consistent winners are very rare. For those who regard investing as play, however, here is a sensible strategy that, at the very least, minimizes your risk.

Before putting my strategy to work, however, you need to know the sources of investment information. Most information sources can be obtained at public libraries. You should be an avid reader of the financial pages of daily newspapers, particularly the New York Times and the Wall Street Journal. Weeklies such as Barron’s should be on your “must-read” list as well. Business magazines such as Bloomberg Businessweek, Fortune, and Forbes are also valuable for gaining exposure to investment ideas. The major investment advisory services are good, too. You should, for example, try to have access to Standard & Poor’s Outlook, the Value Line Investment Survey, and Morningstar. Finally, a wealth of information, including security analysts’ recommendations, is available on the Internet.

In the first edition of A Random Walk Down Wall Street, fifty years ago, I proposed four rules for successful stock selection. I find them just as serviceable today. In abridged form, the rules, some of which have been mentioned in earlier chapters, are as follows:

Rule 1: Confine stock purchases to companies that appear able to sustain above-average earnings growth for at least five years. Difficult as the job may be, picking stocks whose earnings grow is the name of the game. Consistent growth not only increases the earnings and dividends of the company but may also increase the multiple that the market is willing to pay for those earnings. Thus, the purchaser of a stock whose earnings begin to grow rapidly has a potential double benefit—both the earnings and the multiple may increase.

Rule 2: Never pay more for a stock than can reasonably be justified by a firm foundation of value. Although I am convinced that you can never judge the exact intrinsic value of a stock, I do feel that you can roughly gauge when a stock seems to be reasonably priced. The market price-earnings multiple is a good place to start: Buy stocks selling at multiples in line with, or not very much above, this ratio. Look for growth situations that the market has not already recognized by bidding the stock’s multiple to a large premium. If the growth actually takes place, you will often get a double bonus—both the earnings and the price-earnings multiple can rise. Beware of stocks with very high multiples and many years of growth already discounted in their prices. If earnings decline rather than grow, you can get double trouble—the multiple will drop along with the earnings. Following this rule would have avoided the heavy losses suffered by investors in the premier high-tech growth stocks that sold at astronomical price-earnings multiples in early 2000.

Note that, although similar, this is not simply another endorsement of the “buy low P/E stocks” strategy. Under my rule it is perfectly all right to buy a stock with a P/E multiple slightly above the market average—as long as the company’s growth prospects are substantially above average. You might call this an adjusted low P/E strategy. Some people call this a GARP (Growth At A Reasonable Price) strategy. Buy stocks whose P/Es are low relative to their growth prospects. If you can be even reasonably accurate in picking companies that do indeed enjoy above-average growth, you will be rewarded with above-average returns.

Rule 3: It helps to buy stocks with the kinds of stories of anticipated growth on which investors can build castles in the air. I stressed in chapter 2 the importance of psychological elements in stock-price determination. Individual and institutional investors are not computers that calculate warranted price-earnings multiples and then print out buy and sell decisions. They are emotional human beings—driven by greed, gambling instinct, hope, and fear in their stock-market decisions. This is why successful investing demands both intellectual and psychological acuteness. Of course, the market is not totally subjective either; if a positive growth rate appears to be established, the stock is almost certain to develop some type of following. But stocks are like people—some have more attractive personalities than others, and the improvement in a stock’s multiple may be smaller if its story never catches on. The key to success is being where other investors will be, several months before they get there. So ask yourself whether the story about your stock is one that is likely to catch the fancy of the crowd. Can the story generate contagious dreams? Is it a story on which investors can build castles in the air—but castles in the air that really rest on a firm foundation?

