FIRM FOUNDATIONS AND CASTLES IN THE AIR

What is a cynic? A man who knows the price of everything, and the value of nothing.

— Oscar Wilde, Lady Windermere’s Fan

IN THIS BOOK I will take you on a random walk down Wall Street, providing a guided tour of the complex world of finance and practical advice on investment opportunities and strategies. Many people say that the individual investor has scarcely a chance today against Wall Street’s professionals. They point to professional investment strategies using complex derivative instruments and high-frequency trading. They read news reports of accounting fraud, mammoth takeovers, and the activities of well-financed hedge funds. This complexity suggests that there is no longer any room for the individual investor in today’s markets. Nothing could be further from the truth. You can do as well as the experts—perhaps even better. It was the steady investors who kept their heads when the stock market tanked in March 2020, and then saw the value of their holdings eventually recover and continue to produce attractive returns. And many of the pros lost their shirts in 2008 buying derivative securities they failed to understand, as well as during the early 2000s when they overloaded their portfolios with overpriced tech stocks.

This book is a succinct guide for the individual investor. It covers everything from insurance to income taxes. It tells you how to buy life insurance and how to avoid getting ripped off by banks and brokers. It will even tell you what to do about gold, diamonds, and cryptocurrencies. But primarily it is a book about common stocks—an investment medium that not only provided generous long-run returns in the past but also appears to represent good possibilities for the years ahead. The life-cycle investment guide described in Part Four gives individuals of all age groups specific portfolio recommendations for meeting their financial goals, including advice on how to invest in retirement.

A random walk is one in which future steps or directions cannot be predicted on the basis of past history. When the term is applied to the stock market, it means that short-run changes in stock prices are unpredictable. Investment advisory services, earnings forecasts, and chart patterns are useless. On Wall Street, the term “random walk” is an obscenity. It is an epithet coined by the academic world and hurled insultingly at the professional soothsayers. Taken to its logical extreme, it means that a blindfolded monkey throwing darts at the stock listings could select a portfolio that would do as well as one selected by the experts.

Now, financial analysts in pin-striped suits do not like being compared to bare-assed apes. They retort that academics are so immersed in equations and Greek symbols (to say nothing of stuffy prose) that they couldn’t tell a bull from a bear, even in a china shop. Market professionals arm themselves against the academic onslaught with one of two techniques, called fundamental analysis and technical analysis, which we will examine in Part Two. Academics parry these tactics by obfuscating the random-walk theory with three versions (the “weak,” the “semi-strong,” and the “strong”) and by creating their own theory, called the new investment technology. This last includes a concept called beta, including “smart beta,” and I intend to trample on that a bit. By the early 2000s, even some academics had joined the professionals in arguing that the stock market was at least somewhat predictable after all. Still, as you can see, a tremendous battle is going on, and it’s fought with deadly intent because the stakes are tenure for the academics and bonuses for the professionals. That’s why I think you’ll enjoy this random walk down Wall Street. It has all the ingredients of high drama—including fortunes made and lost and classic arguments about their cause.

But before we begin, perhaps I should introduce myself and state my qualifications as guide. I have drawn on three aspects of my background in writing this book; each provides a different perspective on the stock market.

First is my professional experience in the fields of investment analysis and portfolio management. I started my career as a market professional with one of Wall Street’s leading investment firms. Later, I chaired the investment committee of a multinational insurance company and for many years served as a director of one of the world’s largest investment companies. These perspectives have been indispensable to me. Some things in life can never fully be appreciated or understood by a virgin. The same might be said of the stock market.

Second are my current positions as an economist and chair of several investment committees. Specializing in securities markets and investment behavior, I have acquired detailed knowledge of academic research and new findings on investment opportunities.

Last, and certainly not least, I have been a lifelong investor and successful participant in the market. How successful I will not say, for it is a peculiarity of the academic world that a professor is not supposed to make money. A professor may inherit lots of money, marry lots of money, and spend lots of money, but he or she is never, never supposed to earn lots of money; it’s unacademic. Anyway, teachers are supposed to be “dedicated,” or so politicians and administrators often say—especially when trying to justify the low academic pay scales. Academics are supposed to be seekers of knowledge, not of financial reward. It is in the former sense, therefore, that I shall tell you of my victories on Wall Street.

This book has a lot of facts and figures. Don’t let that worry you. It is specifically intended for the financial layperson and offers practical, tested investment advice. You need no prior knowledge to follow it. All you need is the interest and the desire to have your investments work for you.

