Behavioral finance is not a branch of standard finance: it is its replacement with a better model of humanity.

—Meir Statman

THUS FAR I have described stock-market theories and techniques based on the premise that investors are completely rational. They make decisions with the objective of maximizing their wealth and are constrained only by their tolerance for bearing risk. Not so, declares a new school of financial economists who came to prominence in the early part of the twenty-first century. Behavioralists believe that many (perhaps even most) stock-market investors are far from fully rational. After all, think of the behavior of your friends and acquaintances, your fellow workers and your supervisors, your parents and (dare I say) spouse (children, of course, are another matter). Do any of these people act rationally? If your answer is “no” or even “sometimes no,” you will enjoy this journey down the less than rational byways of behavioral finance.

Efficient-market theory, modern portfolio theory, and various asset-pricing relationships between risk and return all are built on the premise that stock-market investors are rational. As a whole, they make reasonable estimates of the present value of stocks, and their buying and selling ensures that the prices of stocks fairly represent their future prospects.

By now, it should be obvious that the phrase “as a whole” represents the economists’ escape hatch. That means they can admit that some individual market participants may be less than rational. But they quickly wriggle out by declaring that the trades of irrational investors will be random and therefore cancel each other out without affecting prices. And even if investors are irrational in a similar way, efficient-market theory believers assert that smart rational traders will correct any mispricings that might arise from the presence of irrational traders.

Psychologists will have none of this economic claptrap. Two in particular—Daniel Kahneman and Amos Tversky—blasted economists’ views about how investors behave and in the process are credited with fathering a whole new economic discipline, called behavioral finance.

The two argued quite simply that people are not as rational as economic models assume. Although this argument is obvious to the general public and non-economists, it took over twenty years for it to become widely accepted in academia. Tversky died in 1996, just as it was gaining increased credibility. Six years later, Kahneman won the Nobel Memorial Prize in Economic Sciences for the work. The award was particularly notable in that it was not given to an economist. Upon hearing the news, Kahneman commented, “The prize . . . is quite explicitly for joint work, but unfortunately there is no posthumous prize.”

Though the insights expounded by Kahneman and Tversky affected all social sciences dealing with the process of decision making, they had a particularly strong impact on economics departments and business schools across the country. Imagine—a whole new field in which to publish papers, give lectures for hefty fees, and write graduate theses.

While that may be all well and good for the professors and the students, what about all the other people who want to invest in stocks. How can behavioral finance help them? More to the point, what’s in it for you? Actually, quite a bit.

Behavioralists believe that market prices are highly imprecise. Moreover, people deviate in systematic ways from rationality, and the irrational trades of investors tend to be correlated. Behavioral finance then takes that statement further by asserting that it is possible to quantify or classify such irrational behavior. Basically, there are four factors that create irrational market behavior: overconfidence, biased judgments, herd mentality, and loss aversion.

Well, yes, believers in efficient markets say. But—and we believers always have a but—the distortions caused by such factors are countered by the work of arbitrageurs. This last is the fancy word used to describe people who profit from any deviation of market prices from their rational value.

In a strict sense, the word “arbitrage” means profiting from prices of the same good that differ in two markets. Suppose in New York you can buy or sell British pounds for $1.50, while in London you can trade dollars for pounds at a $2.00 exchange rate. The arbitrageur would then take $1.50 in New York and buy a pound and simultaneously sell it in London for $2.00, making a 50¢ profit. Similarly, if a common stock sold at different prices in New York and London, it would be justifiable to buy it in the cheap market and sell it in the expensive one. The term “arbitrage” is generally extended to situations where two very similar stocks sell at different valuations or where one stock is expected to be exchanged for another stock at a higher price if a planned merger between the two companies is approved. In the loosest sense of the term, “arbitrage” is used to describe the buying of stocks that appear “undervalued” and the selling of those that have gotten “too high.” In so doing, hardworking arbitrageurs can smooth out irrational fluctuations in stock prices and create an efficiently priced market.

On the other hand, behavioralists believe there are substantial barriers to efficient arbitrage. We cannot count on arbitrage to bring prices in line with rational valuation. Market prices can be expected to deviate substantially from those that could be expected in an efficient market.

The remainder of this chapter explores the key arguments of behavioral finance in explaining why markets are not efficient and why there is no such thing as a random walk down Wall Street. I’ll also explain how an understanding of this work can help protect individual investors from some systematic errors that investors are prone to.

THE IRRATIONAL BEHAVIOR OF INDIVIDUAL INVESTORS

As Part One made abundantly clear, there are always times when investors are irrational. Behavioral finance, however, says that this behavior is continual rather than episodic.

Researchers in cognitive psychology have documented that people deviate in systematic ways from rationality in making judgments amid uncertainty. One of the most pervasive of these biases is the tendency to be overconfident about beliefs and abilities and overoptimistic about assessments of the future.

One class of experiments illustrating this syndrome consists of asking a large group of participants about their competence as automobile drivers in relation to the average driver in the group or to everyone who drives a car. Driving an automobile is clearly a risky activity where skill plays an important role. Answers to this question easily reveal whether people have a realistic conception of their own skill in relationship to others. In the case of college students, 80 to 90 percent of respondents invariably say that they are more skillful, safer drivers than others in the class. As in Lake Wobegon, (almost) all the students consider themselves above average.

In another experiment involving students, respondents were asked about likely future outcomes for themselves and their roommates. They typically had very rosy views about their own futures, which they imagined to include successful careers, happy marriages, and good health. When asked to speculate about their roommates’ futures, however, their responses were far more realistic. The roommates were believed to be far more likely to become alcoholics, suffer illnesses, get divorced, and experience a variety of other unfavorable outcomes.

These kinds of experiments have been repeated many times and in several different contexts. For example, in the business management best-seller In Search of Excellence, Peters and Waterman report that a random sample of male adults were asked to rank themselves in terms of their ability to get along with others. One hundred percent of the respondents ranked themselves in the top half of the population. Twenty-five percent believed that they were in the top 1 percent of the population. Even in judging athletic ability, an area where self-deception would seem more difficult, at least 60 percent of the male respondents ranked themselves in the top quartile. Even the klutziest deluded themselves about their athletic ability. Only 6 percent of male respondents believed that their athleticism was below average.

Daniel Kahneman has argued that this tendency to overconfidence is particularly strong among investors. More than most other groups, investors tend to exaggerate their own skill and deny the role of chance. They overestimate their own knowledge, underestimate the risks involved, and exaggerate their ability to control events.

