Chapter 16

Monetary Policy

So what’s their game plan?

Let’s concentrate on the Federal Reserve as an example. Although it focuses on domestic policy, its actions often send ripples around the globe. It’s a high-stakes game, and its decisions can have far-reaching consequences that extend beyond the nation’s borders.

What Does the Fed Do?

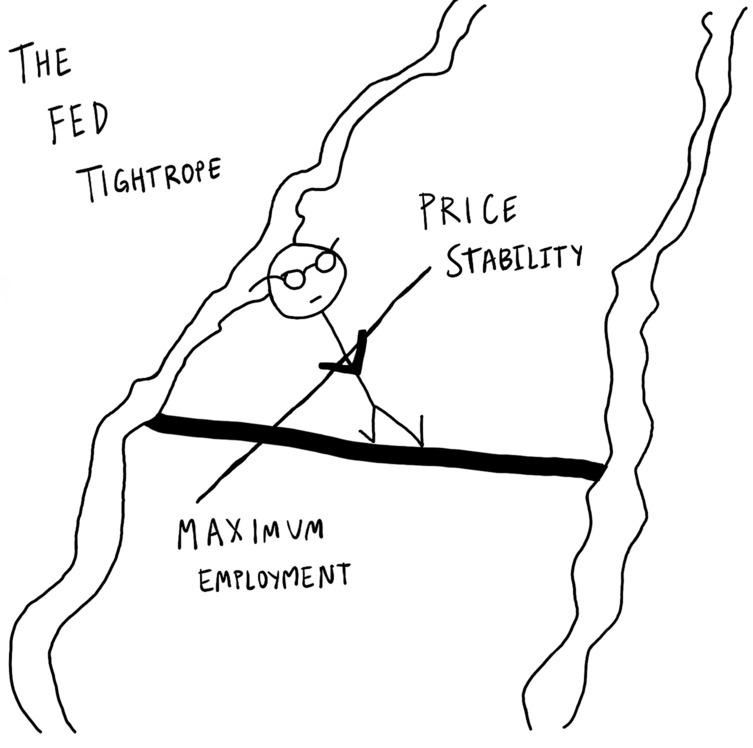

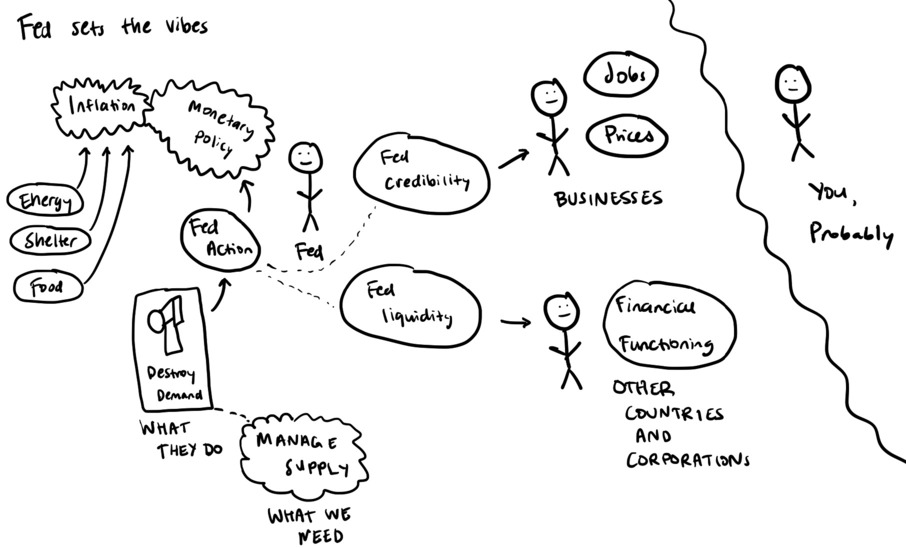

What exactly does the Fed do? It has a dual mandate—a tightrope walk at best.

The Fed wants to make sure that people have choices: that they are able to pay their living expenses and to get a job.

-

Mandate 1: Price stability. How can inflation be managed? How can the panicky “prices are rising” narrative be prevented from becoming a self-fulfilling prophecy? (More on that vicious cycle later.)

-

Mandate 2: Maximum employment. This the Fed’s second big focus in theory, though it’s hard to achieve when it’s hell-bent on keeping inflation down. The metric of maximum employment is about inclusion, diversity, and a job market for everyone.

The Fed has a tough walk on this dual-sided tightrope: It doesn’t want to overreact by moving rates too much and having the economy respond negatively, but it also doesn’t want to underreact and have the economy react even more negatively.

