SPECULATIVE BUBBLES FROM THE SIXTIES INTO THE NINETIES

Everything’s got a moral if only you can find it.

—Lewis Carroll, Alice’s Adventures in Wonderland

THE MADNESS OF the crowd can be truly spectacular. The examples I have just cited, plus a host of others, have persuaded more and more people to put their money under the care of professional portfolio managers—those who run the large pension and retirement funds, mutual funds, and investment counseling organizations. Although the crowd may be mad, the institution is above all that. Very well, let us then take a look at the sanity of institutions.

By the 1990s, institutions accounted for more than 90 percent of the trading volume on the New York Stock Exchange. One would think that the hardheaded, sharp-penciled reasoning of the pros would guarantee that the extravagant excesses of the past would no longer exist. And yet professional investors participated in several distinct speculative movements from the 1960s through the 1990s. In each case, professional institutions bid actively for stocks not because they felt such stocks were undervalued under the firm-foundation principle, but because they anticipated that some greater fools would take the shares off their hands at even more inflated prices. Because these speculative movements relate to present-day markets, I think you’ll find this institutional tour especially useful.

The New “New Era”: The Growth-Stock/New-Issue Craze

We start our journey when I did—in 1959, when I had just gone to Wall Street. “Growth” was the magic word in those days, taking on an almost mystical significance. Growth companies such as IBM and Texas Instruments sold at price-earnings multiples of more than 80. (A year later they sold at multiples in the 20s and 30s.)

Questioning the propriety of such valuations became almost heretical. Though these prices could not be justified on firm-foundation principles, investors believed that buyers would still eagerly pay even higher prices. Lord Keynes must have smiled quietly from wherever it is that economists go when they die.

I recall vividly one of the senior partners of my firm shaking his head and admitting that he knew of no one with any recollection of the 1929–32 crash who would buy and hold the high-priced growth stocks. But the young Turks held sway. Newsweek quoted one broker as saying that speculators have the idea that anything they buy “will double overnight. The horrible thing is, it has happened.”

More was to come. Promoters, eager to satisfy the insatiable thirst of investors for the space-age stocks of the Soaring Sixties, created more new issues in the 1959–62 period than at any previous time in history. The new-issue mania rivaled the South Sea Bubble in its intensity and also, regrettably, in the fraudulent practices that were revealed.

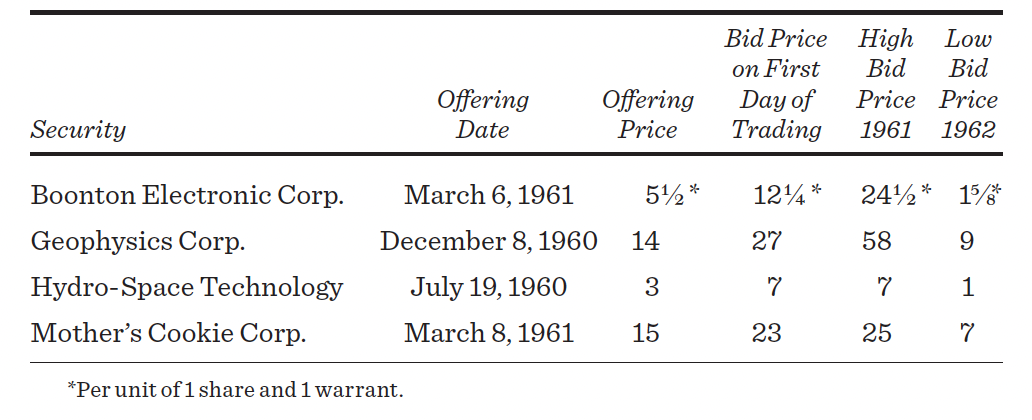

It was called the tronics boom, because the stock offerings often included some garbled version of the word “electronics” in their title, even if the companies had nothing to do with the electronics industry. Buyers of these issues didn’t really care what the companies made—so long as it sounded electronic, with a suggestion of the esoteric. For example, American Music Guild, whose business consisted entirely of the door-to-door sale of phonograph records and players, changed its name to Space-Tone before “going public.” The shares were sold to the public at 2 and, within a few weeks, rose to 14.

