THE EXPLOSIVE BUBBLES IN THE EARLY DECADES OF THE 2000s

If you can keep your head when all about you Are losing theirs . . .

Yours is the Earth and everything that’s in it . . . .

—Rudyard Kipling, “If—”

FINANCIALLY DEVASTATING AS the bubbles of the last decades of the twentieth century were, they cannot compare with those of the early decades of the twenty-first century. When the Internet bubble popped in the early 2000s, over $8 trillion of market value evaporated. It was as if a year’s output of the economies of Germany, France, England, Italy, Spain, the Netherlands, and Russia had completely disappeared. The entire world economy almost crashed when the U.S. real estate bubble popped, and a prolonged world recession followed. In the early 2020s, we experienced enormous bubbles in the prices of meme stocks and cryptocurrencies. Comparing any of these bubbles to the tulip-bulb craze is undoubtedly unfair to the flowers.

Most bubbles have been associated with some new technology (as in the tronics boom) or with some new business opportunity (as when the opening of profitable new trade opportunities spawned the South Sea Bubble). The Internet was associated with both: it represented a new technology, and it offered new business opportunities that promised to revolutionize the way we obtain information and purchase goods and services. The promise of the Internet spawned the largest creation and largest destruction of stock market wealth of all time.

Robert Shiller, in his book Irrational Exuberance, describes bubbles in terms of “positive feedback loops.” A bubble starts when any group of stocks, in this case those associated with the excitement of the Internet, begin to rise. The updraft encourages more people to buy the stocks, which causes more TV and print coverage, which causes even more people to buy, which creates big profits for early Internet stockholders. The successful investors tell you how easy it is to get rich, which causes the stocks to rise further, which pulls in larger and larger groups of investors. But the whole mechanism is a kind of Ponzi scheme where more and more credulous investors must be found to buy the stock from the earlier investors. Eventually, one runs out of greater fools.

Even highly respected Wall Street firms joined in the hot-air float. The venerable investment firm Goldman Sachs argued in mid-2000 that the cash burned by the dot-com companies was primarily an “investor sentiment” issue and not a “long-term risk” for the sector or “space,” as it was often called. A few months later, hundreds of Internet companies were bankrupt, proving that the Goldman report was inadvertently correct. The cash burn was not a long-term risk—it was a short-term risk.

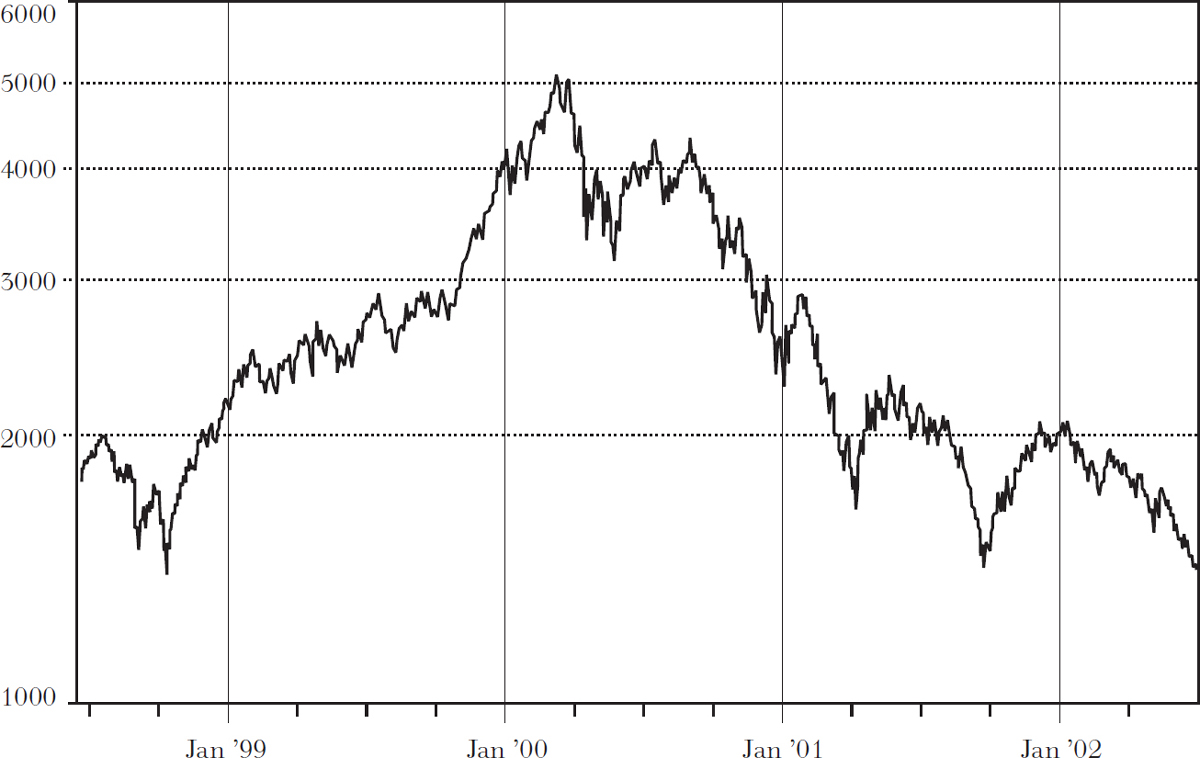

Until that moment, anyone scoffing at the potential for the “New Economy” was a hopeless Luddite. As the chart on page 84 indicates, the NASDAQ Index, an index essentially representing high-tech New Economy companies, more than tripled from late 1998 to March 2000. The price-earnings multiples of the stocks in the index that had earnings soared to over 100.