Rule 4: Trade as little as possible. I agree with the Wall Street maxim “Ride the winners and sell the losers,” but not because I believe in technical analysis. Frequent switching accomplishes nothing but increasing your tax burden when you do realize gains. I do not say, “Never sell a stock on which you have a gain.” The circumstances that led you to buy the stock may change, and, especially when it gets to be tulip time in the market, many of your successful growth stocks may become overweighted in your portfolio, as they did during the Internet bubble of 1999–2000. But it is very difficult to recognize the proper time to sell, and heavy tax costs may be involved. My own philosophy leads me to minimize trading as much as possible. I am merciless with the losers, however. With few exceptions, I sell before the end of each calendar year any stocks on which I have a loss. The reason for this timing is that losses are deductible (up to certain amounts) for tax purposes, or can offset gains you may already have taken. Thus, taking losses can lower your tax bill. I might hold a losing position if the growth I expect begins to materialize and I am convinced that my stock will eventually work out. But I do not recommend too much patience in losing situations, especially when prompt action can produce immediate tax benefits.

The efficient-market theory warns that following even sensible rules such as these is unlikely to lead to superior performance. Nonprofessional investors labor under many handicaps. Earnings reports cannot always be trusted. And once a story is out in the regular press, it’s likely that the market has already taken account of the information. Picking individual stocks is like breeding thoroughbred porcupines. You study and study and make up your mind, and then proceed very carefully. In the final analysis, much as I hope that investors have achieved successful records following my good advice, I am well aware that the winners in the stock-picking game may have benefited mainly from Lady Luck.

For all its hazards, picking individual stocks is a fascinating game. My rules do, I believe, tilt the odds in your favor while protecting you from the excessive risk involved in high-multiple stocks or stocks with no earnings at all. But if you choose this course, remember that a large number of other investors—including the pros—are trying to play the same game. And the odds of anyone’s consistently beating the market are pretty slim. Nevertheless, for many of us, trying to outguess the market is a game that is much too much fun to give up. Even if you were convinced you would not do any better than average, I’m sure that most of you with speculative temperaments would still want to keep on playing the game with at least some portion of your money. My rules permit you to do so in a way that significantly limits your exposure to risk.

If you do want to pick stocks yourself, I strongly suggest a mixed strategy: Index the core of your portfolio, and try the stock-picking game for the money you can afford to put at somewhat greater risk. If the main part of your retirement funds is broadly indexed and your stocks are diversified with bonds and real estate, you can safely take a flyer on some individual stocks, knowing that your basic nest egg is reasonably secure.

THE SUBSTITUTE-PLAYER STEP: HIRING APROFESSIONAL WALL STREET WALKER

There’s an easier way to gamble in your investment walk: Instead of trying to pick the individual winners (stocks), pick the best coaches (investment managers). These “coaches” come in the form of active mutual-fund managers, and there are thousands of them for you to pick from.

In previous editions of this book, I provided the names of several investment managers who had enjoyed long-term records of successful portfolio management as well as brief biographies explaining their investment styles. These managers were among the very few who had shown an ability to beat the market over long periods of time. I have abandoned that practice in the current edition for two reasons.

First, with the exception of Warren Buffett, those managers have now retired from active portfolio management, and Buffett himself was well into his nineties in 2022. Even Buffett trailed the S&P 500 index in the ten years to 2022, and he is now a strong supporter of indexing. Second, I have become increasingly convinced that the past records of mutual-fund managers are essentially worthless in predicting future success. The few examples of consistently superior performance occur no more frequently than can be expected by chance.

I have studied the persistence of mutual-fund performance over more than fifty years and conclude that it is simply impossible for investors to guarantee themselves above-average returns by purchasing those funds with the best recent records. I have tested a strategy whereby at the start of each year investors would rank all general equity funds on the basis of the funds’ records over the past twelve months, five years, or ten years and assumed that the investor buys the top ten funds, the top twenty funds, and so on. There is no way to beat the market consistently by purchasing the mutual funds that have performed best in the past.

I also tested a strategy of purchasing the “best” funds as ranked by the leading financial magazines or advisory services. The clear implication of these tests in the laboratory of fund performance, as well as the academic work reported in Part Two of this book, is that you cannot depend on an excellent record continuing persistently in the future. Indeed, it is more often the case that the hot performers of one period are the dogs of the next.

