A LIFE-CYCLE GUIDE TO INVESTING

There are two times in a man’s life when he should not speculate: when he can’t afford it, and when he can.

—Mark Twain, Following the Equator

INVESTMENT STRATEGY NEEDS to be keyed to one’s life cycle. A thirty-four-year-old and a sixty-eight-year-old saving for retirement should use different financial instruments to accomplish their goals. The thirty-four-year-old—just beginning to enter the peak years of salaried earnings—can use wages to cover any losses from increased risk. The sixty-eight-year-old—likely to depend on investment income to supplement or replace salary income—needs to constrain risk. Even the same financial instrument can mean different things to different people depending on their capacity for risk. Although the thirty-four-year-old and the sixty-eight-year-old may both invest in a certificate of deposit, the younger may do so because of an attitudinal aversion to risk and the older because of a reduced capacity to accept risk. In the first case, one has more choice in how much risk to assume; in the second, one does not.

The most important investment decision you will probably ever make concerns the balancing of asset categories (stocks, bonds, real estate, money-market securities, and so on) at different stages of your life. According to Roger Ibbotson, who has spent a lifetime measuring returns from alternative portfolios, more than 90 percent of an investor’s total return is determined by the asset categories that are selected and their overall proportional representation. Less than 10 percent of investment success is determined by the specific stocks or mutual funds that an individual chooses. In this chapter, I will show you that whatever your aversion to risk—whatever your position on the eat-well, sleep-well scale—your age, income from employment, and specific responsibilities in life go a long way toward helping you determine the mix of assets in your portfolio.

FIVE ASSET-ALLOCATION PRINCIPLES

Before we can determine a rational basis for making asset-allocation decisions, certain principles must be kept firmly in mind. We’ve covered some of them implicitly in earlier chapters, but treating them explicitly here should prove very helpful. The key principles are:

- History shows that risk and return are related.

- The risk of investing in common stocks and bonds depends on the length of time the investments are held. The longer an investor’s holding period, the lower the likely variation in the asset’s return.

- Dollar-cost averaging can be a useful, though controversial, technique to reduce the risk of stock and bond investment.

- Rebalancing can reduce risk and, in some circumstances, increase investment returns.

- You must distinguish between your attitude toward and your capacity for risk. The risks you can afford to take depend on your total financial situation, including the types and sources of your income exclusive of investment income.

1. Risk and Reward Are Related

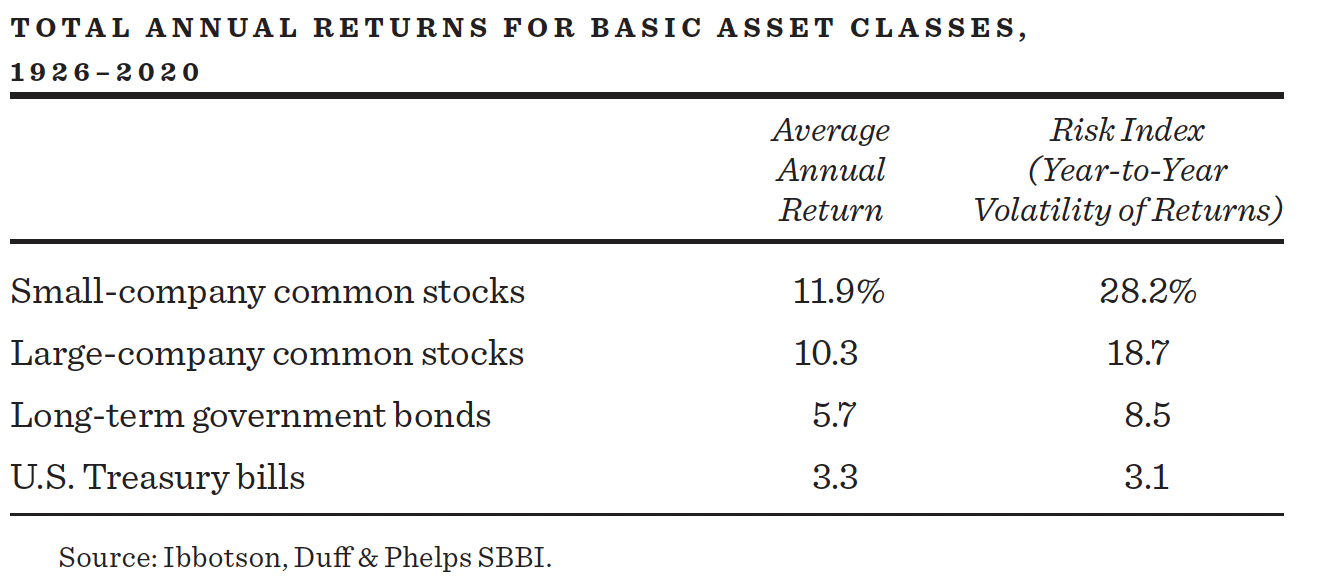

Although you may be tired of hearing that investment rewards can be increased only by the assumption of greater risk, no lesson is more important in investment management. This fundamental law of finance is supported by centuries of historical data. The table below illustrates the point.

Common stocks have clearly provided very generous long-run rates of return. It has been estimated that if George Washington had put just one dollar aside from his first presidential salary and invested it in common stocks, his heirs would have been millionaires more than fifty times over by 2021. Roger Ibbotson estimates that stocks have provided a compounded rate of return of more than 8 percent per year since 1790. (As the table above shows, returns have been even more generous since 1926, when common stocks of large companies earned over 10 percent.) But this return came only at substantial risk to investors. Total returns were negative in about three years out of ten. So as you reach for higher returns, never forget the saying “There ain’t no such thing as a free lunch.” Higher risk is the price one pays for more generous returns.

Your “staying power,” the length of time you hold on to your investment, plays a critical role in the actual risk you assume from any investment decision. Thus, your stage in the life cycle is a critical element in determining the allocation of your assets. Let’s see why the length of your holding period is so important in determining your capacity for risk.

We saw in the preceding table that long-term government bonds have provided an average 5.7 percent annual rate of return over a ninety-year period. The risk index, however, showed that in any single year this rate could stray far from the yearly average. Indeed, in many individual years, it was actually negative. The reason average bond returns were so high in this period was that interest rates were considerably higher during most of the intervening years than they are today. By 2022 the yield on a 30-year U.S. government bond had fallen to 3 percent. But you would be certain to earn that meager 3 percent only if you held the bond for the next 30 years. If you found that you had to sell that bond a year later, your rate of return could be 0 percent, or even a substantial loss if interest rates rose sharply, with existing bond prices falling to adjust to the new higher interest rates. I think you can see why your age and the likelihood that you can stay with your investment program can determine the amount of risk involved in any specific investment program.

What about investing in common stocks? Could it be that the risk of investing in stocks also decreases with the length of time they are held? The answer is a qualified yes. A substantial amount (but not all) of the risk of common-stock investment can be eliminated by adopting a program of long-term ownership, reinvesting dividends, and sticking to it through thick and thin (the buy-and-hold strategy discussed in earlier chapters).

