Chapter 17

The Federal Reserve

The Fed is a pseudogovernmental entity, meaning that it reports to Congress, so it is kind of part of the government, but it isn’t really a part of the government because its board members are technically independent decision-makers with a dual mandate of creating and maintaining price stability and maximum employment. That’s why the Fed’s actions, which create monetary policy, are different from the government’s, which create fiscal policy.

The Fed is not funded by Congress (and therefore not funded by taxpayers). Instead, it earns money from interest earned on government securities that it purchases and fees charged to banks. Congress checks in with it to make sure that things are going okay, but the Fed alone has to make sure that monetary policy keeps the economy alive and stable.

Who Started the Fed?

In short, J. P. Morgan, the founder of today’s JPMorgan Chase bank.

In 1907, there were a lot of bank runs, when lots of customers rushed to pull their money out at the same time. The banking business model doesn’t allow for everyone to say, “Give me my money right now please,” because the banks have loaned out the money elsewhere and can’t summon it back instantaneously. So people would rush to try to get their money, and the banks would have no money to give them. Because the planet wasn’t as globalized as it is now, there weren’t international bank runs—but that has clearly changed in recent years.

J. P. Morgan was getting really sick of it. As the owner of the most successful bank in the United States at the time, he had issued emergency loans to other banks that weren’t managing their money as well. Finally, he put his powerful foot down and said, “Enough. I am too rich to exist in a society such as this.” Speaking for all of us who have done work that was not ours to do, he threw his hands up in frustration and said, “This is not my job.” Everything he’d done to keep the markets afloat gave him the leverage to push through the legislation needed to create a central bank.

The Fed was established and signed into law by President Woodrow Wilson in 1913. (His wife, Edith Wilson, who was also the first woman to hold a driver’s license in Washington, D.C., probably played an outsized role. When Woodrow collapsed from a stroke in 1919, Edith Wilson took the helm of the ship, making decisions on behalf of the president and serving as his filter and access control point. She reviewed documents, worked with advisers, and went to meetings, acting as a pseudopresident in the day-to-day operations of the country. So it might seem as though it was just another group of dudes deciding the fate of the future, but perhaps the story is more complicated than that.)

The Fed was meant to be the solution to the plague of volatility and uncertainty that had haunted the 1800s, making sustained economic growth impossible. It would be a central bank that would be responsible for setting monetary policy to get the economy on track to grow sustainably, plus regulating banks, watching over financial institutions, managing the money supply, and reinforcing citizens’ collective trust in that money, thereby exerting a massive influence on the stock market, bond market, and housing market.

The Fed was—and is—an economic vibe setter.

How Does the Federal Reserve Work?

The Federal Reserve operates in twelve different districts. There is a central authority, the board of governors, located in Washington, D.C., along with a decentralized network of twelve Federal Reserve banks located throughout the United States, each with its own president.

The idea is that the power shouldn’t be concentrated just in Washington, D.C., because the Fed serves the whole country. Each president rotates onto the Federal Open Market Committee (FOMC), which sets interest rates and manages government securities. The Fed has three main components:

Board of Governors

The board is made up of seven members, nominated by the president and confirmed by the Senate, which oversees the twelve Reserve Banks. The members serve staggered fourteen-year terms that expire in even-numbered years, so the whole board isn’t up for renomination at the same time, preventing any sort of political influence resulting from one president stacking the board with his favorites.

Federal Open Market Committee (Fomc)

The monetary policy unit of the Federal Reserve, the FOMC is composed of twelve members: the seven members who make up the board of governors and five of the twelve Reserve Bank presidents. The Federal Reserve chairperson heads up the committee, which meets eight times per year—every six weeks—to figure out how to steer the economic ship.

Federal Reserve Banks

These are the operational arms of the Federal Reserve System that carry out the Fed’s activities. The twelve districts are headquartered in Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, and San Francisco.