Is there any way to select an actively managed fund that is likely to be an above-average performer? I have undertaken many studies of mutual-fund returns over the years in an attempt to explain why some funds perform better than others. As indicated earlier, past performance is not helpful in predicting future returns. The two variables that do the best job in predicting future performance are expense ratios and turnover. High expenses and high turnover depress returns—especially after-tax returns if the funds are held in taxable accounts. The best-performing actively managed funds have moderate expense ratios and low turnover. The lower the expenses charged by the purveyor of the investment service, the more there will be for the investor. As Jack Bogle, the founder of the Vanguard Group, used to say, in the mutual fund business, “you get what you don’t pay for.”

INVESTMENT ADVISERS, STANDARD AND AUTOMATED

If you follow the recommendations in this book carefully, you really don’t need an investment adviser. Unless you have a variety of tax complications or legal issues, you should be able to accomplish the diversification required and do the rebalancing yourself. You might even find that it is fun to be able to take complete charge of your investment program.

The problem with investment advisers is that they tend to be quite expensive and are often conflicted. Many investment advisers will charge you 1 percent of your assets per year or more for the service of establishing an account with an appropriately diversified portfolio. PriceMetrix, Inc. calculated the industry average at just over 1 percent. But most advisers have a minimum annual fee of at least $1,000 to $1,500. That means that small investors are effectively shut out of the market for investment advice, or that they will have to pay a far greater percentage of their investment portfolio than 1 percentage point. In addition, some advisers may be conflicted and will use investment instruments on which they earn an additional commission. As a result, investors are too often steered to expensive, actively-managed portfolios instead of low-cost index funds. If you feel you must get an investment adviser, make sure that adviser is a “fee only” adviser. These advisers do not get paid for distributing investment products and thus are more likely to make decisions that are completely in your interest rather than in their interest.

Fully automated investment services not only provide automated investment advice but also rely solely on the Internet to acquire clients and to establish their accounts. There are no face-to-face meetings. Deposits, withdrawals, transfers, reporting (and of course the investment management itself) are handled electronically via a web or mobile device. At the outset I must make clear my potential conflict of interest. I serve as chief investment officer of Wealthfront, a fully automated investment advisory firm. I also serve on the investment committee of Rebalance, an advisory firm that allows for some telephone contact with a human adviser.

The automated service tailors diversified portfolios allocated among several asset classes, appropriate to the needs of individual clients. By simplifying the channel through which investment management is offered, the automated investment services are able to drastically reduce fees, such as one quarter of 1 percent (25 basis points) even for small accounts as low as $500. Millennials and GenZers are especially attracted to such services. They are used to subscribing to all their services electronically. Many young people perceive having to talk to an adviser as a negative. They tend to define service in terms of convenience rather than interaction.

The process starts with an online interview. The client is asked about his or her salary, tax situation, assets, and indebtedness, if any. The client is asked to provide information on investment objectives as well as to answer a number of questions to assess capacity for risk and temperamental willingness to assume market volatility. The adviser is told if the investment fund is devoted to retirement savings or if there is some specified purpose for the fund, such as accumulating the down payment on a home or providing a safety net in case of illness. The less consistent are the client’s answers to the attitudinal questions, the less risk tolerant the individual is likely to be. The overall risk matrix combines both objective and subjective scores and overweights the component that is more risk averse. This approach tends to offset the tendency for individuals (particularly males) to overstate their true risk tolerances.

The client is encouraged to link any other banking, retirement, and investment accounts to the automated service. This allows the automated service to provide advice that is consistent with the individual’s total financial situation. Linking all of a client’s financial accounts will also allow the automated adviser to provide financial planning as well as targeted investment management services. The automated service is able to advise the client on the amount of the savings over time that is likely to be necessary to meet the individual’s retirement goals. Collection of inputs into financial planning programs is all done electronically.

Data from one’s financial accounts and past investing behavior are more likely to reflect a person’s actual spending practices and attitudes toward risk and be far more accurate than what one might tell a traditional financial adviser. From all this information, the automated service assigns a risk score that is used to select an optimal portfolio from the efficient opportunity set of possible portfolios. Modern portfolio theory, as described in chapter 8, is used to choose the optimal mix of investments.