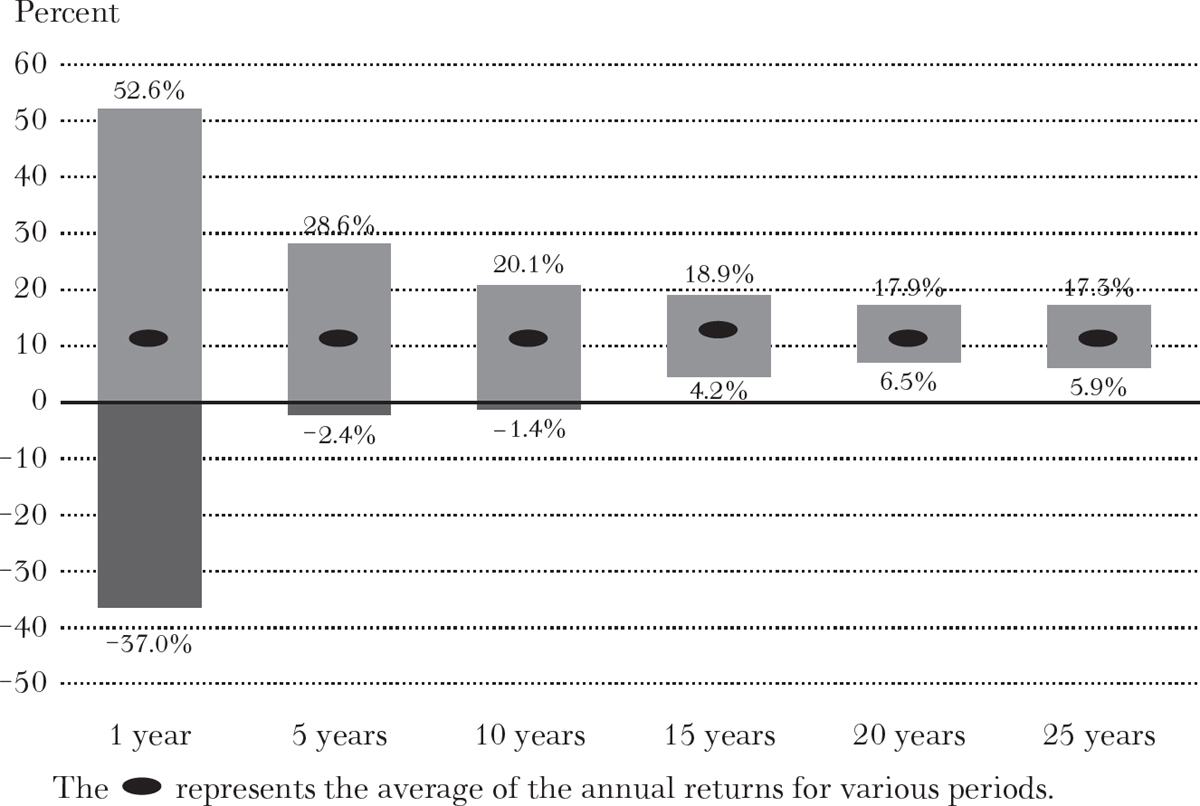

The figure on page 351 is worth a thousand words, so I can be brief in my explanation. If you held a diversified stock portfolio (such as the Standard & Poor’s 500-Stock Index) during the period from 1950 through 2020, you would have earned, on average, a quite generous return of about 10 percent. But the range of outcomes is certainly far too wide for an investor who has trouble sleeping at night. In one year, the rate of return from a typical stock portfolio was more than 52 percent, whereas in another year it was negative by 37 percent. Clearly, there is no dependability of earning an adequate rate of return in any single year. A one-year U.S. Treasury security or a one-year government-guaranteed certificate of deposit is the investment for those who need the money next year.

RANGE OF ANNUAL RETURN RATES ON COMMON STOCKS FOR VARIOUS TIME PERIODS, 1950–2020

But note how the picture changes if you held on to your common-stock investments for twenty-five years. Although there is some variability in the return achieved, depending on the exact twenty-five-year period in question, that variability is not large. On average, investments over all twenty-five-year periods covered by this figure have produced a rate of return of slightly more than 10 percent. This long-run expected rate of return was reduced by only about 4 percentage points if you happened to invest during the worst twenty-five-year period since 1950. It is this fundamental truth that makes a life-cycle view of investing so important. The longer the time period over which you can hold on to your investments, the greater should be the share of common stocks in your portfolio. In general, you are reasonably sure of earning the generous rates of return available from common stocks only if you can hold them for relatively long periods of time.*

Over investment periods of twenty or thirty years, stocks have generally been the clear winners, as is shown in the table below. These data further support the advice that younger people should have a larger proportion of their assets in stocks than older people.

PROBABILITY THAT STOCKS OUTPERFORM BONDS(PERCENTAGE OF PERIODS SINCE 1802 WHEN RETURNS OF STOCKS EXCEED THE RETURN FROM BONDS)

Investment Period |

Percentage of periods when stocks have outperformed bonds |

1 Year |

60.2 |

2 Years |

64.7 |

5 Years |

69.5 |

10 Years |

79.7 |

20 Years |

91.3 |

30 Years |

99.4 |

I do not mean to argue that stocks are not risky over long holding periods. Certainly the variability of the final value of your portfolio does increase the longer you hold your stocks. And we know that investors have experienced decades during which common stocks have produced near-zero overall returns. But for investors whose holding periods can be measured in twenty-five years or more, and especially those who reinvest their dividends and even add to their holdings through dollar-cost averaging, common stocks are very likely to provide higher returns than are available from safe bonds and even safer government-guaranteed savings accounts.

Finally, perhaps the most important reason for investors to become more conservative with age is that they have fewer years of paid labor ahead of them. Thus, they cannot count on salary income to sustain them if the stock market has a period of negative returns. Reverses in the stock market could then directly affect an individual’s standard of living, and the steadier—even if smaller—returns from bonds represent the more prudent investment stance. Hence, stocks should make up a smaller proportion of their assets.

3. Dollar-Cost Averaging Can Reduce the Risks of Investing in Stocks and Bonds

If, like most people, you will be building up your investment portfolio slowly over time with the accretion of yearly savings, you will be taking advantage of dollar-cost averaging. This technique is controversial, but it does help you avoid the risk of putting all your money in the stock or bond market at the wrong time.

Don’t be alarmed by the fancy-sounding name. Dollar-cost averaging simply means investing the same fixed amount of money in, for example, the shares of some index mutual fund, at regular intervals—say, every month or quarter—over a long period of time. Periodic investments of equal dollar amounts in common stocks can reduce (but not avoid) the risks of equity investment by ensuring that the entire portfolio of stocks will not be purchased at temporarily inflated prices.

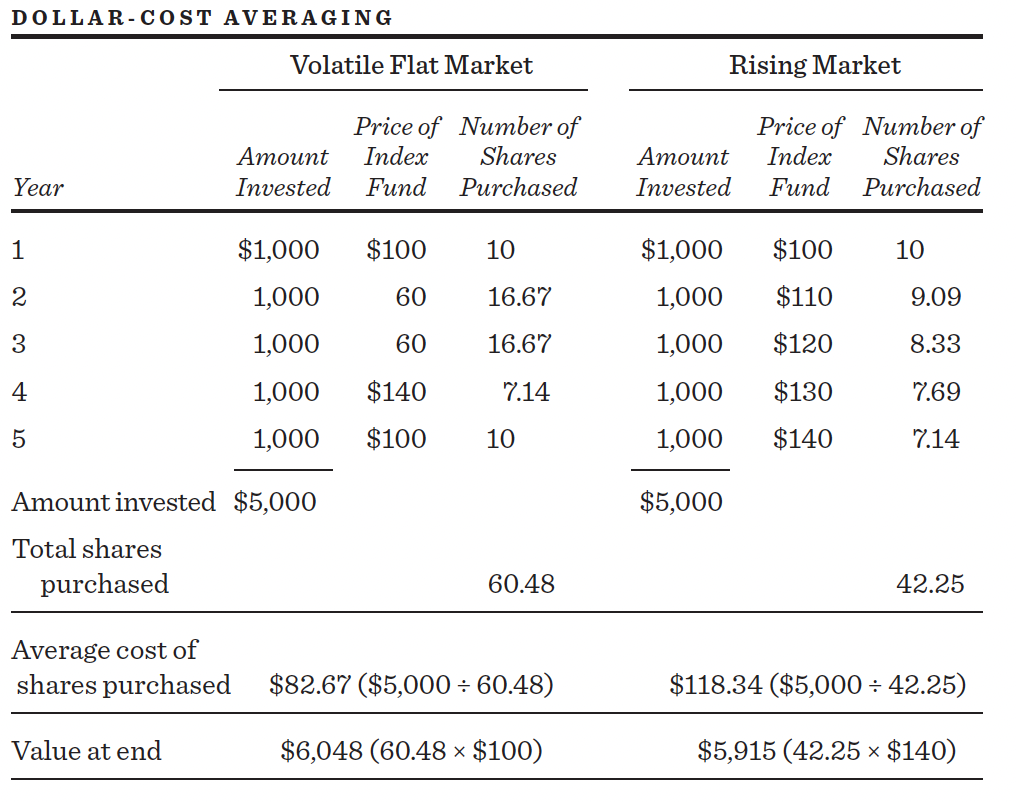

The table on page 354 assumes that $1,000 is invested each year. In scenario one, the market falls immediately after the investment program begins; then it rises sharply and finally falls again, ending, in year five, exactly where it began. In scenario two, the market rises continuously and ends up 40 percent higher. While exactly $5,000 is invested in both cases, the investor in the volatile market ends up with $6,048—a nice return of $1,048—even though the stock market ended exactly where it started. In the scenario where the market rose each year and ended up 40 percent from where it began, the investor’s final stake is only $5,915.