NASDAQ COMPOSITE STOCK INDEX, JULY 1999–JULY 2002

A Broad-Scale High-Tech Bubble

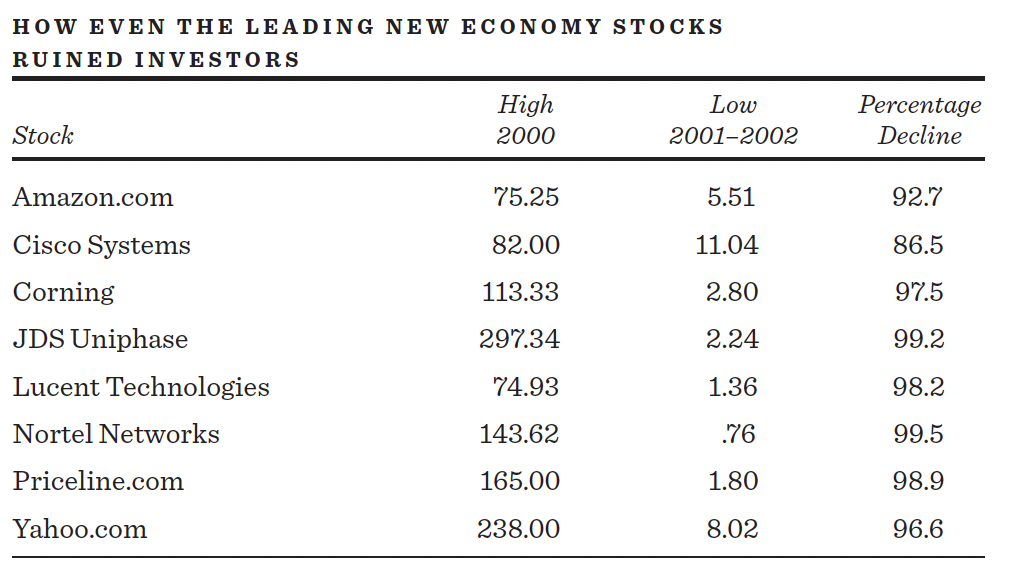

Surveys of investors in early 2000 revealed that expectations of future stock returns ranged from 15 percent per year to 25 percent or higher. For companies such as Cisco, widely known as producing “the backbone of the Internet,” 15 percent returns per year were considered a slam dunk. But Cisco was selling at a triple-digit multiple of earnings and had a market capitalization of almost $600 billion. If Cisco grew its earnings at 15 percent per year, it would still be selling at a well above average multiple ten years later. And if Cisco returned 15 percent per year for the next twenty-five years and the national economy continued to grow at 5 percent over the same period, Cisco would have been bigger than the entire economy. There was a complete disconnect between stock-market valuations and any reasonable expectations of future growth. And even blue-chip Cisco lost over 90 percent of its market value when the bubble burst. It turned out that Cisco did grow its earnings at high rates for the next two decades. But Cisco’s stock sold at a lower price at the start of 2022 than it did at the peak of the bubble in 2000.

In the name game during the tronics boom, all manner of companies added the suffix “tronics” to increase their attractiveness; the same happened during the Internet mania. Dozens of companies, even those that had little or nothing to do with the Net, changed their names to include web-oriented designations such as dot.com, dotnet, or Internet. Companies that changed their names enjoyed an increase in price during the next ten-day period that was 125 percent greater than that of their peers, even when the company’s core business had nothing whatsoever to do with the Net. In the market decline that followed, shares in these companies became worthless. As the following table shows, investors suffered punishing losses even in the leading Internet companies.

PalmPilot, the maker of Personal Digital Assistants (PDAs), is an example of the insanity that went well beyond irrational exuberance. Palm was owned by a company called 3Com, which decided to spin it off to its shareholders. Since PDAs were touted as a sine qua non of the digital revolution, it was assumed that PalmPilot would be a particularly exciting stock.

In early 2000, 3Com sold 5 percent of its shares in Palm in an initial public offering and announced its intention to spin off all the remaining shares to the 3Com shareholders. Palm took off so fast that its market capitalization became twice as large as that of 3Com. The market value of the 95 percent of Palm owned by 3Com was almost $25 billion greater than the total market capitalization of 3Com itself. It was as if all of 3Com’s other assets had been worth a negative $25 billion. If you wanted to buy PalmPilot, you could have bought 3Com and owned the rest of 3Com’s business for minus $61 per share. In its mindless search for riches, the market created bizarre anomalies.

In the first quarter of 2000, 916 venture capital firms invested $15.7 billion in 1,009 startup Internet companies. It was as if the stock market was on steroids. As happened during the South Sea Bubble, many companies that received financing were absurd. Almost all turned out to be dot.com catastrophes. Consider the following examples of Internet startups.

- Digiscents offered a computer peripheral that would make websites and computer games smell. The company ran through millions trying to develop such a product.

- Flooz offered an alternative currency—Flooz—that could be e-mailed to friends and family. In order to jump-start the company, Flooz.com turned to an old business school maxim that “any idiot can sell a one-dollar bill for eighty cents.” Flooz.com launched a special offer to American Express platinum card holders allowing them to buy $1,000 of Flooz currency for just $800. Shortly before declaring bankruptcy, Flooz itself was Floozed when Filipino and Russian gangs bought $300,000 of its currency using stolen credit card numbers.

The names alone of many of the Internet ventures stretch credulity: Bunions.com, Crayfish, Zap.com, Gadzooks, Fogdog, FatBrain, Jungle.com, Scoot.com, and mylackey.com. And then there was ezboard.com, which produced Internet pages called toilet paper, to help you “get the poop” on the online community. These were not business models. They were models for business failure.

My most vivid memory of the IPO boom dates back to an early morning in November 1998, when I was being interviewed on a TV show. While waiting in my suit and tie in the “green room,” I thought how out of place it was to be sitting next to two young men dressed in jeans who looked like teenagers. Little did I realize that they were the first superstars of the Internet boom and the featured attractions on the show. Stephan Paternot and Todd Krizelman had formed TheGlobe.com in Todd’s dorm room at Cornell. The company was an online message board system that hoped to generate large revenues from selling banner advertising. In earlier times, one needed actual revenues and profits to come to market with an IPO. TheGlobe.com had neither. Nevertheless, its bankers, Credit Suisse First Boston, brought it to market at a price of $9 per share. The price immediately soared to $97, at that time the largest first-day gain in history, giving the company a market value of nearly $1 billion and making the two founders multimillionaires. That day we learned that investors would throw money at businesses that only five years before would not have passed normal due diligence hurdles.

While the party was still going strong in early 2000, John Doerr, a leading venture capitalist with the preeminent firm of Kleiner Perkins, called the rise in Internet-related stocks “the greatest legal creation of wealth in the history of the planet.” In 2002, he neglected to write that it was also the greatest legal destruction of wealth on the planet.

Source: Doonesbur y © 1998 G. B. Trudeau. Reprinted with permission of UNIVERSAL UCLICK. All rights reserved.

Wall Street’s high-profile securities analysts provided much of the hot air floating the Internet bubble. Mary Meeker of Morgan Stanley, Henry Blodgett of Merrill Lynch, and Jack Grubman of Salomon Smith Barney became household names and were accorded superstar status. Meeker was dubbed by Barron’s the “Queen of the ’Net.” Blodgett was known as “King Henry,” while Grubman acquired the sobriquet “Telecom Guru.” Like sports heroes, each of them was earning a multimillion-dollar salary. Their incomes, however, were based not on the quality of their analysis but rather on their ability to steer lucrative investment banking business to their firms by implicitly promising that their ongoing favorable research coverage would provide continuing support for the initial public offerings in the after market.

Traditionally, a “Chinese Wall” was supposed to separate the research function of Wall Street firms, which is supposed to work for the benefit of investors, from the very profitable investment banking function, which works for the benefit of corporate clients. But during the bubble, that wall became more like Swiss cheese.

Analysts were the very public cheerleaders for the boom. Blodgett flatly stated that traditional valuation metrics were not relevant in “the big-bang stage of an industry.” Meeker suggested, in a flattering New Yorker profile in 1999, that “this is a time to be rationally reckless.” Their public comments on individual stocks made prices soar. Stock selections were described in terms of powerful baseball hits: A stock that would be expected to quadruple was a “Four Bagger.” More exciting stocks might be “Ten Baggers.”