Jack Dreyfus, of Dreyfus and Company, commented on the mania as follows:

Take a nice little company that’s been making shoelaces for 40 years and sells at a respectable six times earnings ratio. Change the name from Shoelaces, Inc. to Electronics and Silicon Furth-Burners. In today’s market, the words “electronics” and “silicon” are worth 15 times earnings. However, the real play comes from the word “furth-burners,” which no one understands. A word that no one understands entitles you to double your entire score. Therefore, we have six times earnings for the shoelace business and 15 times earnings for electronic and silicon, or a total of 21 times earnings. Multiply this by two for furth-burners and we now have a score of 42 times earnings for the new company.

Let the numbers below tell the story. Even Mother’s Cookie could count on a sizable gain. Think of the glory it could have achieved if it had called itself Mothertron’s Cookitronics. Ten years later, the shares of most of these companies were almost worthless. Today, none exist.

Where was the Securities and Exchange Commission (SEC) all this time? Aren’t new issuers required to register their offerings with the SEC? Can’t they (and their underwriters) be punished for false and misleading statements? Yes, the SEC was there, but by law it had to stand by quietly. As long as a company has prepared (and distributed to investors) an adequate prospectus, the SEC can do nothing to save buyers from themselves. For example, many of the prospectuses of the period contained the following type of warning in bold letters on the cover.

WARNING: THIS COMPANY HAS NO ASSETS OR EARNINGS AND WILL BE UNABLE TO PAY DIVIDENDS IN THE FORESEEABLE FUTURE. THE SHARES ARE HIGHLY RISKY.

But just as the warnings on packs of cigarettes do not prevent many people from smoking, so the warning that this investment may be dangerous to your wealth cannot block a speculator from forking over his money. The SEC can warn fools, but it cannot keep them from parting with their money. And the buyers of new issues were so convinced the stocks would rise in price that the underwriter’s problem was not how he could sell the shares but how to allocate them among the frenzied purchasers.

Fraud and market manipulation are different matters. Here the SEC can take and has taken strong action. Indeed, many of the little-known brokerage houses on the fringes of respectability, which were responsible for most of the new issues and for manipulation of their prices, were suspended for a variety of peculations.

The tronics boom came back to earth in 1962. Yesterday’s hot issue became today’s cold turkey. Many professionals refused to accept the fact that they had speculated recklessly. Very few pointed out that it is always easy to look back and say when prices were too high or too low. Fewer still said that no one seems to know the proper price for a stock at any given time.

Synergy Generates Energy: The Conglomerate Boom

Part of the genius of the financial market is that if a product is demanded, it is produced. The product that all investors desired was expected growth in earnings per share. If growth couldn’t be found in a name, it was a good bet that someone would find another way to produce it. By the mid-1960s, creative entrepreneurs suggested that growth could be created by synergism.

Synergism is the quality of having 2 plus 2 equal 5. Thus, two separate companies with an earning power of $2 million each might produce combined earnings of $5 million if the businesses were consolidated. This magical, surefire new creation was called a conglomerate.

Although antitrust laws at that time kept large companies from purchasing firms in the same industry, it was possible to purchase firms in other industries without Justice Department interference. The consolidations were carried out in the name of synergism. Ostensibly, the conglomerate would achieve higher sales and earnings than would have been possible for the independent entities alone.

In fact, the major impetus for the conglomerate wave of the 1960s was that the acquisition process itself could be made to produce growth in earnings per share. Indeed, the managers of conglomerates tended to possess financial expertise rather than the operating skills required to improve the profitability of the acquired companies. By an easy bit of legerdemain, they could put together a group of companies with no basic potential at all and produce steadily rising per-share earnings. The following example shows how this monkey business was performed.