Each bank has a board of directors divided into three “classes”: A, B, and C. Class A directors are appointed by member banks and represent the banking industry. Class B directors are also appointed by member banks but represent the public interest. Class C directors are appointed by the Board of Governors and also represent the public interest. The board is responsible for overseeing the bank’s operations and appointing the bank’s president.

The Chair of the Board

The president nominates the chairman of the Board of Governors, who then has to be approved by a majority vote in the U.S. Senate. It’s an unspoken rule that a newly elected president should keep the chair that the previous president nominated. That’s because the Fed is meant to be an independent organization. But its independence has been somewhat compromised by recent political moves.

A great example was during the Trump administration, when its not-so-well-kept secret and subsequent independence were breached when President Donald Trump replaced Janet Yellen with Jerome Powell. The next president, Joe Biden, kept Powell on board. That said, there was a question whether Powell would get to keep his seat when it came time for him to be renominated in 2022. At the time, the economy was a bit bonkers. Moderates wanted Powell to be appointed because they were concerned about inflation and wanted continuity during that ongoing crisis. Progressives, on the other hand, wanted a change and to nominate Lael Brainard, the Fed’s vice chair, as she was seen as more aligned with President Biden’s economic agenda, with a focus on climate change and a leading voice on tighter oversight for Wall Street.

The Fed chair appointment process has become increasingly political, like everything else, with people being nominated based on their views on climate change and other social issues rather than their takes on monetary policy. To be clear, it is important that the Fed consider these factors as main nudgers of the economy, but it has limited direct influence on these issues due to its congressional mandate. The Fed can only incentivize different initiatives to support climate change initiatives and other important legislation.

Of course, climate change poses a very clear systemic risk, and regulators will need to take it into consideration. But the continuous entanglement of the Fed into political issues is not the reason that the Fed exists. We need our elected government policymakers to do their jobs.

The Fed’s Narrative

Constituents have to be told the right story. The Federal Reserve promotes the narrative that it is indispensable to the broader narrative of “stock market going up.” Alan Greenspan, the chairman of the Federal Reserve from 1987 to 2006, began the era of the Fed and the markets being intimately intertwined. Not only does the Fed manage things quantitatively, but it also manages them qualitatively, which ends up being the driving force of its narrative creation process.

Greenspan’s tenure as Fed chairman saw periods of strong economic growth and stability, but the Fed also faced a lot of challenges, such as the 1987 stock market crash, the bursting of the dot-com bubble in the early 2000s, and the aftermath of the 9/11 attacks. Throughout those events, he was often credited with effectively managing monetary policy to support economic growth while keeping inflation in check, awarding him the nickname “the Maestro.”

On October 19, 1987, when the stock market experienced a sharp and sudden decline, the Fed, under Greenspan’s leadership, took swift action to inject liquidity and stabilize the financial system. The Fed engaged in intraday rate cuts, meaning that it reduced the target federal funds rate and discount rate during the trading day, providing support to markets and tying it closely to the narrative of “stock market going up.”

Narrative Creation

Most of what drives the Fed’s narrative has to do with maintaining price stability and maximum employment:

-

If inflation is raging, the Fed has to use its tool kit to manage it.

-

If unemployment is skyrocketing, the Fed has to manage that, too.

-

The Fed controls many aspects of its dual mandate through straight-up chatter.

A lot of the Federal Reserve’s actions have become a political hot potato. It has to answer to Congress semiannually, but it also has to answer to the yells of politicians around the clock. Yes, its members can make decisions autonomously without the federal government’s approval, but they’re subject to some oversight by Congress and are charged with working to further the government’s high-level economic objectives.

As talked about in the monetary policy chapter, the Fed has to remain credible. People need to believe in the Fed with all their might. That is the only way that the narrative creation process will work. Sometimes that means conducting monetary policy in a fast and furious way so everyone knows that the Fed isn’t messing around.

