A FITNESS MANUAL FOR RANDOM WALKERS AND OTHER INVESTORS

In investing money, the amount of interest you want should depend on whether you want to eat well or sleep well.

—J. Kenfield Morley, Some Things I Believe

PART FOUR IS a how-to-do-it guide for your random walk down Wall Street. In this chapter, I offer general investment advice that should be useful to all investors, even if they don’t believe that securities markets are highly efficient. In chapter 13, I try to explain the recent fluctuations that have occurred in stock and bond returns and to show how you might estimate what the future holds. In chapter 14, I present a life-cycle investment guide indicating how the stage of your life plays an important role in determining the mix of investments that is most likely to enable you to meet your financial goals.

In the final chapter, I outline specific strategies for equity investors who believe at least partially in the efficient-market theory or who are convinced that even if real expertise does exist, they are unlikely to find it. But if you are sensible, you will take your random walk only after you have made detailed and careful preparations. Even if stock prices move randomly, you shouldn’t. Think of the advice that follows as a set of warm-up exercises that will enable you to make sensible financial decisions and increase your after-tax investment returns.

EXERCISE 1: GATHER THE NECESSARY SUPPLIES

A widely held belief is that the tickets to a comfortable retirement and a fat investment portfolio are instructions on what extraordinary individual stocks or mutual funds you should buy. Unfortunately, these tickets are not even worth the paper they are printed on. The harsh truth is that the most important driver in the growth of your assets is how much you save, and saving requires discipline. Without a regular savings program, it doesn’t matter if you make 5 percent, 10 percent, or even 15 percent on your investment funds. The single most important thing you can do to achieve financial security is to begin a regular savings program and to start it as early as possible. The only reliable route to a comfortable retirement is to build up a nest egg slowly and steadily. Yet few people follow this basic rule, and the savings of the typical American family are woefully inadequate.

It is critically important to start saving now. Every year you put off investing makes your ultimate retirement goals more difficult to achieve. Trust in time rather than in timing. As a sign in the window of a bank put it, little by little you can safely stock up a strong reserve here, but not until you start.

The secret of getting rich slowly (but surely) is the miracle of compound interest, described by Albert Einstein as the “greatest mathematical discovery of all time.” It simply involves earning a return not only on your original investment but also on the accumulated interest that you reinvest.

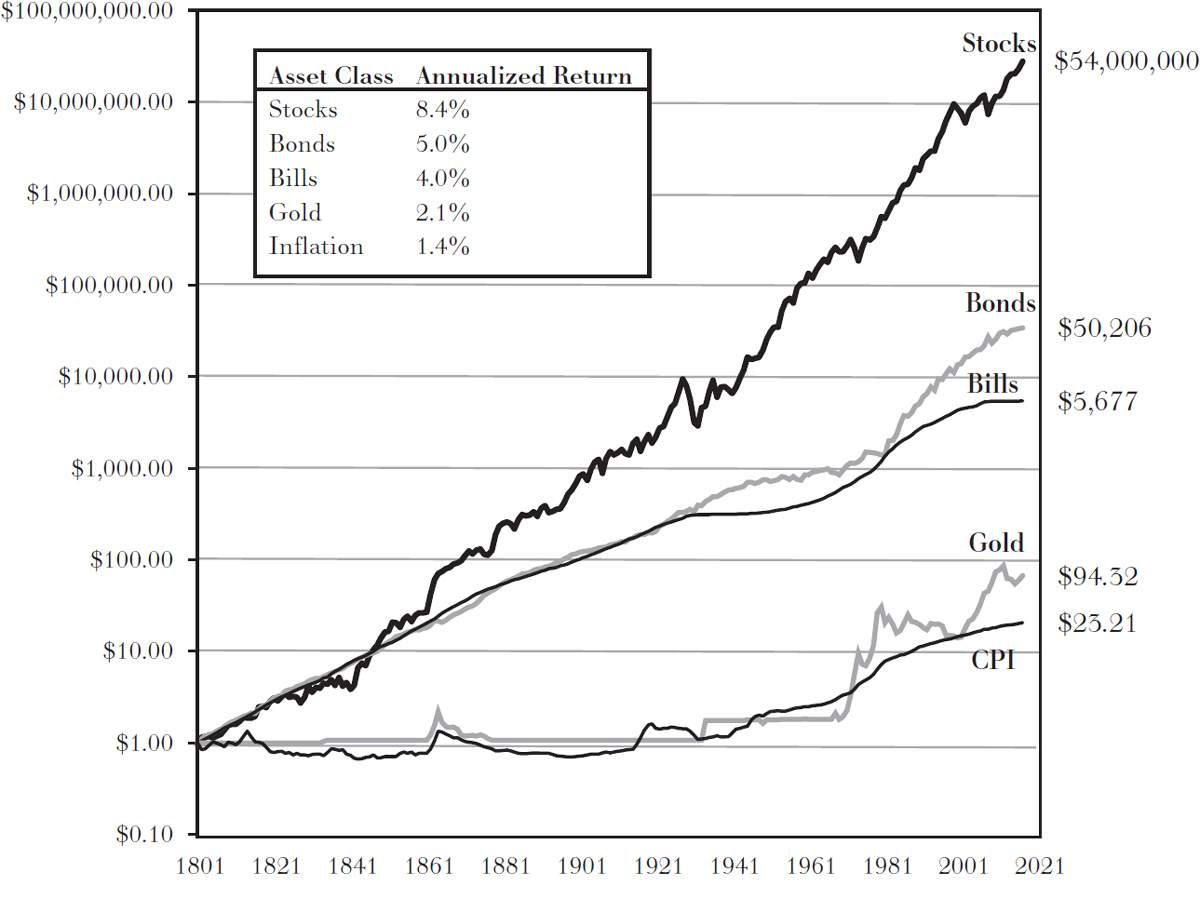

Jeremy Siegel, author of the excellent investing book Stocks for the Long Run, has calculated the returns from a variety of financial assets from 1802 to 2021. His work shows the incredible power of compounding. One dollar invested in stocks in 1802 would have grown to $54 million by the end of 2021. This amount far outdistanced the rate of inflation as measured by the consumer price index (CPI). The figure on page 291 also shows the modest returns that have been achieved by U.S. Treasury bills and gold.

TOTAL RETURN INDEXES

Source: Siegel, Stocks for the Long Run, 6th ed.

If you want a get-rich-quick investment strategy, this is not the book for you. I’ll leave that for the snake oil salesmen. You can only get poor quickly. To get rich, you will have to do it slowly, and you have to start now.

What if you did not save when you were younger and find yourself in your fifties with no savings, no retirement plan, and burdensome credit card debt? It’s going to be a lot harder to plan for a comfortable retirement. But it’s never too late. There is no other way to make up for lost time than to downsize your lifestyle and start a rigorous program of savings. You may also have no other choice but to remain in the workforce and to push back retirement a few years. Fortunately, you can play catch-up with tax-advantaged retirement plans that will be described below.

So put time on your side. Start saving early and save regularly. Live modestly and don’t touch the money that’s been set aside. If you need further discipline, remember that the only thing worse than being dead is to outlive the money you have put aside for retirement. And if projections are to be believed, about one million of today’s baby boomers will live to be at least one hundred.

EXERCISE 2: DON’T BE CAUGHT EMPTY-HANDED: COVER YOURSELF WITH CASH RESERVES AND INSURANCE

Remember Murphy’s Law: What can go wrong will go wrong. And don’t forget O’Toole’s commentary: Murphy was an optimist. Bad things do happen to good people. Life is a risky proposition, and unexpected financial needs occur in everyone’s lifetime. The boiler tends to blow up just at the time that your family incurs whopping medical expenses. A job layoff happens just after your son has totaled the family car. And who knew that even “secure” jobs could disappear during the COVID-19 pandemic? That’s why every family needs a cash reserve as well as adequate insurance to cope with the catastrophes of life.

I know that many brokers will tell you not to miss investing opportunities by sitting on your cash. “Cash is trash” is the mantra of the brokerage community. But everyone needs to keep some reserves in safe and liquid investments to pay for an unexpected medical bill or to provide a cushion during a time of unemployment. Assuming that you are protected by medical and disability insurance at work, this reserve might be established to cover three months of living expenses. The cash reserve fund should be larger, the older you are, but could be smaller if you work in an in-demand profession and/or if you have large investable assets. Moreover, any large future expenditures (such as your daughter’s college tuition bill) should be funded with short-term investments (such as a bank certificate of deposit) whose maturity matches the date on which the funds will be needed.