Kahneman’s tests show how well investors’ probability judgments are calibrated by asking experimental subjects for confidence intervals. He asks a question such as the following:

What is your best estimate of the value of the Dow Jones one month from today? Next pick a high value, such that you are 99% sure (but not absolutely sure) that the Dow Jones a month from today will be lower than that value. Now pick a low value, such that you are 99% sure (but no more) that the Dow Jones a month from today will be higher than that value.

If the instructions are carried out properly, the probability that the Dow will be higher (lower) than your high (low) estimate should be only 1 percent. In other words, the investor should be 98 percent confident that the Dow will be within the given range. Similar experiments have been carried out on estimates for interest rates, the rate of inflation, individual stock prices, and the like.

In fact, few investors are able to set accurate confidence intervals. Correct intervals would lead to actual outcomes being outside the predicted range only 2 percent of the time. Actual surprises do occur close to 20 percent of the time. This is what psychologists mean by overconfidence. If an investor tells you he is 99 percent sure, he would be better off assuming that he was only 80 percent sure. Such precision implies that people tend to put larger stakes on their predictions than are justified. And men typically display far more overconfidence than women, especially about their prowess in money matters.

What should we conclude from these studies? It is clear that people set far too precise confidence intervals for their predictions. They exaggerate their skills and tend to have a far too optimistic view of the future. These biases manifest themselves in various ways in the stock market.

First and foremost, many individual investors are mistakenly convinced that they can beat the market. As a result, they speculate more than they should and trade too much. Two behavioral economists, Terrance Odean and Brad Barber, examined the individual accounts at a large discount broker over a substantial period of time. They found that the more individual investors traded, the worse they did. And male investors traded much more than women, with correspondingly poorer results.

In a more recent study, Barber, Huang, Odean, and Schwarz examined the behavior of individual investors trading on the Robinhood platform. It turned out that the stocks most frequently bought by Robinhood clients had negative absolute and relative returns. These stocks lost about 5 percent over the next month relative to the market as a whole.

This illusion of financial skill may well stem from another psychological finding, called hindsight bias. Such errors are sustained by having a selective memory of success. You remember your successful investments. And in hindsight, it is easy to convince yourself that you “knew Google was going to quintuple right after its initial public offering.” People are prone to attribute any good outcome to their own abilities. They tend to rationalize bad outcomes as resulting from unusual external events. History does not move us as much as a couple of anecdotes of success. Hindsight promotes overconfidence and fosters the illusion that the world is far more predictable than it really is. The people who sell worthless financial advice may even believe that it is good advice. Steve Forbes, the longtime publisher of Forbes magazine, liked to quote the advice he received at his grandfather’s knee: “It’s far more profitable to sell advice than to take it.”

Many behavioralists believe that overconfidence in the ability to predict the future growth of companies leads to a general tendency for so-called growth stocks to be overvalued. If the exciting new computer technology or medical device company catches the public fancy, investors will usually extrapolate success and project high growth rates for the companies involved and hold such beliefs with far more confidence than is justified. The high-growth forecasts lead to higher valuations for growth stocks. But the rosy forecasts are often not realized. The earnings may fall, and so may the price-earnings multiples of the shares, which will lead to poor investment results. Overoptimism in forecasting growth for exciting companies could be one explanation for the long-term tendency of “growth” stocks to underperform “value” stocks.

I meet investors every day who are convinced that they can “control” their investment results. This is especially true of chartists who are confident that they can define the future by looking at past prices.

Larry Swedroe, in his Rational Investing in Irrational Times, provides a wonderful illustration of how hot streaks occur with much greater frequency than people believe.

Each year a statistics professor begins her class by asking each student to write down the sequential outcome of a series of one hundred imaginary coin tosses. One student, however, is chosen to flip a real coin and chart the outcome. The professor then leaves the room and returns in fifteen minutes with the outcomes waiting for her on her desk. She tells the class that she will identify the one real coin toss out of the thirty submitted with just one guess. With great persistence she amazes the class by getting it correct. How does she perform this seemingly magical act? She knows that the report with the longest consecutive streak of H (heads) or T (tails) is highly likely to be the result of the real flip. The reason is that, when presented with a question like which of the following sequences is more likely to occur, HHHHHTTTTT or HTHTHTHTHT, despite the fact that statistics show that both sequences are equally likely to occur, the majority of people select the latter “more random” outcome. They thus tend to write imaginary sequences that look much more like HHTTHTHTTT than HHHTTTHHHH.

Aside from the long-term positive direction of the stock market, streaks of excessively high stock returns do not persist—they are typically followed by lower future returns. There is reversion to the mean. Similarly, the laws of financial gravity also operate in reverse. At least for the stock market as a whole, what goes down eventually comes back up. Yet each era’s conventional wisdom typically assumes that unusually good markets will get better and unusually bad markets will get worse.

Psychologists have long identified a tendency for individuals to be fooled by the illusion that they have some control over situations where, in fact, none exists. In one study, subjects were seated in front of a computer screen divided by a horizontal line, with a ball fluctuating randomly between two halves. The people were given a device to press to move the ball upward, but they were warned that random shocks would also influence the ball so that they did not have complete control. Subjects were then asked to play a game with the object of keeping the ball in the upper half of the screen as long as possible. In one set of experiments, the device was not even attached, so the players had absolutely no control over the movements of the ball. Nevertheless, when subjects were questioned after a period of playing the game, they were convinced that they had a good deal of control over the movement of the ball. (The only subjects not under such an illusion turned out to be those who had been clinically diagnosed with severe depression.)

In another experiment, an office lottery was conducted with two identical sets of baseball cards. One set was placed in a bin from which one card was to be selected by chance. The other set was distributed to the participants. Half the participants were given a choice of which card to take, while the other half were simply given a card. Participants were told that the winner would be the person holding the card that matched the one that would be selected by chance from the bin. The individuals were then told that while all the cards had been distributed, a new player wanted to buy a card. Participants were faced with a choice—sell their cards at some negotiated price or hold on to them and hope to win. Obviously, each card had the same probability of winning. Nevertheless, the prices at which players were willing to sell their cards were systematically higher for those who chose their cards than for the group who had simply been given a card. Insights such as this led to the decision to let state lottery buyers pick their own numbers even though luck alone determines lottery winners.

It is this illusion of control that can lead investors to see trends that do not exist or to believe that they can spot a stock-price pattern that will predict future prices. In fact, despite considerable efforts to tease some form of predictability out of stock-price data, the development of stock prices from period to period is very close to a random walk, where price changes in the future are essentially unrelated to changes in the past.

Biases in judgments are compounded (get ready for some additional jargon) by the tendency of people mistakenly to use “similarity” or “representativeness” as a proxy for sound probabilistic thinking. A famous Kahneman and Tversky experiment best illustrates this “heuristic.” Subjects are shown the following description of Linda:

Linda is 31 years old, single, outspoken and very bright. She majored in philosophy. As a student, she was deeply concerned with issues of discrimination and social justice, and also participated in anti-nuclear demonstrations.