Securities analysts always find reasons to be bullish. Traditionally, ten stocks were rated “buys” for each one rated “sell.” But during the bubble, the ratio was almost a hundred to one. When the bubble burst, the celebrity analysts faced death threats and lawsuits; and their firms faced investigations and fines by the SEC. Blodgett was renamed the “clown prince” of the Internet bubble by the New York Post. Grubman was ridiculed before a congressional committee and investigated for changing his stock ratings to help obtain investment banking business. Both Blodgett and Grubman left their firms. Fortune magazine summed it all up with a picture of Mary Meeker on the cover and the caption “Can We Ever Trust Wall Street Again?”

In order to justify ever higher prices for Internet-related companies, security analysts began to use a variety of “new metrics” that could be used to value the stocks. After all, the New Economy stocks were a breed apart—they should certainly not be held to the fuddy-duddy old-fashioned standards such as price-earnings multiples that had been used to value traditional old-economy companies.

Somehow, in the brave new Internet world, sales, revenues, and profits were irrelevant. In order to value Internet companies, analysts looked instead at “eyeballs”—the number of people viewing a web page or “visiting” a website. Particularly important were numbers of “engaged shoppers”—those who spent three minutes on a website. Mary Meeker gushed about Drugstore.com because 48 percent of the eyeballs viewing the site were “engaged shoppers.” No one cared whether the engaged shopper ever forked over any greenbacks. Sales were so old-fashioned. Drugstore.com hit $67.50 during the height of the bubble of 2000. A year later, when eyeballs started looking at profits, it was a “penny” stock.

“Mind share” was another popular nonfinancial metric that convinced me that investors had lost their collective minds. For example, the online home seller Homestore.com was highly recommended in October 2000 by Morgan Stanley because 72 percent of all the time spent by Internet users on real estate websites was spent on properties listed by Homestore.com. But “mind share” did not lead Internet users to make up their minds to buy the properties listed and did not prevent Homestore.com from falling 99 percent from its high during 2001.

Special metrics were established for telecom companies. Security analysts clambered into tunnels to count the miles of fiber-optic cable in the ground rather than examining the tiny fraction that was actually lit up with traffic. Each telecom company borrowed money with abandon, and enough fiber was laid to circle the earth 1,500 times. As a sign of the times, the telecom and Internet service provider PSI Net (now bankrupt) put its name on the Baltimore Ravens’ football field. As the prices of telecom stocks continued to skyrocket well past any normal valuation standards, security analysts did what they often do—they just lowered their standards.

The ease with which telecoms could raise money from Wall Street led to massive oversupply—too much long-distance fiber-optic cable, too many computers, and too many telecom companies. Most of the trillion dollars thrown into telecom investments during the bubble vaporized.

The bubble was aided and abetted by the media, which turned us into a nation of traders. Like the stock market, journalism is subject to the laws of supply and demand. Since investors wanted more information about Internet investing opportunities, the supply of magazines increased to fill the need. And since readers were not interested in downbeat skeptical analyses, they flocked to those publications that promised an easy road to riches. Investment magazines featured stories such as “Internet stocks likely to double in the months ahead.” As Jane Bryant Quinn remarked, it was “investment pornography”—“soft core rather than hard core, but pornography all the same.”

A number of business and technology magazines devoted to the Internet sprang up to satisfy the insatiable public desire for more information. Wired described itself as the vanguard of the digital revolution. The Industry Standard ’s IPO tracker was the most widely followed index. Business 2.0 was the “oracle of the New Economy.” The proliferation of publications was a classic sign of a speculative bubble. The historian Edward Chancellor pointed out that during the 1840s, fourteen weeklies and two dailies covered the new railroad industry. During the financial crisis of 1847, many perished. When the Industry Standard failed in 2001, the New York Times editorialized, “it may well go down as the day the buzz died.”

Online brokers were also a critical factor in fueling the Internet boom. Trading was cheap, at least in terms of the small dollar amount of commissions charged. The discount brokerage firms advertised heavily and made it seem that it was easy to beat the market. In one commercial, the customer boasted that she did not simply want to beat the market but to “throttle its scrawny little body to the ground and make it beg for mercy.” In another popular TV commercial, Stuart, the cybergeek from the mailroom, was encouraging his old-fashioned boss to make his first online stock purchase. “Let’s light this candle.” When the boss protested that he knew nothing about the stock, Stuart said, “Let’s research it.” After one click on the keyboard, the boss, thinking himself much wiser, bought his first hundred shares.

Cable networks such as CNBC and Bloomberg became cultural phenomena. Across the world, health clubs, airports, bars, and restaurants were permanently tuned in to CNBC. The stock market was treated like a sports event with a pre-game show (what to expect), a play-by-play during trading hours, and a post-game show to review the day’s action and to prepare investors for the next. CNBC implied that listening would put you “ahead of the curve.” Most guests were bullish. There was no need to remind a CNBC anchor that, just as the family dog that bites the baby is likely to have a short tenure, sourpuss skeptics did not encourage high ratings. The market was a hotter story than sex. Even Howard Stern would interrupt more usual discussions about porn queens and body parts to muse about the stock market and then to tout some particular Internet stocks.

Fraud Slithers In and Strangles the Market

Speculative manias, such as the Internet bubble, bring out the worst aspects of our system. Let there be no mistake: It was the extraordinary New Economy mania that encouraged a string of business scandals that shook the capitalist system to its roots. One spectacular example was the rise and subsequent bankruptcy of Enron—at one time the seventh-largest corporation in America. The collapse of Enron, where over $65 billion of market value was wiped out, can be understood only in the context of the enormous bubble in the New Economy part of the stock market. Enron was seen as the perfect New Economy stock that could dominate the market not just for energy but also for broadband communications, widespread electronic trading, and commerce.

Enron was a clear favorite of Wall Street analysts. Old utility and energy companies were likened by Fortune magazine to “a bunch of old fogies and their wives shuffling around to the sounds of Guy Lombardo.” Enron was likened to a young Elvis Presley “crashing through the skylight” in his skintight gold-lamé suit. The writer left out the part where Elvis ate himself to death. Enron set the standard for thinking outside the box—the quintessential killer app, paradigm-shifting company. Unfortunately, it also set new standards for obfuscation and deception.

Deception appeared to be a way of life at Enron. The Wall Street Journal reported that Ken Lay and Jeff Skilling, Enron’s top executives, were personally involved in establishing a fake trading room to impress Wall Street security analysts, in an episode employees referred to as “The Sting.” The best equipment was purchased, employees were given parts to play arranging fictitious deals, and even the phone lines were painted black to make the operation look particularly slick. The whole thing was an elaborate charade. In 2006, Lay and Skilling were convicted of conspiracy and fraud. A broken man, Ken Lay died later that year.

One employee, who lost his job and his retirement savings when Enron collapsed into bankruptcy, took to the web, where he sold T-shirts with the message “I got lay’d by enron.”

But Enron was only one of a number of accounting frauds that were perpetrated on unsuspecting investors. Various telecom companies overstated revenues through swaps of fiber-optic capacity at inflated prices. WorldCom admitted that it had overstated profits and cash flow by $7 billion, by classifying ordinary expenses, which should have been charged against earnings, as capital investments. In far too many cases, corporate chief executive officers (CEOs) acted more like chief embezzlement officers, and some chief financial officers (CFOs) could more appropriately be called corporate fraud officers. While analysts were praising stocks like Enron and WorldCom to the skies, some corporate officers were transforming the meaning of EBITDA from earnings before interest, taxes, depreciation, and amortization to “earnings before I tricked the dumb auditor.”