Most people need insurance. Those with family obligations are downright negligent if they don’t purchase insurance. We risk death every time we get into our automobile or cross a busy street. A hurricane or fire could destroy our home and possessions. Pandemics that shut down whole economies happen. People need to protect themselves against the unpredictable.

For individuals, home and auto insurance are a must. So is health and disability insurance. Life insurance to protect one’s family from the death of the breadwinner(s) is also a necessity. You don’t need life insurance if you are single with no dependents. But if you have a family with young children who count on your income, you do need life insurance and lots of it.

Two broad categories of life insurance products are available: high-premium policies that combine insurance with an investment account, and low-premium term insurance that provides death benefits only, with no buildup of cash value.

The high-premium policies do have some advantages and are often touted for their tax-saving benefits. Earnings on the part of the insurance premiums that go into the savings plan accumulate tax-free, and this can be advantageous for some individuals who have maxed out on their tax-deferred retirement savings plans. Moreover, individuals who will not save regularly may find that the periodic premium bills provide the discipline necessary for them to make sure that a certain amount will be available for their families if they die and that a cash value builds up on the investment part of the program. But policies of this kind provide the most advantages for the insurance agent who sells them and who collects high sales charges. Early premiums go mainly for sales commissions and other overhead rather than for buildup of cash value. Thus, not all your money goes to work. For most people, I therefore favor the do-it-yourself approach. Buy term insurance for protection and invest the difference yourself in a tax-deferred retirement plan. Such an investment plan is far superior to “whole life” or “variable life” insurance policies.

My advice is to buy renewable term insurance; you can keep renewing your policy without the need for a physical examination. So-called decreasing term insurance, renewable for progressively lower amounts, should suit many families best, because as time passes (and the children and family resources grow), the need for protection usually diminishes. You should understand, however, that term-insurance premiums escalate sharply when you reach the age of sixty or seventy or higher. If you still need insurance at that point, you will find that term insurance has become prohibitively expensive. But the major risk at that point is not premature death; it is that you may live too long and outlive your assets. You can increase those assets more effectively by buying term insurance and investing the money you save yourself.

Shop around for the best deal. Use quote services or the Internet to ensure that you are getting the best rates. For example, you can go to www.term4sale.com and see a number of alternative policies at varying prices. You don’t need an insurance agent. Policies available from agents will be more expensive since they need to include extra premiums to pay the agent’s sales commission. You can get a much better deal by doing it yourself.

Do not buy insurance from any company with an A.M. Best rating of less than A. A lower premium will not compensate you for taking any risk that your insurance company will get into financial difficulty and be unable to pay its claims. Don’t bet your life on a poorly capitalized insurance carrier.

You can obtain A.M. Best’s ratings of insurance companies at their website www.ambest.com. Insurance companies pay Best for the ratings. A somewhat more objective and critical rating is offered by Weiss Research, a consumer-supported company. The Weiss website is at www.weissratings.com.

I would avoid buying variable-annuity products, especially the high-cost products offered by insurance salespeople. A deferred variable annuity is essentially an investment product (typically a mutual fund) with an insurance feature. The insurance feature stipulates that if you die and the value of the investment fund has fallen below the amount you put in, the insurance company will pay back your full investment. These policies are very expensive because you typically pay high sales commissions and a premium for the insurance feature. Unless your mutual fund declines sharply with a fall in the stock market and you drop dead soon after purchasing a variable annuity, the value of this insurance is likely to be small. Remember the overarching rule for achieving financial security: keep it simple. Avoid any complex financial products as well as the hungry agents who try to sell them to you. The only reason you should even consider a variable annuity is if you are super wealthy and have maxed out on all the other tax-deferred savings alternatives. And even then you should purchase such an annuity directly from one of the low-cost providers such as the Vanguard Group.

EXERCISE 3: BE COMPETITIVE—LET THE YIELD ON YOUR CASH RESERVE KEEP PACE WITH INFLATION

As I’ve already pointed out, some ready assets are necessary for pending expenses, such as college tuition, possible emergencies, or even psychological support. Thus, you have a real dilemma. You know that if you keep your money in a savings bank and get, say, 1 percent interest in a year in which the inflation rate exceeds 2 percent, you will lose real purchasing power. In fact, the situation is even worse because the interest you get is subject to regular income taxes. Moreover, short-term interest rates were abnormally low during the 2010s and early 2020s. So what’s a small saver to do? Several short-term investments are likely to help provide the best rate of return, although no good alternatives exist when interest rates are very low.

Money-Market Mutual Funds (Money Funds)

Money-market mutual funds often provide investors the best instrument for parking their cash reserves. They combine safety and the ability to write large checks against your fund balance, generally in amounts of at least $250. Interest rates on these funds generally ranged from 1 to 5 percent during the first decade of the 2000s. For much of the 2010s and early 2020s, however, interest rates were very low and money-fund yields were near zero. Not all money-market funds are created equal; some have significantly higher expense ratios (the costs of running and managing the funds) than others. In general, lower expenses mean higher returns. A sample of relatively low-expense funds is presented in the Random Walker’s Address Book and Reference Guide at the end of this book.

Bank Certificates of Deposit (CDs)

A reserve for any known future expenditure should be invested in a safe instrument whose maturity matches the date on which the funds will be needed. Suppose you have set aside money for junior’s tuition bills that will need to be paid at the end of one, two, and three years. One appropriate investment plan in this case would be to buy three bank CDs with maturities of one, two, and three years. Bank CDs are even safer than money funds, typically offer higher yields, and are an excellent medium for investors who can tie up their liquid funds for at least six months.

Bank CDs do have some disadvantages. They are not easily converted into cash, and penalties are usually imposed for early withdrawal. Also, the yield on CDs is subject to state and local income taxes. Treasury bills (short-term U.S. government IOUs), which are discussed below, are exempt from state and local taxes.

Bank CD rates vary widely. Use the Internet to find the most attractive returns. Go to www.bankrate.com and search the site for the highest rates around the country. Deposits at all banks and credit unions listed at this site are insured by the Federal Deposit Insurance Corporation. Addresses and phone numbers are given for each listing, and you can call to confirm that the deposits are insured and learn what current rates of return are being offered.

Investors can also take advantage of online financial institutions that reduce their expenses by having neither branches nor tellers and by conducting all their business electronically. Thanks to their low overhead, they can offer rates significantly above both typical savings accounts and money-market funds. And, unlike money-market funds, those Internet banks that are members of the Federal Deposit Insurance Corporation can guarantee the safety of your funds. To find an Internet bank, go to the Google search engine and type in “Internet bank.” You will also see many of them popping up when you do a rate search on www.bankrate.com for the banks with the highest yields. The Internet banks generally post the highest CD rates available in the market.

Popularly known as T-bills, these are the safest financial instruments you can find and are widely treated as cash equivalents. Issued and guaranteed by the U.S. government, T-bills are auctioned with maturities of four weeks, three months, six months, or one year. They are sold at a minimum $1,000 face value and in $1,000 increments above that. T-bills offer an advantage over money-market funds and bank CDs in that their income is exempt from state and local taxes. In addition, T-bill yields are often higher than those of money-market funds. For information on purchasing T-bills directly, go to www.treasurydirect.gov.

If you find yourself lucky enough to be in the highest federal tax bracket, you will find tax-exempt money-market funds to be the best vehicle for your reserve funds. These funds invest in a portfolio of short-term issues of state and local government entities and generate income that is exempt from both federal and state taxes if the fund confines its investments to securities issued by entities within the state. They also offer free checking for amounts of $250 or more. The yields on these funds are lower than those of the taxable funds. Nevertheless, individuals in the highest income tax brackets will find the earnings from these funds more attractive than the after-tax yields on regular money-market funds. Most of the mutual-fund complexes also offer selected state tax-exempt funds. If you live in a state with high state income taxes, these funds can be very attractive on an after-tax basis. You should call one of the mutual-fund companies listed in the Random Walker’s Address Book to find out whether they have a money fund that invests only in the securities of the state in which you pay taxes.