Subjects were then asked to rate the relative likelihood that eight different statements about Linda were true. Two of the statements on the list were “Linda is a bank teller” and “Linda is a bank teller and is active in the feminist movement.” Over 85 percent of subjects judged it more likely that Linda was both a bank teller and a feminist than that she was a bank teller. But this answer is a violation of a fundamental axiom of probability theory (the conjunction rule): the probability that somebody belongs to both category A and category B is less than or equal to the probability that she belongs to category A alone. Obviously, few respondents had learned much probability theory.

The description of Linda made her seem like a feminist, so being a bank teller and a feminist seems a more natural description, and thus more representative of Linda, than simply being a bank teller. This experiment has been replicated many times with naive and sophisticated subjects (including those who had backgrounds in probability but who had not studied all its nuances).

Kahneman and Tversky came up with the term “representative heuristic” to describe this finding. Its application leads to a number of other biases in judgment—for example, the underuse of base-rate probabilities. One cardinal rule of probability (Bayes’ law) tells us that our assessment of the likelihood that someone belongs to a particular group should combine “representativeness” with base rates (the percentage of the population falling into various groups). In everyday English, this means that if we see somebody who looks like a criminal (seems to represent our idea of a criminal type), our assessment of the probability that he is a criminal also requires knowledge about base rates—that is, the percentage of people who are criminals. But in experiment after experiment, subjects have been shown to underuse the knowledge of base rates when making predictions. Arcane as this all may seem, the representativeness heuristic is likely to account for a number of investing mistakes such as chasing hot funds or excessive extrapolation from recent evidence.

In general, research shows that groups tend to make better decisions than individuals. If more information is shared, and if differing points of view are considered, informed discussion of the group improves the decision-making process.

The wisdom of crowd behavior is perhaps best illustrated in the economy as a whole by the free-market price system. A variety of individual decisions by consumers and producers leads the economy to produce the goods and services that people want to buy. Responding to the forces of demand and supply, the price system guides the economy through Adam Smith’s invisible hand to produce the correct quantity of products. As communist economies have discovered to their dismay, an all-powerful central planner cannot possibly achieve any semblance of market efficiency in deciding what goods to produce and how resources should be allocated.

Similarly, millions of individual and institutional investors by their collective buying and selling decisions produce a tableau of stock-market prices that appear to make one stock just as good a buy as another. And while market forecasts of future returns are often erroneous, as a group they appear to be more correct than the forecasts made by any individual investor. Most active portfolio managers must hold their heads in shame when their returns are compared with the results of investing in a low-cost, broad-based equity index fund.

As all readers of this book recognize, the market as a whole does not invariably make correct pricing decisions. At times, there is a madness to crowd behavior, as we have seen from seventeenth-century tulip bulbs to twenty-first-century Internet and meme stocks. It is this occasional pathological crowd behavior that has attracted the attention of behavioral finance.

One widely recognized phenomenon in the study of crowd behavior is the existence of “group think.” Groups of individuals will sometimes reinforce one another into believing that some incorrect point of view is, in fact, the correct one. Surely, the wildly overoptimistic group forecasts regarding the earnings potential of the Internet and the incorrect pricing of New Economy stocks during early 2000 are examples of the pathology of herd behavior.

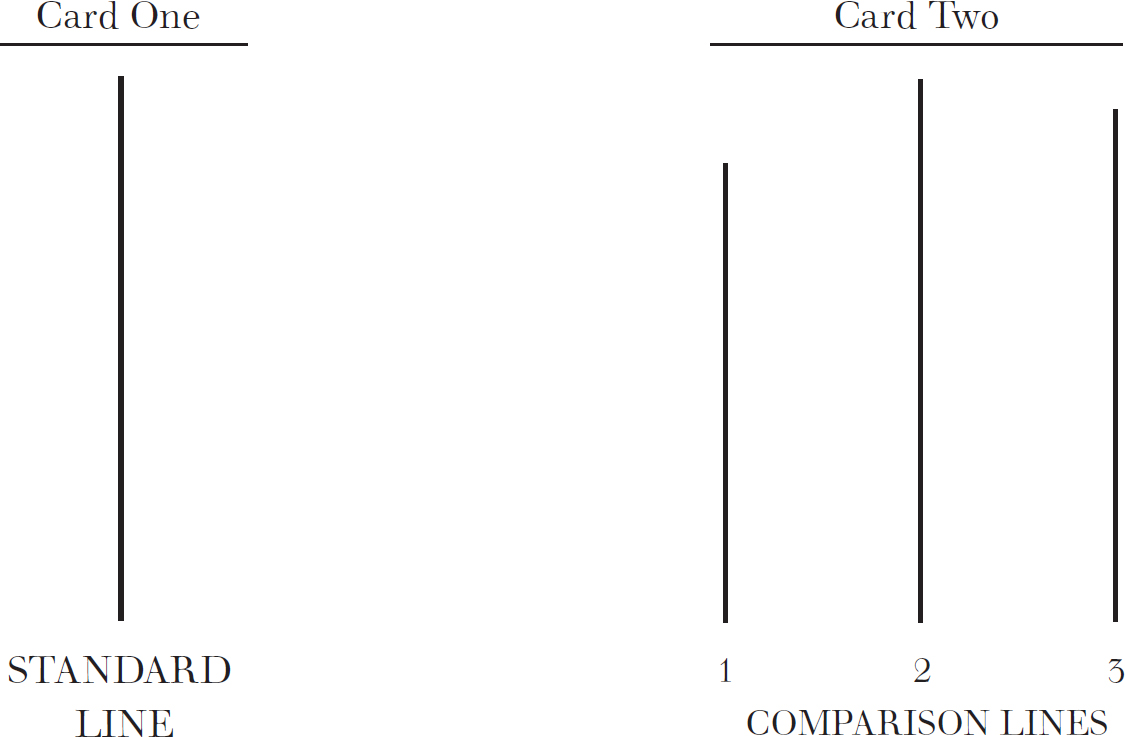

The social psychologist Solomon Asch was one of the first to study how group behavior may lead to incorrect decision making. During the 1950s, Asch conducted a famous laboratory experiment in which a group of participants was asked to answer a simple question that any child could answer correctly. The subjects were shown two cards with vertical lines such as the cards shown below. The card on the left showed one vertical line. The subjects were asked which line on the card on the right was the same length as the line on the first card. Seven subjects participated in a series of such questions.