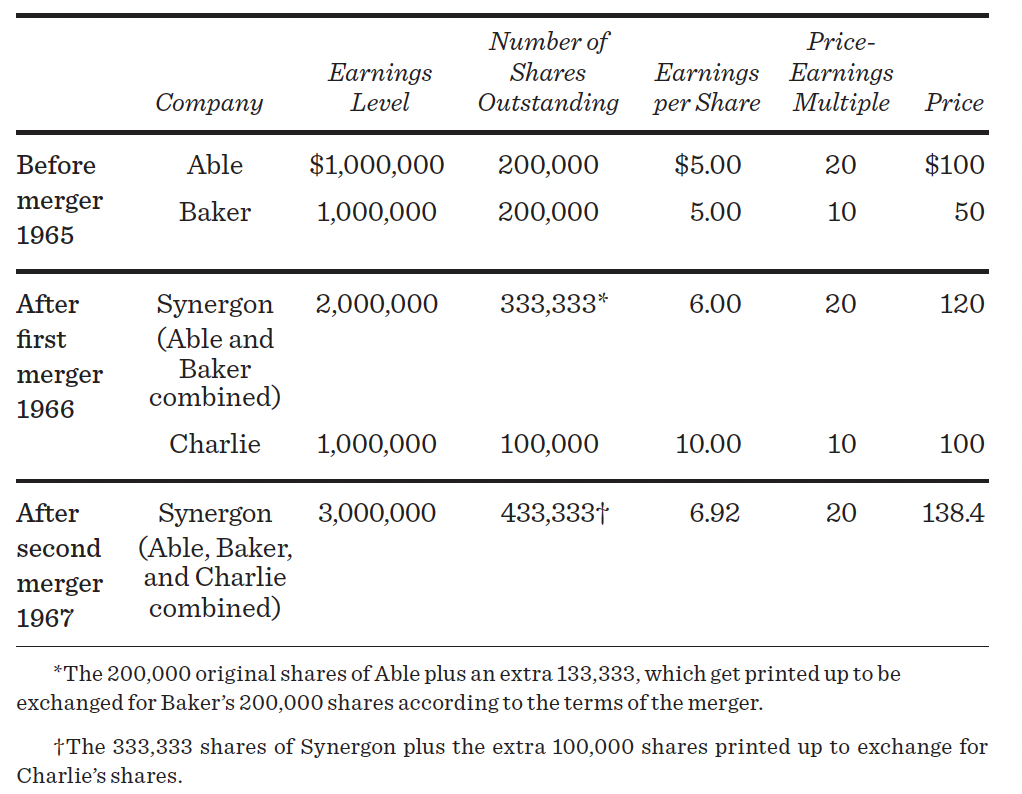

Suppose we have two companies—the Able Circuit Smasher Company, an electronics firm, and Baker Candy Company, which makes chocolate bars. Each has 200,000 shares outstanding. It’s 1965 and both companies have earnings of $1 million a year, or $5 per share. Let’s assume that neither business is growing and that, with or without merger activity, earnings would just continue along at the same level.

The two firms sell at different prices, however. Because Able Circuit Smasher Company is in the electronics business, the market awards it a price-earnings multiple of 20, which, multiplied by its $5 earnings per share, gives it a market price of $100. Baker Candy Company, in a less glamorous business, has its earnings multiplied at only 10 times and, consequently, its $5 per-share earnings command a market price of only $50.

The management of Able Circuit would like to become a conglomerate. It offers to absorb Baker by swapping stock at the rate of two for three. The holders of Baker shares would get two shares of Able stock—which have a market value of $200—for every three shares of Baker stock—with a total market value of $150. Clearly, Baker’s stockholders are likely to accept cheerfully.

We have a budding conglomerate, newly named Synergon, Inc., which now has 333,333 shares outstanding and total earnings of $2 million to put against them, or $6 per share. Thus, by 1966, when the merger has been completed, we find that earnings have risen by 20 percent, from $5 to $6, and this growth seems to justify Able’s former price-earnings multiple of 20. Consequently, the shares of Synergon (née Able) rise from $100 to $120, and everyone goes home rich and happy. In addition, the shareholders of Baker who were bought out need not pay any taxes on their profits until they sell their shares of the combined company. The top three lines of the table on page 69 illustrate the transaction.

A year later, Synergon finds Charlie Company, which earns $10 per share, or $1 million with 100,000 shares outstanding. Charlie Company is in the relatively risky military-hardware business, so its shares command a multiple of only 10 and sell at $100. Synergon offers to absorb Charlie Company on a share-for-share exchange basis. Charlie’s shareholders are delighted to exchange their $100 shares for the conglomerate’s $120 shares. By the end of 1967, the combined company has $3 million in earnings, 433,333 shares outstanding, and $6.92 of earnings per share.

Here we have a case where the conglomerate has literally manufactured growth. None of the three companies was growing at all; yet simply by virtue of their merger, our conglomerate will show the following earnings growth:

Synergon is a growth stock, and its record of extraordinary performance appears to have earned it a high and possibly even an increasing multiple of earnings.