EXERCISE 4: LEARN HOW TO DODGE THE TAX COLLECTOR

One of the jokes making the rounds of the Internet goes as follows:

A couple, both age seventy-eight, went to a sex therapist’s office. The doctor asked, “What can I do for you?” The man said, “Will you watch us have sexual intercourse?” The doctor looked puzzled, but agreed. When the couple finished, the doctor said, “There’s nothing wrong with the way you have intercourse,” and charged them $50. The couple asked for another appointment and returned once a week for several weeks. They would have intercourse, pay the doctor, then leave. Finally, the doctor asked, “Just exactly what are you trying to find out?” The old man said, “We’re not trying to find out anything. She’s married and we can’t go to her house. I’m married and we can’t go to my house. The Holiday Inn charges $93 and the Hilton Inn charges $108. We do it here for $50, and I get $43 back from Medicare.”

By telling this story, I do not mean to suggest that you attempt to cheat the government. But I do mean to suggest that you take advantage of every opportunity to make your savings tax-deductible and to let your savings and investments grow tax-free. For most people, there is no reason to pay any taxes on the earnings from the investments that you make to provide for your retirement. Almost all investors, except those who are super wealthy to begin with, can build up a substantial net worth in ways that ensure that nothing will be siphoned off by Uncle Sam. This exercise shows how you can legally stiff the tax collector.

Individual Retirement Accounts

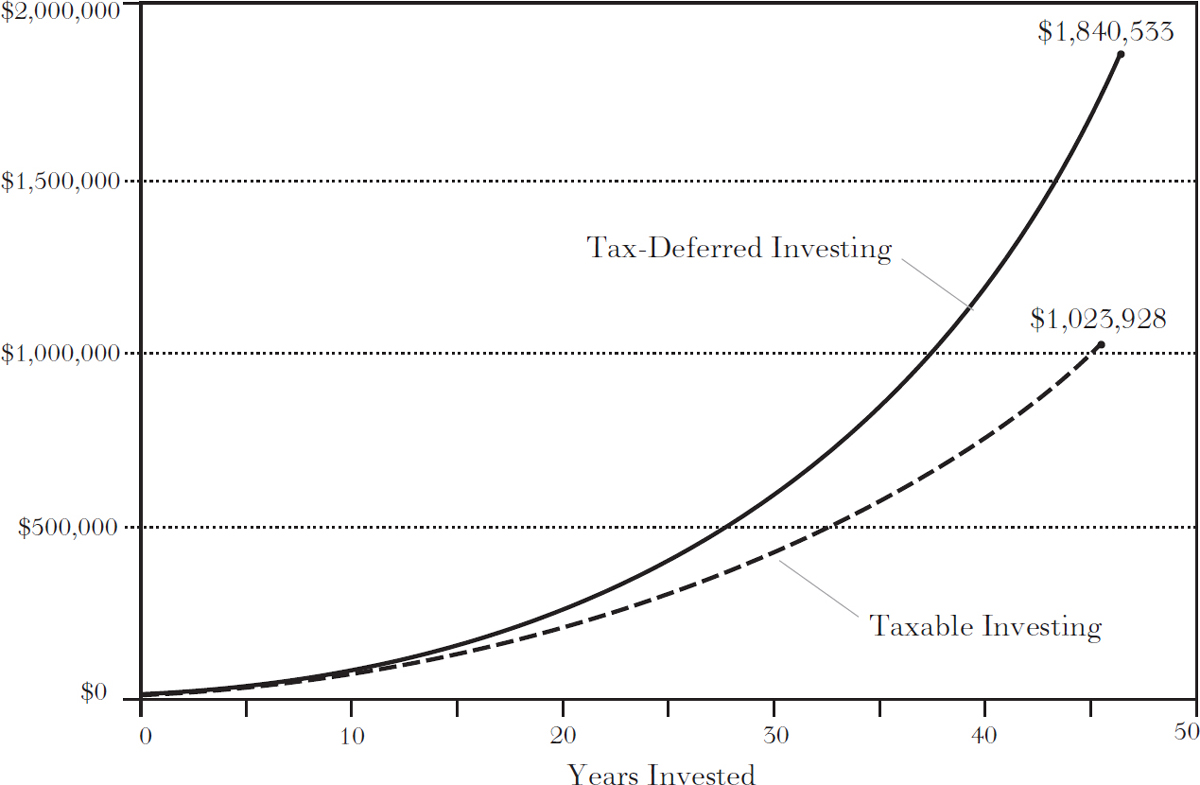

Let’s start with the simplest form of retirement plan, a straightforward Individual Retirement Account (IRA). In 2022, you could take $6,000 per year and invest it in some investment vehicle such as a mutual fund and, for people with moderate incomes, deduct the entire $6,000 from income. (Individuals who earn relatively high incomes cannot take an initial tax deduction, but they still get all the other tax advantages described below.) If you are in the 28 percent tax bracket, the contribution really costs you only $4,320 since the tax deduction saves you $1,680 in tax. You can think of it as having the government subsidize your savings account. Now suppose your investment earns 7 percent per year, and you continue to put $6,000 per year into the account for forty-five years. No taxes whatsoever are paid on the earnings from funds deposited in an IRA. The investor who saves through an IRA has a final value of more than $1.8 million, whereas the same contributions without the benefit of an IRA (where all the earnings are taxed at 28 percent each year) total just over $1 million. Even after paying taxes at 28 percent on what you withdraw from the IRA (and in retirement you might even be in a lower tax bracket), you end up with considerably more money. The following chart shows the dramatic advantage of investing through a tax-advantaged plan.

THE ADVANTAGE OF INVESTING THROUGH AN IRA TAX-DEFERRED VS. TAXABLE INVESTING OF $6,000 A YEAR

Source: Adapted from John J. Brennan, Straight Talk on Investing.

This chart compares the final values of two hypothetical accounts, one tax-deferred and one taxable. In both accounts, the investors contributed $6,000 annually for forty-five years and earned pre-tax annual returns of 7 percent after expenses.

For those individuals who neglected to save early in life and must now play catch-up, the limits are $7,000 for those over age 50.

Investors may also choose another form of individual retirement account called a Roth IRA. The traditional IRA offers “jam today” in the form of an immediate tax deduction (provided your income is low enough to make you eligible). Once in the account, the money and its earnings are taxed only when taken out at retirement. The Roth IRA offers “jam tomorrow”—you don’t get an up-front tax deduction, but your withdrawals (including investment earnings) are completely tax-free. In addition, you can Roth and roll. You can roll your regular IRA into a Roth IRA if your income is below certain thresholds. You will need to pay tax on all the funds converted, but then neither future investment income nor withdrawals at retirement will be taxed. Moreover, there are no lifetime minimum distribution requirements for a Roth IRA, and contributions can continue to be made after age seventy and a half. Thus, significant amounts can be accumulated tax-free for the benefit of future generations.

The decision of which IRA is best for you and whether to convert can be a tough call. Fortunately, the financial services industry offers free software that lets you analyze whether or not conversion makes sense for you. Many mutual-fund companies and brokers have Roth analyzers that are reasonably easy to use. If you are close to retirement and your tax bracket is likely to be lower in retirement, you probably shouldn’t convert, especially if conversion will push you into a higher bracket now. On the other hand, if you are far from retirement and are in a lower tax bracket now, you are very likely to come out well ahead with a Roth IRA. If your income is too high to allow you to take a tax deduction on a regular IRA but low enough to qualify for a Roth, then there is no question that a Roth is right for you, since your contribution is made after tax in any event.

A variety of pension plans are available from your employer. In addition, self-employed people can set up plans for themselves.

401(k) and 403(b) Pension Plans. Check whether your employer has a pension profit-sharing plan such as a 401(k), available from most corporate employers, or a 403(b), available from most educational institutions. These are perfect vehicles for saving and investing since the money gets taken out of your salary before you even see it. Moreover, many employers match some portion of the employee’s contribution so that every dollar saved gets multiplied. As of 2022, up to $20,500 per year can be contributed to these plans, and the contributions do not count as taxable income. For people over fifty, some of whom may need to play catch-up, contribution limits for 2022 were $27,000 per year.

Self-Employed Plans. For self-employed people, Congress has created the SEP IRA. All self-employed individuals—from accountants to Avon ladies, barbers to real estate brokers, doctors to decorators—are permitted to establish such a plan, to which they can contribute as much as 25 percent of their income, up to $61,000 annually, as of 2022. If you moonlight from your regular job, you can establish a SEP IRA for the income you earn on the side. The money paid into a SEP IRA is deductible from taxable income, and the earnings are not taxed until they are withdrawn. The plan is self-directed, which means the choice of how to invest is up to you. Any of the mutual-fund companies that I list in the Random Walker’s Address Book can do all the necessary paperwork for you.