But Asch added a diabolical twist to the experiment. In some of the experiments, he recruited six of the seven participants to deliberately give the wrong answer and to do so before the seventh participant had a chance to express an opinion. The results were astonishing. The seventh participant would often give the incorrect answer. Asch conjectured that social pressure caused participants to pick the wrong line even when they knew that their answer was incorrect.

SAMPLE CARDS USED IN ASCH EXPERIMENT

Source: Solomon E. Asch, Social Psychology (Oxford, 1987). By permission of Oxford University Press, http://www.oup.com.

A 2005 study by Gregory Berns, a neuroscientist, used MRI scanners to examine the workings of the brain to determine whether people gave in to the group knowing that their answers were incorrect or whether their perceptions had actually changed. If caving in to the group was the result of social pressure, the study reasoned, one should see changes in the area of the forebrain involved in monitoring conflicts. But if the conformity stemmed from actual changes in perception, one would expect changes in the posterior brain areas dedicated to vision and spatial perception. In fact, the study found that when people went along with the group in giving wrong answers, activity increased in the area of the brain devoted to spatial awareness. In other words, it appeared that what other people said actually changed what subjects believed they saw. It seems that other people’s errors actually affect how someone perceives the external world.

In another study, social psychologists put a single person on a street corner and asked him to look up at an empty sky for sixty seconds. The psychologists then observed that a tiny fraction of the pedestrians on the street stopped to see what the person was looking at, but most simply walked past. Then the psychologists put five people on the corner looking at the sky; this time four times as many people stopped by to gaze at an empty sky. When the psychologists put fifteen people on the corner looking at the sky, almost half of the passersby stopped. Increasing the number of people looking skyward increased the number of gazing pedestrians even more.

Clearly, the Internet bubble of the 1999–early 2000 period provides a classic example of incorrect investment judgments leading people to go mad in herds. Individual investors, excited by the prospect of huge gains from stocks catering to the New Economy, got infected with an unreasoning herd mentality. Word-of-mouth communications from friends at the golf club, associates at work, and fellow card players provided a powerful message that great wealth was being created by the growth of the Internet, and social media made the propagation of rumors and misinformation even easier. Investors then began to purchase common stocks for no other reason than that prices were rising and other people were making money, even if the price increases could not be justifiable by fundamental reasons such as the growth of earnings and dividends. As the economic historian Charles Kindleberger has stated, “There is nothing so disturbing to one’s well-being and judgment as to see a friend get rich.” And as Robert Shiller, author of the best-selling Irrational Exuberance, has noted, the process feeds on itself in a “positive feedback loop.” The initial price rise encourages more people to buy, which in turn produces greater profits and induces a larger and larger group of participants. The phenomenon is another example of the Ponzi scheme that I described in chapter 4, in connection with the Internet bubble. Eventually one runs out of greater fools.

Such herding is not limited to unsophisticated individual investors. Mutual-fund managers have a tendency to follow the same strategies and herd into the same stocks. Indeed, a study by Harrison Hong, Jeffrey Kubik, and Jeremy Stein, three leaders in the field of behavioral finance, determined that mutual-fund managers were more likely to hold similar stocks if other managers in the same city were holding similar portfolios. Such results are consistent with an epidemic model, in which investors quickly and irreversibly spread information about stocks by word of mouth. Such herding has had devastating effects for the individual investor. Although long-run returns from the stock market have been generous, the returns for the average investor have been significantly poorer. This is because investors tended to buy equity mutual funds just when exuberance had led to market peaks. During the twelve months ending in March of 2000, more new cash flow went into equity mutual funds than during any preceding period. But while the market was reaching troughs in the falls of 2002 and 2008, individuals made significant withdrawals from their equity investments. A study by Dalbar Associates suggests that the average investor may earn a rate of return 5 percentage points lower than the average market return because of this timing penalty.

In addition, investors tend to put their money into the kinds of mutual funds that have recently had good performance. For example, the large inflows into equity mutual funds in the first quarter of 2000 went entirely into high-tech “growth” funds. So-called “value” funds experienced large fund outflows. Over the subsequent two years, the growth funds declined sharply in value, while the value funds actually produced positive returns. This selection penalty exacerbates the timing penalty described above. One of the most important lessons of behavioral finance is that individual investors must avoid being carried away by herd behavior.

Kahneman and Tversky’s most important contribution is called prospect theory, which describes individual behavior in the face of risky situations where there are prospects of gains and losses. In general, financial economists such as Harry Markowitz constructed models where individuals made decisions based on the likely effect of those choices on the person’s final wealth. Prospect theory challenges that assumption. People’s choices are motivated instead by the values they assign to gains and losses. Losses are considered far more undesirable than equivalent gains are desirable. Moreover, the language used to present the possible gains and losses will influence the final decision that is made. In psychological terms, this is known as “how the choice is framed.”

For example, you are told that a fair coin will be flipped and that if it comes up heads you will be given $100. If the coin comes up tails, however, you must pay $100. Would you accept such a gamble? Most people would say no, even though the gamble is a fair one in the sense that in repeated trials you would end up even. Half the time you would gain $100 and half the time you would lose $100. In mathematical terms, the gamble has an “expected value” of zero, calculated as follows:

Probability of heads × payoff if heads + probability of tails × payoff if tails = Expected value. Expected value = ½($100) + ½(–$100) = 0.

Kahneman and Tversky then tried this experiment with many different subjects, varying the amount of the positive payoff to test what it would take to induce people to accept the gamble. They found that the positive payoff had to be about $250. Note that the expected value of the gain from such a gamble is $75, so this is a very favorable bet.

Expected value = ½($250) + ½(–$100) = $75.

Kahneman and Tversky concluded that losses were 2½ times as undesirable as equivalent gains were desirable. In other words, a dollar loss is 2½ times as painful as a dollar gain is pleasurable. People exhibit extreme loss aversion, even though a change of $100 of wealth would hardly be noticed for most people with substantial assets. We’ll see later how loss aversion leads many investors to make costly mistakes.

Interestingly, however, when individuals faced a situation where sure losses were involved, the psychologists found that they were overwhelmingly likely to take the gamble. Consider the following two alternatives:

1. A sure loss of $750.

2. A 75 percent chance to lose $1,000 and a 25 percent chance to lose nothing.

Note that the expected values of the two alternatives are the same—that is, a loss of $750. But almost 90 percent of the subjects tested chose alternative (2), the gamble. In the face of sure losses, people seem to exhibit risk-seeking behavior.

Kahneman and Tversky also discovered a related and important “framing” effect. The way choices are framed to the decision maker can lead to quite different outcomes. They posed the following problem.

Imagine that the U.S. is preparing for the outbreak of an unusual Asian disease, which is expected to kill 600 people. Two alternative programs to combat the disease have been proposed. Assume that the exact scientific estimates of the consequences of the programs are as follows:

If Program A is adopted, 200 people will be saved.