The trick that makes the game work is the ability of the electronics company to swap its high-multiple stock for the stock of another company with a lower multiple. The candy company can “sell” its earnings only at a multiple of 10. But when these earnings are averaged with those of the electronics company, the total earnings (including those from selling chocolate bars) could be sold at a multiple of 20. And the more acquisitions Synergon could make, the faster earnings per share would grow and thus the more attractive the stock would look to justify its high multiple.

The whole thing is like a chain letter—no one would get hurt as long as the growth of acquisitions proceeded exponentially. Although the process could not continue for long, the possibilities were mind-boggling for those who got in at the start. It seems difficult to believe that Wall Street professionals could fall for the conglomerate con game, but accept it they did for a period of several years. Or perhaps as subscribers to the castle-in-the-air theory, they only believed that other people would fall for it.

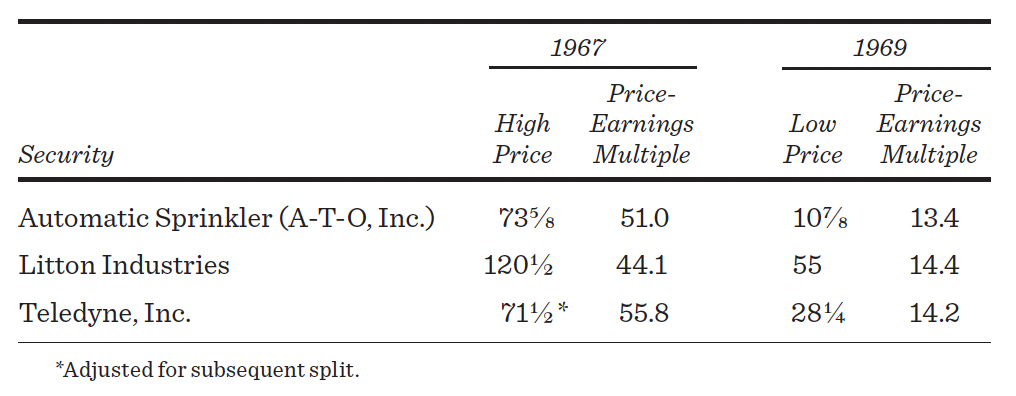

Automatic Sprinkler Corporation (later called A-T-O, Inc., and later still, at the urging of its modest chief executive officer Mr. Figgie, Figgie International) is a real example of how the game of manufacturing growth was actually played. Between 1963 and 1968, the company’s sales volume rose by more than 1,400 percent, a phenomenal record due solely to acquisitions. In the middle of 1967, four mergers were completed in a twenty-five-day period. These newly acquired companies, all selling at relatively low price-earnings multiples, helped to produce a sharp growth in earnings per share. The market responded to this “growth” by bidding up the price-earnings multiple to more than 50 times earnings in 1967 and the company’s stock price from about $8 per share in 1963 to $73⅝ in 1967.

Mr. Figgie, the president of Automatic Sprinkler, performed the public relations job necessary to help Wall Street build its castle in the air. He automatically sprinkled his conversations with talismanic phrases about the energy of the free-form company and its interface with change and technology. He was careful to point out that he looked at twenty to thirty deals for each one he bought. Wall Street loved every word of it.

Mr. Figgie was not alone in conning Wall Street. Managers of other conglomerates almost invented a new language in the process of dazzling the investment community. They talked about market matrices, core technology fulcrums, modular building blocks, and the nucleus theory of growth. No one from Wall Street really knew what the words meant, but they all got the nice, warm feeling of being in the technological mainstream.

Conglomerate managers also found a new way of describing the businesses they had bought. Their shipbuilding businesses became “marine systems.” Zinc mining became the “space minerals division.” Steel fabrication plants became the “materials technology division.” A lighting fixture or lock company became part of the “protective services division.” And if one of the “ungentlemanly” security analysts (somebody from City College of New York rather than Harvard Business School) had the nerve to ask how you can get 15 to 20 percent growth from a foundry or a meat packer, he was told that efficiency experts had isolated millions of dollars of excess costs; that marketing research had found several fresh, uninhabited markets; and that profit margins could be easily tripled within two years. Instead of going down with merger activity, the price-earnings multiples of conglomerate stocks rose for a while. Prices and multiples for a selection of conglomerates in 1967 are shown in the following table.