Millions of taxpayers are currently missing out on what is one of the truly good deals around. My advice is to save as much as you can through these tax-sheltered means. Use up any other savings you may have for current living expenses, if you must, so you can contribute the maximum allowed.

Saving for College: As Easy as 529

“529” college savings accounts allow parents and grandparents to give gifts to children that can later be used for college education. Named after the provision of the tax code that sanctioned them, the gifts can be invested in stocks and bonds, and no federal taxes will be imposed on the investment earnings as long as the withdrawals are made for qualified higher education purposes. Moreover, as of 2022, the plans allow an individual donor to contribute as much as $80,000 to a 529 plan without gift taxes and without reducing estate tax credits. For couples, the amount doubles to $160,000. If you have kids or grandchildren who plan to go to college and you can afford to contribute to a 529 plan, the decision to establish such a plan is a no-brainer.

Are there pitfalls to avoid? You bet. Most salespeople pushing these plans receive hefty commissions that eat into investment returns. Be an educated consumer and contact a company such as Vanguard for a no-load, low-expense alternative. While it’s always nice to stiff the tax man, some high-expense 529 plans could end up shortchanging you. Also note that 529 plans are sanctioned by individual states, and some states allow you to take a tax deduction on your state income tax return for at least part of your contribution. Thus, if you live in such a state, you will want to get a plan from that state. If your state does not allow a tax deduction, choose a plan from a low-expense state such as Utah. Moreover, if you don’t use the proceeds of 529 plans for qualified education expenses (including midcareer retooling or postretirement education), withdrawals are not only subject to income tax but also carry a 10 percent penalty.

Keep in mind that colleges are likely to consider 529 assets in determining need-based financial aid. Thus, if parents believe they will be eligible for financial aid when their child goes to college, they could be better off keeping the assets in their own names or, better still, in the names of the child’s grandparents. Of course, if you won’t qualify for need-based aid in any case, by all means establish a low-expense 529.*

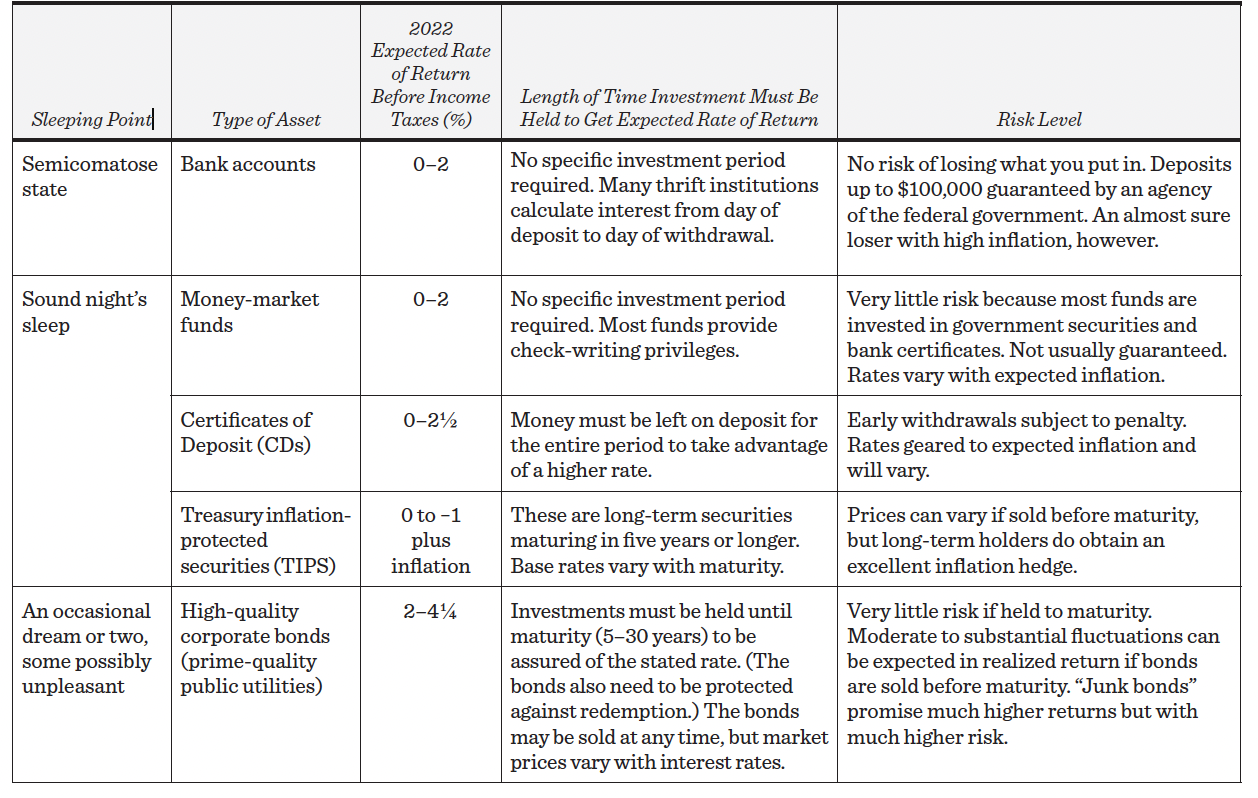

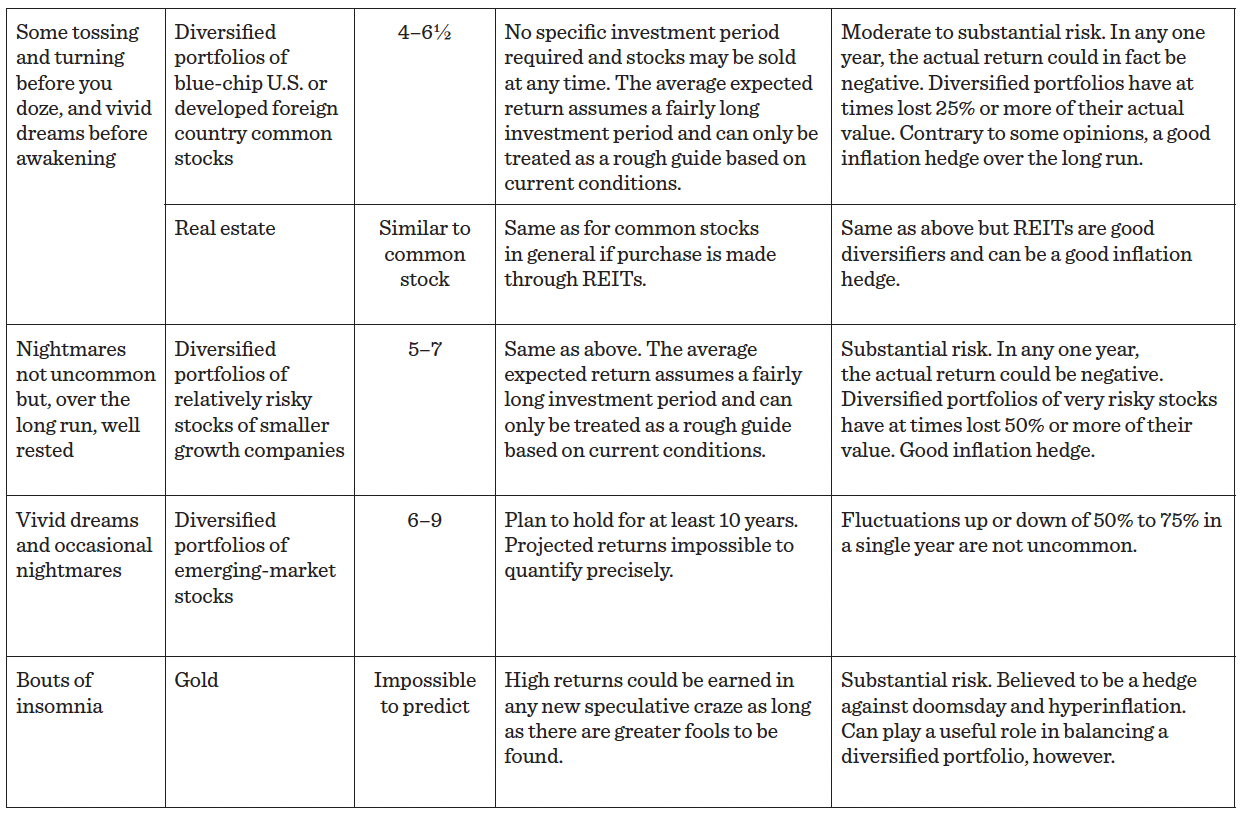

THE SLEEPING SCALE OF MAJOR INVESTMENTS

EXERCISE 5: MAKE SURE THE SHOE FITS: UNDERSTAND YOUR INVESTMENT OBJECTIVES

Determining clear goals is a part of the investment process that too many people skip, with disastrous results. You must decide at the outset what degree of risk you are willing to assume and what kinds of investments are most suitable to your tax bracket. The securities markets are like a large restaurant with a variety of menu choices suitable for different tastes and needs. Just as there is no one food that is best for everyone, so there is no one investment that is best for all investors.

