October. This is one of the peculiarly dangerous months to speculate in stocks in. The others are July, January, September, April, November, May, March, June, December, August and February.

—Mark Twain, Pudd’nhead Wilson

GREED RUN AMOK has been an essential feature of every spectacular boom in history. In their frenzy, market participants ignore firm foundations of value for the dubious but thrilling assumption that they can make a killing by building castles in the air. Such thinking has enveloped entire nations.

The psychology of speculation is a veritable theater of the absurd. Several of its plays are presented in this chapter. The castles that were built during the performances were based on Dutch tulip bulbs, English “bubbles,” and good old American blue-chip stocks. In each case, some of the people made money some of the time, but only a few emerged unscathed.

History, in this instance, does teach a lesson: Although the castle-in-the-air theory can well explain such speculative binges, outguessing the reactions of a fickle crowd is a most dangerous game. “In crowds it is stupidity and not mother-wit that is accumulated,” Gustave Le Bon noted in his 1895 classic on crowd psychology. It would appear that not many have read the book. Skyrocketing markets that depend on purely psychic support have invariably succumbed to the financial law of gravitation. Unsustainable prices may persist for years, but eventually they reverse themselves. Such reversals come with the suddenness of an earthquake; and the bigger the binge, the greater the resulting hangover. Few of the reckless builders of castles in the air have been nimble enough to anticipate these reversals and to escape when everything came tumbling down.

The tulip-bulb craze was one of the most spectacular get-rich-quick binges in history. Its excesses become even more vivid when one realizes that it happened in staid old Holland in the early seventeenth century. The events leading to this speculative frenzy were set in motion in 1593 when a newly appointed botany professor from Vienna brought to Leyden a collection of unusual plants that had originated in Turkey. The Dutch were fascinated with this new addition to the garden—but not with the professor’s asking price (he had hoped to sell the bulbs and make a handsome profit). One night a thief broke into the professor’s house and stole the bulbs, which were subsequently sold at a lower price but at greater profit.

Over the next decade or so, the tulip became a popular but expensive item in Dutch gardens. Many of these flowers succumbed to a nonfatal virus known as mosaic. It was this mosaic that helped to trigger the wild speculation in tulip bulbs. The virus caused the tulip petals to develop contrasting colored stripes or “flames.” The Dutch valued highly these infected bulbs, called bizarres. In a short time, popular taste dictated that the more bizarre a bulb, the greater the cost of owning it.

Slowly, tulipmania set in. At first, bulb merchants simply tried to predict the most popular variegated style for the coming year, much as clothing manufacturers do in gauging the public’s taste in fabric, color, and hemlines. Then they would buy an extra-large stockpile to anticipate a rise in price. Tulip-bulb prices began to rise wildly. The more expensive the bulbs became, the more people viewed them as smart investments. Charles Mackay, who chronicled these events in his book Extraordinary Popular Delusions and the Madness of Crowds, noted that the ordinary industry of the country was dropped in favor of speculation in tulip bulbs: “Nobles, citizens, farmers, mechanics, seamen, footmen, maid-servants, even chimney sweeps and old clotheswomen dabbled in tulips.” Everyone imagined that the passion for tulips would last forever.

People who said the prices could not possibly go higher watched with chagrin as their friends and relatives made enormous profits. The temptation to join them was hard to resist. In the last years of the tulip spree, which lasted approximately from 1634 to early 1637, people started to barter their personal belongings, such as land, jewels, and furniture, to obtain the bulbs that would make them even wealthier. Bulb prices reached astronomical levels.

Part of the genius of financial markets is that when there is a real demand for a method to enhance speculative opportunities, the market will surely provide it. The instruments that enabled tulip speculators to get the most action for their money were “call options” similar to those popular today in the stock market.

A call option conferred on the holder the right to buy tulip bulbs (call for their delivery) at a fixed price (usually approximating the current market price) during a specified period. He was charged an amount called the option premium, which might run 15 to 20 percent of the current market price. An option on a tulip bulb currently worth 100 guilders, for example, would cost the buyer only about 20 guilders. If the price moved up to 200 guilders, the option holder would exercise his right; he would buy at 100 and simultaneously sell at the then current price of 200. He then had a profit of 80 guilders (the 100 guilders appreciation less the 20 guilders he paid for the option). Thus, he enjoyed a fourfold increase in his money, whereas an outright purchase would only have doubled his money. Options provide one way to leverage one’s investment to increase the potential rewards as well as the risks. Such devices helped to ensure broad participation in the market. The same is true today.