Warren Buffett presents a lucid rationale for this investment principle. In one of his published essays he says:

A short quiz: If you plan to eat hamburgers throughout your life and are not a cattle producer, should you wish for higher or lower prices for beef? Likewise, if you are going to buy a car from time to time but are not an auto manufacturer, should you prefer higher or lower car prices? These questions, of course, answer themselves.

But now for the final exam: If you expect to be a net saver during the next five years, should you hope for a higher or lower stock market during that period? Many investors get this one wrong. Even though they are going to be net buyers of stocks for many years to come, they are elated when stock prices rise and depressed when they fall. In effect, they rejoice because prices have risen for the “hamburgers” they will soon be buying. This reaction makes no sense. Only those who will be sellers of equities in the near future should be happy at seeing stocks rise. Prospective purchasers should much prefer sinking prices.

Dollar-cost averaging is not a panacea that eliminates the risk of investing in common stocks. It will not save your 401(k) plan from a devastating fall in value during a year such as 2008, because no plan can protect you from a punishing bear market. And you must have both the cash and the confidence to continue making the periodic investments even when the sky is the darkest. No matter how scary the financial news, no matter how difficult it is to see any signs of optimism, you must not interrupt the automatic-pilot nature of the program. Because if you do, you will lose the benefit of buying at least some of your shares after a sharp market decline when they are for sale at low prices. Dollar-cost averaging will give you this bargain: Your average price per share will be lower than the average price at which you bought shares. Why? Because you’ll buy more shares at low prices and fewer at high prices.

Some investment advisers are not fans of dollar-cost averaging, because the strategy is not optimal if the market does go straight up. (You would have been better off putting all $5,000 into the market at the beginning of the period.) But it does provide a reasonable insurance policy against poor future stock markets. And it does minimize the regret that inevitably follows if you were unlucky enough to have put all your money into the stock market during a peak period such as March of 2000 or October of 2007. To further illustrate the benefits of dollar-cost averaging, let’s move from a hypothetical to a real example. The following table shows the results (ignoring taxes) of a $500 initial investment made on January 1, 1978, and thereafter $100 per month, in the shares of the Vanguard 500 Index mutual fund. Less than $53,200 was committed to the program. The final value was over $1,460,000.

ILLUSTRATION OF DOLLAR-COST AVERAGING WITH VANGUARD’S 500 INDEX FUND

Year Ended December 31 |

Total Cost of Cumulative Investments |

Total Value of Shares Acquired |

1978 |

$1,600 |

$1,669 |

1979 |

2,800 |

3,274 |

1980 |

4,000 |

5,755 |

1981 |

5,200 |

6,630 |

1982 |

6,400 |

9,487 |

1983 |

7,600 |

12,783 |

1984 |

8,800 |

14,864 |

1985 |

10,000 |

20,905 |

1986 |

11,200 |

25,935 |

1987 |

12,400 |

28,221 |

1988 |

13,600 |

34,079 |

1989 |

14,800 |

46,126 |

1990 |

16,000 |

45,803 |

1991 |

17,200 |

61,010 |

1992 |

18,400 |

66,817 |

1993 |

19,600 |

74,687 |

1994 |

20,800 |

76,779 |

1995 |

22,000 |

106,944 |

1996 |

23,200 |

132,768 |

1997 |

24,400 |

178,217 |

1998 |

25,600 |

230,619 |

1999 |

26,800 |

280,565 |

2000 |

28,000 |

256,271 |

2001 |

29,200 |

226,622 |

2002 |

30,400 |

177,503 |

2003 |

31,600 |

229,524 |

2004 |

32,800 |

255,479 |

2005 |

34,000 |

268,933 |

2006 |

35,200 |

312,318 |

2007 |

36,400 |

330,350 |

2008 |

37,600 |

208,941 |

2009 |

38,800 |

265,756 |

2010 |

40,000 |

306,756 |

2011 |

41,200 |

313,981 |

2012 |

42,400 |

364,932 |

2013 |

43,600 |

483,743 |

2014 |

44,800 |

550,388 |

2015 |

46,000 |

558,467 |

2016 |

47,200 |

625,764 |

2017 |

48,400 |

762,690 |

2018 |

49,600 |

729,295 |

2019 |

60,800 |

959,096 |

2020 |

62,000 |

1,135,535 |

2021 |

53,200 |

1,460,868 |

Source: Vanguard.

Of course, no one can be sure that the next forty-five years will provide the same returns as past periods. But the table does illustrate the tremendous potential gains possible from consistently following a dollar-cost averaging program. But remember, because there is a long-term uptrend in common-stock prices, this technique is not necessarily appropriate if you need to invest a lump sum such as a bequest.

If possible, keep a small reserve (in a money fund) to take advantage of market declines and buy a few extra shares if the market is down sharply. I’m not suggesting for a minute that you try to forecast the market. However, it’s usually a good time to buy after the market has fallen out of bed. Just as hope and greed can sometimes feed on themselves to produce speculative bubbles, so do pessimism and despair react to produce market panics. The greatest market panics are just as unfounded as the most pathological speculative explosions. For the stock market as a whole (not for individual stocks), Newton’s law has always worked in reverse: What goes down has come back up.

4. Rebalancing Can Reduce Investment Risk and Possibly Increase Returns

A very simple investment technique called rebalancing can reduce investment risk and, in some circumstances, even increase investment returns. The technique simply involves bringing the proportions of your assets devoted to different asset classes (e.g., stocks and bonds) back into the proportions suited to your age and your attitude toward and capacity for risk. Suppose you decided that your portfolio ought to consist of 60 percent stocks and 40 percent bonds and at the start of your investment program you divided your funds in those proportions between those two asset classes. But after one year you discovered that your stocks had risen sharply while the bonds had fallen in price, so the portfolio was now 70 percent stocks and 30 percent bonds. A 70–30 mix would then appear to be a riskier allocation than the one most suitable for your risk tolerance. The rebalancing technique calls for selling some stocks (or equity mutual funds) and buying bonds to bring the allocation back to 60–40.