INVESTING AS A WAY OF LIFE TODAY

At this point, it’s probably a good idea to explain what I mean by “investing” and how I distinguish this activity from “speculating.” I view investing as a method of purchasing assets to gain profit in the form of reasonably predictable income (dividends, interest, or rentals) and/or appreciation over the long term. It is the definition of the time period for the investment return and the predictability of the returns that often distinguish an investment from a speculation. A speculator buys stocks hoping for a short-term gain over the next days or weeks. An investor buys stocks likely to produce a dependable future stream of cash returns and capital gains when measured over years or decades.

Let me make it quite clear that this is not a book for speculators; nor is it a book for day traders enticed by zero commissions to gamble on the hourly fluctuations of stock prices. Indeed, a subtitle for this book might well have been The Get Rich Slowly but Surely Book. Remember, just to stay even, your investments have to produce a rate of return equal to inflation.

Inflation in the United States and throughout most of the developed world fell to 2 percent or below in the early decades of the 2000s; while inflation spiked in the early 2020s, many analysts believe that relative price stability will return. They suggest that inflation is the exception rather than the rule. It may well be that little inflation will occur during the decades ahead, but I believe investors should not dismiss the possibility that noticeable inflation will characterize the future. Although productivity growth accelerated in the 1990s and early 2000s, it has recently slowed, and history tells us that the pace of improvement has always been uneven. Moreover, productivity improvements are harder to come by in some service-oriented activities. It will still take four musicians to play a string quartet and one surgeon to perform an appendectomy throughout the twenty-first century, and if musicians’ and surgeons’ salaries rise over time, so will the cost of concert tickets and appendectomies. Thus, upward pressure on prices cannot be dismissed.

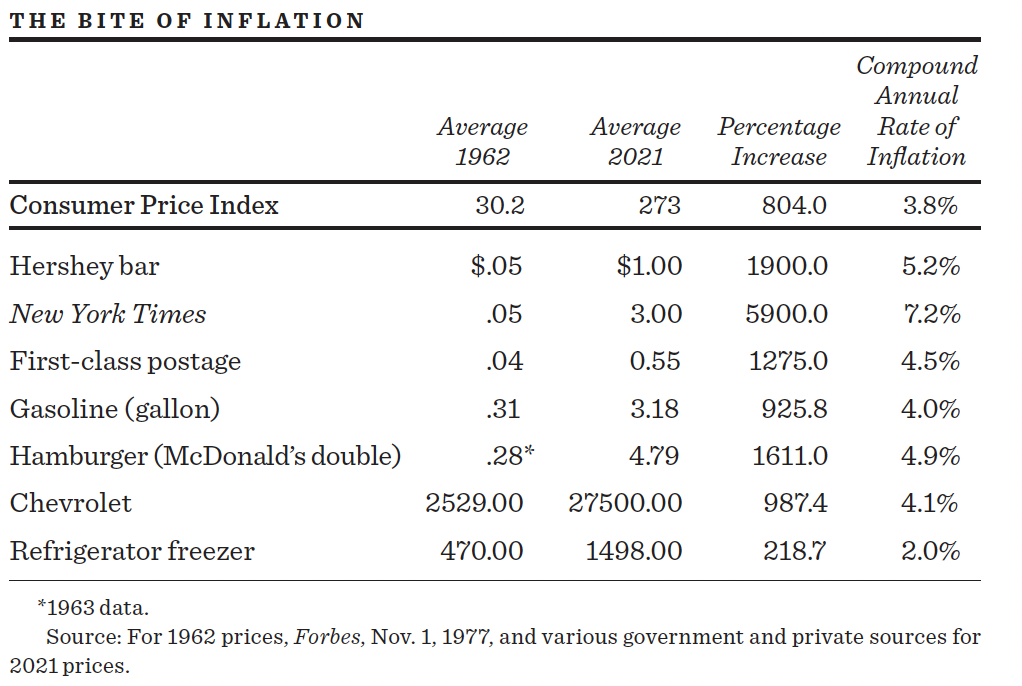

If inflation were to proceed at a 2 to 3 percent rate—a rate much lower than in the 1970s and early 1980s—the effect on our purchasing power would still be devastating. The table on the following page shows what an average inflation rate of close to 4 percent has done over the 1962–2021 period. My morning newspaper has risen 5,900 percent. My afternoon Hershey bar is twenty times more expensive, and it’s actually smaller than it was in 1962, when I was in graduate school. If inflation continued at the same rate, today’s morning paper would cost more than five-and-a-half dollars by 2030. It is clear that if we are to cope with even a mild inflation, we must undertake investment strategies that maintain our real purchasing power; otherwise, we are doomed to an ever-decreasing standard of living.