Resistance to the Narrative

The biggest question about a lot of Federal Reserve actions is whether they will work or not. Monetary policy is nudge-nudge, wink-wink, and the underlying worry is that things won’t work the way they are expected to. In fact, they often don’t work the way they are expected to. A global pandemic, supply chain stressors, consumer credit overextension, the amount of oil stockpiles, and an unrecovered manufacturing sector have all created a lot of stress on the Fed’s narrative. We can’t forget at the end of the day that we exist with our feet on the ground. This may seem a bit dark, but if you die in the metaverse, you die in real life, as Mark Zuckerberg, the founder of Facebook, said.

The biggest nuance of all is the politicalization of markets. The Federal Reserve and other central banks have become primarily inflation firefighters. They have to deal with whatever is right in front of them. But the market is kind of like the one person who keeps calling the fire department because they can’t open a jar. It’s dramatic. It’s loud. And the Fed still has to respond when they call.

There are a lot of examples of central banks losing their independence, as political interference begins to influence monetary policy. “In Turkey, central bank independence is now an endangered species,” political scientists writing in Foreign Policy warned in 2022. As of the time of writing of this book, Turkish president Recep Tayyip Erdoğan has fired three bank governors who disagreed with his economic agenda, packing the bench with loyalists who enable his meddling. Despite surging inflation peaking at 85.5 percent in October 2022, Erdoğan pushed to lower interest rates dramatically, a puzzling move that defied economic orthodoxy. Naturally, this has raised concerns about the central bank’s ability to maintain price stability independently and do its job well.