Should We Have Known the Dangers?

Fraud aside, we should have known better. We should have known that investments in transforming technologies have often proved unrewarding for investors. In the 1850s, the railroad was widely expected to greatly increase the efficiency of communications and commerce. It certainly did so, but it did not justify the prices of railroad stocks, which rose to enormous speculative heights before collapsing in August 1857. A century later, airlines and television manufacturers transformed our country, but most of the early investors lost their shirts. The key to investing is not how much an industry will affect society or even how much it will grow, but rather its ability to make and sustain profits. And history tells us that eventually all excessively exuberant markets succumb to the laws of gravity. The consistent losers in the market, from my personal experience, are those who are unable to resist being swept up in some kind of tulip-bulb craze. It is not hard, really, to make money in the market. As we shall see later, an investor who simply buys and holds a broad-based portfolio of stocks can make reasonably generous long-run returns. What is hard to avoid is the alluring temptation to throw your money away on short, get-rich-quick speculative binges. The ability to avoid such horrendous mistakes is probably the most important factor in preserving one’s capital and allowing it to grow. The lesson is so obvious and yet so easy to ignore.

THE U.S. HOUSING BUBBLE AND CRASH OF THE EARLY 2000s

Although the Internet bubble may have been the biggest stock-market bubble in the United States, the bubble in single-family home prices that inflated during the early 2000s was undoubtedly the biggest U.S. real estate bubble. Moreover, the boom and later collapse in house prices had far greater significance for the average American than any gyrations in the stock market. The single-family home represents the largest asset in the portfolios of most ordinary investors, so falling home prices have an immediate impact on family wealth and sense of well-being. The deflation of the housing bubble almost brought down the U.S. (and international) financial system and ushered in a sharp worldwide recession. In order to understand how this bubble was financed and why it created such far-reaching collateral damage, we need to understand the fundamental changes in the banking and financial systems.

A story I like to tell concerns a middle-aged woman who has a serious heart attack. Lying in the emergency room, she has a near-death experience in which she comes face to face with God. “Is this it?” she asks. “Am I about to die?” God assures her that she will survive and has thirty more years to live. Sure enough, she does survive, gets stents put in to open up her clogged arteries, and feels better than ever. She then says to herself, “If I have thirty more years to live, I might as well make the most of it.” And since she’s already in the hospital, she decides to undergo what might charitably be called “comprehensive cosmetic surgery.” Now she looks and feels great. With a jaunty step she bounds out of the hospital, only to be hit by a speeding ambulance and instantly killed. She goes to the Pearly Gates and again meets God. “What happened?” she asks. “I thought I had thirty more years to live.” “I’m terribly sorry, Madam,” God responds. “I didn’t recognize you.”

If a financier had awakened from a thirty-year nap during the early 2000s, the financial system would have appeared unrecognizable. Under the old system, which might be called the “originate and hold” system, banks would make mortgage loans and hold those loans until they were repaid. In such an environment, bankers were very careful about the loans they made. After all, if a mortgage loan went into default, someone would come back to the loan officer and question the original credit judgment. In this environment, both substantial down payments and documentation were required to verify the creditworthiness of the borrower.

This system fundamentally changed in the early 2000s to what might be called the “originate and distribute” model of banking. Mortgage loans were still made by banks (as well as by big specialized mortgage companies). But the loans were held by the originating institution for only a few days, until they could be sold to an investment banker. The investment banker would then assemble packages of these mortgages and issue mortgage-backed securities—derivative bonds “securitized” by the underlying mortgages. These collateralized securities relied on the payments of interest and principal from the underlying mortgages to service the interest payment on the new mortgage-backed bonds.

To make matters even more complicated, there was not just one bond issued against a package of mortgages. The mortgage-backed securities were sliced into different “tranches,” each tranche with different claim priority against payments from the underlying mortgages and each with a different bond rating. It was called “financial engineering.” Even if the underlying mortgage loans were of low quality, the bond-rating agencies were happy to bestow an AAA rating on the bond tranches with the first claims on the payments from the underlying mortgages. The system should more accurately be called “financial alchemy,” and the alchemy was employed not only with mortgages but with all sorts of underlying instruments, such as credit card loans and automobile loans. These derivative securities were in turn sold all over the world.

It gets even murkier. Second-order derivatives were sold on the derivative mortgage-backed bonds. Credit-default swaps were issued as insurance policies on the mortgage-backed bonds. Briefly, the swap market allowed two parties—called counterparties—to bet for or against the performance of the mortgage bonds, or the bonds of any other issuer. For example, if I hold bonds issued by General Electric and I begin to worry about GE’s creditworthiness, I could buy an insurance policy from a company like AIG (the biggest issuer of default swaps) that would pay me if GE defaulted. The problem with this market was that the insurers had inadequate reserves to pay the claims if trouble occurred. And anyone from any country could buy the insurance without owning the underlying bonds. Eventually, the credit-default swaps trading in the market grew to a multiple of the value of the underlying bonds, pushed by demand from institutions around the world. This change made the world’s financial system very much riskier and much more interconnected.

To round out this dangerous picture, the financiers created structured investment vehicles, or SIVs, that kept derivative securities off their books, in places where the banking regulators couldn’t see them. The mortgage-backed security SIV would borrow the money needed to buy the derivatives, and all that showed up on the investment bank’s balance sheet was a small investment in the equity of the SIV. In the past, banking regulators might have flagged the vast leverage and the risk it carried, but that was overlooked in the new finance system.

This new system led to looser lending standards by bankers and mortgage companies. If the only risk a lender took was the risk that a mortgage loan would go bad in the few days before it could be sold to the investment banker, the lender did not need to consider the creditworthiness of the borrower. When I took out my first home mortgage, the lender insisted on a 30 percent down payment. But in the new system loans were made with no equity down, expecting that housing prices would rise forever. Moreover, so-called NINJA loans were common—those were loans to people with no income, no job, and no assets. Increasingly, lenders did not even bother to ask for documentation about ability to pay. Those were called NO-DOC loans. Money for housing was freely available, and housing prices rose rapidly.

The government itself played an active role in inflating the housing bubble. Under pressure by Congress to make mortgage loans easily available, the Federal Housing Administration was directed to subsidize the mortgages of low-income borrowers. Indeed, almost two-thirds of the bad mortgages in the financial system as of the start of 2010 were bought by government agencies. It was not simply “predatory lenders” but the government itself that caused many mortgage loans to be made to people who did not have the wherewithal to service them.

The combination of government policies and changed lending practices led to an enormous increase in the demand for houses. Fueled by easy credit, house prices began to rise rapidly. The initial rise in prices encouraged even more buyers. Buying houses or apartments appeared to be risk free as house prices appeared consistently to go up. And some buyers made their purchases with the objective not of finding a place to live but rather of quickly selling (flipping) the house to some future buyer at a higher price.