Investing requires work, make no mistake about it. Romantic novels are replete with tales of great family fortunes lost through neglect or lack of knowledge on how to care for money. Who can forget the sounds of the cherry orchard being cut down in Chekhov’s great play? Free enterprise, not the Marxist system, caused the downfall of the Ranevsky family: They had not worked to keep their money. Even if you trust all your funds to an investment adviser or to a mutual fund, you still have to know which adviser or which fund is most suitable to handle your money. Armed with the information contained in this book, you should find it a bit easier to make your investment decisions.

Most important of all, however, is the fact that investing is fun. It’s fun to pit your intellect against that of the vast investment community and to find yourself rewarded with an increase in assets. It’s exciting to review your investment returns and to see how they are accumulating at a faster rate than your salary. And it’s also stimulating to learn about new ideas for products and services, and innovations in the forms of financial investments. A successful investor is generally a well-rounded individual who puts a natural curiosity and an intellectual interest to work.

All investment returns—whether from common stocks or exceptional diamonds—are dependent, to varying degrees, on future events. That’s what makes the fascination of investing: It’s an activity whose success depends on an ability to predict the future. Traditionally, the pros in the investment community have used one of two approaches to asset valuation: the firm-foundation theory or the castle-in-the-air theory. Millions of dollars have been gained and lost on these theories. To add to the drama, they appear to be mutually exclusive. An understanding of these two approaches is essential if you are to make sensible investment decisions. It is also a prerequisite for keeping you safe from serious blunders. Toward the end of the twentieth century, a third theory, born in academia and named the new investment technology, became popular on “the Street.” Later in the book, I will describe that theory and its application to investment analysis.

The firm-foundation theory argues that each investment instrument, be it a common stock or a piece of real estate, has a firm anchor of something called intrinsic value, which can be determined by careful analysis of present conditions and future prospects. When market prices fall below (rise above) this firm foundation of intrinsic value, a buying (selling) opportunity arises, because this fluctuation will eventually be corrected—or so the theory goes. Investing then becomes a dull but straightforward matter of comparing something’s actual price with its firm foundation of value.

In The Theory of Investment Value, Williams presented a formula for determining the intrinsic value of stock. Williams based his approach on dividend income. In a fiendishly clever attempt to keep things from being simple, he introduced the concept of “discounting.” Discounting basically involves looking at income backwards. Rather than seeing how much money you will have next year (say $1.05 if you put $1 in an investment yielding 5 percent), you look at money expected in the future and see how much less it is worth currently (thus, next year’s $1 is worth today only about 95¢, which could be invested at 5 percent to produce approximately $1 at that time).

Williams actually was serious about this. He went on to argue that the intrinsic value of a stock was equal to the present (or discounted) value of all its future dividends. Investors were advised to “discount” the value of moneys received later. Because so few people understood it, the term caught on and “discounting” now enjoys popular usage among investment people. It received a further boost under the aegis of Professor Irving Fisher of Yale, a distinguished economist and investor.

The logic of the firm-foundation theory is quite respectable and can be illustrated with common stocks. The theory stresses that a stock’s value ought to be based on the stream of earnings a firm will be able to distribute in the future in the form of dividends or stock buybacks. It stands to reason that the greater the present dividends and their rate of increase, the greater the value of the stock; thus, differences in growth rates are a major factor in stock valuation. Now the slippery little factor of future expectations sneaks in. Security analysts must estimate not only long-term growth rates but also how long they can be maintained. When the market gets overly enthusiastic about how far into the future growth can continue, it is popularly held on Wall Street that stocks are discounting not only the future but perhaps even the hereafter. The point is that the firm-foundation theory relies on some tricky forecasts of the extent and duration of future growth. The foundation of intrinsic value may thus be less dependable than is claimed.

The firm-foundation theory is not confined to economists alone. Thanks to a very influential book, Benjamin Graham and David Dodd’s Security Analysis, a whole generation of Wall Street security analysts was converted to the fold. Sound investment management, the practicing analysts learned, simply consisted of buying securities whose prices were temporarily below intrinsic value and selling ones whose prices were temporarily too high. It was that easy. Perhaps the most successful disciple of the Graham and Dodd approach was a canny midwesterner named Warren Buffett, often called “the sage of Omaha.” Buffett compiled a legendary investment record, allegedly following the approach of the firm-foundation theory.

The castle-in-the-air theory of investing concentrates on psychic values. John Maynard Keynes, a famous economist and successful investor, enunciated the theory most lucidly in 1936. It was his opinion that professional investors prefer to devote their energies not to estimating intrinsic values, but rather to analyzing how the crowd of investors is likely to behave in the future and how during periods of optimism they tend to build their hopes into castles in the air. The successful investor tries to beat the gun by estimating what investment situations are most susceptible to public castle-building and then buying before the crowd.