The music slowed drastically for the conglomerates on January 19, 1968, when the granddaddy of the conglomerates, Litton Industries, announced that earnings for the second quarter of that year would be substantially less than had been forecast. It had recorded 20 percent yearly increases for almost a decade. The market had so thoroughly come to believe in alchemy that the announcement was greeted with disbelief and shock. In the selling wave that followed, conglomerate stocks declined by roughly 40 percent before a feeble recovery set in.

Worse was to come. In July, the Federal Trade Commission announced that it would make an in-depth investigation of the conglomerate merger movement. Again the stocks went tumbling down. The SEC and the accounting profession finally made their move and began to make attempts to clarify the reporting techniques for mergers and acquisitions. The sell orders came flooding in. Shortly afterwards, the SEC and the U.S. Assistant Attorney General in charge of antitrust indicated a strong concern about the accelerating pace of the merger movement.

The aftermath of this speculative phase revealed two disturbing factors. First, conglomerates could not always control their far-flung empires. Indeed, investors became disenchanted with the conglomerate’s new math; 2 plus 2 certainly did not equal 5, and some investors wondered whether it even equaled 4. Second, the government and the accounting profession expressed concern about the pace of mergers and about possible abuses. These two worries reduced—and in many cases eliminated—the premium multiples that had been paid in anticipation of earnings growth from the acquisition process alone. This result in itself makes the alchemy game almost impossible, for the acquiring company has to have an earnings multiple larger than the acquired company if the ploy is to work at all.

An interesting footnote to this episode is that during the first two decades of the 2000s deconglomeration came into fashion. Spin-offs of company subsidiaries into separate companies were as a rule rewarded with rising stock prices. The two distinct companies usually had a higher combined market value than the original conglomerate.

In the 1970s, Wall Street’s pros vowed to return to “sound principles.” Concepts were out and blue-chip companies were in. They would never come crashing down like the speculative favorites of the 1960s. Nothing could be more prudent than to buy their shares and then relax on the golf course.

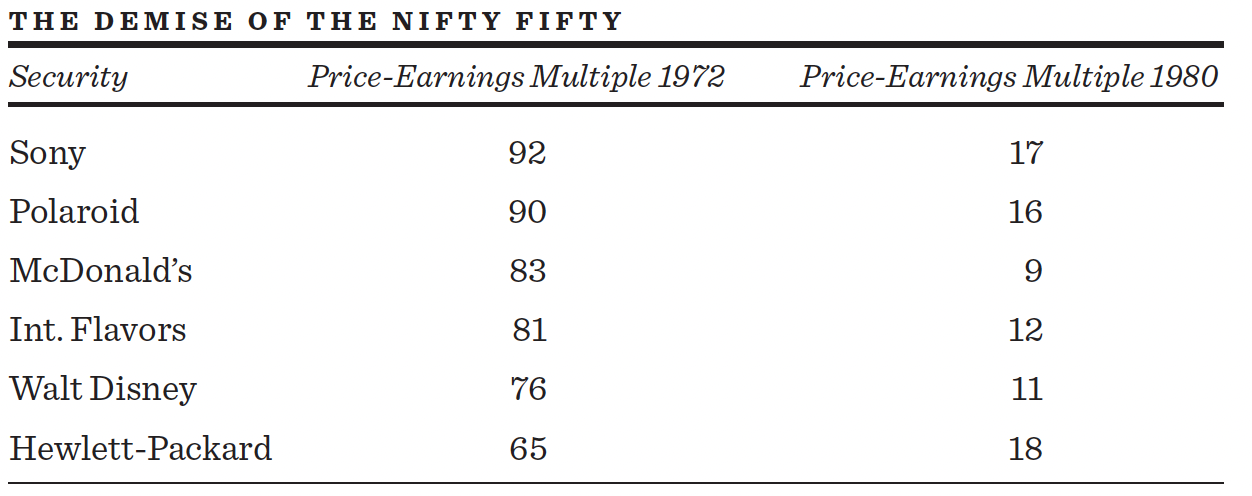

There were only four dozen or so of these premier growth stocks. Their names were familiar—IBM, Xerox, Avon Products, Kodak, McDonald’s, Polaroid, and Disney—and they were called the Nifty Fifty. They were “big capitalization” stocks, which meant that an institution could buy a good-sized position without disturbing the market. And because most pros realized that picking the exact correct time to buy is difficult if not impossible, these stocks seemed to make a great deal of sense. So what if you paid a price that was temporarily too high? These stocks were proven growers, and sooner or later the price would be justified. In addition, these were stocks that—like the family heirlooms—you would never sell. Hence they also were called “one decision” stocks. You made a decision to buy them, once, and your portfolio-management problems were over.