The history of the period was filled with tragicomic episodes. One such incident concerned a returning sailor who brought news to a wealthy merchant of the arrival of a shipment of new goods. The merchant rewarded him with a breakfast of fine red herring. Seeing what he thought was an onion on the merchant’s counter, and no doubt thinking it very much out of place amid silks and velvets, he proceeded to take it as a relish for his herring. Little did he dream that the “onion” would have fed a whole ship’s crew for a year. It was a costly Semper Augustus tulip bulb. The sailor paid dearly for his relish—his no longer grateful host had him imprisoned for several months on a felony charge.

Historians regularly reinterpret the past, and some financial historians who have reexamined the evidence about various financial bubbles have argued that considerable rationality in pricing may have existed after all. One of these revisionist historians, Peter Garber, has suggested that tulip-bulb pricing in seventeenth-century Holland was far more rational than is commonly believed.

Garber makes some good points, and I do not mean to imply that there was no rationality at all in the structure of bulb prices during the period. The Semper Augustus, for example, was a particularly rare and beautiful bulb and, as Garber reveals, was valued greatly even in the years before the tulipmania. Moreover, Garber’s research indicates that rare individual bulbs commanded high prices even after the general collapse of bulb prices, albeit at levels that were only a fraction of their peak prices. But Garber can find no rational explanation for such phenomena as a twentyfold increase in tulip-bulb prices during January of 1637 followed by an even larger decline in prices in February. Apparently, as happens in all speculative crazes, prices eventually got so high that some people decided they would be prudent and sell their bulbs. Soon others followed suit. Like a snowball rolling downhill, bulb deflation grew at an increasingly rapid pace, and in no time at all panic reigned.

Government ministers stated officially that there was no reason for tulip bulbs to fall in price—but no one listened. Dealers went bankrupt and refused to honor their commitments to buy tulip bulbs. A government plan to settle all contracts at 10 percent of their face value was frustrated when bulbs fell even below this mark. And prices continued to decline. Down and down they went until most bulbs became almost worthless—selling for no more than the price of a common onion.

Suppose your broker has called you and recommended that you invest in a new company with no sales or earnings—just great prospects. “What business?” you say. “I’m sorry,” your broker explains, “no one must know what the business is, but I can promise you enormous riches.” A con game, you say. Right you are, but 300 years ago in England this was one of the hottest new issues of the period. And, just as you guessed, investors got very badly burned. The story illustrates how fraud can make greedy people even more eager to part with their money.

At the time of the South Sea Bubble, the British were ripe for throwing away money. A long period of prosperity had resulted in fat savings and thin investment outlets. In those days, owning stock was considered something of a privilege. As late as 1693, for example, only 499 souls benefited from ownership of East India stock. They reaped rewards in several ways, not least of which was that their dividends were untaxed. Also, their number included women, for stock represented one of the few forms of property that British women could possess in their own right. The South Sea Company, which obligingly filled the need for investment vehicles, had been formed in 1711 to restore faith in the government’s ability to meet its obligations. The company took on a government IOU of almost £10 million. As a reward, it was given a monopoly over all trade to the South Seas. The public believed immense riches were to be made in such trade and regarded the stock with distinct favor.

From the very beginning, the South Sea Company reaped profits at the expense of others. Holders of the government securities to be assumed by the company simply exchanged their securities for those of the South Sea Company. Those with prior knowledge of the plan quietly bought up government securities selling as low as £55 and then turned them in at par for £100 worth of South Sea stock when the company was incorporated. Not a single director of the company had the slightest experience in South American trade. This did not stop them from quickly outfitting African slave ships (the sale of slaves being one of the most lucrative features of South American trade). But even this venture did not prove profitable, because the mortality rate on the ships was so high.

The directors were, however, wise in the art of public appearance. An impressive house in London was rented, and the boardroom was furnished with thirty black Spanish upholstered chairs whose beechwood frames and gilt nails made them handsome to look at but uncomfortable to sit in. In the meantime, a shipload of company wool that was desperately needed in Vera Cruz was sent instead to Cartagena, where it rotted on the wharf for lack of buyers. Still, the stock of the company held its own and even rose modestly over the next few years despite the dilutive effect of “bonus” stock dividends and a war with Spain that led to a temporary collapse in trading opportunities. John Carswell, the author of an excellent history, The South Sea Bubble, wrote of John Blunt, a director and one of the prime promoters of the securities of the South Sea Company, that “he continued to live his life with a prayer-book in his right hand and a prospectus in his left, never letting his right hand know what his left hand was doing.”

Across the Channel, another company was formed by an exiled Englishman named John Law. Law’s goal in life was to replace metal as money and create more liquidity through a national paper currency. (Bitcoin promotors are following a long tradition.) To further his purpose, Law acquired a derelict concern called the Mississippi Company and proceeded to build a conglomerate that became one of the largest capital enterprises ever to exist.

The Mississippi Company attracted speculators and their money from throughout the Continent. The word “millionaire” was invented at this time, and no wonder: The price of Mississippi stock rose from £100 to £2,000 in just two years, even though there was no logical reason for such an increase. At one time the inflated total market value of the stock of the Mississippi Company in France was more than eighty times that of all the gold and silver in the country.