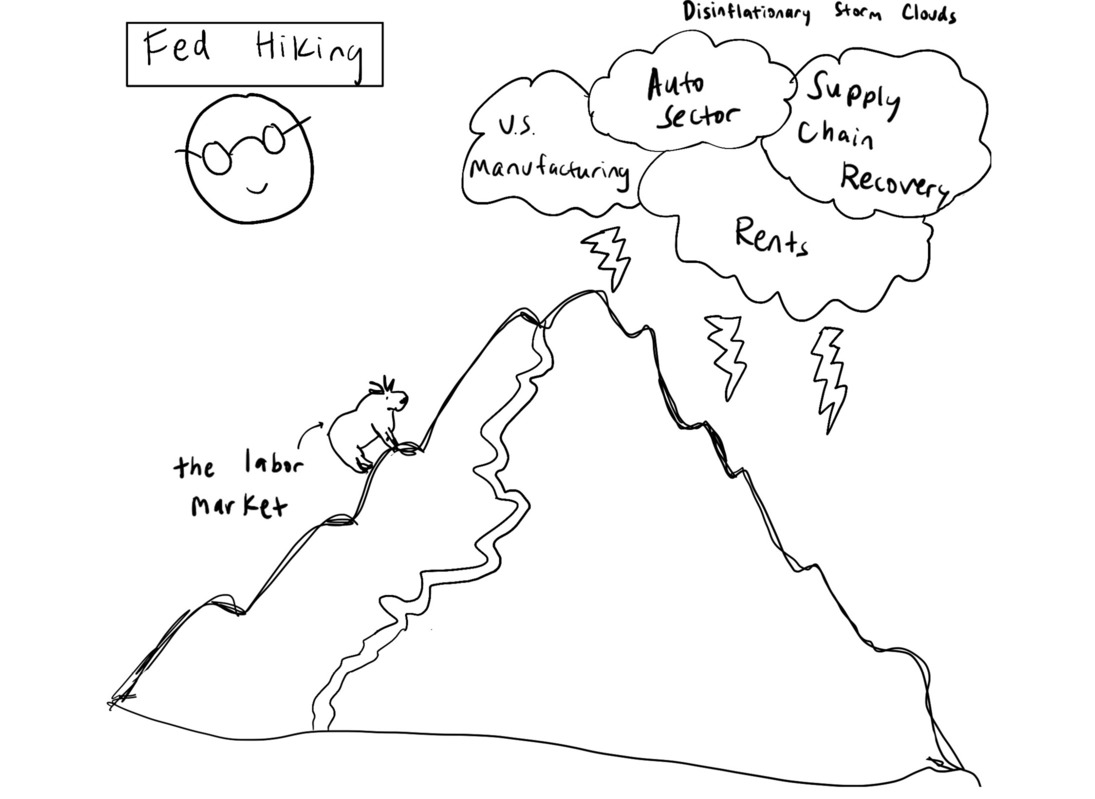

The United States has come under fire, too. Former president Trump was critical of the Federal Reserve’s interest rate policy, urging the central bank to lower rates. A lot of the Fed’s job—and this narrative maintenance—is actually quite similar to climbing a mountain.

The Fed’s Mountain

If you hike or climb, you know that many mountain trails are a series of switchbacks. Zigzagging up the sides of the mountain makes the path less steep and takes a certain amount of effort out of the hike.

The 1970s

But sometimes the Fed climbs the mountain directly—no switchbacks, no trekking poles, just pure love of the grind. The 1970s were a good example of when the Fed was in grind mode. At the time, the United States faced a severe inflation crisis, with double-digit inflation rates and a stagnant economy. The crisis was sparked by the oil price shock of 1973, when OPEC put a squeeze on the world’s oil supply. And of course, oil is in everything, so as oil skyrocketed in price, so did everything else. There were supply chain issues and eventually a wage-price spiral. Prices were rising quickly, wages were rising quickly, and everything was out of control.

Paul Volcker was appointed as the chairman of the Federal Reserve in 1979 and caused something called the Volcker Shock. (Sounds cool but was not.) He implemented tight monetary policy, which involved raising interest rates to unprecedented levels. The rate set by the Fed was 11% in 1979, but by 1980, it hit 20%, the highest level in U.S. history.

Volcker’s aim was to reduce the money supply to slow economic activity and make inflation chill out. He increased the reserve requirement, let the dollar fall in value against other currencies, and collaborated with other central banks on anti-inflationary efforts. This aggressive move triggered a severe recession, marked by high unemployment and economic contraction. While it effectively reduced inflation to around 4 percent by 1987, the strategy had substantial short-term repercussions, including widespread unemployment and sluggish economic growth. That was, unsurprisingly, very unpopular. After making everyone mad, Volcker’s Fed then implemented a gradual reduction in interest rates to stimulate growth and bring the economy out of recession. By the mid-1980s, inflation had fallen to more manageable levels. But the economy had paid a terrible price, hitting double-digit unemployment during a two-year-long recession.

Here’s the thing: The Volcker Shock was one way to fight inflation, and it did get the job done eventually. But some economists argue that it wasn’t the only way out. They say that other tools in the economic toolbox could have been used. For example, some suggest that the government could have focused on fiscal policies, such as controlling government spending or tweaking taxes, to address the inflation. Others argue that Volcker could have taken a more gradual approach to raising interest rates, giving businesses and people more time to adjust. That might have softened the blow to the economy and reduced the pain of the high interest rates. Before 1979, the Fed was subject to a lot of political pressure from Congress. But Volcker came in with a baseball bat and raised rates aggressively, setting a precedent for the Fed to focus on what was best for the economy in the long term, not just what was popular with members of Congress and the public in the short term. Of course, to stay with the theme of this book that “everything is weird,” in a 2022 paper published by the Federal Reserve, the economists David Ratner and Jae Sim challenged the idea that central banks, particularly Paul Volcker’s actions, were solely responsible for controlling inflation in the 1970s and 1980s. They wrote: “Conventional wisdom has it that the sound monetary policy since the 1980s not only conquered the Great Inflation, but also buried the Phillips curve itself. This paper provides an alternative explanation: labor market policies that have eroded worker bargaining power might have been the source of the demise of the Phillips curve.”

This theory suggests that inflation was curbed not just through monetary policy but also through changes in labor dynamics, particularly the weakening of labor unions and reduced worker ability to negotiate higher wages.