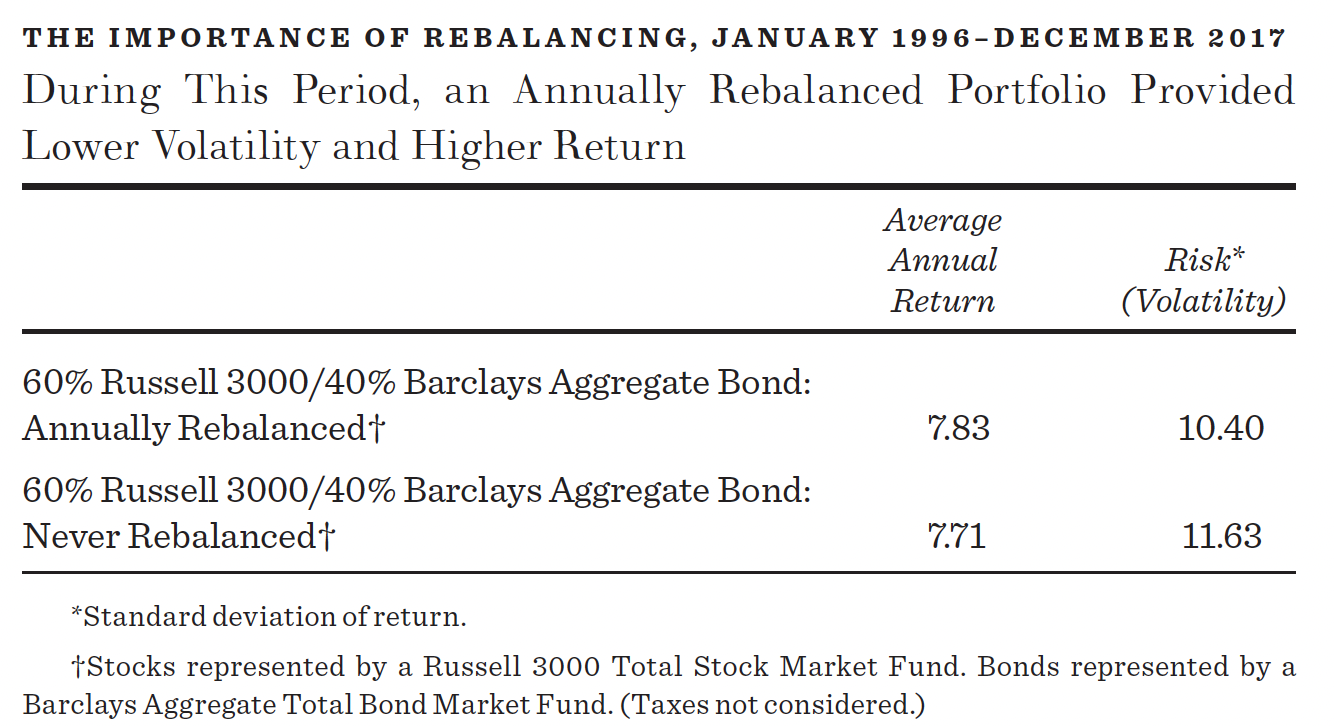

The table below shows the results of a rebalancing strategy over the twenty years ending in December 2017. Every year (no more than once a year) the asset mix was brought back to the 60–40 initial allocation. Investments were made in low-cost index funds. The table shows that the volatility of the market value of the portfolio was markedly reduced by the rebalancing strategy. Moreover, rebalancing improved the average annual portfolio return. Without rebalancing, the portfolio returned 7.71 percent over the period. Rebalancing improved the annual rate of return to 7.83 percent with less volatility.

What kind of alchemy permitted the investor who followed a rebalancing strategy at the end of each year to increase her rate of return? Think back to what was happening to the stock market over this period. By late 1999, the stock market had experienced an unprecedented bubble and equity values soared. The investor who rebalanced had no idea that the top of the market was near, but she did see that the equity portion of the portfolio had soared far above her 60 percent target. Thus, she sold enough equities (and bought enough bonds) to restore the original mix. Then, in late 2002, at just about the bottom of the bear market for stocks (and after a strong positive market for bonds), she found that the equity share was well below 60 percent and the bond share was well above 40 percent, and she rebalanced into stocks. Again, at the end of 2008, when stocks had plummeted and bonds had risen, she sold bonds and bought stocks. We all wish that we had a little genie who could reliably tell us to “buy low and sell high.” Systematic rebalancing is the closest analogue we have.

5. Distinguishing between Your Attitude toward and Your Capacity for Risk

As I mentioned at the beginning of this chapter, the kinds of investments that are appropriate for you depend significantly on your noninvestment sources of income. Your earning ability outside your investments, and thus your capacity for risk, is usually related to your age. Three illustrations will help you understand this concept.

Mildred G. is a recently widowed sixty-four-year-old. She has been forced to give up her job as a registered nurse because of increasingly severe arthritis. Her modest house in Homewood, Illinois, is still mortgaged. Although the mortgage was taken out at a relatively low rate, it involves substantial monthly payments. Apart from monthly Social Security checks, all Mildred has to live on are the earnings on a $250,000 insurance policy of which she is the beneficiary and a $50,000 portfolio of small-growth stocks accumulated by her late husband.

It is clear that Mildred’s capacity to bear risk is severely constrained by her financial situation. She has neither the life expectancy nor the physical ability to earn income outside her portfolio. Moreover, she has substantial fixed expenditures on her mortgage. She would have no ability to recoup a loss on her portfolio. She needs a portfolio of safe investments that can generate substantial income. Bonds and high-dividend-paying stocks, as from an index fund of real estate investment trusts, are the kinds of investments that are suitable. Risky (often non-dividend-paying) stocks of small-growth companies—no matter how attractive their prices may be—do not belong in Mildred’s portfolio.

Tiffany B. is an ambitious, single twenty-six-year-old who recently completed an MBA at Stanford’s Graduate School of Business and has entered a training program at the Bank of America. She just inherited a $50,000 legacy from her grandmother’s estate. Her goal is to build a sizable portfolio that in later years could finance the purchase of a home and be available as a retirement nest egg.

For Tiffany, one can safely recommend an aggressive portfolio. She has both the life expectancy and the earning power to maintain her standard of living in the face of any financial loss. Although her personality will determine the precise amount of risk exposure she is willing to undertake, it is clear that Tiffany’s portfolio belongs toward the far end of the risk-reward spectrum. Mildred’s portfolio of small-growth stocks would be far more appropriate for Tiffany than for a sixty-four-year-old widow who is unable to work.

In an earlier edition of this book, I presented the case of Carl P., a forty-three-year-old foreman at a General Motors production plant in Pontiac, Michigan, who made over $70,000 per year. His wife, Joan, had a $12,500 annual income from selling Avon products. The Ps had four children, ages six to fifteen. Carl and Joan wanted all the children to attend college. They realized that private colleges were probably beyond their means but hoped that an education within the excellent Michigan state university system would be feasible. Fortunately, Carl had been saving regularly through the GM payroll savings plan but had chosen the option of purchasing GM stock under the plan. He had accumulated GM stock worth $219,000. He had no other assets but did have substantial equity in a modest house with only a small mortgage remaining to be paid off.

I suggested that Carl and Joan had a highly problematic portfolio. Both their income and their investments were tied up in GM. A negative development that caused a sharp loss in GM’s common stock could ruin both the value of the portfolio and Carl’s livelihood. Indeed, the story ended badly. General Motors declared bankruptcy in 2009. Carl lost his job as well as his investment portfolio. And this is not an isolated example. Remember the sad lesson learned by many Enron employees who lost not only their jobs but all their savings in Enron stock when the company went under. Never take on the same risks in your portfolio that attach to your major source of income.

THREE GUIDELINES TO TAILORING A LIFE-CYCLE INVESTMENT PLAN

Now that I have set the stage, the next sections present a life-cycle guide to investing. We will look here at some general rules that will be serviceable for most individuals at different stages of their lives. In the next section I summarize them in an investment guide. Of course, no guide will fit every individual case. Any game plan will require some alteration to fit individual circumstances. This section reviews three broad guidelines that will help you tailor an investment plan to your particular circumstances.

1. Specific Needs Require Dedicated Specific Assets

Always keep in mind: A specific need must be funded with specific assets dedicated to that need. Consider a young couple in their twenties attempting to build a retirement nest egg. The advice in the life-cycle investment guide that follows is certainly appropriate to meet those long-term objectives. But suppose that the couple expects to need a $50,000 down payment to purchase a house next year. That $50,000 to meet a specific need should be invested in a safe security, maturing when the money is required, such as a one-year certificate of deposit (CD). Similarly, if college tuitions will be needed in three, four, five, and six years, funds might be invested in zero-coupon securities of the appropriate maturity or in different CDs.

2. Recognize Your Tolerance for Risk

By far the biggest individual adjustment to the general guidelines suggested concerns your own attitude toward risk. It is for this reason that successful financial planning is more of an art than a science. General guidelines can be extremely helpful in determining what proportion of a person’s funds should be deployed among different asset categories. But the key to whether any recommended asset allocation works for you is whether you are able to sleep at night. Risk tolerance is an essential aspect of any financial plan, and only you can evaluate your attitude toward risk. You can take some comfort in the fact that the risk involved in investing in common stocks and long-term bonds is reduced the longer the time period over which you accumulate and hold your investments. But you must have the temperament to accept considerable short-term fluctuations in your portfolio’s value. How did you feel when the market fell by almost 50 percent in 2008? How well did you sleep when the market dropped by a third in a month between February and March of 2020, including a 13 percent decline on a single day, March 16, 2020? If you panicked and became physically ill because a large proportion of your assets was invested in common stocks, then clearly you should pare down the stock portion of your portfolio. Thus, subjective considerations also play a major role in the asset allocations you can accept, and you may legitimately stray from those recommended here depending on your aversion to risk.

3. Persistent Saving in Regular Amounts,No Matter How Small, Pays Off

One final preliminary before presenting the asset-allocation guide. What do you do if right now you have no assets to allocate? So many people of limited means believe that it is impossible to build up a sizable nest egg. Accumulating meaningful amounts of retirement savings often seems out of reach. Don’t despair. The fact is that a program of regular saving each week—persistently followed, as through a payroll savings or 401(k) retirement plan—can in time produce substantial sums of money. Can you afford to put aside $23 per week? Or $11.50 per week? If you can, the possibility of eventually accumulating a large retirement fund is easily attainable if you have many working years ahead of you.

The table below shows the results from an initial $500 investment and a continuing regular savings program of $100 per month, all placed in a Vanguard equity index fund.