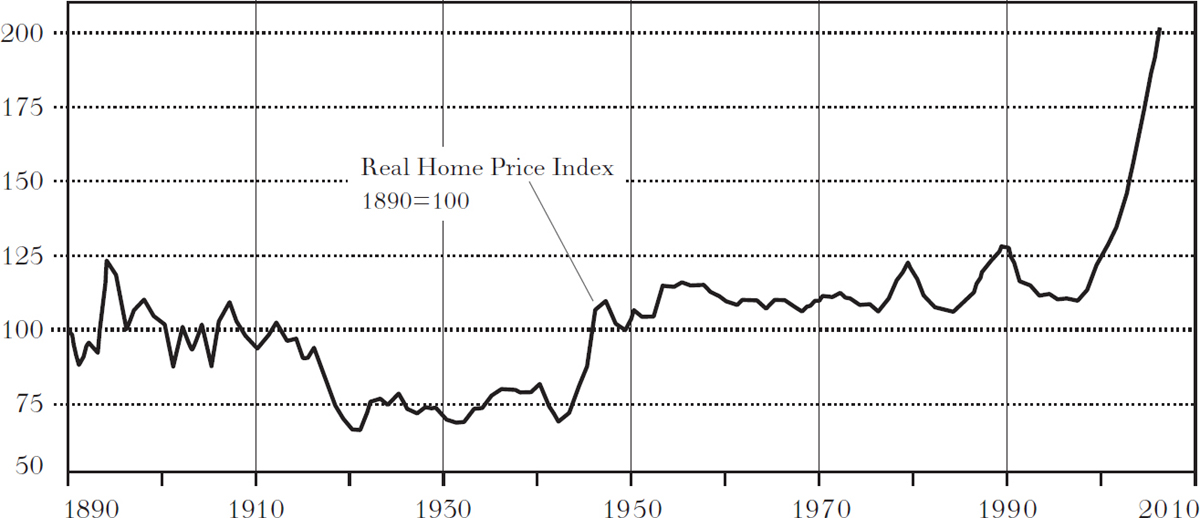

The graph on page 99 illustrates the dimensions of the bubble. The data come from the Case-Shiller inflation-adjusted home-price indexes. The adjustment works by considering that if house prices increased by 5 percent when prices in general increased by 5 percent, no inflation-adjusted housing price increase occurred. If house prices went up by 10 percent, however, then the inflation-adjusted price would be recorded as a 5 percent increase.

The graph shows that for the hundred-year period from the late 1800s to the late 1900s, inflation-adjusted house prices were stable. House prices went up, but only as much as the general price level. Prices did dip during the Great Depression of the 1930s, but they ended the century at about the same level at which they started. In the early 2000s, the house price index doubled. This index is a composite index of prices in twenty cities.

INFLATION-ADJUSTED HOME PRICES

Source: Case-Shiller.

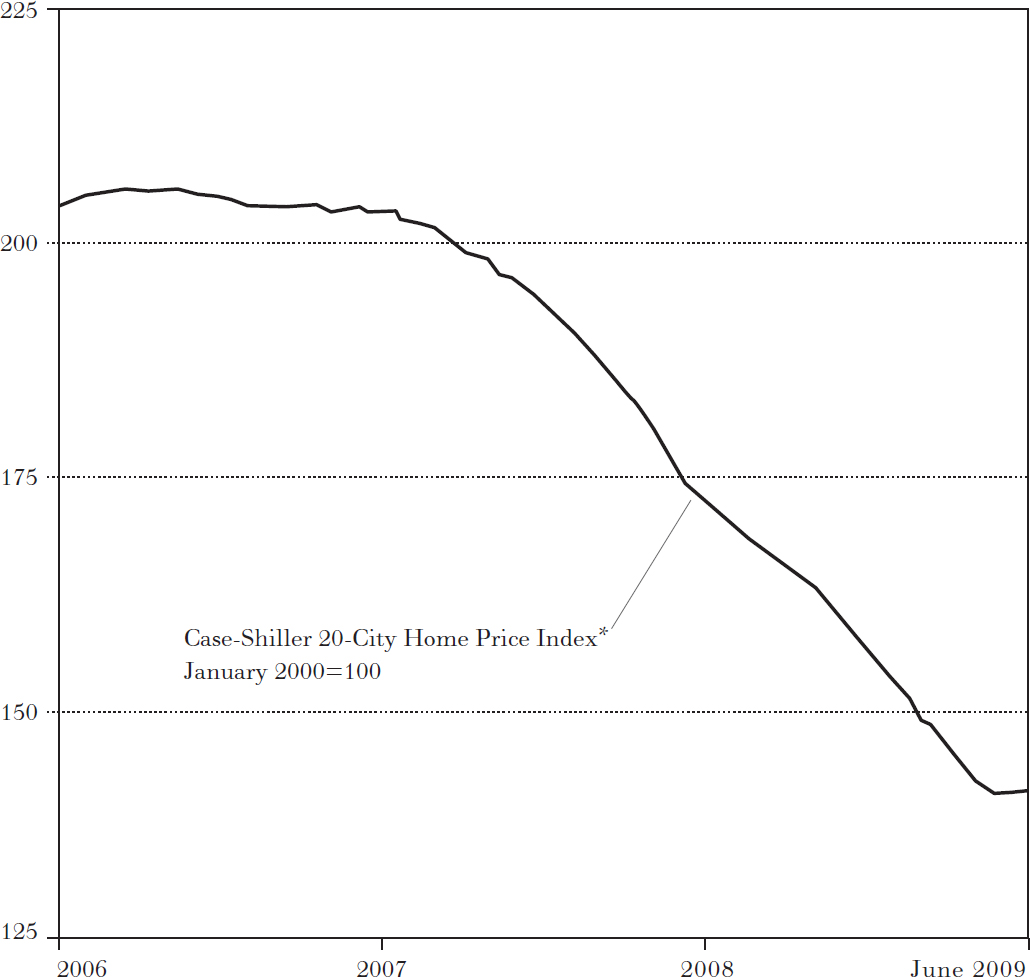

What we know about all bubbles is that eventually they pop. The next graph depicts the broad-based and devastating decline. Many home buyers found that the amount of their mortgage far exceeded the value of their home. Increasingly, they defaulted and returned the house keys to the lender. In an instance of macabre financial humor, bankers referred to this practice as “jingle mail.”

THE BURSTING OF THE BUBBLE

Data: Standard and Poor’s.

*Seasonally adjusted

The effects on the economy were devastating. As home equity collapsed, consumers pulled in their horns and went on a spending strike. And consumers who previously might have taken out a second mortgage or a home equity loan on their house were no longer able to finance their consumption in that manner.

The drop in house prices destroyed the value of the mortgage-backed securities as well as the financial institutions that had eaten their own cooking and held these toxic assets with borrowed money. Spectacular bankruptcies ensued, and some of our largest financial institutions had to be rescued by the government. Lending institutions turned full circle, and shut off credit to small businesses and consumers. The recession that followed was painful and prolonged, exceeded in its intensity only by the Great Depression of the 1930s.