We would all like to double our capital overnight, but how many of us can afford to see half our capital disintegrate just as quickly? J. P. Morgan once had a friend who was so worried about his stock holdings that he could not sleep at night. The friend asked, “What should I do about my stocks?” Morgan replied, “Sell down to the sleeping point.” He wasn’t kidding. Every investor must decide the trade-off he or she is willing to make between eating well and sleeping well. The decision is up to you. High investment rewards can only be achieved by accepting substantial risk. Finding your sleeping point is one of the most important investment steps you must take.

To help raise your investment consciousness, I’ve prepared a sleeping scale on investment risk (see pages 304–5) and expected rate of return. At the stultifying end of the spectrum are a variety of short-term investments such as bank accounts and money-market funds. If this is your sleeping point, you’ll be interested in the information in Exercise 3.

Treasury inflation-protected securities (TIPS) come next in the safety scale. These bonds promise a low (or during the early 2020s a negative) guaranteed rate that is augmented each year by the rate of increase of the consumer price index. Because they are long-term bonds, they can fluctuate in price with changes in real interest rates (stated interest rates reduced by the rate of inflation). But if held to maturity, they are guaranteed to preserve real purchasing power. In Exercise 7, I’ll discuss the advantages of having a small portion of your portfolio invested in these bonds.

Corporate bonds are somewhat riskier, and some dreams will start intruding into your sleep pattern if you choose this form of investment. Should you sell before then, your return will depend on the level of interest rates at the time of sale. If interest rates rise, your bonds will fall to a price that makes their yield competitive with new bonds offering a higher stated interest rate. Your capital loss could be enough to eat up a whole year’s interest—or even more. On the other hand, if interest rates fall, the price of your bonds will rise. If you sell prior to maturity, your actual yearly return could vary considerably, and that is why bonds are riskier than short-term instruments, which carry almost no risk of principal fluctuation. Generally, the longer a bond’s term to maturity, the greater the risk and the greater the resulting yield.† You will find some useful information on how to buy bonds in Exercise 7.

No one can say for sure what the returns on common stocks will be. But the stock market is like a gambling casino where the odds are rigged in favor of the players. Although stock prices do plummet, as they did so disastrously in the early 2000s as well as 2007 and early 2020 at the start of the COVID-19 pandemic, the overall return during the entire twentieth century was about 9 percent per year, including both dividends and capital gains. At their elevated prices in early 2022, I believe that a portfolio of domestic common stocks will have a 4 to 6½ percent long-run return, somewhat lower than the annual rates of return during the twentieth century. Comparable returns are likely from the major companies in developed foreign markets. The actual yearly return in the future can and probably will deviate substantially from this target—in down years you may lose as much as 25 percent or more. Can you stand the sleepless nights in the bad years?

How about dreams in full color with quadraphonic sound? You may want to choose a portfolio of somewhat riskier (more volatile) stocks, like those in aggressive smaller-company mutual funds. These are the stocks in younger companies in newer technologies, where the promise of greater growth exists. Such companies are likely to be more volatile, and these issues can easily lose half of their value in a bad market year. But your average future rate of return for the twenty-first century could be 5 to 7 percent per year. Portfolios of smaller stocks have tended to outperform the market averages by small amounts. If you have no trouble sleeping during bear markets, and if you have the staying power to stick with your investments, an aggressive common-stock portfolio may be just right for you. Even greater returns, as well as greater market swings, are likely from portfolios of stocks from many fast-growing emerging markets.

Commercial real estate has been an unattainable investment for many individuals. Nevertheless, the returns from real estate have been quite generous, similar to those from common stocks. I’ll argue in Exercise 6 that individuals who can afford to buy their own homes are well advised to do so. I’ll also show that it is much easier today for individuals to invest in commercial real estate. I believe that real estate investment trusts (REITs) deserve a position in a well-diversified investment portfolio.

I realize that my table slights gold and omits art objects, venture capital, hedge funds, commodities, cryptocurrencies, and other more exotic investment possibilities. Many of these have done very well and can serve a useful role in balancing a well-diversified portfolio of paper assets. Because of their substantial risk, and thus extreme volatility, it is impossible to predict their rates of return; Exercise 8 reviews them in greater detail.

In all likelihood, your sleeping point will be greatly influenced by the way a loss would affect your financial survival. That is why the typical “widow in ill health” is often viewed as unable to take on much risk. The widow has neither the life expectancy nor the ability to earn, outside her portfolio, the income she would need to recoup losses. Any loss of capital and income will immediately affect her standard of living. At the other end of the spectrum is the “aggressive young businesswoman.” She has both the life expectancy and the earning power to maintain her standard of living in the face of any financial loss. Your stage in the “life cycle” is so important that I have devoted chapter 14 to this determinant of how much risk is appropriate for you.

In addition, your psychological makeup will influence the degree of risk you should assume. One investment adviser suggests that you consider what kind of Monopoly player you once were (or still are). Were you a plunger? Did you construct hotels on Boardwalk and Park Place? True, the other players seldom landed on your property, but when they did, you could win the whole game in one fell swoop. Or did you prefer the steadier but moderate income from the orange monopoly of St. James Place, Tennessee Avenue, and New York Avenue? The answers to these questions may give you some insight into your psychological makeup with respect to investing. It is critical that you understand yourself. Perhaps the most important question to ask yourself is how you felt during a period of sharply declining stock markets. If you became physically ill and even sold out all your stocks rather than staying the course with a diversified investment program, then a heavy exposure to common stocks is not for you.

A second key step is to review how much of your investment return goes to Uncle Sam and how much current income you need. Check last year’s income tax form (1040) and the taxable income you reported for the year. For those in a high marginal tax bracket (the rate paid on the last dollar of income), there is a substantial tax advantage from municipal (tax-exempt) bonds. If you are in a high tax bracket, with little need for current income, you will prefer bonds that are tax-exempt and stocks that have low dividend yields but promise long-term capital gains (on which taxes do not have to be paid until gains are realized—perhaps never, if the stocks are part of a bequest). On the other hand, if you are in a low tax bracket and need high current income, you should prefer taxable bonds and high-dividend-paying common stocks so that you don’t have to incur the transactions charges involved in selling off shares periodically to meet income needs.

The two steps in this exercise—finding your risk level, and identifying your tax bracket and income needs—seem obvious. But it is incredible how many people go astray by mismatching the types of securities they buy with their risk tolerance and their income and tax needs. The confusion of priorities so often displayed by investors is not unlike that exhibited by a young woman whose saga was recently written up in a London newspaper:

RED FACES IN PARK

London, Oct. 30

Secret lovers were locked in a midnight embrace when it all happened.

Wedged into a tiny two-seater sports car, the near-naked man was suddenly immobilized by a slipped disc, according to a doctor writing in a medical journal here.

Trapped beneath him his desperate girlfriend tried to summon help by sounding the hooter button with her foot. A doctor, ambulance men, firemen and a group of interested passers-by quickly surrounded the couple’s car in Regents Park.

Dr. Brian Richards of Kent said: “The lady found herself trapped beneath 200 pounds of a pain-racked, immobile man.

“To free the couple, firemen had to cut away the car frame,” he added.

The distraught girl, helped out of the car and into a coat, sobbed: “How am I going to explain to my husband what has happened to his car?”

—Reuters

Investors are often torn by a similar confusion of priorities. You can’t seek safety of principal and then take a plunge with investment into the riskiest of common stocks. You can’t shelter your income from high marginal tax rates and then lock in returns of 6 percent from high-yield taxable corporate bonds, no matter how attractive these may be. Yet the annals of investment counselors are replete with stories of investors whose security holdings are inconsistent with their investment goals.