These stocks provided security blankets for institutional investors in another way, too. They were respectable. Your colleagues could never question your prudence in investing in IBM. True, you could lose money if IBM went down, but that was not considered a sign of imprudence. Like greyhounds in chase of the mechanical rabbit, big pension funds, insurance companies, and bank trust funds loaded up on the Nifty Fifty one-decision growth stocks. Hard as it is to believe, institutions started to speculate in blue chips. The table below tells the story. Institutional managers blithely ignored the fact that no sizable company could ever grow fast enough to justify an earnings multiple of 80 or 90. They once again proved the maxim that stupidity well packaged can sound like wisdom.

The Nifty Fifty craze ended like all other speculative manias. The same money managers who had worshiped the Nifty Fifty decided that the stocks were overpriced and made a second decision—to sell. In the debacle that followed, the premier growth stocks fell completely from favor.

The high-technology, new-issue boom of the first half of 1983 was an almost perfect replica of the 1960s episodes, with the names altered slightly to include the new fields of biotechnology and microelectronics. The 1983 craze made the promoters of the 1960s look like pikers. The total value of new issues during 1983 was greater than the cumulative total of new issues for the entire preceding decade.

Take, for example, a company that “planned” to mass-produce personal robots, called Androbot, and a chain of three restaurants in New Jersey called Stuff Your Face, Inc. Indeed, the enthusiasm extended to “quality” issues such as Fine Art Acquisitions Ltd. This was not some philistine outfit peddling discount clothing or making computer hardware. This was a truly aesthetic enterprise. Fine Art Acquisitions, the prospectus tells us, was in the business of acquiring and distributing fine prints and Art Deco sculpture replicas. One of the company’s major assets consisted of a group of nude photographs of Brooke Shields taken about midway between her time in the stroller and her entrance to Princeton. The pictures were originally owned by—this is absolutely true—a man named Garry Gross. While Fine Arts saw nothing wrong with the pictures of the prepubescent eleven-year-old Brooke, her mother did. The ending, in this case, was a happy one for Brooke: the pictures were returned to Gross and never sold by Fine Arts. The ending was not quite as blissful for Fine Arts, or for most of the other new issues ushered in during the craze. Fine Arts morphed into Dyansen Corporation, complete with gallery in the glitzy Trump Tower, and eventually defaulted on its debt in 1993.

Probably the offering of Muhammad Ali Arcades International burst the bubble. This offering was not particularly remarkable, considering all the other garbage coming out at the time. It was unique, however, in that it showed that a penny could still buy a lot. The company proposed to offer units of one share and two warrants for the modest price of 1¢. Of course, this was 333 times what insiders had recently paid for their own shares, which wasn’t unusual either, but when it was discovered that the champ himself had resisted the temptation to buy any stock in his namesake company, investors began to take a good look at where they were. Most did not like what they saw. The result was a 90 percent decline in small-company stocks in general and in the market prices of initial public offerings in particular.

The prospectus cover of Muhammad Ali Arcades International featured a picture of the former champ standing over a fallen opponent. In his salad days, Ali used to claim that he could “float like a butterfly and sting like a bee.” It turned out that the Ali Arcades offering (as well as the Androbot offering that was scheduled for July 1983) never did get floated. But many others did, particularly stocks of those companies on the bleeding edge of technology, and it was the investors who got stung.

The saga of ZZZZ Best is an incredible Horatio Alger story that captivated investors. In the fast-paced world of entrepreneurs who strike it rich before they can shave, Barry Minkow was a genuine legend of the 1980s. Minkow’s career began at age nine. His family could not afford a babysitter, so Barry often went to work at the carpet-cleaning shop managed by his mother. There he began soliciting jobs by phone. By age ten he was actually cleaning carpets. Working evenings and summers, he saved $6,000 within the next four years, and by age fifteen bought some steam-cleaning equipment and started his own carpet-cleaning business in the family’s garage. The company was called ZZZZ Best (pronounced “zeee best”). Still in high school and too young to drive, Minkow hired a crew to pick up and clean carpets while he sat in class fretting over each week’s payroll. With Minkow working a punishing schedule, the business flourished. He was proud of the fact that he hired his father and mother to work for the business. By age eighteen, Minkow was a millionaire.