Meanwhile, back on the English side of the Channel, a bit of jingoism now began to appear in some of the great English houses. Why should all the money be going to the French Mississippi Company? What did England have to counter this? The answer was the South Sea Company, whose prospects were beginning to look a bit better, especially with the news that there would be peace with Spain and hence the way to the South American trade would at last be clear. Mexicans supposedly were waiting for the opportunity to empty their gold mines in return for England’s abundant supply of cotton and woolen goods. This was free enterprise at its finest.

In 1720, the directors, an avaricious lot, decided to capitalize on their reputation by offering to fund the entire national debt, amounting to £31 million. This was boldness indeed, and the public loved it. When a bill to that effect was introduced in Parliament, the stock promptly rose from £130 to £300.

Various friends and backers who had shown interest in getting the bill passed were rewarded with free stock grants that could be “sold” back to the company when the price went up, with the individual collecting the profit. Among those rewarded were George I’s mistress and her “nieces,” all of whom bore a startling resemblance to the king.

On April 12, 1720, five days after the bill became law, the South Sea Company sold a new issue of stock at £300. The issue could be bought on the installment plan—£60 down and the rest in eight easy payments. Even the king could not resist; he subscribed for stock totaling £100,000. Fights broke out among other investors surging to buy. To ease the public appetite, the South Sea directors announced another new issue—this one at £400. But the public was ravenous. Within a month the stock was £550. On June 15 yet another issue was floated. This time the payment plan was even easier—10 percent down and not another payment for a year. The stock hit £800. Half the House of Lords and more than half the House of Commons signed on. Eventually, the price rose to almost £1,000. The speculative craze was in full bloom.

Not even the South Sea Company was capable of handling the demands of all the fools who wanted to be parted from their money. Investors looked for other new ventures where they could get in on the ground floor. Just as speculators today search for the next Microsoft, so in England in the early 1700s they looked for the next South Sea Company. Promoters obliged by organizing and bringing to the market a flood of new issues to meet the insatiable craving for investment.

As the days passed, new financing proposals ranged from ingenious to absurd—from importing a large number of jackasses from Spain (even though there was an abundant supply in England) to making salt water fresh. Increasingly the promotions involved some element of fraud, such as making boards out of sawdust. There were nearly one hundred different projects, each more extravagant and deceptive than the other, but each offering the hope of immense gain. They soon received the name of “bubbles,” as appropriate a name as could be devised. Like bubbles, they popped quickly—usually within a week or so.

The public, it seemed, would buy anything. New companies seeking financing during this period were organized for such purposes as the building of ships against pirates; encouraging the breeding of horses in England; trading in human hair; building hospitals for bastard children; extracting silver from lead; extracting sunlight from cucumbers; and even producing a wheel of perpetual motion.

The prize, however, must surely go to the unknown soul who started “A Company for carrying on an undertaking of great advantage, but nobody to know what it is.” The prospectus promised unheard-of rewards. At nine o’clock in the morning, when the subscription books opened, crowds of people from all walks of life practically beat down the door in an effort to subscribe. Within five hours, one thousand investors handed over their money for shares in the company. Not being greedy himself, the promoter promptly closed up shop and set off for the Continent. He was never heard from again.

Not all investors in the bubble companies believed in the feasibility of the schemes to which they subscribed. People were “too sensible” for that. They did believe, however, in the “greater fool” theory—that prices would rise, that buyers would be found, and that they would make money. Thus, most investors considered their actions the height of rationality, expecting that they could sell their shares at a premium in the “after market,” that is, the trading market in the shares after their initial issue.