According to Keynes, the firm-foundation theory involves too much work and is of doubtful value. Keynes practiced what he preached. While London’s financial men toiled many weary hours in crowded offices, he played the market from his bed for half an hour each morning. This leisurely method of investing earned him several million pounds for his account and a tenfold increase in the market value of the endowment of his college, King’s College, Cambridge.

In the depression years in which Keynes gained his fame, most people concentrated on his ideas for stimulating the economy. It was hard for anyone to build castles in the air or to dream that others would. Nevertheless, in his book The General Theory of Employment, Interest and Money, Keynes devoted an entire chapter to the stock market and to the importance of investor expectations.

With regard to stocks, Keynes noted that no one knows for sure what will influence future earnings’ prospects and dividend payments. As a result, he said, most people are “largely concerned, not with making superior long-term forecasts (for) an investment over its whole life, but with foreseeing changes in the conventional basis of valuation a short time ahead of the general public.” Keynes, in other words, applied psychological principles rather than financial evaluation to the study of the stock market. He wrote, “It is not sensible to pay 25 for an investment of which you believe the prospective yield to justify a value of 30, if you also believe that the market will value it at 20 three months hence.”

Keynes described the playing of the stock market in terms readily understandable by his fellow Englishmen: It is analogous to entering a newspaper beauty-judging contest in which one must select the six prettiest faces out of a hundred photographs, with the prize going to the person whose selections most nearly conform to those of the group as a whole.

The smart player recognizes that personal criteria of beauty are irrelevant in determining the contest winner. A better strategy is to select those faces the other players are likely to fancy. This logic tends to snowball. After all, the other participants are likely to play the game with at least as keen a perception. Thus, the optimal strategy is not to pick those faces the player thinks are prettiest, or those the other players are likely to fancy, but rather to predict what the average opinion is likely to be about what the average opinion will be, or to proceed even further along this sequence. So much for British beauty contests.

The newspaper-contest analogy represents the ultimate form of the castle-in-the-air theory of price determination. An investment is worth a certain price to a buyer because she expects to sell it to someone else at a higher price. The investment, in other words, holds itself up by its own bootstraps. The new buyer in turn anticipates that future buyers will assign a still higher value.

In this kind of world, a sucker is born every minute—and he exists to buy your investments at a higher price than you paid for them. Any price will do as long as others may be willing to pay more. There is no reason, only mass psychology. All the smart investor has to do is to beat the gun—get in at the very beginning. This theory might less charitably be called the “greater fool” theory. It’s OK to pay three times what something is worth if later on you can find some innocent to pay five times what it’s worth.

The castle-in-the-air theory has many advocates, in both the financial and the academic communities. The Nobel laureate Robert Shiller, in his book Irrational Exuberance, argues that the mania in Internet and high-tech stocks during the late 1990s can be explained only in terms of mass psychology. At universities, so-called behavioral theories of the stock market, stressing crowd psychology, gained favor during the early 2000s. The psychologist Daniel Kahneman won the Nobel Prize in Economics in 2002 for his seminal contributions to the field of “behavioral finance.” Earlier, Oskar Morgenstern was a leading champion, arguing that the search for intrinsic value in stocks is a search for the will-o’-the-wisp. He believed that every investor should post the following Latin maxim above his desk:

Res tantum valet quantum vendi potest.

(A thing is worth only what someone else will pay for it.)

HOW THE RANDOM WALK IS TO BE CONDUCTED

With this introduction out of the way, come join me for a random walk through the investment woods, with an ultimate stroll down Wall Street. My first task will be to acquaint you with the historical patterns of pricing and how they bear on the two theories of pricing investments. It was Santayana who warned that if we did not learn the lessons of the past we would be doomed to repeat the same errors. Therefore, I will describe some spectacular crazes—both long past and recently past. Some readers may pooh-pooh the mad public rush to buy tulip bulbs in the seventeenth-century Netherlands and the eighteenth-century South Sea Bubble in England. But no one can disregard the “Nifty Fifty” craze of the 1970s, the incredible boom in Japanese land and stock prices and the equally spectacular crash in the early 1990s, the “Internet craze” of 1999 and early 2000, and the U.S. real estate bubble of 2006–2007. And the wild speculation in so-called meme stocks and cryptocurrencies in the 2020s reminds us that markets may change but they fundamentally remain the same. These provide continual warnings that neither individuals nor investment professionals are immune from the errors of the past.