EXERCISE 6: BEGIN YOUR WALK AT YOUR OWN HOME—RENTING LEADS TO FLABBY INVESTMENT MUSCLES

Remember Scarlett O’Hara? She was broke at the end of the Civil War, but she still had her beloved plantation, Tara. A good house on good land keeps its value no matter what happens to money. As long as the world’s population continues to grow, the demand for real estate will be among the most dependable inflation hedges.

Although the calculation is tricky, the long-run returns on residential real estate have been quite generous. We did have a bubble in single-family home prices during 2007 and 2008. By the second decade of the 2000s, however, home prices returned to “normal.” Again there was some froth in the market in 2021, as many people decided to leave crowded cities, but supply of new homes began to rise robustly. You should be aware that the real estate market is less efficient than the stock market. Hundreds of knowledgeable investors study the worth of every common stock. Only a handful of prospective buyers assess the worth of a particular property. Hence, individual pieces of property are not always appropriately priced. Finally, real estate returns seem to be higher than stock returns during periods when inflation is accelerating, but do less well during periods of disinflation. In sum, real estate has proved to be a good investment providing generous returns and excellent inflation-hedging characteristics.

The natural real estate investment for most people is the single-family home or the condominium. You have to live somewhere, and buying has several tax advantages over renting. Interest on up to $750,000 in mortgage debt on new home purchases was deductible from taxes in 2021, as were property taxes up to $10,000. Also, realized gains in the value of your house, up to $500,000 for married couples, are excluded from taxation. In addition, ownership of a house is a good way to force yourself to save, and a house provides enormous emotional satisfaction.

You may also wish to consider ownership of commercial real estate through the medium of real estate investment trusts (REITs, pronounced “reets”). Properties from apartment houses to office buildings and shopping malls have been packaged into REIT portfolios and managed by professional real estate operators. The REITs themselves are like any other common stock and are actively traded on the major stock exchanges. This has afforded an excellent opportunity for individuals to add commercial real estate to their investment portfolios.

If you want to move your portfolio toward terra firma, I strongly suggest you invest some of your assets in REITs. There are many reasons why they should play a role in your investment program. First, ownership of real estate has produced comparable rates of return to common stocks and good dividend yields. Equally important, real estate is an excellent vehicle to provide the benefits of diversification described in chapter 8. Real estate returns have often exhibited only a moderate correlation with other assets, thereby reducing the overall risk of an investment program. Moreover, real estate has been a dependable hedge against inflation.

Unfortunately, the job of sifting through the hundreds of outstanding REITs is a daunting one. Moreover, a single-equity REIT is unlikely to provide the necessary diversification across property types and regions. Individuals could stumble badly by purchasing the wrong REIT. Now, however, investors have a rapidly expanding group of real estate mutual funds that are more than willing to do the job for them. The funds cull through the available offerings and put together a diversified portfolio of REITs, ensuring that a wide variety of property types and regions are represented. Moreover, investors have the ability to liquidate their fund holdings whenever they wish. There are also low-expense REIT index funds (listed in the Address Book), and I believe these funds will continue to produce the best net returns for investors.

EXERCISE 7: HOW TO INVESTIGATE A PROMENADE THROUGH BOND COUNTRY

Let’s face it, from World War II until the early 1980s, bonds were a lousy place to put your money. Inflation ate away at the real value of the bonds with a vengeance. For example, savers who bought U.S. savings bonds for $18.75 in the early 1970s and redeemed them five years later for $25 found, much to their dismay, that they had actually lost real purchasing power. The trouble was that, although the $18.75 invested in such a bond five years before might have filled one’s gas tank twice, the $25 obtained at maturity did not even fill it once. In fact, an investor’s real return was negative, as inflation had eroded purchasing power faster than interest earnings were compounding. Small wonder that many investors view the bond as an unmentionable four-letter word.

Bonds were a poor investment until the early 1980s because the interest rates they carried did not offer adequate inflation protection. But bond prices adjusted to give investors excellent returns over the next forty years. Moreover, bonds proved to be excellent diversifiers with low or negative correlation with common stocks from 1980 through 2021. In my view, there are four kinds of bond purchases that you may want to consider: (1) zero-coupon bonds (which allow you to lock in yields for a predetermined length of time); (2) no-load bond mutual funds (which permit you to buy shares in bond portfolios); (3) tax-exempt bonds and bond funds (for those in high tax brackets); and (4) U.S. Treasury inflation-protected securities (TIPS). But their attractiveness for investment varies considerably with market conditions. And with the low interest rates of the early 2020s, investors must approach the bond market with considerable caution.

Zero-Coupon Bonds Can Be Useful to Fund Future Liabilities

These securities are called zero coupons or simply zeros because owners receive no periodic interest payments, as they do in a regular interest-coupon-paying bond. Instead, these securities are purchased at discounts from their face value (for example, 75 cents on the dollar) and gradually rise to their face or par values over the years. If held to maturity, the holder is paid the full stated amount of the bond. These securities are available on maturities ranging from a few months to over twenty years. They are excellent vehicles for putting money aside for required expenditures on specific future dates.

The principal attraction of zeros is that the purchaser is faced with no reinvestment risk. A zero-coupon Treasury bond guarantees an investor that his or her funds will be continuously reinvested at the yield-to-maturity rate.

The main disadvantage of zeros is that the Internal Revenue Service requires that taxable investors declare annually as income a pro rata share of the dollar difference between the purchase price and the par value of the bond. This is not required, however, for investors who hold zeros in tax-deferred retirement plans.

Two warnings are in order. Some brokers will charge small investors fairly large commissions for the purchase of zero-coupon bonds in small denominations. In addition, you should know that redemption at face value is assured only if you hold the bonds to maturity. In the meantime, prices can be highly variable as interest rates change.

No-Load Bond Funds Can Be Appropriate Vehicles for Individual Investors

Open-end bond (mutual) funds give some of the long-term advantages of the zeros but are much easier and less costly to buy or sell. Those that I have listed in the Address Book all invest in long-term securities. Although there is no guarantee that you can reinvest your interest at constant rates, these funds do offer long-run stability of income and are particularly suitable for investors who plan to live off their interest income.

Because bond markets tend to be at least as efficient as stock markets, I recommend low-expense bond index funds. Bond index funds and ETFs, which just buy and hold a broad variety of bonds, generally outperform actively managed bond funds. In no event should you ever buy a load fund with a commission fee. There’s no point in paying for something if you can get it free.

The Address Book lists several types of funds: those specializing in corporate bonds, those that buy a portfolio of GNMA mortgage-backed bonds, those investing in tax-exempt bonds (which I will discuss in the next section), as well as some riskier high-yield funds appropriate for investors willing to accept extra risk in return for higher expected returns.

Tax-Exempt Bonds Are Useful for High-Bracket Investors

If you are in a high tax bracket, taxable money funds, zeros, and taxable bond funds may be suitable only within your retirement plan. Otherwise, you need the tax-exempt bonds issued by state and local governments and by various governmental authorities, such as port authorities or toll roads. The interest from these bonds doesn’t count as taxable income on your federal tax form, and bonds from the state in which you live are typically exempt from any state income taxes.

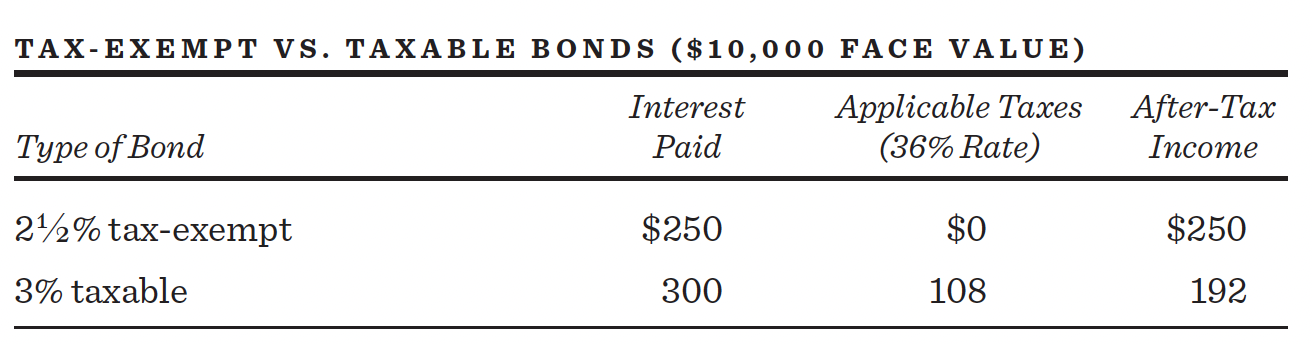

During 2021, good-quality long-term corporate bonds were yielding about 3 percent, and tax-exempt issues of comparable quality yielded about 2½ percent. Suppose your tax bracket (the rate at which your last dollar of income is taxed) is about 36 percent, including both federal and state taxes. The following table shows that the after-tax income is $58 higher on the tax-exempt security, which is clearly the better investment for a person in your tax bracket. Even if you are in a lower tax bracket, tax-exempts may still pay, depending on the exact yields available in the market when you make your purchase. Of course in 2021 neither bond provided a real return since the inflation rate was greater than 2½ percent.