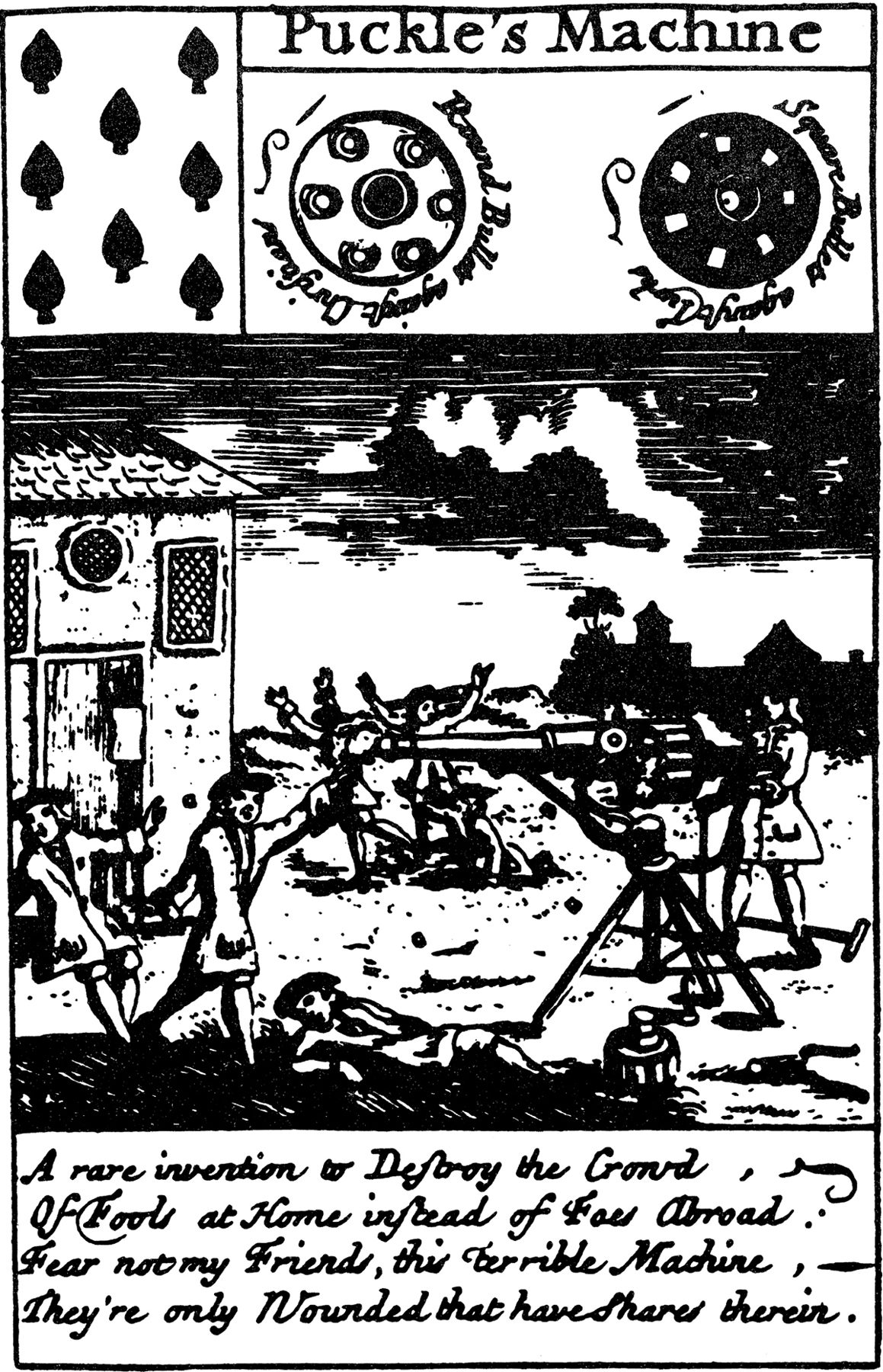

Whom the gods would destroy, they first ridicule. Signs that the end was near appeared with the issuance of a pack of South Sea playing cards. Each card contained a caricature of a bubble company, with an appropriate verse inscribed underneath. One of these, the Puckle Machine Company, was supposed to produce machines discharging both round and square cannonballs and bullets. Puckle claimed that his machine would revolutionize the art of war. The eight of spades, shown on the following page, described it as follows:

A rare invention to destroy the crowd,

Of fools at home instead of foes abroad:

Fear not my friends, this terrible machine,

They’re only wounded that have shares therein.