HOW RETIREMENT FUNDS CAN BUILD: $500 INITIAL INVESTMENT AND $100 PER MONTH

Year |

Cumulative Investment |

Total Year Value |

1 |

$1,600 |

$1,669 |

5 |

$6,400 |

$9,487 |

10 |

$12,400 |

$28,221 |

20 |

$24,400 |

$178,217 |

44 |

$53,200 |

$1,460,686 |

If you are able to save only $50 per month—less than $2 per day—cut the numbers in the table in half; if you can save $200 per month, double them. Pick a no-load index mutual fund to accumulate your nest egg. ETFs, with a zero commission broker, would also be suitable. Automatic reinvestment of interest, or dividends and capital gains, is assumed in the table. Finally, make sure you check whether your employer has a matched-savings plan. Obviously, if by saving through a company-sponsored retirement plan you are able to match your savings with company contributions and gain tax deductions as well, your nest egg will grow that much faster.

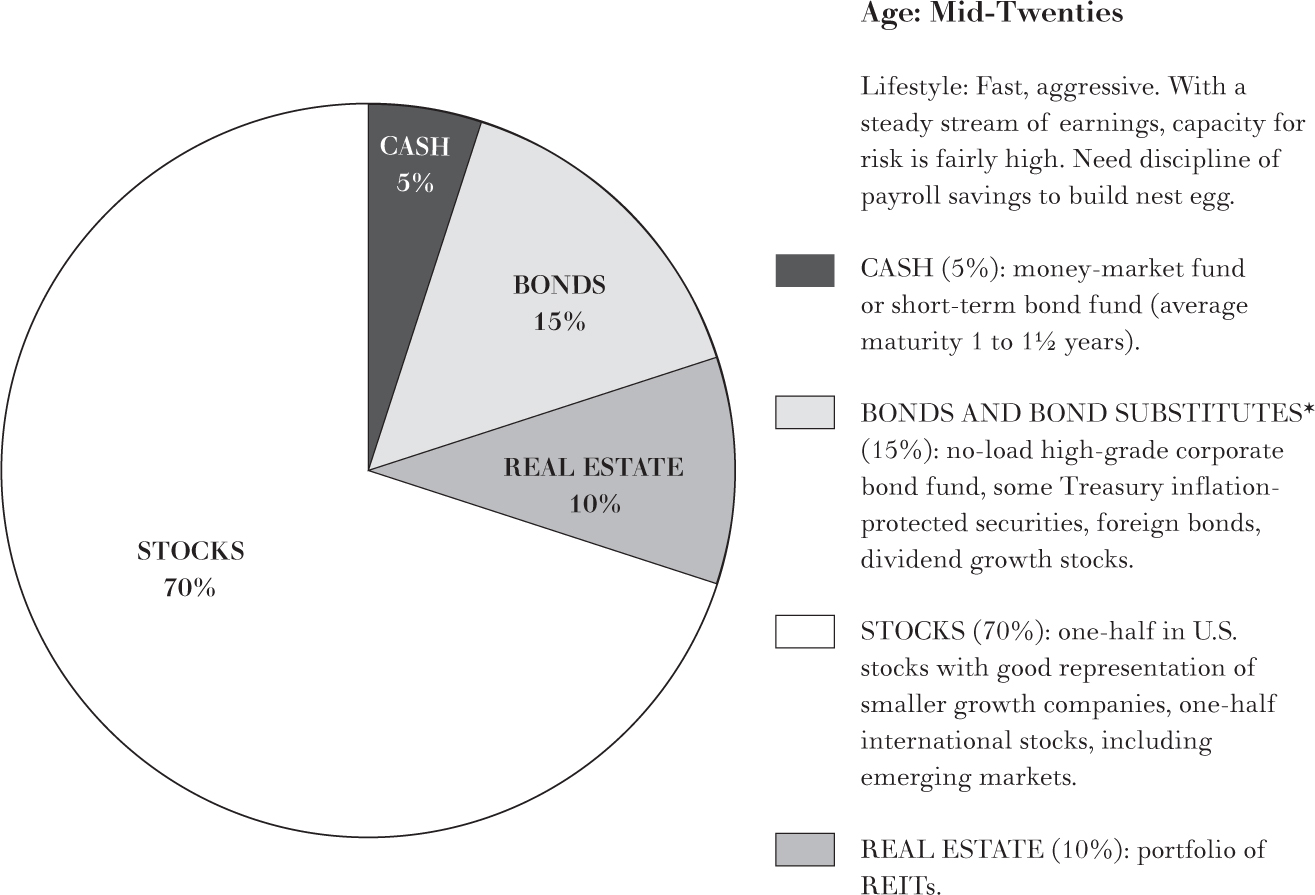

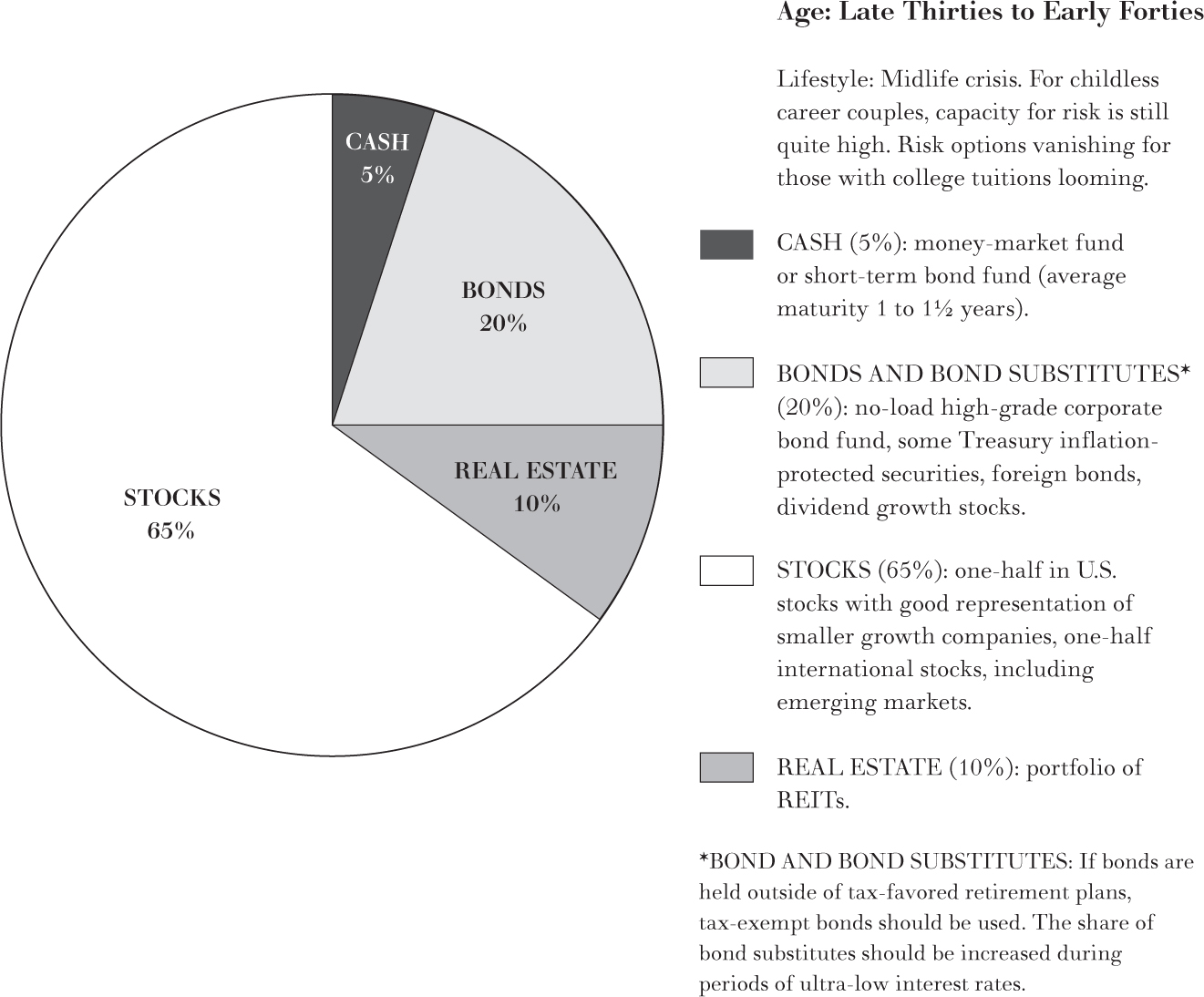

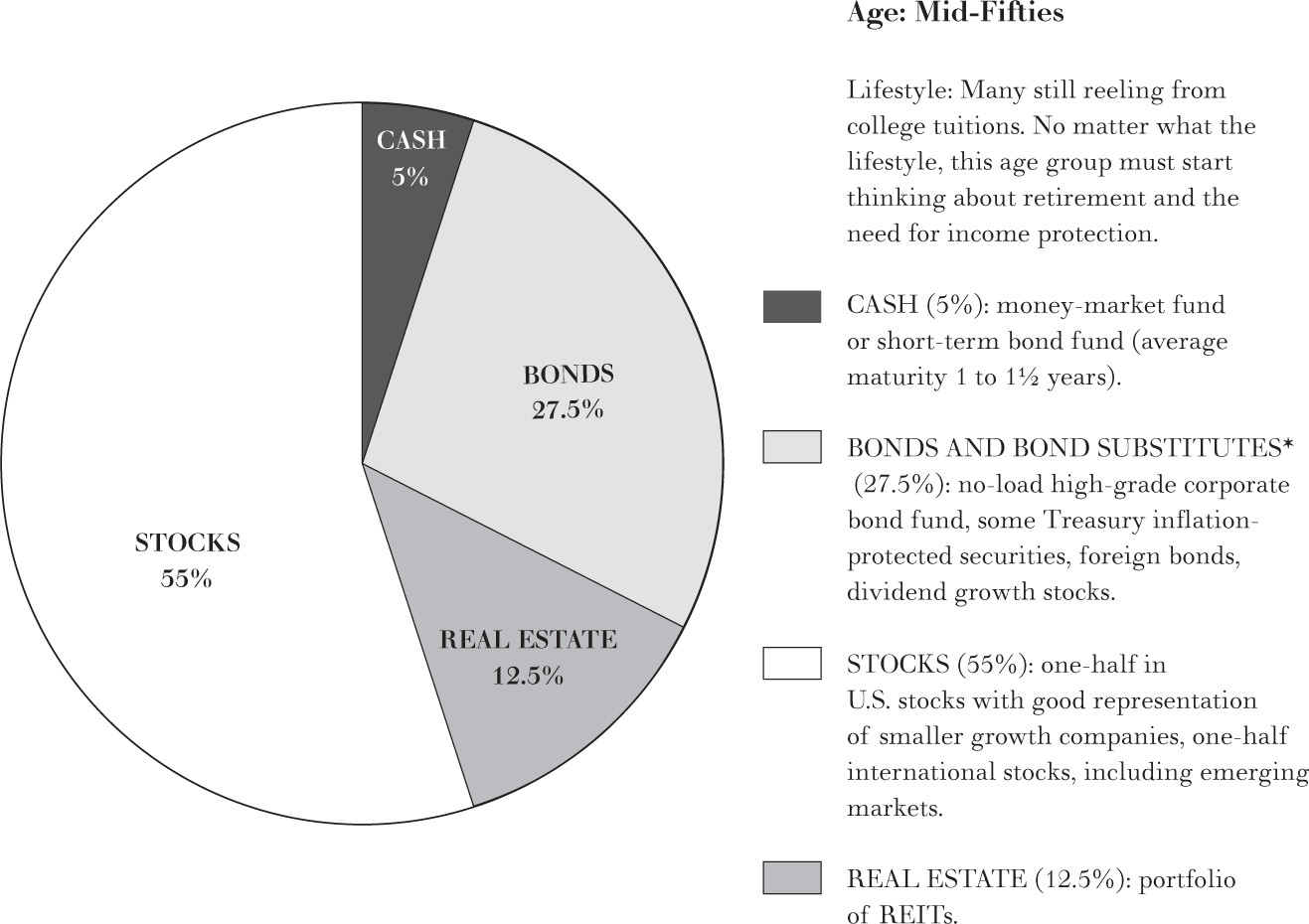

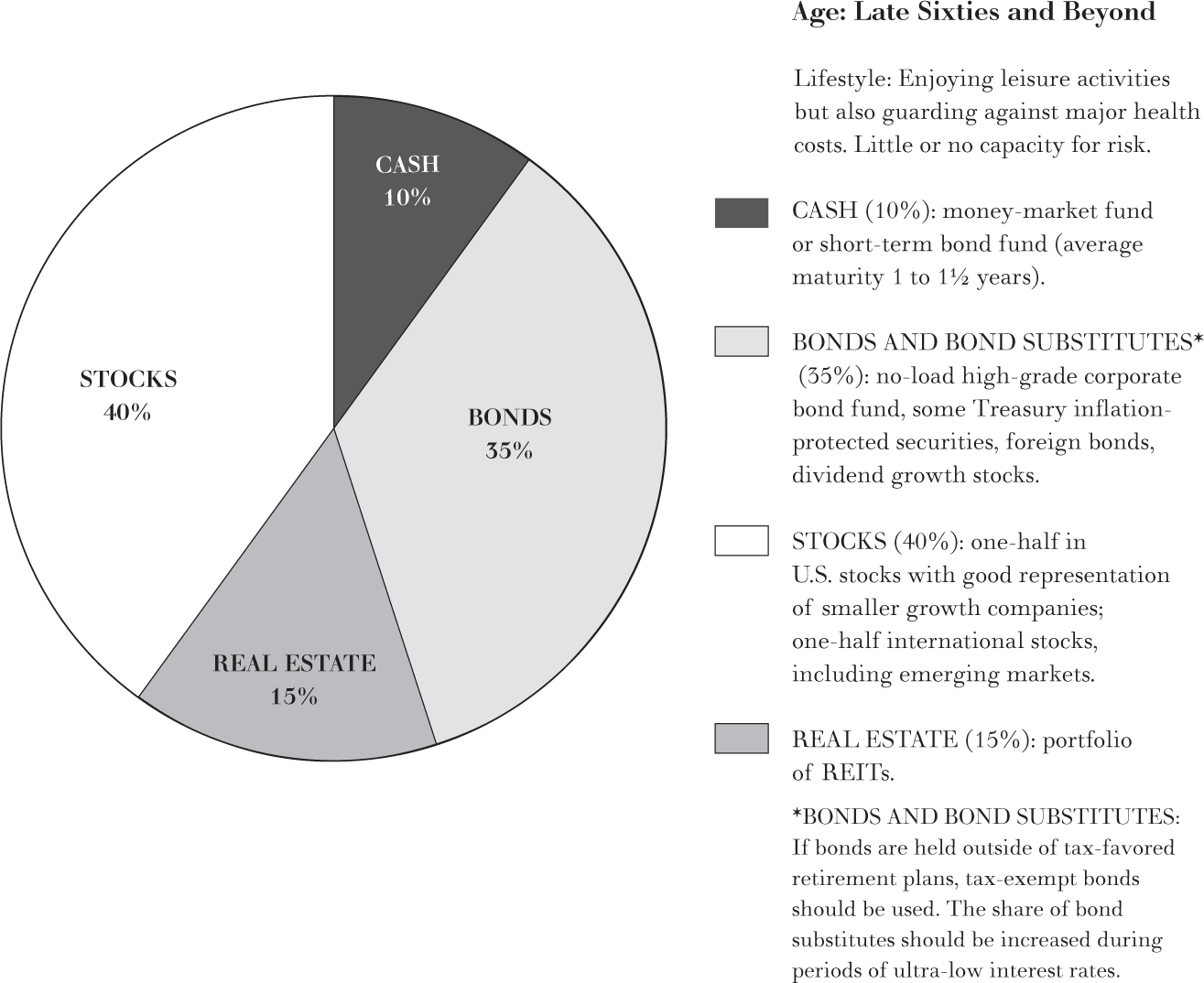

THE LIFE-CYCLE INVESTMENT GUIDE

The charts on pages 366–67 present a summary of the life-cycle investment guide. In the Talmud, Rabbi Isaac said that one should always divide one’s wealth into three parts: a third in land, a third in merchandise (business), and a third ready at hand (in liquid form). Such an asset allocation is hardly unreasonable, but we can improve on this ancient advice because we have more refined instruments and a greater appreciation of the considerations that make different asset allocations appropriate for different people. The general ideas behind the recommendations have been spelled out in detail above. For those in their twenties, a very aggressive investment portfolio is recommended. At this age, there is lots of time to ride out the peaks and valleys of investment cycles, and you have a lifetime of earnings from employment ahead of you. The portfolio is not only heavy in common stocks but also contains a substantial proportion of international stocks, including the higher-risk emerging markets. As mentioned in chapter 8, one important advantage of international diversification is risk reduction. Plus, international diversification enables an investor to gain exposure to other growth areas in the world even as world markets become more closely correlated.