There are several aspects of investment management that an automated adviser can do more efficiently than a traditional face-to-face adviser. Most automated portfolios are made up almost exclusively of index funds. Only the lowest cost index funds are used, and they are accessed through ETFs. Automated advisers can set up programs to ensure that the client’s portfolio is automatically rebalanced to keep the risk levels of the holdings consistent with the client’s preference. Rebalancing can often be accomplished by investing dividends or by allocating new deposits of cash into the asset classes that have become underweighted. An automated procedure can easily determine when rebalancing is desirable and how it should be implemented.

The index funds used by automated advisers are already tax efficient since the funds are passive and do not realize capital gains as do active managers. Tax-loss harvesting (TLH) can add significantly to the after-tax return of the investor. While traditional advisers offer this service to wealthy investors, automated advisers, by monitoring portfolios continuously, can harvest losses far more efficiently and can make the technique available to a far larger clientele.

TLH is the crown jewel of tax management. It involves selling an investment that is trading at a loss and replacing it with a highly correlated but not identical investment. Doing so allows you to maintain the risk and return characteristics of your portfolio while generating losses that can be used to reduce your current taxes.

While tax-loss harvesting only defers your taxes, the tax savings generated can be reinvested and compounded over time. As a result, you are better off paying taxes later rather than sooner. In addition, the long-term capital gain tax rate you pay on your decreased basis will be lower than the tax rate from which you benefited from harvesting a short-term capital loss. Moreover, if the portfolio is held for a future bequest to one’s heirs or is used for a charitable contribution, the tax can be avoided permanently under current tax laws.

Tax-loss harvesting does entail switching from security to security in order to realize tax losses. But the strategy is entirely consistent with traditional indexing. In the following example, I will use the S&P 500 as a market proxy. (The same strategy can be used for a total stock-market proxy such as the Russell 3000 Index.) We can replicate the behavior of the S&P 500 by holding a sample of 250 stocks. These stocks are chosen to replicate the industry and size composition of the index while minimizing tracking error between the sample and the overall index.

Now suppose large pharmaceutical stocks have declined in value. You might sell Merck to realize a loss and buy Pfizer to enable you to continue to track the index. Or if the autos declined you could sell Ford and buy General Motors. Automating the process, one can continuously look for losses to realize. It has been shown that tax-loss harvesting can add a meaningful amount to the annual after-tax return of the investor.

The losses generated from selling positions with unrealized losses can offset any gains realized in the other parts of the portfolio. Suppose, for example, that an investor had realized gains from a real estate transaction such as selling a house. Or perhaps gains had been realized from an actively managed mutual fund or a multifactor smart beta fund described in chapter 11. Tax-loss harvesting enables an investor to avoid the tax that would have been required, and net tax losses up to $3,000 can be deducted from income. The technique is perfectly compatible with broad-based indexing and can provide dependable benefits for investors. Software is uniquely suited to maximize the benefits of TLH. By monitoring portfolios 24/7, the automated adviser can take advantage of temporary dips in the market.†

In addition to fully automated services, there are hybrid services that use technology to assist in some functions but also allow some limited individual contact with a human adviser. Vanguard Personal Advisory Services provides portfolio management services using both low-cost indexed investments and funds managed by Vanguard. Vanguard gives clients the ability to speak directly with an adviser either by phone or by video chat. The human touch comes with a price as this service charges investors an annual management fee of 30 basis points (30/100 of 1 percent) and the minimum investment requirement ($50,000) tends to be higher than the fully automated services.

Rebalance specializes in tax-advantaged retirement portfolios. They are the least automated of all the portfolio services (portfolios are selected by an investment committee). They stress the advantage of having a dedicated adviser who is always available by telephone. The annual fee is 50 basis points, which is still lower than the typical fee charged by traditional face-to-face advisers.