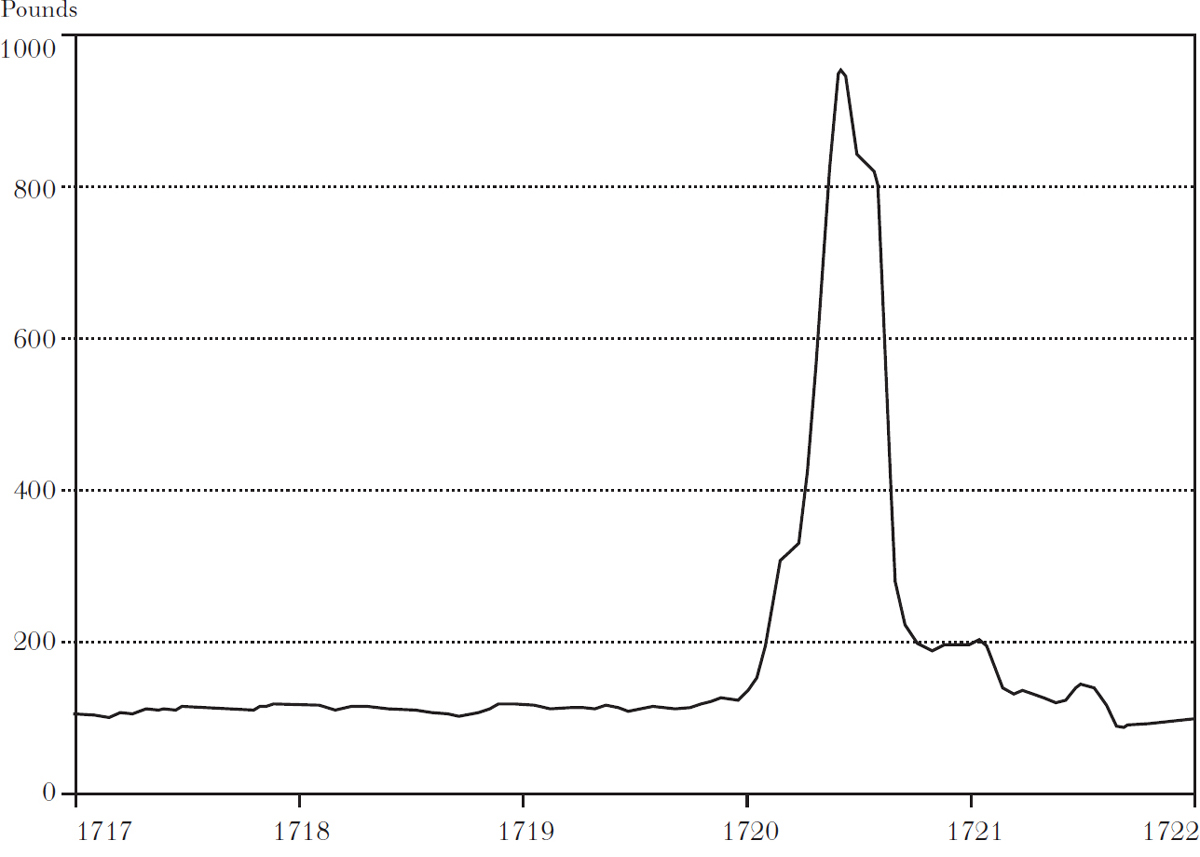

Many individual bubbles had been pricked without dampening the speculative enthusiasm, but the deluge came in August with an irreparable puncture to the South Sea Company. Realizing that the price of the shares in the market bore no relationship to the real prospects of the company, the directors and officers sold out in the summer.

The news leaked and the stock fell. Soon the price of the shares collapsed and panic reigned. The chart below shows the spectacular rise and fall of the stock of the South Sea Company. Government officials tried in vain to restore confidence, and a complete collapse of the public credit was barely averted. Similarly, the price of Mississippi Company shares fell to a pittance as the public realized that an excess of paper currency creates no real wealth, only inflation. Big losers in the South Sea Bubble included Isaac Newton, who is reported to have said, “I can calculate the motions of heavenly bodies, but not the madness of people.” So much for castles in the air.

To protect the public from further abuses, Parliament passed the Bubble Act, which forbade the issuing of stock certificates by companies. For more than a century, until the act was repealed in 1825, there were relatively few share certificates in the British market.

BRITISH SOUTH SEA COMPANY PRICE, 1717–1722

Source: Larry Neal, The Rise of Financial Capitalism (Cambridge University Press, 1990).

The bulbs and bubbles are, admittedly, ancient history. Could the same sort of thing happen in more modern times? Let’s turn to more recent events. America, the land of opportunity, had its turn in the 1920s. And given our emphasis on freedom and growth, we produced one of the most spectacular booms and loudest crashes civilization has ever known.

Conditions could not have been more favorable for a speculative craze. The country had been experiencing unrivaled prosperity. One could not but have faith in American business, and as Calvin Coolidge said, “The business of America is business.” Businessmen were likened to religious missionaries and almost deified. Such analogies were even made in the opposite direction. Bruce Barton, of the New York advertising agency Batten, Barton, Durstine & Osborn, wrote in The Man Nobody Knows that Jesus was “the first businessman” and that his parables were “the most powerful advertisements of all time.”