This is a class-based theory of inflation, where the loss of bargaining power among workers contributed to lower inflation, not mega-high interest rates. Inflation subsided because workers lacked the power to sustain it. Not because monetary policy worked.

Volcker in 2022

The Fed’s 2021–2023 inflation fight was a bit of a Volcker-style takedown of the economy. During this period, there were rising prices and energy conflicts similar to those of the 1970s. However, the underlying inflationary dynamics were quite different. This raises questions about whether using the same tool (raising rates) was the best way to combat a different type of inflation. And remember, the Fed has a dual mandate. Its policies are meant to optimize both price stability and the labor market—and those two mandates were in conflict for most of the early 2020s.

In the 2021–2023 inflation fight, Fed officials often talked about how strong the labor market was and how they needed it to calm down. The dynamic between jobs and higher prices is a strange one, and it can feel disconcerting to hear things such as “Job growth remained stubbornly robust” or “The consumer is too strong for comfort,” as the Fed once put it.

But the Fed had a job to do. So it raised interest rates à la Volcker, and somehow the labor market was still incredibly strong into 2023. But the dynamics of the labor market are shifting and evolving—to something that will likely require a whole new policy tool kit to deal with.

2 Percent Target

The Fed is going relentlessly after a target of 2 percent inflation. In order for it to summit and complete its hike, the economy needs to hit that 2 percent target. But what’s supercool about the mountain is that no one knows where the summit is. There’s no map, no GPS coordinates, no guides from people who have been there before. Being able to achieve 2 percent inflation and end our decades-long era of hikes is something we just kind of manifest into existence.

That’s because the 2 percent figure is sort of random. The idea originally came from Arthur Grimes, the Labour Party finance minster of New Zealand in the 1980s. He went on TV and said, “Two percent should be our inflation target,” and now everybody goes after that magic number.

Here’s the secret, though: Inflation doesn’t need to be 2 percent all the time. It’s simply the general direction in which things are meant to be headed. And to be clear, we don’t know what it takes to get down to 2 percent and we don’t know if 2 percent is the right target in the first place. As are other things in this book: it’s uncertain.

If the inflation target changed, it wouldn’t be the end of the world; it might actually be good! Goldman Sachs found that a 3 percent target would be “positive for risk assets, as the tailwind from stronger economic growth would more than offset the headwind from higher nominal bond yields across the curve.” What that basically means is “good for stocks because the economy will grow faster even if bond yields are higher.” Basically, the economy will normalize; 2 percent is not the be-all and end-all.

The Fed informs everyone where rates are and where it thinks they need to be in order to move toward the 2 percent inflation “summit” by releasing its Summary of Economic Projections, its projections of key economic indicators such as inflation, GDP growth, the unemployment rate, and the individual forecasts of each Federal Open Market Committee (FOMC) participant for the federal funds rate over the next few years.

The Summary of Economic Projections also includes the final resting point for rates, known as the terminal rate; this is the point at which they stop their upward journey (peak inflation). But of course, staying at the top of the mountain is a form of monetary policy, too—because the only way any hike really ends is if the rate comes back down.

How the Fed Deals with Markets

To complete the analogy, the Fed also has to be mindful of unruly and unpredictable “snow” coming from the stock and bond markets, which could potentially lead to an avalanche and bury us all. Like a companion who signs up to hike a mountain with you, the Fed needs to make sure that its friends in the market understand that even if it rolls up to a yield or stop sign on the mountain, that doesn’t mean it will be changing its course. A lot of the time the market interprets little signs by the Fed as signals that it is going in a certain direction—and freaks out in response. The Fed can’t really control the “snow,” but it can plow routes around it!

If you are a hiker, you know that choosing a companion can be tricky. Sometimes, you’ll have a ride-or-die friend who is willing to grind with you. Other times, you’ll have people with you who complain the whole way even if you take the easiest switchbacks possible.