As investors age, they should start cutting back on riskier investments and start increasing the proportion of the portfolio committed to bonds and bond substitutes such as dividend growth stocks during periods of ultra-low interest rates. The allocation is also increased to REITs that pay generous dividends. By the age of fifty-five, investors should start thinking about the transition to retirement and moving the portfolio toward income production. The proportion of bonds and bond substitutes increases, and the stock portfolio becomes more conservative and income-producing and less growth-oriented. In retirement, a portfolio heavily weighted in a variety of bonds and bond substitutes is recommended. A general rule of thumb used to be that the proportion of bonds in one’s portfolio should equal one’s age. Nevertheless, even in one’s late sixties, I suggest that 40 percent of the portfolio be committed to ordinary common stocks and 15 percent to real estate equities (REITs) to give some income growth to cope with inflation. Indeed, since life expectancies have increased significantly since I first presented these asset allocations during the 1980s, I have increased the proportion of equities accordingly.

For most people, I recommend starting with a broad-based, total stock market index fund rather than individual stocks for portfolio formation. I do so for two reasons. First, most people do not have sufficient capital to buy properly diversified portfolios themselves. Second, I recognize that most young people will not have substantial assets and will be accumulating portfolios by monthly investments. This makes mutual funds a very good choice. As your assets grow, a U.S. stock-market fund should be augmented with a total international stock (index) fund that includes stocks from fast-growing emerging markets. You don’t have to use the index funds I suggest, but do make sure that any mutual funds you buy are “no-load” and low cost. You will also see that I have included real estate explicitly in my recommendations. I said earlier that everyone should attempt to own his or her own home. I believe that everyone should have substantial real estate holdings, and some part of one’s equity holdings should be in real estate investment trust (REIT) index mutual funds described in chapter 12. With respect to your bond holdings, the guide recommends taxable bonds and bond substitutes. If, however, you are in the highest tax bracket and live in a high-tax state such as New York and your bonds are held outside of your retirement plan, use tax-exempt money funds and bond funds tailored to your state so that they are exempt from both federal and state taxes.

LIFE-CYCLE (TARGET DATE) FUNDS

Do you want to avoid the hassle of adjusting your portfolio as you age and rebalancing yearly as the proportions of your assets devoted to different asset classes vary with the ups and downs of the market? A new type of product has been developed during the 2000s just for those investors who want to set up a program and then forget about it. It is called the “life-cycle fund,” or “target date fund,” and it automatically does the rebalancing and moves to a safer asset allocation as you age. Life-cycle funds are particularly useful for IRAs, 401(k)s, and other non-taxable retirement plans. They can have adverse tax consequences when used in taxable accounts.

You pick the particular life-cycle fund that is appropriate by picking a date when you expect to retire. For example, suppose you are forty years old in 2025, and you plan to retire at age seventy. You should then buy a life-cycle fund with a “target maturity 2055.” Subsequent contributions can be directed to the same fund. The fund will be rebalanced annually, and the equity mix will become more conservative over time. The major mutual-fund complexes such as Vanguard, Fidelity, American Century, and T. Rowe Price all offer life-cycle funds. Details of the different maturities and the asset allocations offered may be found at the various company websites. When bond yields are extremely low, I tend to favor the life-cycle funds that are more aggressive—i.e., that start off with a larger allocation to equities and use fewer bonds. For those looking for the easiest way to manage their retirement monies, the automatic pilot aspect of life-cycle funds is a user-friendly feature. But before you sign up, check the fee schedule. Low fees mean more money in your pocket to enjoy a more comfortable retirement.

INVESTMENT MANAGEMENT ONCE YOU HAVE RETIRED

More than ten thousand baby boomers are reaching the age of sixty-five each day, a pattern that will continue until year 2030. According to the U.S. Census Bureau, more than one million baby boomers will live beyond the age of one hundred. A typical sixty-five-year-old has an average life expectancy of about twenty years. And half of all retirees will live longer than their average life expectancy. Yet most boomers have not heeded the advice in this book and have failed to save adequately for retirement. We have been a nation of consumers rather than savers. Given the long-run state of the federal budget, we can’t rely on the government to bail us out.

Inadequate Preparation for Retirement

According to a survey of consumer finances conducted by the Federal Reserve Board of Governors, the typical American family has little money in the bank and considerable credit card debt. Only half of all Americans have any kind of retirement account, and only 11 percent of Americans in the bottom wealth quartile have a savings/retirement plan. While older Americans (between the ages of fifty-five and sixty-four) have, on average, $308,000 in retirement savings, that amount would not be sufficient to replace more than 15 percent of their household income in retirement. It’s not a pretty picture. For many Americans, the golden years are likely to be extremely grim. Boomers approaching retirement who wish to avoid a life of privation have only two realistic choices. They can begin saving in a serious way. Alternatively, they can beat the odds and die early. As Henny Youngman used to say, “I’ve got all the money I’ll ever need if I die by four o’clock.”

For readers who find themselves in the situation I have described, I have no easy answers. You have no alternative but to work during your retirement years and to control expenses and save as much as possible. But there is a bright side even for you. There are many part-time jobs that can be done from home thanks to the Internet, especially after COVID. And there are psychological and health benefits to working in retirement. Those who do some work have a better feeling of self-worth and connectedness, and they are also healthier. Indeed, I would recommend that everyone should delay retirement as long as possible and put off taking Social Security until full retirement age so as to maximize annual benefits. Only for those in very poor health with a short life expectancy would I recommend starting to take benefits at the earliest age at which you can start to collect.

INVESTING A RETIREMENT NEST EGG

If you’ve been prescient enough to save for your retirement, what investment strategies will help ensure that your money lasts as long as you do? There are two basic alternatives. First, one can annuitize all or part of one’s retirement nest egg. Second, the retiree can continue to hold his investment portfolio and set up a withdrawal rate that provides for a comfortable retirement while minimizing the risk of outliving the money. How should one decide between the two alternatives?

Sturgeon’s Law, coined by the science fiction writer Theodore Sturgeon, states, “95 percent of everything you hear or read is crap.” That is certainly true in the investment world, but I sincerely believe that what you read here falls into the category of the other 5 percent. With respect to the advice regarding annuities, I suspect that the percentage of misinformation is closer to 99 percent. Your friendly annuity salesman will tell you that annuities are the only reasonable solution to the retirement investment problem. But many financial advisers are likely to say, “Don’t buy an annuity: You’ll lose all your money.” What’s an investor to make of such diametrically opposite advice?

Let’s first get straight what annuities are and describe their two basic types. An annuity is often called “long-life insurance.” Annuities are contracts made with an insurance company where the investor pays a sum of money to guarantee a series of periodic payments that will last as long as the annuitant lives. For example, during early 2022 a $1,000,000 premium for a fixed lifetime annuity would purchase an average annual income stream of about $61,250 for a sixty-five-year-old male. If a sixty-five-year-old couple retired and desired a joint and survivor option (that provided payments as long as either member of the couple was alive), the million dollars would provide fixed annual payments of about $51,500.

Of course, with any inflation, the purchasing power of those payments would tend to decrease over time. For that reason, many people prefer to purchase “variable annuities.” Variable annuities provide the possibility of rising payments over time, depending upon the type of investment assets (typically mutual funds) chosen by the annuitants. If the annuitant chooses common stocks, the payments will rise over time if the stock market does well, but they will fall if the stock market falters. Annuities can also be purchased with a guaranteed payment period. A twenty-year guaranteed period means that even if you die immediately after purchasing the annuity, your heirs will receive twenty years of payments. Of course, the annuitant will pay for that guarantee by accepting a substantial reduction in the dollar amount of the annual payments. The reduction for a seventy-year-old male is likely to be over 20 percent. Thus, if you are really bothered by the possibility of dying early and leaving nothing behind, it’s probably better to scale back the proportion of your retirement nest egg used for an annuity purchase.