If Program B is adopted, there is a one-third probability that 600 people will be saved and a two-thirds probability that no people will be saved.

Note first that the expected value of the number of people saved is the same 200 in both programs. But according to prospect theory, people are risk-averse when considering possible gains from the two programs, and, as expected, about two-thirds of the respondents to this question picked Program A as the more desirable.

But suppose we framed the problem differently.

If Program A* is adopted, 400 people will die.

If Program B* is adopted, there is a one-third probability that nobody will die and a two-thirds probability that 600 people will die.

Note that the options A and A* as well as B and B* are identical. But the presentation in the second problem is in terms of the risks of people’s dying. When the problem was framed in this way, over 75 percent of the subjects chose Program B*. This illustrated the effect of “framing” as well as risk-seeking preferences in the domain of losses. When doctors are faced with decisions regarding treatment options for people with cancer, different choices tend to be made if the problem is stated in terms of survival probabilities rather than mortality probabilities.

Behavioralists also stress the importance of the emotions of pride and regret in influencing investor behavior. Investors find it very difficult to admit, even to themselves, that they have made a bad stock-market decision. Feelings of regret may be amplified if such an admission had to be made to friends or a spouse. On the other hand, investors are usually quite proud to tell the world about their successful investments that produced large gains.

Many investors may feel that if they hold on to a losing position, it will eventually recover and feelings of regret will be avoided. These emotions of pride and regret may be behind the tendency of investors to hold on to their losing positions and to sell their winners. The Barber and Odean study of the trading records of 10,000 clients of a large discount brokerage firm found a pronounced “disposition effect.” There was a clear disposition among investors to sell their winning stocks and to hold on to their losing investments. Selling a stock that has risen enables investors to realize profits and build their self-esteem. If they sold their losing stocks, they would realize the painful effects of regret and loss.

This reluctance to take losses is clearly non-optimal according to rational investment theory and stupid in commonsense terms. Selling stocks with gains (outside tax-advantaged retirement accounts) involves paying capital gains taxes. Selling stock on which losses have been realized involves reducing taxes on other realized gains or a tax deduction, up to certain limits. Even if the investor believed that his losing stock would recover in the future, it would pay to sell the stock and purchase a stock in the same industry with similar prospects and risk characteristics. A similar reluctance to take losses appears to be evident in the residential housing market. When house prices are rising, the volume of sales rises and houses tend to sell quickly at asking prices or higher. During periods of falling prices, however, sales volumes decline and individuals let their homes sit on the market for long periods of time with asking prices well above market prices. Extreme loss aversion helps explain sellers’ reluctance to sell their properties at a loss.

BEHAVIORAL FINANCE AND SAVINGS

Behavioral-finance theory also helps explain why many people refuse to join a 401(k) savings plan at work, even when their company matches their contributions. If one asks an employee who has become used to a particular level of take-home pay to increase his allocation to a retirement plan by one dollar, he will view the resulting deduction (even though it is less than a dollar because contributions to retirement plans are deductible from taxable income up to certain generous amounts) as a loss of current spending availability. Individuals weigh these losses much more heavily than gains. When this loss aversion is coupled with the difficulty of exhibiting self-control, the ease of procrastinating, and the ease of making no changes (status quo bias), it becomes, as psychologists teach us, perfectly understandable why people tend to save too little.

Two suggestions have been made to overcome people’s reluctance to save. The first is to overcome inertia and status quo bias by changing the framing of the choice. We know that if we ask employees actively to sign up for a 401(k) savings plan, many will decline to join. But if the problem is framed differently, so that one must actively “opt out” of the savings plan, participation rates will be much greater. Corporations that frame their 401(k) savings plans with an automatic enrollment feature (where a conscious decision must be made to fill out an “opt out” declaration) have far higher participation rates than do plans where employees must actively “opt in” to the plan.

Another brilliant enticement has been developed by the economists Richard Thaler and Shlomo Benartzi. Some employees will decline to save even with plans that have automatic enrollment because they can barely make ends meet with their current salary. The essence of the Thaler-Benartzi “Save More Tomorrow” plan is to have employees commit in advance to allocate a portion of any salary increases toward retirement savings. If employees join the plan, their contribution to their retirement savings plan is increased, beginning with the first paycheck after a raise. This feature mitigates the perceived loss aversion of a cut in take-home pay. The contribution rate continues to increase on each scheduled raise until it reaches the maximum tax-deductible amount allowed by law. In this way, inertia and status quo bias work toward keeping people in the plan. The employee is allowed to opt out of the plan at any time.

Thaler and Benartzi first implemented their plan in 1998 at a midsize manufacturing company. The company was suffering from low participation in its retirement savings plan at the time. The Save More Tomorrow plan proved to be very popular. More than three-quarters of the employees of the firm agreed to join. In addition, over 80 percent of those employees stayed with it through subsequent pay raises. Even those who withdrew did not reduce their contribution rates to the original levels; they merely stopped the future increases from taking place. Thus, even these workers were saving significantly more than they had been before joining the plan.

Thus far we have considered the cognitive biases that influence investors and, therefore, security prices. The actions of individual investors are often irrational, or at least not fully consistent with the economist’s ideal of optimal decision making. In perhaps the most pathological case, individuals appear to go mad in herds and bid some categories of stocks to unreasonable heights. Since the errors of irrational investors do not cancel out but often reinforce each other, especially in the era of social media, how can stocks be efficiently priced? Believers in efficient markets rotely state that “arbitrage” will make the market efficient even if many individual investors are irrational. Arbitrageurs, such as hedge-fund managers, will take offsetting positions—such as selling overpriced stocks short and buying underpriced ones—so that any mispricing caused by irrational investors is quickly corrected. Rational traders are expected to offset the impact of behavioral traders. Thus, the second major pillar on which some behavioralists rest their case against efficient markets is that such arbitrage is severely constrained. Behavioralists believe that important limits to arbitrage exist that prevent out-of-whack prices from being corrected.

Suppose irrational investors cause an oil company security to become overpriced relative to both its fundamental value and its peer oil companies. Arbitrageurs can simply sell the overpriced security short and buy a similar substitute oil company security. Thus, the arbitrageur is hedged in the sense that favorable or unfavorable events affecting the oil industry will influence both companies. A rise in the price of oil that makes the shorted security rise will make the arbitrageur’s long position rise as well.

But this kind of arbitrage is extremely risky. Suppose the “overpriced” security reports some unusually good news, such as a significant oil strike that was not anticipated. Or suppose the “fairly valued” security suffers some unforeseen setback, such as the explosion of a deep-water oil well, which causes its price to fall. The arbitrageur could conceivably lose on both sides of the trade. The security that had been sold short could rise, and the security held long could fall.