Our survey of historical bubbles makes clear that the bursting of bubbles has often been followed by severe disruptions in real economic activity. The fallout from asset-price bubbles has not been confined to speculators. Bubbles are particularly dangerous when they are associated with a credit boom and widespread increases in leverage both for consumers and for financial institutions.

The housing bubble provides a dramatic illustration. Increased demand for housing raised home prices, which in turn encouraged further mortgage lending, which led to further price increases in a continuing positive feedback loop. The cycle of increased leverage involved loosening credit standards and even further increase in leverage. At the end of the process, individuals and institutions alike became dangerously vulnerable.

When the bubble bursts, the feedback loop goes into reverse. Prices decline and individuals find not only that their wealth has declined but that their mortgage indebtedness may exceed the value of their houses. Loans then go sour, and consumers reduce their spending. Overly leveraged financial institutions begin a deleveraging process. The attendant tightening of credit weakens economic activity, and the outcome of the negative feedback loop is a severe recession. Credit boom bubbles are the ones that pose the greatest danger to real economic activity.

Does This Mean That Markets Are Inefficient?

This chapter’s review of the Internet and housing bubbles seems inconsistent with the view that our stock and real estate markets are rational and efficient. The lesson, however, is not that markets occasionally can be irrational and that we should therefore abandon the firm-foundation theory of the pricing of financial assets. Rather, the clear conclusion is that, in every case, the market did correct itself. The market eventually corrects any irrationality—albeit in its own slow, inexorable fashion. Anomalies can crop up, markets can get irrationally optimistic, and often they attract unwary investors. But, eventually, true value is recognized by the market, and this is the main lesson investors must heed.

I am also persuaded by the wisdom of Benjamin Graham, author of Security Analysis, who wrote that in the final analysis the stock market is not a voting mechanism but a weighing mechanism. Valuation metrics have not changed. Eventually, every stock can only be worth the present value of its cash flow.

Markets can be highly efficient even if they make errors. Some are doozies, as when Internet stocks in the early 2000s appeared to discount not only the future but the hereafter. Forecasts are invariably incorrect. Moreover, investment risk is never clearly perceived, so the appropriate rate at which the future should be discounted is never certain. Thus, market prices must always be wrong. But at any particular time, it is not obvious to anyone (including professional investors) whether they are too high or too low. The best and the brightest on Wall Street cannot consistently distinguish correct valuations from incorrect ones. There is no evidence that anyone can generate excess returns by making consistently correct bets against the collective wisdom of the market. Markets are not always or even usually correct. But NO ONE PERSON OR INSTITUTION CONSISTENTLY KNOWS MORE THAN THE MARKET.

Nor does the unprecedented bubble and bust in house prices during the first decade of the 2000s drive a stake through the heart of the efficient-market hypothesis. If individuals are given an opportunity to buy houses with no money down, it can be the height of rationality to be willing to pay an inflated price. If the house rises in value, the buyer will profit. If the bubble bursts and the house price declines, the buyer walks away and leaves the lender (and perhaps ultimately the government) with the loss. Yes, the incentives were perverse, regulation was lax, and some government policies were ill considered. But in no sense was this sorry episode and the deep recession that followed caused by a blind faith in the efficient-market hypothesis.

A meme is an image, idea, or behavior that is mimicked and widely disseminated by the Internet. The most popular memes “go viral” through social media. A meme stock is one whose price is entirely determined by social sentiment as opposed to the company’s financial condition. One of the platforms at the center of the meme stock craze was WallStreetBets (WSB) on Reddit, with literally millions of followers. Other platforms such as Facebook and YouTube helped whip up an army of online stock traders.

The best example of the meme stock phenomenon was the epically insane rise and fall of the shares of GameStop (GME). GameStop was a struggling brick-and-mortar retailer of video game discs at a time when the distribution of such games was increasingly done online. Interest in GME was sparked by thirty-four-year-old track star Richard Gill, who was well known on Reddit as “Deep F---ing Value,” and as “Roaring Kitty” on YouTube. In addition to touting GME as a “turnaround” play, there was at least some logic to expect significant future buying of the shares. Hedge funds had made massive “short sales” of GME. A short sale is the sale of stock you don’t own in the hopes of profiting by buying it back at a cheaper price later. The hedge funds were so negative on GME that the number of shares sold short exceeded the total number of shares outstanding. “Roaring Kitty” correctly knew that eventually these shares had to be purchased to “cover” the short positions. By mobilizing an array of frenzied buyers, one could drive the price up. As the price rose, it would increase the loss of the hedge funds, who would then be forced to buy, pushing the stock price even higher. Thus there was a David-and-Goliath element to this tale. Some Redditers bought GME stock for no other reason than to screw the fat cats. And the frenzied buyers found they could leverage their bets by buying options on GME that could produce outsized profits if the stock rose further.

Traders in GameStop tended to follow the mantra “You Only Live Once.” The acronym was also used as a verb, as in a tweet saying, “I just YOLOd my life savings of $50,000 into GME options,” with screenshots of the individual’s actual brokerage account at Robinhood.

Whatever logic there may have been inciting the Internet mob, the price action of the stock was simply insane. GME’s share price started trading in January 2021 at $17 per share. By late in the month the price reached almost $400 a share before plunging below $40 in February. During the remainder of the year the price continued to fluctuate violently. Some traders, especially those who got in the game early, profited greatly. But most traders lost. For every dollar taken from the coffers of hedge funds, probably $20 was simply transferred from one hapless trader to another.

One GME trader, frustrated with his losses, consoled himself with the following tweet: “Investing in GameStock is worse than a divorce—You lose half your money and your wife is still with you.” Unfortunately, some of the outcomes were tragic rather than humorous. One Robinhood trader committed suicide when facing an apparent $730,000 loss from his options trading.

Another popular meme stock was the movie theater chain AMC. As all the theaters closed during the pandemic, AMC kept clinging to life by borrowing intensively to cover their losses. AMC was another heavily shorted stock. In early January 2021 the stock traded at less than $2 per share. By mid-year it sold at over $60. For the online trading community, it was better than going to Las Vegas. Again those who got in early made profits. But those who were still in when the music stopped lost heavily.

There is one paradox in this morality tale. In the case of GME and AMC, both companies issued more than a billion dollars each of new equity to take advantage of their soaring stock prices. The irony of this bizarre story is that the two companies were, at least temporarily, saved from failure by the behavior of an irrational mob. Whether we should be happy that the capital allocation process can be influenced by market participants trading stocks as if they were numbers on a roulette wheel is a more consequential question.

THE BUBBLES IN CRYPTOCURRENCIES

Perhaps the most uninhibited trading in the early decades of the 2000s did not involve stocks. The immense public interest in bitcoin and other digital currencies spurred massive worldwide trading activity and unprecedented volatility in market prices. The rise in prices for the cryptocurrencies and the way they captured the imagination of the public were eerily similar to the madness that accompanied the dot.com bubble.