Charles Schwab, the leading discount broker, has introduced its own portfolio service called Schwab Intelligent Portfolios. Schwab requires a $5,000 minimum investment and selects and rebalances portfolios consistent with the investor’s age and goals. While no explicit fee is charged for the service, the portfolios may contain Schwab-sponsored funds with expense ratios that are generally higher than the ratios of simple capitalization-weighted index funds. Moreover, the investor is required to hold a substantial portion of the portfolio in cash. While Schwab describes its service as “automated,” the selected portfolios are unlikely to be consistent with those resulting from an automated optimized program.

SOME LAST REFLECTIONS ON OUR WALK

We are now at the end of our walk. Let’s look back for a moment and see where we have been. It is clear that the ability to beat the averages consistently is extremely rare. Neither fundamental analysis of a stock’s firm foundation of value nor technical analysis of the market’s propensity for building castles in the air can produce reliably superior results. Even the pros must hide their heads in shame when they compare their results with those obtained by the dartboard method of picking stocks.

Sensible investment policies for individuals must then be developed in two steps. First, it is crucially important to understand the risk-return trade-offs that are available and to tailor your choice of securities to your temperament and requirements. Part Four provided a careful guide for this part of the walk, including a number of warm-up exercises concerning everything from tax planning to the management of reserve funds and a life-cycle guide to portfolio allocations. This chapter has covered the major part of our walk down Wall Street—three important steps for buying common stocks. I began by suggesting sensible strategies that are consistent with the existence of reasonably efficient markets. The indexing strategy is the one I recommend most highly. At least the core of every investment portfolio ought to be indexed. I recognize, however, that telling most investors that there is no hope of beating the averages is like telling a six-year-old that there is no Santa Claus. It takes the zing out of life.

For those of you incurably smitten with the speculative bug, who insist on picking individual stocks in an attempt to beat the market, I offered four rules. The odds are really stacked against you, but you may just get lucky and win big. I also am very skeptical that you can find investment managers who have some talent for finding those rare $100 bills lying around in the marketplace. Never forget that past records are far from reliable guides to future performance.

Investing is a bit like lovemaking. Ultimately, it is really an art requiring a certain talent and the presence of a mysterious force called luck. Indeed, luck may be 99 percent responsible for the success of the very few people who have beaten the averages. “Although men flatter themselves with their great actions,” La Rochefoucauld wrote, “they are not so often the result of great design as of chance.”

The game of investing is like lovemaking in another important respect, too. It’s much too much fun to give up. If you have the talent to recognize stocks that have good value, and the art to recognize a story that will catch the fancy of others, it’s a great feeling to see the market vindicate you. Even if you are not so lucky, my rules will help you limit your risks and avoid much of the pain that is sometimes involved in the playing. If you know you will either win or at least not lose too much, and if you index at least the core of your portfolio, you will be able to play the game with more satisfaction. At the very least, I hope this book makes the game all the more enjoyable.

One of the most rewarding features for me in writing thirteen editions of this book has been the many letters I have received from grateful investors. They tell me how much they have benefited from following the simple advice that has remained the same for fifty years. Those timeless lessons involve broad diversification, annual rebalancing, using index funds, and staying the course.