The trader who tries to “correct” perceived mispricings also runs the risk that investors will become even more overenthusiastic about the “overpriced” security. Suppose an arbitrageur, convinced during 1999 that Internet stocks were outrageously overpriced, sold Internet favorites short, hoping to buy them back later at lower prices. But as enthusiasm for the New Economy continued to grow, the prices of these stocks rose even further—many of them doubling and then doubling again. Only in retrospect do we know that the bubble burst during 2000. In the meantime, many traders lost their shirts. The market can remain irrational longer than the arbitrageur can remain solvent. This is especially true when the arbitrageur is credit constrained. Long Term Capital Management, a hedge fund in which Nobel laureates devised the strategies, found itself in an untenable position when the prices of its hedges moved against it and it had insufficient capital to keep them afloat. And the hedge fund Melvin Capital lost half of its $13 billion capital from its short position in GameStop during the 2021 meme stock craze.

The natural players in the game of selling overpriced securities short and buying underpriced ones are global hedge funds, with trillions of dollars to invest. One might suppose that these funds would have recognized the unsustainability of the prices of Internet stocks and exploited the mispricing by selling short. A study by Markus Brunnermeier and Stefan Nagel examined hedge-fund behavior during the 1998–2000 period to see whether these funds restrained the rise in speculative favorites.

The findings were surprising. Sophisticated speculators such as hedge funds were not a correcting force during the bubble period. They actually helped inflate the bubble by riding it rather than attacking it. Hedge funds were net buyers of Internet stocks throughout the 1998–early 2000 period. Their strategy reflected their belief that contagious enthusiasm and herding of unsophisticated investors would cause the mispricing to grow. They were playing the game described earlier in Keynes’s famous newspaper beauty contest. While a stock selling at $30 might be “worth” only $15, it would be a good buy if some greater fools would be willing to pay $60 for the stock at some future time.

It appears that hedge funds also played a destabilizing role in the oil market during 2005 and 2006. From 2004 to 2006 the price of a barrel of crude oil more than doubled. Although economic forces such as the growth of the world economy provided some fundamental reasons for the upward price pressure, it seems that speculative activity, especially by hedge funds, helped fuel the advance. And the few hedge funds that went short in the oil futures market experienced substantial losses. It is clear that arbitrage trades to correct a perceived price bubble are inherently risky.

And there are also times when short selling is not possible or at least severely constrained. Typically in selling short, the security that is shorted is borrowed in order to deliver it to the buyer. If, for example, I sell short 100 shares of IBM, I must borrow the securities and deliver them to the buyer. (I must also pay the buyer any dividends that are declared on the stock during the period I hold the short position.) In some cases it may be impossible to find stock to borrow, and thus it may be technically impossible or prohibitively expensive to execute a short sale. In some of the most glaring examples of inefficient pricing, constraints on short selling prevented arbitrageurs from correcting mispricings.

Arbitrages may also be hard to establish if a close substitute for the overpriced security is hard to find. For an arbitrage to be effective, there must be a similar fairly priced security that can be bought to offset the short position and that can be expected to rise if some favorable event occurs that influences the whole market or the sector to which the security belongs.

One of the best examples used by behavioralists to show that market prices can be inefficient is the case of two identical shares that do not trade at identical prices. Royal Dutch Petroleum and Shell Transport are considered Siamese twin companies. These companies agreed in 1907 to form an alliance and to split their after-tax profits 60 percent for Royal Dutch, 40 percent for Shell. In an efficient market, the market value of Royal Dutch should always be 1½ times as great as the market value of Shell. In fact, Royal Dutch has often traded at a premium to Shell of up to 20 percent over fair value. In efficient markets, the same cash flows ought to sell at equivalent valuations.

The problem with this example is that the two securities trade in different national markets with different rules and possibly different future restrictions. But even if Royal Dutch and Shell were considered equivalent in all respects, the arbitrage between the two securities would be inherently risky. If Royal Dutch sells at a 10 percent premium to Shell, the appropriate arbitrage is to sell the overpriced Royal Dutch shares short and buy the cheap Shell shares. The arbitrage is risky, however. An overpriced security can always become more overpriced, causing losses for the short seller. Bargains today can become better bargains tomorrow. It is clear that one cannot rely completely on arbitrage to smooth out any deviations of market prices from fundamental value. Constraints on short selling undoubtedly played a role in the propagation of the housing bubble during the end of the first decade of the 2000s. When it is virtually impossible to short housing in specific areas of the country, only the votes of the optimists get counted. When the optimists are able to leverage themselves easily with mortgage loans, it is easy to see why a housing bubble is unlikely to be constrained by arbitrage.

WHAT ARE THE LESSONS FOR INVESTORS FROM BEHAVIORAL FINANCE?

Night owls like myself often watch the late-night TV shows. One of the funnier bits from David Letterman’s former show was the segment “Stupid Pet Tricks,” where pet owners have their animals perform all manner of dumb antics. Unfortunately, investors often act very much like the owners and pets on the TV show—and it isn’t funny. They are overconfident, get trampled by the herd, harbor illusions of control, and refuse to recognize their investment mistakes. The pets actually look smart in comparison.

We have just seen how various aspects of human behavior influence investing. In investing, we are often our worst enemy. As Pogo put it, “We have met the enemy and it is us.” An understanding of how vulnerable we are to our own psychology can help us avoid the stupid investor delusions that can screw up our financial security. There is an old adage about the game of poker: If you sit down at the table and can’t figure out who the sucker is, get up and leave because it’s you. These insights about investor psychology can keep you from being the patsy.

Charles Ellis, a longtime observer of stock markets and author of the brilliant investing book Winning the Loser’s Game, observes that, in the game of amateur tennis, most points are won not by adroit plays on your part but rather by mistakes on the part of your opponent. So it is in investing. Ellis argues that most investors beat themselves by engaging in mistaken stock-market strategies rather than accepting the passive buy-and-hold indexing approach recommended in this book. The way most investors behave, the stock market becomes a loser’s game.

How easy it was in early 2000, when the tech stock you bought moved persistently higher, to convince yourself that you were an investment genius. How easy it was then to convince yourself that chasing the last period’s best-performing mutual fund was a sure strategy for success. And for the few who gave up their jobs during the bubble to engage in day-trading, how exhilarating it was to buy a stock at 10:00 a.m. and find that it had risen 10 percent by noon. All of these strategies ended in disaster. Frequent traders invariably earn lower returns than steady buy-and-hold investors.