Bitcoin, the worldwide cryptocurrency, has variously been labeled the “currency of the future” or a “worthless fraud,” whose growth resembles that of a pyramid scheme and could turn out to be one of the greatest financial bubbles of all time. The price of a bitcoin has oscillated dramatically, rising from pennies per digital token to $20,000 at the end of 2017. A year later it sold for less than $4,000. In April 2021 bitcoin traded at prices well above $60,000. Two months later it sold for under $30,000. It has fluctuated by 50 percent in a matter of months. No wonder it appealed to the Reddit mob.

Bitcoin was created by an unknown person or persons writing under the pseudonym “Satoshi Nakamoto.” The goal was to create a “purely peer-to-peer version of electronic cash,” as he wrote in a white paper published in 2008. The elusive Nakamoto communicated only by email and social media. While several people have been identified as Nakamoto, the real identity of the bitcoin creator has never been confirmed. After creating the original rules for the bitcoin network and releasing the accompanying software in 2009, Nakamoto disappeared two years later. He was reported to own a million tokens, which quickly became worth billions of dollars, making him one of the richest people in the world.

The bitcoin system works through a secure public ledger called a blockchain. A coded and password-protected (but anonymous) entry on the ledger records ownership of the bitcoin. The blockchain provides proof of who owns the tokens at any time as well as the payment history of every bitcoin in circulation. The network is maintained by independent computers around the world. The payment for maintaining these computers and processing new transactions is made in bitcoin in a process known as bitcoin mining. All the tokens in existence were created by this process. There is a maximum limit of 21 million tokens in circulation.*

The blockchain is a continually growing public ledger of records, referred to as blocks, that are linked to previous blocks and that document transactions on the network. Copies are spread around the computers or “nodes” of the network so that anyone can check if anything is amiss. This keeps the network honest. If some party helping to maintain the database tried to alter their own copy of the records to add money to their own account, other computers would recognize the discrepancy. Conflicts are resolved by consensus and a strong encryption system has thus far made the network secure.

By 2022 there were millions of unique users, and both legal and illegal transactions were completed through the bitcoin protocol. The level of the bitcoin exchange rate does not matter. Transactions can be completed whether the bitcoin is worth one dollar or $100,000. One can buy the cryptocurrency and simultaneously send it to a vendor who can convert it immediately into dollars. As long as the bitcoin does not fluctuate in value during the short period in which the transaction takes place, the dollar value does not matter. The argument for the disruptive technology involved is that it can allow for seamless and anonymous transactions without the need to go through the banking system and without the use of national currencies.

Traditional finance professionals have been deeply skeptical of the cryptocurrency phenomenon. Legendary investors such as Howard Marks and Warren Buffett have suggested that the cryptocurrencies are not real and have no value. But the same can be said for any national currency. A dollar bill has no intrinsic value. All paper currencies suffer from various degrees of skepticism, although they are not normally disparaged as a kind of Ponzi scheme. So let’s examine whether bitcoin and other digital currencies should be considered money or not.

What is the definition of money? This may seem an odd question but in fact it raises some subtle issues with respect to bitcoin. For an economist, money is what money does. Money performs three functions in the economy. First, it is a medium of exchange. We value money because it enables us to buy goods and services. We keep cash in our wallet so that we can buy a sandwich for lunch and a can of soda when we are thirsty.

Second, money is a unit of account, the yardstick that is needed to post prices and record debts now and in the future. The New York Times cost $3.00 in 2021. If I take out a $100,000 interest-only mortgage at a 5 percent interest rate, my yearly interest payments will be $5,000, and I will owe $100,000 when the loan matures.

Third, money is a store of value. A seller may accept money for the sale of a good or service because she can use the money to buy something in the future. While she might hold another asset such as common stock to store value, money is the most liquid asset available. Money is the preferred asset to hold for making purchases that are likely to be required over the immediate future.

How well does the bitcoin meet the traditional requirements needed for an asset to be considered money? Bitcoin appears to some extent to meet the first requirement. It is accepted worldwide for many different types of transactions. And while the authentication process is cumbersome, it could potentially involve lower transaction costs for some types of international business dealings. For transactions that border on the illegal, it also provides an anonymity that participants value and that undoubtedly makes it the preferred payment vehicle. And it may give the holder somewhat greater assurance that it will be harder to confiscate by some government authority in a country with weak property rights. It is not surprising that most of the early trading in cryptocurrencies has occurred in Asian countries where fears of confiscation are the strongest.

It is the extreme volatility in the value of the bitcoin that makes it fail the second and third common definitions of money. An asset that gains and loses a substantial percentage of its initial value each day will serve neither as a useful unit of account nor as a dependable store of value. There is no natural anchor for the value of a cryptocurrency. For those who seek to avoid the risk of assuming the high volatility in the bitcoin marketplace, a further transaction—converting the bitcoin into an asset or national currency whose value is more stable—will be required. At least for the U.S. dollar and most of the world’s major currencies, there is a central bank whose goals involve maintaining the stability of the value of the currency.

The situation reminds me of the classic story of the sardine trader who kept a warehouse full of cans of sardines. One day a hungry worker opened one of the cans, hoping for a tasty lunch, but found that the can was filled with sand. Confronting the trader, the worker was told that the cans were for trading, not for eating. It appears that the story applies to bitcoin as well.

For most traders of bitcoin and other cryptocurrencies, the game was a speculative bet that the price will continue to soar. For those who got into the game early, the rewards have been enormous. Remember the 6'5" Olympic rower twins Cameron and Tyler Winklevoss, who accused Mark Zuckerberg of stealing their idea for Facebook when they attended Harvard College? The twins’ lawsuit was settled for $65 million and Zuckerberg went on to become a billionaire from his holdings of Facebook (now Meta Platforms) stock. Don’t feel too bad for the twins, who thought they deserved more money. They took $11 million of the settlement and invested in bitcoin at $120 per token. Soon the twins became bitcoin billionaires.

Should the Bitcoin Phenomenon Be Called a Bubble?

So what do we conclude? Are we witnessing the dawn of a promising new technology that will greatly improve the international payments mechanism? Or is this simply another speculative bubble that will lead many of the participants to financial ruin? Perhaps the answer is yes to both questions. The blockchain technology behind the bitcoin phenomenon is real, and improved versions could become more widespread. In any event, the international payments mechanism will be profoundly changed by technology.

The promise of the blockchain and similar “distributed ledger” technologies is that the systems can be used for other purposes such as medical records and a history of vehicle repairs. The state of Delaware, which has made a business of incorporating companies from all over the world, has been working on the use of blockchains for corporate record keeping. Dubai has announced that it wants to have all governmental documents eventually secured on a blockchain. Similar kinds of decentralized record keeping are associated with other cryptocurrencies that have proliferated after the success of bitcoin.

Technology does have the potential to reduce transactions costs and increase transactions speed. Digital currencies can facilitate secure transactions between sellers and buyers without the mediation of either financial institutions or governments. But because an underlying phenomenon is “real” does not mean that it is not susceptible to “bubble” pricing. The promise of the Internet was real in the late 1990s but that did not prevent a company like Cisco Systems, which made the switches and routers making up the “backbone of the Internet,” from losing 90 percent of its value when the bubble burst. And there are clear indications that the rise in the prices of bitcoin and other digital currencies represents a classic bubble.