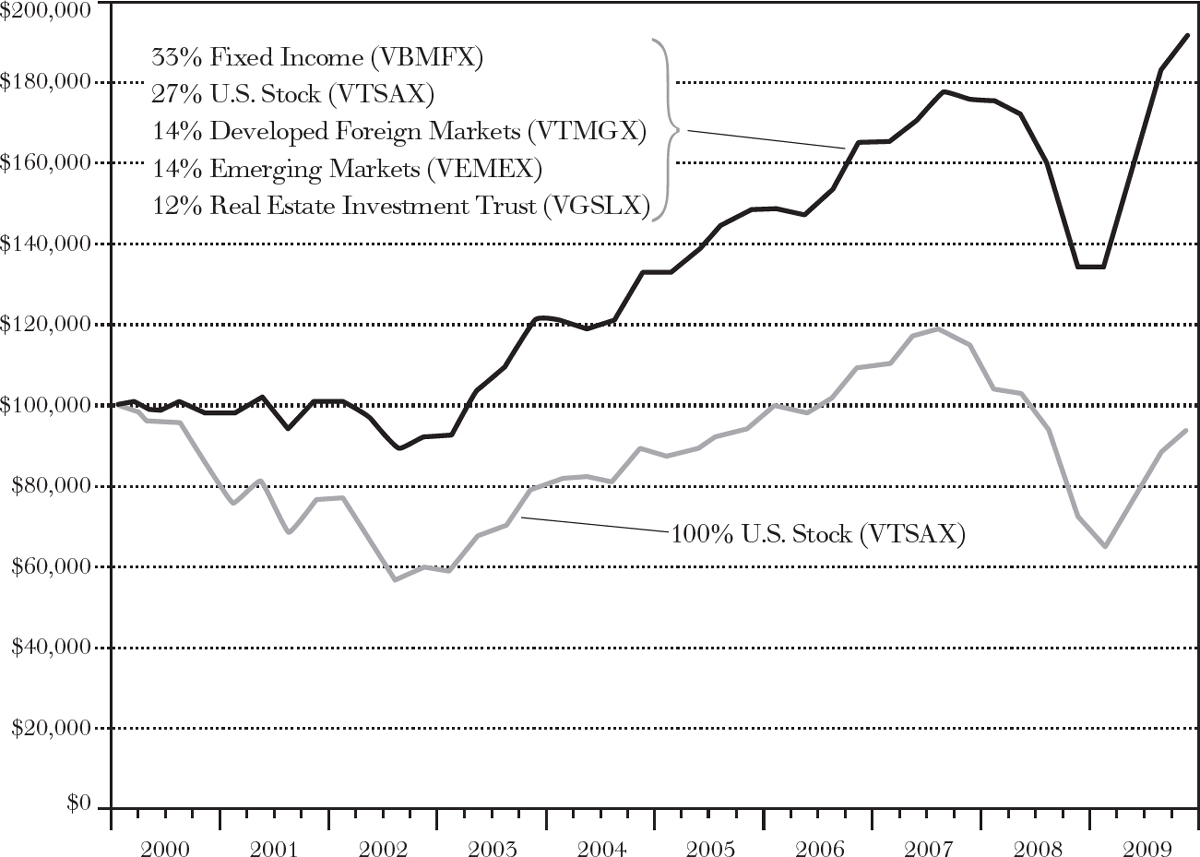

BROADLY DIVERSIFIED PORTFOLIO OF MUTUAL FUNDS (WITH ANNUAL REBALANCING) PRODUCED ACCEPTABLE RETURNS EVEN DURING THE FIRST DECADE OF THE 2000s

Source: Vanguard and Morningstar.

The first decade of the new millennium was one of the most challenging times for investors. Even a broadly diversified total stock market fund devoted solely to U.S. stocks lost money. But even in this horrible decade, following the timeless lessons I have espoused would have produced satisfactory results. The chart above shows that an investment in the VTSAX (the Vanguard Total Stock Market Fund) did not produce positive returns in the “lost” first decade of the 2000s. But suppose an investor diversified her portfolio with the approximate conservative percentages I suggested on page 386 for a mid-fifties investor. The diversified portfolio (annually rebalanced) produced a quite satisfactory return even during one of the worst decades investors have ever experienced. And if the investor also used dollar-cost averaging to add small amounts to the portfolio consistently over time, the results were even better. If you will follow the simple rules and timeless lessons espoused in this book, you are likely to do just fine, even during the toughest of times.

* Many discount brokers offer commission-free trading of ETFs. In such cases, holding ETFs and automatically reinvesting dividends can work as well as investing in mutual funds.

† Even if you don’t use an automated adviser, you could do some tax-loss harvesting yourself. For example, if your MSCI emerging-markets ETF declined in price, you could sell it and buy a Vanguard EM ETF to maintain your exposure. Because the two ETFs use different underlying indexes, the sale does not run afoul of IRS regulations.