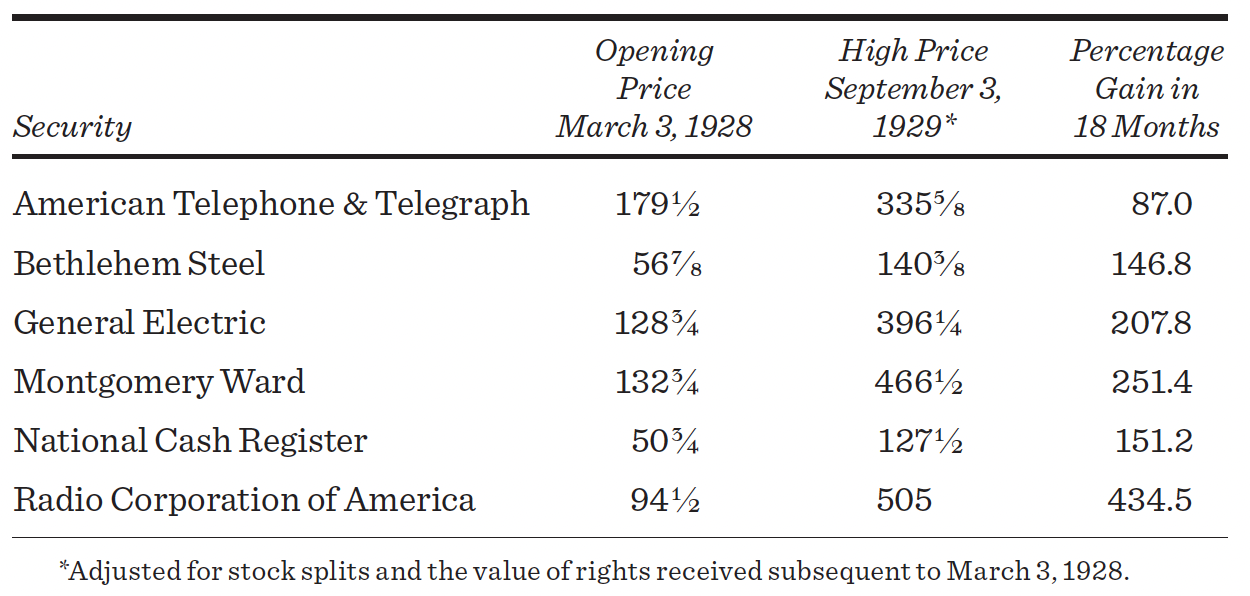

In 1928, stock-market speculation became a national pastime. From early March 1928 through early September 1929, the market’s percentage increase equaled that of the entire period from 1923 through early 1928. Stock prices of major industrial corporations sometimes rose 10 or 15 points per day. The price increases are illustrated in the table below.

Not “everybody” was speculating in the market. Borrowing to buy stocks (buying on margin) did increase from $1 billion in 1921 to almost $9 billion in 1929. Nevertheless, only about one million people owned stocks on margin in 1929. Still, the speculative spirit was at least as widespread as in the previous crazes and was certainly unrivaled in its intensity. More important, stock-market speculation was central to the culture. John Brooks, in Once in Golconda,* recounted the remarks of a British correspondent newly arrived in New York: “You could talk about Prohibition, or Hemingway, or air conditioning, or music, or horses, but in the end you had to talk about the stock market, and that was when the conversation became serious.”

Unfortunately, there were hundreds of smiling operators only too glad to help the public construct castles in the air. Manipulation on the stock exchange set new records for unscrupulousness. No better example can be found than the operation of investment pools. One such undertaking raised the price of RCA stock 61 points in four days.

An investment pool required close cooperation on the one hand and complete disdain for the public on the other. Generally such operations began when a number of traders banded together to manipulate a particular stock. They appointed a pool manager (who justifiably was considered something of an artist) and promised not to double-cross each other through private operations.

The pool manager accumulated a large block of stock through inconspicuous buying over a period of weeks. If possible, he also obtained an option to buy a substantial block of stock at the current market price. Next he tried to enlist the stock’s exchange specialist as an ally.

Pool members were in the swim with the specialist on their side. A stock-exchange specialist functions as a broker’s broker. If a stock was trading at $50 a share and you gave your broker an order to buy at $45, the broker typically left that order with the specialist. If and when the stock fell to $45, the specialist then executed the order. All such orders to buy below the market price or sell above it were kept in the specialist’s supposedly private “book.” Now you see why the specialist could be so valuable to the pool manager. The book gave information about the extent of existing orders to buy and sell at prices below and above the current market. It was always helpful to know as many of the cards of the public players as possible. Now the real fun was ready to begin.

Generally, at this point the pool manager had members of the pool trade among themselves. For example, Haskell sells 200 shares to Sidney at 40, and Sidney sells them back at 40⅛. The process is repeated with 400 shares at prices of 40¼ and 40½. Next comes the sale of a 1,000-share block at 40⅝, followed by another at 40¾. These sales were recorded on ticker tapes across the country, and the illusion of activity was conveyed to the thousands of tape watchers who crowded into the brokerage offices of the country. Such activity, generated by so-called wash sales, created the impression that something big was afoot.

Now tipsheet writers and market commentators under the control of the pool manager would tell of exciting developments in the offing. The pool manager also tried to ensure that the flow of news from the company’s management was increasingly favorable. If all went well, and in the speculative atmosphere of the 1928–29 period it could hardly miss, the combination of tape activity and managed news would bring the public in.

Once the public came in, the free-for-all started and it was time discreetly to “pull the plug.” As the public did the buying, the pool did the selling. The pool manager began feeding stock into the market, first slowly and then in larger and larger blocks before the public could collect its senses. At the end of the roller-coaster ride, the pool members had netted large profits and the public was left holding the suddenly deflated stock.