The first step in dealing with the pernicious effects of our behavioral foibles is to recognize them. Bow to the wisdom of the market. Just as the tennis amateur who simply tries to return the ball with no fancy moves is the one who usually wins, so does the investor who simply buys and holds a diversified portfolio comprising all of the stocks that trade in the market. Don’t be your own worst enemy: Avoid stupid investor tricks. Here are the most important insights from behavioral finance.

Behavioral financial economists understand the feedback mechanisms that lead investors to follow the crowd. When Internet or meme stocks were consistently rising, it was hard not to get swept up in the euphoria—especially when all your friends were boasting of their spectacular stock-market profits. A large literature documents the pervasiveness of the influence of friends on one’s investment decisions. Robert Shiller and John Pound surveyed 131 individual investors and asked what had drawn their attention to the stock they had most recently purchased. A typical response was that a personal contact, such as a friend or relative, had recommended the purchase. Hong, Kubik, and Stein provided more systematic evidence as to the importance of friends in influencing investors’ decisions. They found that social households—those who interact with their neighbors, or attend church—are substantially more likely to invest in the market than nonsocial households.

Any investment that has become a topic of widespread conversation is likely to be hazardous to your wealth. It was true of gold in the early 1980s and Japanese real estate and stocks in the late 1980s. It was true of Internet-related stocks in the late 1990s and condominiums in California, Nevada, and Florida in the first decade of the 2000s, as well as bitcoin, GameStop, and AMC Entertainment in 2021.

Invariably, the hottest stocks or funds in one period are the worst performers in the next. And just as herding induces investors to take greater and greater risks during periods of euphoria, so the same behavior often leads many investors simultaneously to throw in the towel when pessimism is rampant. The media tend to encourage such self-destructive behavior by hyping the severity of market declines and blowing the events out of proportion to gain viewers and listeners. Even without excessive media attention, large market movements encourage buy and sell decisions that are based on emotion rather than on logic.

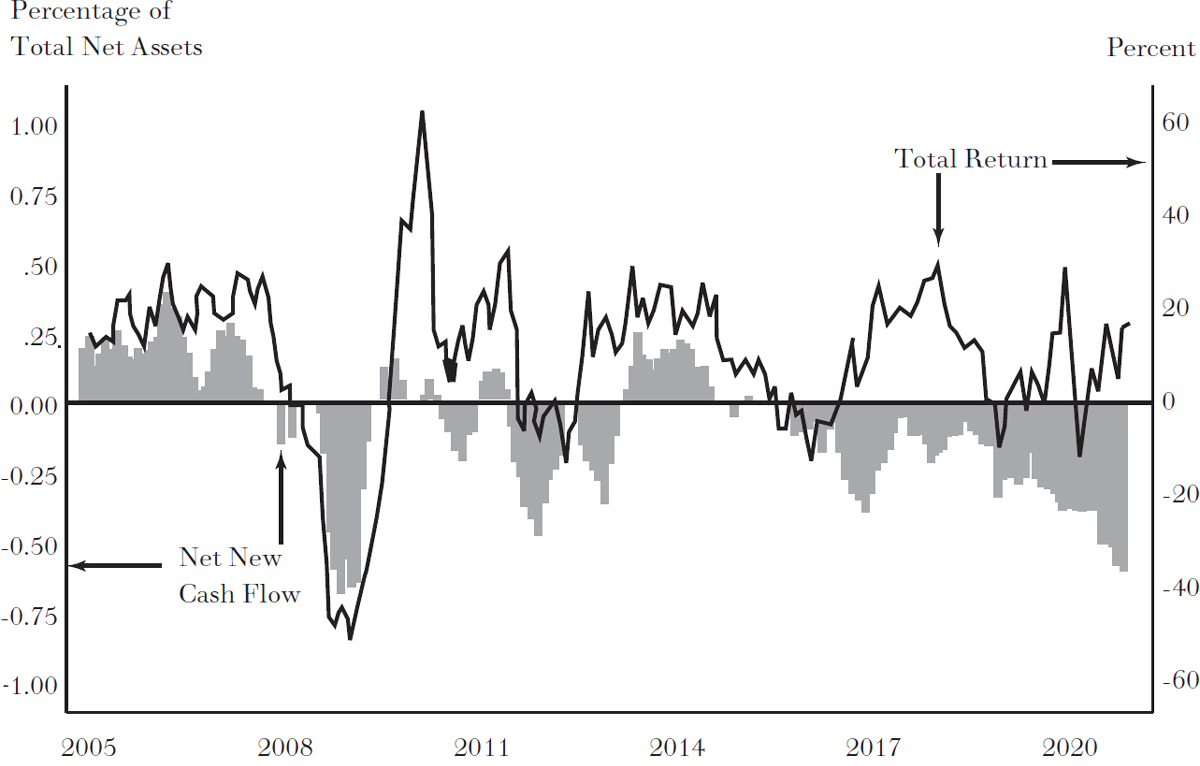

Because of bad timing, the typical mutual-fund investor earns a rate of return from the stock market far below the returns that would be earned by simply buying and holding a market index fund. This is because investors tend to put their money into mutual funds at or near market tops (when everyone is enthusiastic) and to pull their money out at market bottoms (when pessimism reigns). The exhibit on page 252 helps make the point. Net new cash flow into mutual funds peaked when the market reached a high in early 2000. At the market trough in the fall of 2002, investors pulled their money out. The chart shows that in 2008 and early 2009, just at the bottom of the market during the financial crisis, more money went out of the market than ever before. You can see the effects of this timing penalty in the chart.

There is also a selection penalty. At the peak of the market in early 2000, money flowed into “growth”-oriented mutual funds, typically those associated with high technology and the Internet, and flowed out of “value” funds, those funds holding old-economy stocks that sold at low prices relative to their book values and earnings. Over the next three years, the “value” funds provided generous positive returns to their investors, and “growth” funds declined sharply. During the third quarter of 2002, after an 80 percent decline from the peak of the NASDAQ Index, there were large redemptions out of growth funds. Chasing today’s hot investment usually leads to tomorrow’s investment freeze.

DO NOT TRY TO TIME THE MARKET: FLOWS TO EQUITY FUNDS RELATED TO STOCK-PRICE PERFORMANCE

Source: 2021 Investment Company Institute Fact Book

Behavioral finance specialists have found that investors tend to be overconfident in their judgments and invariably do too much trading for their own financial well-being. Many investors move from stock to stock or from mutual fund to mutual fund as if they were selecting and discarding cards in a game of gin rummy. Investors accomplish nothing from this behavior except to incur transactions costs and to pay more in taxes. Short-term gains are taxed at regular income tax rates. The buy-and-hold investor defers any tax payments on the gains and may avoid taxes completely if stocks are held until distributed as part of one’s estate. Remember the advice of the legendary investor Warren Buffett: Lethargy bordering on sloth remains the best investment style. The correct holding period for the stock market is forever.