One indication of a speculative bubble is the extent to which the price of the object rises. In a short period of time the price of a bitcoin rose from pennies to almost $20,000 in early 2017 before quickly plummeting. During 2021, Bitcoin ranged in price from a low of $28,800 to a high of almost $69,000. The tokens have been extremely volatile, rising or falling by as much as a third in a single twenty-four-hour period. Prices of other cryptocurrencies have followed similar patterns. The price increase far exceeded that of tulip bulbs in seventeenth-century Holland, and none of the bubbles described earlier in this book came close to approximating the inflation of bitcoin prices. Both the magnitude of the price increases and their volatility are suggestive of one of the biggest bubbles in history.

Bubbles are propagated by attractive stories that become part of the popular culture. The bitcoin story is an ideal example of how a meme has generated special enthusiasm among millennials and GenZers. It is also the story of how the Internet facilitates the progagation of memes and intensifies financial bubbles.

What Can Make the Bitcoin Bubble Deflate?

A large number of risks suggest extreme caution in assessing the future of bitcoin. Bitcoin mining operations use considerable computer power and are energy intensive. Restrictions can be imposed on the computers that run the public distributed ledger central to the transactions network. Creating a single token requires as much electricity as the typical American household consumes in two years. The total network of computers comprising the bitcoin network consumes as much energy each year as some medium-sized countries.

Bitcoin enthusiasts often made their case by emphasizing that the total size of the token market was capped at 21 million. But the argument was flawed. There is no cap on the competing cryptocurrencies that proliferated. Supporters of Ethereum and its currency called “Ether” would argue that it is superior to bitcoin. The Ethereum protocol is designed to provide more flexibility and increased functionality. Ripple, and its coin “XRP,” was specifically created to improve international transactions by reducing costs and speeding up transaction times. The total size of all cryptocurrencies in the market is unlimited. The tulip-bulb bubble burst when “investors” and speculators in bulbs finally decided to cash in their profits. Holders of large amounts of bitcoin are called “whales,” and they can send prices plummeting by selling even a small portion of their holdings.

The use of bitcoin to facilitate illegal transactions creates particular dangers for the currency. When “ransomware” and other illegal activities, including tax evasion, become enabled by the cryptocurrency, we cannot expect governments to stand by idly. Nor will governments be willing to give up control of their national currencies. From Beijing to Washington, it would be unwise to bet against government efforts to smother the mining and trading of bitcoin. Governments themselves will be more likely than other private enterprises to sponsor the widely accepted digital currencies of the future.

Mini-bubbles continued to proliferate in the 2020s. Three of my favorites were SPACs, another digital currency called the Dogecoin, and NFTs.

Remember the laughable new issue during the South Sea Bubble: “A company for carrying out an undertaking of great advantage, but nobody to know what it is.” This is an almost perfect description of Special Acquisition Companies. SPACs are formed to raise capital in an initial public offering for the sole purpose of acquiring one or more private companies. The SPAC itself is not an operational company. It exists only as a temporary cash box to identify some unknown company to merge with and indirectly take public. The SPAC provides a way of going public through the back door. In 2020, 248 SPACs were formed, raising $83 billion in equity capital and becoming one of the fastest growing financial instruments in the world.

SPACs advertise themselves as offering quick riches and a way to let the ordinary investor into the lucrative IPO market. In fact most of the riches go to the SPAC sponsor, who often gets 20 percent of the SPAC stock, leaving the public buyers of the SPAC only the remaining fraction. All too often the SPAC also becomes a way to take dodgy companies public without their having to overcome the careful scrutiny of the Securities and Exchange Commission. Most of the SPACs have lost money for their public investors even during some of the most ebullient equity markets in history.

My next favorite mini-bubble, the Dogecoin, started as a joke. Two friends in a chatroom invented the coin as a way to mock the success of bitcoin and the bizarre craze surrounding the trading of cryptocurrencies. The name was taken from the “doge” Internet meme of the talking Shiba Inu dog. Dogecoin’s creators expected that their coin would prove amusing but quickly be forgotten. But the joke was picked up by the Reddit crowd and quickly rose to stardom. On January 1, 2021, the coin traded at ½ cent. By May it jumped to 75 cents before falling sharply after crypto enthusiast Elon Musk ridiculed it on Saturday Night Live. Supporters on Reddit were not deterred. The common thread in the community of Doge fans: “You Only Live Once,” written as “YOLO,” and “We Are Going to the Moon.”

The list of mini-bubbles kept growing in the 2020s. One of the most consequential was the faddish Nonfungible Token. The NFT is a unique virtual certificate of ownership that is stored on a blockchain and can be bought and sold in the market. Mike Winkelman, a digital artist who goes by the name Beeple, sold a tokenized collection of his art at Christie’s auction house for $69 million even though a JPEG of the images could be freely downloaded on the Internet. A proliferation of NFTs followed from CryptoKitties to digital sneakers. A Charmin NFT was sold as the world’s first nonfungible toilet paper. Jack Dorsey, the CEO of Twitter, sold the first tweet on the platform for $3 million as an NFT.

Perhaps the most absurd NFT of all was launched in January 2022 by reality star Stephanie Matto. Stephanie began her entrepreneurial career by bottling her farts in jars to sell to her fans. She would consume several bowls of black bean soup to be able to keep up with the skyrocketing demand. But after she experienced sharp chest pains, her doctor advised her that windbreaking was taking a dangerous toll on her body. She then shifted her business model to producing digital art works featuring her fart jars. People collect all sorts of things and many collectibles rise in price over time. But most lose value. For myself, I’d rather have a Picasso.

We have reviewed centuries of history documenting how the madness of crowds has inflated asset prices and led the unwary to financial ruin. The clear lesson of history is that eventually all excessively exuberant markets succumb to the laws of gravity. The consistent losers in the market, from my personal experience, are those who are unable to resist being swept up in some kind of tulip-bulb craze. And there is abundant empirical evidence that most day traders lose money. It is not hard, really, to make money in the market. As we shall see later, an investor who simply buys and holds a broad-based portfolio of stocks can make reasonably generous long-run returns. What is hard to avoid is the alluring temptation to throw your money away on short, get-rich-quick speculative binges.

I have no objection to people who like to gamble—I enjoy gambling myself. But if you do so, gamble with small amounts of money you can afford to lose. Do not confuse gambling with investing, and never commit your retirement savings to some currently popular technologies that promise to transform the world. Investments in transforming technologies, especially those that are wildly popular, have usually proved unrewarding for investors.

The lessons of history are immutable. Speculative bubbles will persist. But they ultimately lead most of their participants to financial ruin. Even real technology revolutions do not guarantee benefits for investors. The ability to avoid horrendous investing mistakes is probably the most important factor in preserving one’s capital and allowing it to grow. The lesson is so obvious and yet so easy to ignore.

* When the maximum limit is reached a different method of payment for maintaining the network will be required, such as the sharing of transaction fees.