Minkow’s insatiable appetite for work extended to self-promotion. He drove a red Ferrari and lived in a lavish home with a large pool, which had a big black Z painted on the bottom. He wrote a book entitled Making It in America, in which he claimed that teenagers didn’t work hard enough. He appeared on Oprah as the boy genius of Wall Street and recorded antidrug commercials with the slogan “My act is clean, how’s yours?” By this time, ZZZZ Best had 1,300 employees and locations throughout California as well as in Arizona and Nevada.

Was more than 100 times earnings too much to pay for a mundane carpet-cleaning company? Of course not, when the company was run by a spectacularly successful businessman, who could also show his toughness. Minkow’s favorite line to his employees was “My way or the highway.” And he once boasted that he would fire his own mother if she stepped out of line. When Minkow told Wall Street that his company was better run than IBM and that it was destined to become “the General Motors of carpet cleaning,” investors listened raptly. As one security analyst told me, “This one can’t miss.”

In 1987, Minkow’s bubble burst with shocking suddenness. It turned out that ZZZZ Best was cleaning more than carpets—it was also laundering money for the mob. ZZZZ Best was accused of acting as a front for organized-crime figures who would buy equipment for the company with “dirty” money and replace their investment with “clean” cash skimmed from the proceeds of ZZZZ Best’s legitimate carpet-cleaning business. The spectacular growth of the company was produced with fictitious contracts, phony credit card charges, and the like. The operation was a giant Ponzi scheme in which money was recycled from one set of investors to pay off another. Minkow was also charged with skimming millions from the company treasury for his own personal use. Minkow and all the investors in ZZZZ Best were in wall-to-wall trouble.

The next chapter of the story (after chapter 11) occurred in 1989 when Minkow, then twenty-three, was convicted of fifty-seven counts of fraud, sentenced to twenty-five years in prison, and required to make restitution of $26 million he was accused of stealing from the company. The U.S. district judge, in rejecting pleas for leniency, told Minkow, “You are dangerous because you have this gift of gab, this ability to communicate.” The judge added, “You don’t have a conscience.”

But the story does not end there. Minkow spent fifty-four months in Lompoc Federal Prison, where he became a born-again Christian, earning bachelor’s and master’s correspondence school degrees from Liberty University, founded by Jerry Falwell. After his release in December 1994, he became senior pastor at Community Bible Church in California, where he held his congregation in rapt attention with his evangelical style. He wrote several books, including Cleaning Up and Down, But Not Out. He was also hired as a special adviser for the FBI on how to spot fraud. In 2006, Minkow’s prosecutor, James Asperger, wrote, “Barry has made a remarkable turnaround—both in his personal life and in uncovering more fraud than he ever perpetrated.” In 2010, the movie Minkow was filmed. It was billed as “a powerful tale of redemption and inspiration.” Unfortunately, the movie story was pure fiction, and its release was cancelled. In 2011, Minkow was sentenced to five years in prison for involvement in a securities fraud; in 2014, he pleaded guilty to embezzling $3 million from the San Diego Community Bible Church, where he had been pastor. Minkow never reformed. But the film was finally released in March 2018, albeit with a different title: Con Man.

The lessons of market history are clear. Styles and fashions in investors’ evaluations of securities can and often do play a critical role in the pricing of securities. The stock market at times conforms well to the castle-in-the-air theory. For this reason, the game of investing can be extremely dangerous.

Another lesson that cries out for attention is that investors should be very wary of purchasing today’s hot “new issue.” Most initial public offerings underperform the stock market as a whole. And if you buy the new issue after it begins trading, usually at a higher price, you are even more certain to lose.

Certainly investors in the past have built many castles in the air with IPOs. Remember that the major sellers of the stock of IPOs are the managers of the companies themselves. They try to time their sales to coincide with a peak in the prosperity of their companies or with the height of investor enthusiasm. In such cases, the urge to get on the bandwagon—even in high-growth industries—produced a profitless prosperity for investors.