But people didn’t have to band together to defraud the public. Many individuals, particularly corporate officers and directors, did quite well on their own. Take Albert Wiggin, the head of Chase, the nation’s second-largest bank at the time. In July 1929, Mr. Wiggin became apprehensive about the dizzy heights to which stocks had climbed and no longer felt comfortable speculating on the bull side of the market. (He was rumored to have made millions in a pool boosting the price of his own bank.) Believing that the prospects for his own bank’s stock were particularly dim, he sold short more than 42,000 shares of Chase stock. Selling short is a way to make money if stock prices fall. It involves selling stock you do not currently own in the expectation of buying it back later at a lower price. It’s hoping to buy low and sell high, but in reverse order.

Wiggin’s timing was perfect. Immediately after the short sale, the price of Chase stock began to fall, and when the crash came in the fall the stock dropped precipitously. When the account was closed in November, he had netted a multimillion-dollar profit from the operation. Conflicts of interest apparently did not trouble Mr. Wiggin. In fairness, it should be pointed out that he did retain a net ownership position in Chase stock during this period. Nevertheless, the rules in existence today would not allow an insider to make short-swing profits from trading his own stock.

On September 3, 1929, the market averages reached a peak that was not to be surpassed for a quarter of a century. The “endless chain of prosperity” was soon to break; general business activity had already turned down months before. Prices drifted for the next day, and on the following day, September 5, the market suffered a sharp decline known as the “Babson Break.”

This was named in honor of Roger Babson, a frail, goateed, pixyish-looking financial adviser from Wellesley, Massachusetts. At a financial luncheon that day, he had said, “I repeat what I said at this time last year and the year before, that sooner or later a crash is coming.” Wall Street professionals greeted the new pronouncements from the “sage of Wellesley,” as he was known, with their usual derision.

As Babson implied, he had been predicting the crash for several years and he had yet to be proven right. Nevertheless, at two o’clock in the afternoon, when Babson’s words were quoted on the “broad” tape (the Dow Jones financial news tape, which was an essential part of the furniture in every brokerage house), the market went into a nosedive. In the last frantic hour of trading, American Telephone and Telegraph went down 6 points, Westinghouse 7 points, and U.S. Steel 9 points. It was a prophetic episode. After the Babson Break the possibility of a crash, which was entirely unthinkable a month before, suddenly became a common subject for discussion.

Confidence faltered. September had many more bad than good days. At times the market fell sharply. Bankers and government officials assured the country that there was no cause for concern. Professor Irving Fisher of Yale, one of the progenitors of the intrinsic-value theory, offered his soon-to-be-immortal opinion that stocks had reached what looked like a “permanently high plateau.”

By Monday, October 21, the stage was set for a classic stock-market break. The declines in stock prices had led to calls for more collateral from margin customers. Unable or unwilling to meet the calls, these customers were forced to sell their holdings. This depressed prices and led to more margin calls and finally to a self-sustaining selling wave.

The volume of sales on October 21 zoomed to more than 6 million shares. The ticker fell way behind, to the dismay of the tens of thousands of individuals watching the tape from brokerage houses around the country. Nearly an hour and forty minutes had elapsed after the close of the market before the last transaction was actually recorded on the stock ticker.

The indomitable Fisher dismissed the decline as a “shaking out of the lunatic fringe that attempts to speculate on margin.” He went on to say that prices of stocks during the boom had not caught up with their real value and would go higher. Among other things, the professor believed that the market had not yet reflected the beneficent effects of Prohibition, which had made the American worker “more productive and dependable.”

On October 24, later called Black Thursday, the market volume reached almost 13 million shares. Prices sometimes fell $5 and $10 on each trade. Many issues dropped 40 and 50 points during a couple of hours. On the next day, Herbert Hoover offered his famous diagnosis, “The fundamental business of the country . . . is on a sound and prosperous basis.”