If you buy bonds directly (rather than indirectly through mutual funds), I suggest that you buy new issues rather than already outstanding securities. New-issue yields are usually a bit sweeter than the yields of seasoned outstanding bonds, and you avoid paying transactions charges on new issues. I think you should keep your risk within reasonable bounds by sticking with issues rated at least A by Moody’s and Standard & Poor’s rating services. Also consider so-called AMT bonds. These bonds are subject to the alternative minimum (income) tax and, therefore, are not attractive to individuals who have sheltered a significant part of their income from tax. But if you are not subject to the alternative minimum tax, you can get some extra yield from holding AMT bonds.

There is one nasty “heads I win, tails you lose” feature of bonds. If interest rates go up, the price of your bonds will go down. But if interest rates go down, the issuer can often “call” the bonds away from you (repay the debt early) and then issue new bonds at lower rates. To protect yourself, make sure that your long-term bonds have a ten-year call-protection provision that prevents the issuer from refunding the bonds at lower rates.

For some good tax-exempt bond funds, consult the list in the Address Book. If you have substantial funds to invest in tax-exempts, however, I see little reason for you to make your tax-exempt purchases through a fund and pay the management fees involved. If you confine your purchases to high-quality bonds, including those guaranteed by bond insurance, there is little need for you to diversify, and you’ll earn more interest. If you have just a few thousand dollars to invest, however, a fund will provide convenient liquidity and diversification. There are also funds that confine their purchases to the bonds of a single state so that you can avoid both state and federal income taxes.

Hot TIPS: Inflation-Protected Bonds

We know that unanticipated inflation is devastating to bondholders. Inflation tends to increase interest rates, and as they go up, bond prices fall. And there’s more bad news: Inflation also reduces the real value of a bond’s interest and principal payments. Now a lead shield is available to investors in the form of Treasury inflation-protected securities (TIPS). These securities are immune to the erosion of inflation if held to maturity and guarantee investors that their portfolios will retain their purchasing power. Long-term TIPS paid a basic interest rate of about 1 percent during the 2010s. But in contrast to old-fashioned Treasuries, the interest payment is based on a principal amount that rises with the consumer price index (CPI). If the price level were to rise 3 percent next year, the $1,000 face value of the bond would increase to $1,030 and the semiannual interest payment would increase as well. When the TIPS mature, the investor gets a principal payment equal to the inflation-adjusted face value at that time. Thus, TIPS provide a guaranteed real rate of return and a repayment of principal in an amount that preserves its real purchasing power.

No other financial instrument available today offers investors as reliable an inflation hedge. TIPS also are great portfolio diversifiers. When inflation accelerates, TIPS will offer higher nominal returns, whereas stock and bond prices are likely to fall. Thus, TIPS have low correlations with other assets and are uniquely effective diversifiers. They provide an effective insurance policy for the white-knuckle crowd.

TIPS do have a nasty tax feature, however, that limits their usefulness. Taxes on TIPS returns are due on both the coupon payment and the increase in principal amount reflecting inflation. The problem is that the Treasury does not pay out the increase in principal until maturity. If inflation were high enough, the small coupon payments might be insufficient to pay the taxes and the imbalance would worsen at higher rates of inflation. Thus, TIPS are far from ideal for taxable investors and are best used only in tax-advantaged retirement plans. As inflation began to accelerate during the early 2020s, the base yield on TIPS became negative. During late 2021, 10-year TIPS sold at a base rate of minus 1 percent, while the inflation rate had risen to about 6 percent.

U.S. Treasury I Bonds: The Best Alternative for Individuals

There is an excellent alternative available for individual investors to standard TIPS: U.S. Treasury I Savings Bonds. The bonds pay a fixed rate for the life of the bond, plus the annualized CPI inflation rate, which is adjusted twice a year. These I Bonds paid a total interest rate of 7.12 in early 2022, well in excess of any other safe yield obtainable. The interest on an I Bond is deferred until the bond matures or is cashed in, and it is exempt from state and local income taxes. If you use the proceeds for qualified higher education expenses, the interest is exempt from federal taxes as well. The bonds mature in 30 years, but you can cash them in after one year (with a small penalty). After holding them for five years, there is no redemption penalty. The maximum purchase allowed is $10,000 each year for each social security recipient. Thus, a couple could purchase $20,000 of these I Bonds. In addition, one could obtain an extra $5,000 bond by using funds from an income tax refund. Available at the U.S. Treasury website (treasurydirect.gov), they are Uncle Sam’s best deal for risk-averse investors.

Should You Be a Bond-Market Junkie?

Is the bond market immune to the maxim that investment risk and reward are related? Not at all! During most periods, so-called junk bonds (lower credit quality, higher-yielding bonds) have given investors a net rate of return up to 3 percentage points higher than the rate that could be earned on U.S. Treasury bonds. Thus, even if 1 percent of the lower-grade bonds defaulted on their interest and principal payments and produced a total loss, a diversified portfolio of low-quality bonds would still produce net returns higher than those available from Treasury bonds. Many investment advisers have therefore recommended well-diversified portfolios of high-yield bonds as sensible investments.

There is, however, another school of thought that advises investors to “just say no” to junk bonds. Most junk bonds have been issued as a result of a massive wave of corporate mergers, acquisitions, and leveraged (mainly debt-financed) buyouts. The junk-bond naysayers point out that lower credit bonds are most likely to be serviced in full only during good times in the economy. But watch out if the economy falters.

So what’s a thoughtful investor to do? The answer depends in part on how well you sleep at night when you assume substantial investment risk. High-yield or junk-bond portfolios are not for insomniacs. Even with diversification, there is substantial risk in these investments. Moreover, they are not for investors who depend solely on interest payments as their major source of income. And they are certainly not for any investors who do not adequately diversify their holdings. However, at least historically, the gross-yield premium from junk bonds has more than compensated for actual default experience.

There are many foreign countries whose bond yields are higher than those in the United States. This is particularly true in some emerging markets. Conventional wisdom has usually recommended against bonds from emerging markets, citing their high risk and poor quality. But many emerging economies have lower debt-to-GDP ratios and better government fiscal balances than are found in the developed world. The emerging economies are also growing faster. Hence, a diversified portfolio of higher-yielding foreign bonds, including those from emerging markets, can be a useful part of a fixed-income portfolio for risk-tolerant investors.

Low interest rates present a daunting challenge for bond investors. All the developed countries of the world are burdened with excessive amounts of debt. Like the United States, governments around the world are having an extraordinarily difficult time reining in entitlement programs in the face of aging populations.

The easier path for the U.S. and other governments is to keep interest rates artificially low as the real burden of the debt is reduced and the debt is restructured on the backs of the bondholders. We have seen this movie before. At the end of World War II, the United States deliberately kept interest rates at very low levels to help service the debt that had accumulated during the war. By doing so, the United States reduced its debt-to-GDP ratio from 122 percent in 1946 to 33 percent in 1980. But it was achieved at the expense of bondholders. This is what is meant by the term “financial repression.”

One technique to deal with the problem is to use an equity dividend substitution strategy for some portion of what in normal times would have been a bond portfolio. Portfolios of relatively stable dividend growth stocks have yields much higher than the bonds of the same companies and allow the possibility of growth in the future. An example of the sort of company in such a portfolio is Verizon. Verizon’s 15-year bonds yielded about 3¼ percent in late 2021. Its common stock has a dividend yield of 4⅜ percent, and the dividend has been growing over time. Retired people who live off dividends and interest will be better rewarded with Verizon stock than with its bonds. And portfolios of dividend growth stocks may be no more volatile than an equivalent portfolio of bonds of the same companies. During periods of financial repression, the standard recommendations regarding bonds need to be fine-tuned and a partial substitution of stocks for bonds in that part of the portfolio designed for lower risk may be appropriate.