Variable annuities provide one approach to addressing inflation risk. Another possibility is an annuity with an explicit inflation-adjustment factor. Such a guarantee will naturally lower the initial payment substantially. A sixty-five-year-old couple desiring a joint and survivor option would find that $1,000,000 would provide an initial annual payment of less than $40,000 per year.

Annuities have one substantial advantage over a strategy of investing your retirement nest egg yourself. The annuity guarantees that you will not outlive your money. If you are blessed with the good health to live well into your nineties, it is the insurance company that takes the risk that it has paid out to you far more than your original principal plus its investment earnings. Risk-averse investors should certainly consider putting some or even all of their accumulated savings into an annuity contract upon retirement.

What, then, are the disadvantages of annuities? There are four possible disadvantages. Annuitization is inconsistent with a bequest motive, it gives the annuitant an inflexible path of consumption, it can involve high transactions costs, and it can be tax inefficient.

1. Desire to Leave a Bequest. Suppose a retiree has saved a substantial nest egg and can live comfortably off the dividends and interest from the investments. While an even larger amount of yearly income could be provided by annuitization, there would be no money left over for bequests when the annuitant dies. Many individuals have a strong desire to be able to leave some funds for children, relatives, or eleemosynary institutions. Full annuitization is inconsistent with such bequest motives.

2. Flexibility of Consumption. Suppose a couple retires in good health at age sixty-five and purchases an annuity that pays a fixed sum each year as long as either partner is alive. Such a “joint life” annuity is a common way for couples to structure their retirement. But right after signing the contract with the insurance company, both husband and wife learn that they have incurable diseases that are highly likely to reduce the period each will survive to a precious few years. The couple might reasonably want to take the around-the-world trip they had always dreamed of. Annuitization gives them no flexibility to alter their path of consumption if circumstances change.

3. Annuities Can Be Costly. Many annuities, especially those sold by insurance agents, can be very costly. The purchaser pays not only the fees and expenses of the insurance company but also a sales commission for the selling agent. Some annuities can thus be very poor investments.

4. Annuities Can Be Tax Inefficient. While there are some advantages to fixed annuities relative to bonds in terms of tax deferral, variable annuities turn preferentially taxed capital gains into ordinary income subject to higher tax rates. Also, partial annuitization of retirement account assets does not offset the required minimum distributions (RMDs) you must take. If you annuitize 50 percent of your IRA, you still have to take RMDs on the other half. This is no problem if you are spending at least that total amount, but tax inefficient if you are not.

So what should smart investors do? Here are my rules: At least partial annuitization usually does make sense. It is the only no-risk way of ensuring that you will not outlive your income. Reputable companies offer annuities with low costs and no sales commissions. In order to make sensible decisions on annuities, you should do some comparison shopping on the Internet at http://www.valic.com. You will find considerable variation in rates from different providers.

Many retirees will prefer to keep control of at least a portion of the assets they have saved for a retirement nest egg. Let’s suppose the assets are invested in accordance with the bottom pie chart shown on page 367, that is, a bit more than half in equities and the rest in income-producing investments. Now that you are ready to crack open the nest egg for living expenses in retirement, how much can you spend if you want to be sure that your money will last as long as you do? I suggested in previous editions that you use “the 4 percent solution.”† With interest rates as low as they are in 2022, a 3½ (or even a 3) percent rate is more likely to give you some assurance that you will not outlive your money.

Under the “3½ percent solution,” you should spend no more than 3½ percent of the total value of your nest egg annually. At that rate the odds are good that you will not run out of money even if you live to a hundred. It is highly likely, too, that you will also be able to leave your heirs with a sum of money that has the same purchasing power as the total of your retirement nest egg. Under the 3½ percent rule, you would need $514,286 of savings to produce an income in retirement of $1,500 per month or $18,000 per year.

Why only 3½ percent? It is likely that a diversified portfolio of stocks and bonds will return more than 3½ percent in the years ahead. But there are two reasons to limit the take-out rate. First, you need to allow your monthly payments to grow over time at the rate of inflation. Second, you need to ensure that you could ride out several years of the inevitable bear markets that the stock market can suffer during certain periods.

Let’s see first where the 3½ percent figure comes from. We suggested on page 344 that stocks might be expected to produce a long-run rate of return of about 6 percent per annum. A diversified bond portfolio, including a large proportion of bond substitutes, might produce something like a 4 percent return. Hence we can project that a balanced portfolio of half stocks and half bonds should produce approximately a 5 percent return per year. Now suppose that over the long pull the inflation rate is 1½ percent. That means that the corpus of the investment fund will have to rise by 1½ percent a year to preserve its purchasing power. Thus, in a typical year the investor will spend 3½ percent of the fund, and the nest egg will grow by 1½ percent. Spending in the following year can also grow by 1½ percent so that the retiree will still be able to buy the same market basket of goods. By spending less than the total return from the portfolio, the retiree can preserve the purchasing power of both the investment fund and its annual income. The general rule is: First estimate the return of the investment fund, and then deduct the inflation rate to determine the sustainable level of spending. If inflation is likely to be 2 percent per year (the Federal Reserve’s target), then a 3 percent spending rate would be more appropriate.

There is a second reason to set the spending rate below the estimated rate of return for the whole fund. Actual returns from stocks and bonds vary considerably from year to year. Stock returns may average 6 percent, but in some years the return will be higher, whereas in other years it might be negative. Suppose you retired at age sixty-five and then encountered a bear market as severe as the one in 2008 and 2009, when stocks declined by about 50 percent. Had you withdrawn 6 percent annually, your savings could have been exhausted in less than ten years. But had you withdrawn only 3½ percent, you would be unlikely to run out of money even if you lived to a hundred. A conservative spending rate maximizes your chances of never running out of money. So if you are not retired, think hard about stashing away as much as you can so that later you can live comfortably even with a conservative withdrawal rate.

Three footnotes need to be added to our retirement rules. First, in order to smooth out your withdrawals over time, don’t just spend 3½ percent of whatever value your investment fund achieves at the start of each year. Since markets fluctuate, your spending will be far too uneven and undependable from year to year. My advice is to start out spending 3½ percent of your retirement fund and then let the amount you take out grow by 1½ percent per year. This will smooth out the amount of income you will have in retirement.

Second, you will find that the interest income from your bonds and bond substitutes plus the dividends from your stocks are very likely to be less than the 3½ percent you wish to take out of your fund. So you will have to decide which of your assets to tap first. You should sell from the portion of your portfolio that has become overweighted relative to your target asset mix. Suppose that the stock market has rallied so sharply that an initial 50-50 portfolio has become lopsided with 60 percent stocks and 40 percent bonds. While you may be delighted that the stocks have done well, you should be concerned that the portfolio has become riskier. Take whatever extra moneys you need out of the stock portion of the portfolio, adjusting your asset allocation and producing needed income at the same time. Even if you don’t need to tap the portfolio for spending income, I would recommend rebalancing your portfolio annually so as to keep the risk level of the portfolio consistent with your tolerance for risk.

Third, develop a strategy of tapping assets so as to defer paying income taxes as long as possible. When you start taking federally mandated required minimum distributions from IRAs and 401(k)s, you will need to use these before tapping other accounts. In taxable accounts, you are already paying income taxes on the dividends, interest, and realized capital gains that your investments produce. Thus, you certainly should spend these moneys next (or even first if you have not yet reached the age of seventy and a half when withdrawals are required). Next, spend additional tax-deferred assets. If your bequests are likely to be to your heirs, spend Roth IRA assets last. There is no required withdrawal for these accounts, and these assets will keep accumulating earnings tax-free. In general, the last dollars you will want to spend are your Roth IRA dollars.

No one can guarantee that the rules I have suggested will keep you from outliving your money. And depending on your health and other income and assets, you may well want to alter my rules in one direction or another. If you find yourself at age eighty, withdrawing 3½ percent each year and with a growing portfolio, either you have profound faith that medical science has finally discovered the Fountain of Youth, or you should consider loosening the purse strings.

*Technically, the finding that risk is reduced by longer holding periods depends on the reversion-to-the-mean phenomenon described in chapter 11. The interested reader is referred to Paul Samuelson’s article “The Judgment of Economic Science on Rational Portfolio Management” in the Journal of Portfolio Management (Fall 1989).

† In the ninth edition of this book, I recommended a 4½ percent rule because bond yields were considerably higher than they are in the early 2020s.