The cost of overtrading is quite substantial. Using data on the trading behavior of approximately 66,000 households during the period 1991–96, Barber and Odean found that the average household in the sample earned an annual return of 16.4 percent, while the market returned 17.9 percent. In contrast, the annual return to the portfolio of households that traded the most was only 11.4 percent. In other words, the portfolios of those households that traded the most substantially underperformed more passive benchmarks. In addition, men tended to be more overconfident and trade far more frequently than women. Odean’s advice to investors: If you are contemplating making a stock trade (and you are married), ask your wife whether you should do it.

Fidelity Investments repeated the study in 2021. Fidelity’s analysis covered 5.2 million customer accounts from 2011 to 2020. They found that female customers earned on average considerably more than their male counterparts. The source of women’s superior returns was the way they trade, or more accurately, their propensity not to trade. Male Fidelity customers traded twice as often as female customers. Vanguard saw similar patterns during the same decade. The evidence suggests that trading too much is hazardous to your wealth.

3. If You Do Trade: Sell Losers, Not Winners

We have seen that people are far more distressed at taking losses than they are overjoyed at realizing gains. Thus, paradoxically, investors might take greater risks to avoid losses than they would to achieve equivalent gains. Moreover, investors are likely to avoid selling stocks or mutual funds that went down, in order to avoid the realization of a loss and the necessity of admitting that they made a mistake. On the other hand, investors are generally willing to discard their winners because that enables them to enjoy the success of being correct.

Sometimes, it is sensible to hold on to a stock that has declined during a market meltdown, especially if you have reason to believe the company is still successful. Moreover, you would suffer double the regret if you sold it and the stock subsequently went up. But it makes no sense to hold on to losing stocks such as Enron and WorldCom because of the mistaken belief that if you don’t sell, you have not taken a loss. A “paper loss” is just as real as a realized loss. The decision not to sell is exactly the same as the decision to buy the stock at the current price. Moreover, if you own the stock in a taxable account, selling allows you to take a tax loss, and the government will help cushion the blow by lowering the amount of your taxes. Selling your winners will add to your tax burden.

4. Other Stupid Investor Tricks

Be Wary of New Issues. Do you think you can make lots of money by getting in on the ground floor of the initial public offering (IPO) of a company just coming to market? Particularly during the great Internet bubble that collapsed in 2000, it seemed that IPOs were the sure path to riches. Some successful IPOs began trading at two, three, and (in one case) even seven times the price at which they were first offered to the public. No wonder some investors came to believe that getting in on an IPO was the easiest way to coin money in the stock market.

My advice is that you should not buy IPOs at their initial offering price and that you should never buy an IPO just after it begins trading at prices that are generally higher than the IPO price. Historically, IPOs have been a bad deal. In measuring all IPOs five years after their initial issuance, researchers have found that IPOs underperform the total stock market by about 4 percentage points per year. The poor performance starts about six months after the issue is sold. Six months is generally set as the “lock-up” period, where insiders are prohibited from selling stock to the public. Once that constraint is lifted, the price of the stock often tanks.

The investment results are even poorer for individual investors. You will never be allowed to buy the really good IPOs at the initial offering price. The hot IPOs are snapped up by the big institutional investors or the very best wealthy clients of the underwriting firm. If your broker calls to say that IPO shares will be available for you, you can bet that the new issue is a dog. Only if the brokerage firm is unable to sell the shares to the big institutions and the best individual clients will you be offered a chance to buy at the initial offering price. Hence, it will systematically turn out that you will be buying only the poorest of the new issues. There is no strategy I am aware of likely to lose you more money, except perhaps the horse races or the gaming tables of Las Vegas.

Stay Cool to Hot Tips. We’ve all heard the stories. Your uncle Gene knows about a diamond mine in Zaire that’s a guaranteed winner. Please remember that a mine is usually a hole in the ground with a liar standing in front of it. Your cousin’s sister-in-law Gertrude was told confidentially about an undiscovered little biotech company. “It’s a screaming bargain. It’s selling at only a dollar a share, and they’re ready to announce a cure for cancer. Think, for $2,000 you can buy 2,000 shares.” Tips come at you from all fronts—friends, relatives, the telephone, and the Internet. Don’t go there. Steer clear of any hot tips. They are overwhelmingly likely to be the poorest investments of your life. And remember: Never buy anything from someone who is out of breath.

Distrust Foolproof Schemes. You will be told by amateurs and professionals alike that schemes exist to pick the best fund managers and to keep you out of the market when prices are falling. The sad fact is that it can’t be done. Sure, there are portfolio strategies that in hindsight produced above-average returns, but they all self-destruct over time. There are even market-timing strategies that have been successful for years and even decades. In the long run, though, I agree with Bernard Baruch, a legendary investor of the early twentieth century, who said, “Market timing can only be accomplished by liars.” And Jack Bogle, a legend of the late twentieth century, remarked, “I do not know of anybody who has done it [market timing] successfully and consistently.”

Investors should also never forget the age-old maxim “If something is too good to be true, it is too good to be true.” Heeding this maxim could have saved investors from falling prey to the largest Ponzi scheme ever: the Bernard L. Madoff fraud uncovered in 2008, in which $50 billion was said to have been lost. The real con in the Madoff affair is that people fell for the myth that Madoff could consistently earn between 10 and 12 percent a year for investors in his fund.

The “genius” of the fraud was that Madoff offered what seemed to be a modest and safe return. Had he offered a 50 percent return, people might well have been skeptical of such pie-in-the-sky promises. But consistent returns of 10 to 12 percent per year seemed well within the realm of possibility. In fact, however, earning such returns year after year in the stock market (or in any other market) is not remotely possible, and such claims should have been a dead giveaway. The U.S. stock market may have averaged over 9 percent a year over long periods of time, but only with tremendous volatility, including years when investors have lost as much as 40 percent of their capital. The only way Madoff could report such a performance was by cooking the books. And don’t count on the regulators to protect you from such fraudulent schemes. The SEC was warned that Madoff’s results were impossible, but the agency failed to act. Your only protection is to realize that anything that seems too good to be true undoubtedly is untrue.

DOES BEHAVIORAL FINANCE TEACH WAYS TO BEAT THE MARKET?

Some behavioralists believe that the systematic errors of investors can provide opportunities for unemotional, rational investors to beat the market. They believe that irrational trading creates predictable stock-market patterns that can be exploited by wise investors. These ideas are far more controversial than the lessons provided above, and we will examine some of them in the next chapter.