The Japanese Yen for Land and Stocks

So far, I have covered only U.S. speculative bubbles. It is important to note that we are not alone. Indeed, one of the largest booms and busts of the late twentieth century involved the Japanese real estate and stock markets. From 1955 to 1990, the value of Japanese real estate increased more than 75 times. By 1990, the total value of all Japanese property was estimated at nearly $20 trillion—equal to more than 20 percent of the entire world’s wealth and about double the total value of the world’s stock markets. America is twenty-five times bigger than Japan in terms of physical acreage, and yet Japan’s property in 1990 was appraised to be worth five times as much as all American property. Theoretically, the Japanese could have bought all the property in America by selling off metropolitan Tokyo. Just selling the Imperial Palace and its grounds at their appraised value would have raised enough cash to buy all of California.

The stock market countered by rising like a helium balloon on a windless day. Stock prices increased 100-fold from 1955 to 1990. At their peak, in December 1989, Japanese stocks had a total market value of about $4 trillion, almost 1.5 times the value of all U.S. equities and close to 45 percent of the world’s equity-market capitalization. Firm-foundation investors were aghast that Japanese stocks sold at more than 60 times earnings, almost 5 times book value, and more than 200 times dividends. In contrast, U.S. stocks sold at about 15 times earnings, and London equities sold at 12 times earnings. The value of NTT Corporation, Japan’s telephone giant, exceeded the value of AT&T, IBM, Exxon, General Electric, and General Motors put together.

Supporters of the stock market had answers to all the logical objections that could be raised. Were price-earnings ratios in the stratosphere? “No,” said the salespeople at Kabuto-cho (Japan’s Wall Street). “Japanese earnings are understated relative to U.S. earnings because depreciation charges are overstated and earnings do not include the earnings of partially owned affiliated firms.” Price-earnings multiples adjusted for these effects would be much lower. Were yields, at well under ½ of 1 percent, unconscionably low? The answer was that this simply reflected the low interest rates at the time in Japan. Was it dangerous that stock prices were five times the value of assets? Not at all. The book values did not reflect the dramatic appreciation of the land owned by Japanese companies. And the high value of Japanese land was “explained” by both the density of Japanese population and the various regulations and tax laws restricting the use of habitable land.

In fact, none of the “explanations” could hold water. Even when earnings were adjusted, the multiples were still far higher than in other countries and extraordinarily inflated relative to Japan’s own history. Moreover, Japanese profitability had been declining, and the strong yen was bound to make it more difficult for Japan to export. Although land was scarce in Japan, its manufacturers, such as its auto makers, were finding abundant land for new plants at attractive prices in foreign lands. And rental income had been rising far more slowly than land values, indicating a falling rate of return on real estate. Finally, the low interest rates that had been underpinning the market had already begun to rise in 1989.

Much to the distress of those speculators who had concluded that the fundamental laws of financial gravity were not applicable to Japan, Isaac Newton arrived there in 1990. Interestingly, it was the government itself that dropped the apple. The Bank of Japan (Japan’s Federal Reserve) saw the ugly specter of a general inflation stirring amid the borrowing frenzy and the liquidity boom underwriting the rise in land and stock prices. And so the central bank restricted credit and engineered a rise in interest rates. The hope was that further rises in property prices would be choked off and the stock market might be eased downward.

The stock market was not eased down; instead, it collapsed. The fall was almost as extreme as the U.S. stock-market crash from the end of 1929 to mid-1932. The Japanese (Nikkei) stock-market index reached a high of almost 40,000 on the last trading day of the 1980s. By mid-August 1992, the index had declined to 14,309, a drop of about 63 percent. The following chart shows dramatically that the rise in stock prices during the mid- and late 1980s represented a change in valuation relationships. The fall in stock prices from 1990 on simply reflected a return to the price-to-book-value relationships that were typical in the early 1980s. The Japanese stock market remained depressed for the next several decades. At the start of 2022, the Nikkei sold at under 29,000, substantially below where it sold more than thirty years earlier.

The air also rushed out of the real estate balloon during the early 1990s. Various measures of land prices and property values indicate a decline roughly as severe as that of the stock market. The financial laws of gravity know no geographic boundaries.

THE JAPANESE STOCK-MARKET BUBBLE JAPANESE STOCK PRICES RELATIVE TO BOOK VALUES, 1980–2000

Source: Morgan Stanley Research and author’s estimates.