The Fed is the same way. There are often questions as to whether the Fed is becoming too focused on the market response versus the economic response (because the two can be and often are different). I asked San Francisco Fed president Mary Daly about this in October 2023, specifically about how the Fed balances managing markets (making sure markets don’t flip whenever the Fed says something) and telling people what they need to hear. Her response:

So when I look at the markets, I’m asking several questions. Are they understanding the reaction function that the Federal Reserve has, that the FOMC has? Do they see the data the way I’m seeing it? And if not, let me learn from what they’re seeing and see if it builds my understanding…. So I use the financial markets as data and as opposed to managing them, I’m trying to communicate to them just like I am to all of you, so that they clearly understand what we’re trying to achieve.

Jerome Powell has addressed the market directly in some press conferences—for example, in 2021, stating that “what’s been driving asset prices isn’t monetary policy.” But as the Fed itself said in 2022, “An unwarranted easing in financial conditions, especially if driven by a misperception by the public of the committee’s reaction function, would complicate the committee’s effort to restore price stability.”

Translation? “F*ck off, markets. We have a job to do. And we are going to get it done.”

Jerome Powell tends to follow the markets in terms of tone. When he was erroneously told in a November 2022 press conference that stocks had reacted positively to the Fed raising rates, he immediately began listing all the reasons why investors should not be happy that the Fed was raising rates. Managing expectations is a large part of the Fed’s battle, and they did not need a happy market in this inflation battle. Neel Kashkari, the president of the Federal Reserve Bank of Minneapolis, said in 2022, “I certainly was not excited to see the stock market rallying after our last Federal Open Market Committee meeting…. Because I know how committed we all are to getting inflation down.”

The Fed needs to balance ego and effect. Its members have to make sure that they don’t become too focused on earning back Fed cred on the mountain hike and harming everybody else in the process.

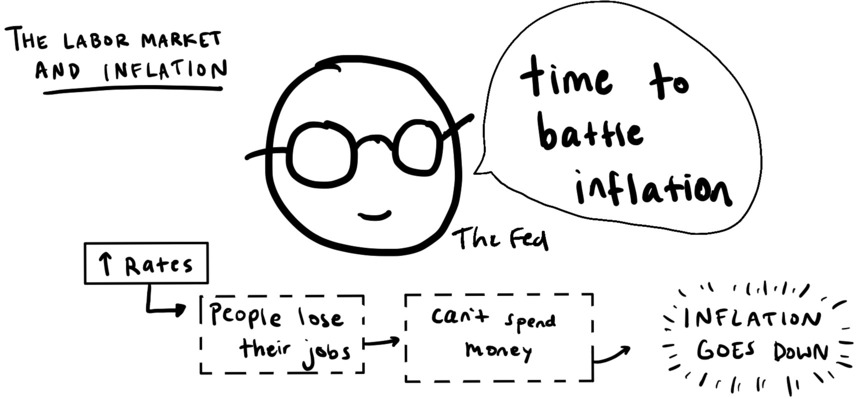

The Fed and the Labor Market

The whole point of hiking the mountain is to slow the economy down. The Fed has a dual mandate of creating and maintaining price stability and maximum employment. Price stability is achieved by raising or lowering rates, but this often comes at the expense of the labor market. We can think of the labor market as a mountain goat on the mountain, something that the Fed needs to work with but is sort of in the way.

Ultimately, the Fed wants to quietly tame the labor market goat off the mountain (nonviolently) because that will make the economy chill out. It’s an unfortunate reality: When the labor market is strong, when the goat is hanging on to the mountain in an inflationary environment, the Fed doesn’t love it. It makes the hike that much harder!

The labor market goat can be kicked off the mountain in one of two ways:

-

More people find jobs (labor force participation rate increases).

-

More people lose their jobs (unemployment rate increases).