EXERCISE 8: TIPTOE THROUGH THE FIELDS OF GOLD, COLLECTIBLES, AND OTHER INVESTMENTS

In previous editions of this book I took different positions on whether gold belongs in a well-diversified portfolio. At the start of the 1980s, as gold had risen in price past $800 an ounce, I took a quite negative view of gold. Twenty years later, at the start of the new millennium, with gold selling in the $200s, I became more positive. Today, with gold selling at over $1,800 an ounce, I find it hard to be enthusiastic. But there could be a modest role for gold in your portfolio. Returns from gold tend to be very little correlated with the returns from paper assets. Hence, even modest holdings (say, 5 percent of the portfolio) can help an investor reduce the variability of the total portfolio. And if high inflation were to be persistent, gold would likely produce acceptable returns. But prudence suggests—at best—a limited role for gold as a vehicle for obtaining broader diversification.

What about diamonds, which are often described as everybody’s best friend? They pose enormous risks and disadvantages for individual investors. One must remember that buying diamonds involves large commission costs. It’s also extraordinarily hard for an individual to judge quality, and I can assure you that the number of telephone calls you get from folks wishing to sell diamonds will greatly exceed the calls from those who want to buy them.

Another popular current strategy is investment in collectibles. Thousands of salesmen are touting everything from Renoir to rugs, Tiffany lamps to rare stamps, Art Deco to airsick bags. And eBay has made buying and selling collectibles much more efficient. I think there’s nothing wrong in buying things you can love—and God knows people do have strange tastes—but my advice is to buy those things because you love them, not because you expect them to appreciate in value. Don’t forget that fakes and forgeries are common. A portfolio of collectibles also often requires hefty insurance premiums and endless maintenance charges—so you are making payments instead of receiving dividends or interest. To earn money collecting, you need great originality and taste. In my view, most people who think they are collecting profit are really collecting trouble.

Even if you are fortunate enough to buy a piece of art that turns out to be a major masterpiece, you still may not have made a smart investment. In November 2017, the painting Salvator Mundi, attributed to Leonardo da Vinci, sold at a Christie’s auction for more than $450 million. Jason Zweig, a financial columnist for the Wall Street Journal, estimated that the painting sold for the equivalent of about half a million dollars during the early 1500s. The ability to say today that “I own a Leonardo painting” may be priceless. But as a financial investment it returned a paltry 1.35 percent from 1519 to 2018.

© George Price / New Yorker / Conde Nast

Another popular instrument these days is the commodities futures contract. You can buy not only gold but also contracts for the delivery of a variety of commodities, from grains to metals as well as different currencies. It’s a fast market where professionals can benefit greatly, but individuals who don’t know what they are doing can easily get clobbered. My advice to the nonprofessional investor: Don’t go against the grain.

I would also steer clear of hedge-fund and private-equity and venture-capital funds. These can be great moneymakers for the fund managers who pocket large management fees and 20 percent of the profits, but individual investors are unlikely to benefit. The average performance of these funds is deeply disappointing. True, the best funds have done quite well, but unless you are an institutional investor who has established a clearly preferential position, your chance of investing with the best is realistically zero. Ignore these exotics—they are not for you.

If you feel tempted by the allure of hedge funds, remember the famous bet of Warren Buffett. At the end of 2007, Buffett offered any takers the following one-million-dollar wager: “I’ll bet you can’t select five bundles of hedge funds that will outperform the Standard and Poor’s 500-Stock Index over the next decade.” The winner of the bet could select his favorite charity to receive the proceeds. Protégé Partners took up the challenge and selected five funds that invested in a portfolio of hedge funds. When the bet ended on the last day of 2017, the S&P 500 Index Fund had returned 7.1 percent per year. The basket of hedge funds returned 2.2 percent annually. The real winner was Buffett’s charity Girls, Inc., an organization that provides after-school care and summer programs for girls between five and eighteen years old. The losers were those who invested in portfolios of high-cost hedge funds. Finally, I would avoid cryptocurrencies, non-fungible tokens, or whatever else has attracted the attention of the social networks. These are for gamblers. They do not belong in retirement portfolios.

EXERCISE 9: REMEMBER THAT INVESTMENT COSTS ARE NOT RANDOM; SOME ARE LOWER THAN OTHERS

Many brokers today will execute your stock orders at zero standard commission rates, especially if you are willing to trade online. Trading stocks online is easy to do on your laptop or phone. But let me warn you, few investors who try to trade in and out of stocks each day make profits. Don’t let zero commission rates seduce you into becoming one of the legion of unsuccessful former day traders.

While we are on the subject of commission costs, you should be aware of a Wall Street innovation called the “wrap account.” For a single fee, your broker obtains the services of a professional money manager, who then selects for you a portfolio of stocks, bonds, and perhaps real estate. Brokerage commissions and advisory fees are “wrapped” into the overall fee. The costs involved in wrap accounts are extremely high. Annual fees can be up to 3 percent per year, and there may be additional execution fees and fund expenses if the manager uses mutual funds or REITs. With those kinds of expenses, it will be virtually impossible for you to beat the market. My advice here is: Avoid taking the wrap.

Remember also that costs matter when buying mutual funds or ETFs. There is a strong tendency for those funds that charge the lowest fees to the investor to produce the best net returns. The fund industry is one where you actually get what you don’t pay for. Of course, the quintessential low-cost funds are index funds, which tend to be very tax efficient as well.

There is much about investing you cannot control. You can’t do anything about the ups and downs of the stock and bond markets. But you can control your investment costs. And you can organize your investments to minimize taxes. Controlling the things you can control should play a central role in developing a sensible investment strategy.

EXERCISE 10: AVOID SINKHOLES AND STUMBLING BLOCKS: DIVERSIFY YOUR INVESTMENT STEPS

In these warm-up exercises, we have discussed a number of investment instruments. The most important part of our walk down Wall Street will take us to the corner of Broad Street—to a consideration of sensible investment strategies with respect to common stocks. A guide to this part of our walk is contained in the final three chapters, because I believe common stocks should form the cornerstone of most portfolios. Nevertheless, in our final warm-up exercise, we recall the important lesson of modern portfolio theory—the advantages of diversification.

A biblical proverb states that “in the multitude of counselors there is safety.” The same can be said of investments. Diversification reduces risk and makes it far more likely that you will achieve the kind of long-run return that meets your investment objective. Therefore, within each investment category you should hold a variety of individual issues, and although common stocks should be a major part of your portfolio, they should not be the sole investment instrument. Just remember the teary-eyed ex-Enron employees who held nothing but Enron stock in their retirement plans. When Enron went under, they lost not only their jobs but all their retirement savings as well. Whatever the investment objectives, the investor who is wise diversifies.

Recall also the sinkholes and stumbling blocks covered in chapter 10, which enumerates the lessons for investors from behavioral finance. We are all too often our own worst enemy when it comes to investing. An understanding of how vulnerable we are to our own psychology can help us avoid the common pitfalls that can make us stumble on our walk down Wall Street.

Now that you have completed your warm-up exercises, let’s take a moment for a final checkup. The theories of valuation worked out by economists and the performance recorded by the professionals lead to a single conclusion: There is no sure and easy road to riches. High returns can be achieved only through higher risk-taking (and perhaps through accepting lower liquidity).

The amount of risk you can tolerate is partly determined by your sleeping point. The next chapter discusses the risks and rewards of stock and bond investing and will help you determine the kinds of returns you should expect from different financial instruments. But the risk you can assume is also significantly influenced by your age and by the sources and dependability of your noninvestment income. Chapter 14—“A Life-Cycle Guide to Investing”—will give you a clearer notion of how to decide what portion of your capital should be placed in common stocks, bonds, real estate, and short-term investments. The final chapter presents specific stock-market strategies that will enable amateur investors to achieve results as good as or better than those of the most sophisticated professionals.

*Comprehensive information about 529 plans can be found at www.savingforcollege.com. The $80,000 contribution assumes a “5-year election.”

†This isn’t always the case. During some periods, short-term securities actually yielded more than long-term bonds. The catch was that investors could not count on continually reinvesting their short-term funds at such high rates, and later short-term rates had declined sharply. Thus, investors can reasonably expect that continual investment in short-term securities will not produce as high a return as investment in long-term bonds. In other words, there is a reward for taking on the risk of owning long-term bonds even if short-term rates are temporarily above long-term rates.