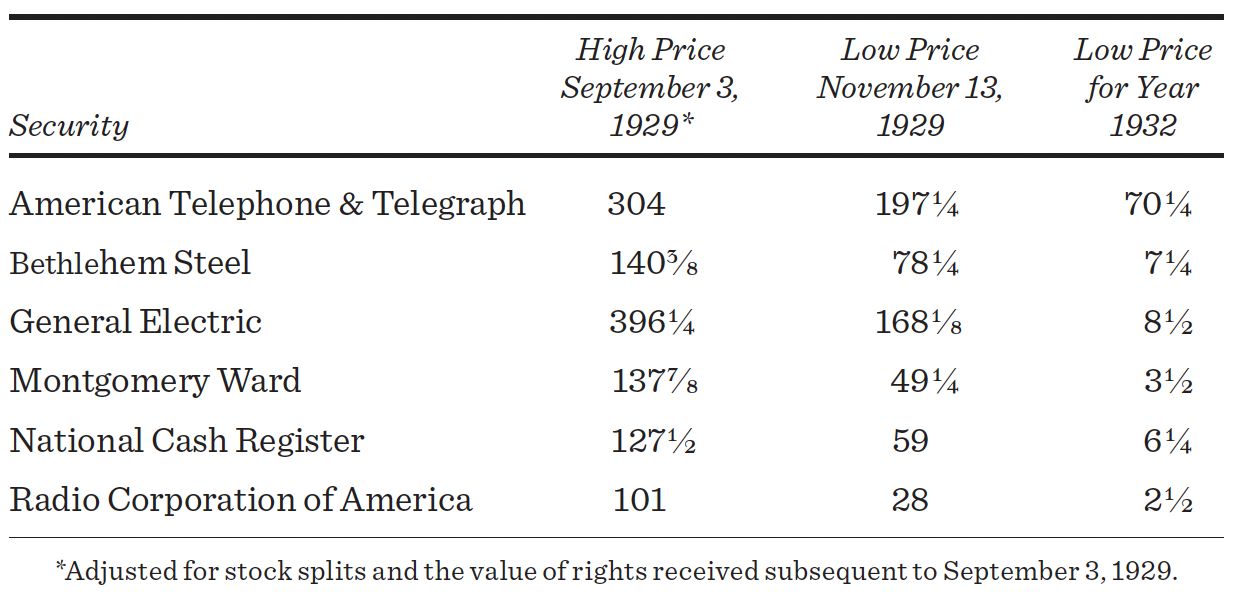

Tuesday, October 29, 1929, was among the most catastrophic days in the history of the New York Stock Exchange. Only October 19 and 20, 1987, rivaled in intensity the panic on the exchange. More than 16.4 million shares were traded on that day in 1929. (A 16-million-share day in 1929 would be equivalent to a multibillion-share day today because of the greater number of listed shares.) Prices fell almost perpendicularly, and kept on falling, as is illustrated by the following table, which shows the extent of the decline during the autumn of 1929 and over the next three years. With the exception of “safe” AT&T, which lost only three-quarters of its value, most blue-chip stocks had fallen 95 percent or more by the time the lows were reached in 1932.

Perhaps the best summary of the debacle was given by Variety, the show-business weekly, which headlined the story “Wall Street Lays an Egg.” The speculative boom was dead, and billions of dollars of share values—as well as the dreams of millions—were wiped out. The crash in the stock market was followed by the most devastating depression in history.

Again, there are revisionist historians who say there was a method to the madness of the stock-market boom of the late 1920s. Harold Bierman Jr., for example, in his book The Great Myths of 1929, has suggested that, without perfect foresight, stocks were not obviously overpriced in 1929. After all, very intelligent people, such as Irving Fisher and John Maynard Keynes, believed that stocks were reasonably priced. Bierman goes on to argue that the extreme optimism undergirding the stock market might even have been justified had it not been for inappropriate monetary policies. The crash itself, in his view, was precipitated by the Federal Reserve Board’s policy of raising interest rates to punish speculators. There are at least grains of truth in Bierman’s arguments, and economists today often blame the severity of the 1930s depression on the Federal Reserve for allowing the money supply to decline sharply. Nevertheless, history teaches us that very sharp increases in stock prices are seldom followed by a gradual return to relative price stability. Even if prosperity had continued into the 1930s, stock prices could never have sustained their advance of the late 1920s.

In addition, the anomalous behavior of closed-end investment company shares (which I will cover in chapter 15) provides clinching evidence of wide-scale stock-market irrationality during the 1920s. The “fundamental” value of these closed-end funds consists of the market value of the securities they hold. In most periods since 1930, these funds have sold at discounts of 10 to 20 percent from their asset values. From January to August 1929, however, the typical closed-end fund sold at a premium of 50 percent. Moreover, the premiums for some of the best-known funds were astronomical. Goldman, Sachs Trading Corporation sold at twice its net asset value. Tri-Continental Corporation sold at 256 percent of its asset value. This meant that you could go to your broker and buy, say, AT&T at whatever its market price was, or you would purchase it through the fund at 2½ times the market value. It was irrational speculative enthusiasm that drove the prices of these funds far above the value at which their individual security holdings could be purchased.

Why are memories so short? Why do such speculative crazes seem so isolated from the lessons of history? I have no apt answer, but I am convinced that Bernard Baruch was correct in suggesting that a study of these events can help equip investors for survival. The consistent losers in the market, from my personal experience, are those who are unable to resist being swept up in some kind of tulip-bulb craze. It is an obvious danger, but one frequently ignored.

*Golconda, now in ruins, was a city in India. According to legend, everyone who passed through it became rich.