The more harmful one (people losing their jobs) is usually easier to make happen. Increasing the labor force participation rate would tighten the labor market, put downward pressure on wage growth, and make it so there isn’t so much slack for employers. An increase in the unemployment rate would do those three things as well, but in a more painful way.

You might be asking, “Why does the Fed need to sacrifice the labor market to get inflation down?” The main reason that the Fed freaks out so deeply about the labor market is that nominal wage growth is tied to an inflation measure that it paid a lot of attention to in 2022 called “core services ex shelter” (basically services that we need—or want, in some instances—including such things as transportation, healthcare, and haircuts), so it was worried that if wage growth—particularly in the services sector—didn’t soften, inflation wouldn’t soften. Unfortunately, the general idea behind battling inflation is that if the Fed raises interest rates, people will lose their jobs, and if they don’t have jobs, they have no money to spend, so inflation will chill out. This makes sense in theory, but it creates problems such as wage growth imbalances and wealth inequality.

There’s a short memoir called The Crane Wife by C. J. Hauser. Hauser had recently broken off an engagement and headed to Texas to study whooping cranes for a novel. This is what she says:

Here is what I learned once I began studying whooping cranes: only a small part of studying them has anything to do with the birds. Instead we counted berries. Counted crabs. Measured water salinity. Stood in the mud. Measured the speed of the wind.

It turns out, if you want to save a species, you don’t spend your time staring at the bird you want to save. You look at the things it relies on to live instead. You ask if there is enough to eat and drink. You ask if there is a safe place to sleep. Is there enough here to survive? (Author’s emphasis.)

When you want to save something, you increase the things it relies on to live. When you want to destroy something, you reduce the things it relies on to live. That’s how monetary policy works, right? The Fed makes a move to slow wage rises in an attempt to slow the labor market in an attempt to slow hiring in an attempt to slow the economy in an attempt to slow inflation. Wages are the things we rely on to live. And they are often a tool in the fight against inflation.

The tool kit is limited.

Navigating the Fog

Its primary goal is to reach the summit of 2 percent inflation, even if it’s foggy and confusing. But Jeremy Rudd, a senior Federal Reserve economist, published a paper in 2022 that talked about how inflation expectations don’t really matter anymore. This is basically like saying the summit doesn’t exist (and maybe never did). He wrote, “Economists and economic policymakers believe that households’ and firms’ expectations of future inflation are a key determinant of actual inflation. A review of the relevant theoretical and empirical literature suggests that this belief rests on extremely shaky foundations.” (Author’s emphasis.)

Rather than saying, “Oh, yes, we know exactly what is happening,” Rudd was essentially saying, “Actually, we don’t know what is happening, and using expectations as a policy tool is extremely concerning.” Because when you zoom out and look at the overall situation, the Fed is wrong most of the time (as we all are).

It’s not so much the level of the rates (rates can be low and things can be fine; rates can be high and things can be less fine but still okay) but rather the big moves in rates. Low rates aren’t dangerous, but if they rise quickly, it’s financially destabilizing.

So the whole economic situation is energy prices, it’s a clearly higher cost of living, it’s higher wages but not really, but price increases anyway, and it’s supply chains and goods pressure—it’s how fast the Fed moves, how well monetary policy works—it’s a lot of little questions bubbling up to one big question: How can we fix it? It’s a tightrope, right? Companies have to pay people more to get them to work to make the things that people want because people have to spend money so GDP will go up because then the economy will grow, but it can’t grow too fast because then inflation will occur, but it can’t grow too slowly because then a recession will occur.

But the economic data points and subsequent interpretation are all relative. In the long run, inflation expectations are important, and almost every market to some degree is driven by this behavior based on expectations.

How well people expect stocks and cryptocurrencies to perform has a role in how they do perform in the long run. So reality is really about expectations. The economy is made up of people, right? So it checks out that what people think is going to happen (expectations) will drive their behavior (reality) and thus the Fed’s response (policy).

I mean technically, we are all the Federal Reserve.