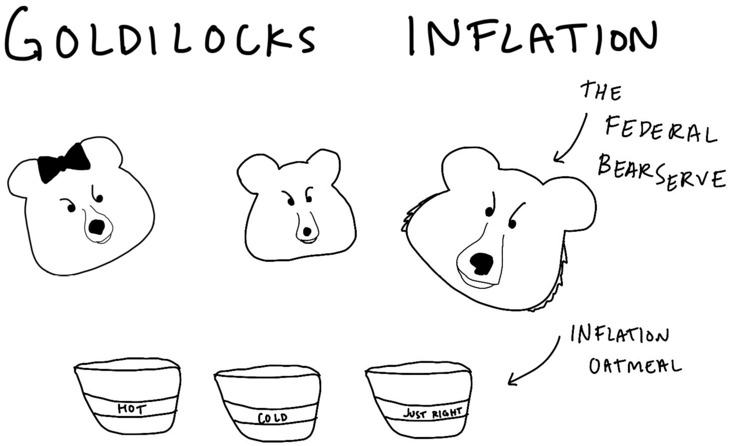

This is a delicate balance to maintain. It’s very much like Goldilocks and the porridge. Monetary policy is a big decision with a teeny tiny hammer, and there is a lot of gray area that the Federal Reserve has to be mindful of. Inflation can’t be too hot or too cold—it has to be just right, a Goldilocks zone.

The Federal Reserve has to manage both price stability (keeping prices reasonable) and jobs (keeping people employed), which is very difficult to do. If the scale tips in either direction, it can be disastrous.

Also on the high wire, it has to make sure that it maintains long-term, moderate interest rates. This is its secret third mandate, which translates to “making sure rates aren’t going wacky.” So how does the Fed make sure that it is meeting this dual mandate, as well as the secret third mandate? The most common tools used by central banks (including the Federal Reserve) are reserve requirements, open-market operations, the discount rate, and the fed funds rate.

How Do the Fed’s Tools Work?

There are two main types of monetary policy—contractionary and expansionary. Contractionary policy (raising rates, shrinking the balance sheet) is used when the Fed wants to slow the economy down. Expansionary monetary policy (cutting rates, increasing the balance sheet) is used when the Fed wants to speed the economy up.

Reserve Requirements

The reserve requirement is the minimum amount of money that a bank must hold in reserve to make sure that it has enough money to supply its customers’ demands. The Fed sets this number by mandating the percentage of a bank’s total deposits (including checking accounts, savings accounts, and money market accounts) that it’s required to have on hand overnight.

-

When the Fed increases the reserve requirement, it can reduce the amount of funds that institutions have available to lend, which slows the economy down.

-

When the Fed decreases the requirement, it increases the amount of funds available, which can speed the economy up.

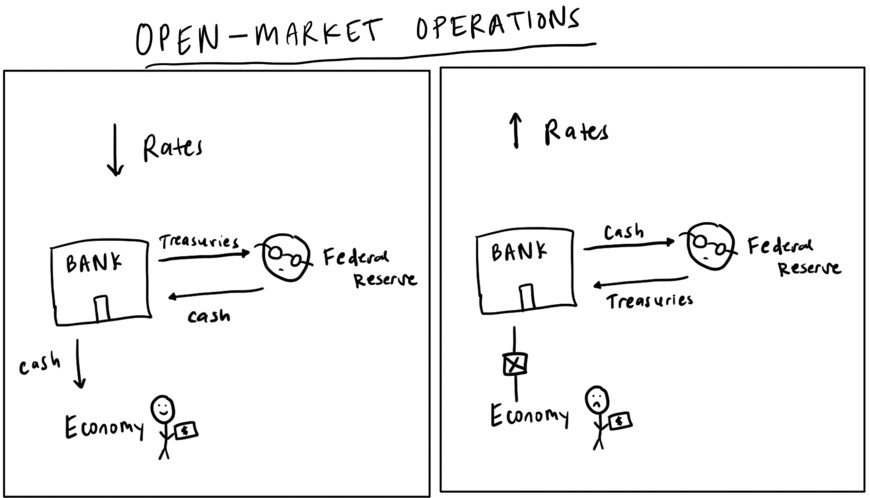

Open-Market Operations

The Fed can buy and sell U.S. Treasury securities (along with other financial assets) on the open market to regulate the money supply and nudge banks toward meeting the fed funds rate.

-

Quantitative Easing: If the Fed wants to lower interest rates, it buys Treasury bills from banks. This increases the reserves for banks because they get cash in exchange for the Treasury bills they sell to the Fed, enabling them to make more loans and more money to enter into the economy.

-

Quantitative Tightening: If the Fed wants to raise interest rates, it does the opposite by selling Treasury bills to banks. This decreases banks’ reserves and allows less money to enter the economy, thereby slowing things down.

Repo Agreements

The Federal Reserve engages in various market operations, including term and overnight repurchase (repo) agreements. These serve as short-term borrowing arrangements between financial institutions and central banks. The primary purpose of these agreements is to provide liquidity, which refers to access to cash or assets that can easily be converted into cash.

Here’s how repo agreements work:

-

The Federal Reserve buys securities, such as Treasury bonds, from financial institutions.

-

However, this purchase is not permanent. Instead, there is an agreement between the two parties that the financial institution will repurchase the same securities from the Federal Reserve at an agreed-upon date later on.

-

This repurchase arrangement acts as a collateralized short-term loan.

-

The key feature of a repo agreement is that the sale price of the security is higher than the repurchase price, creating a price difference between the two, which effectively represents the interest earned by the Federal Reserve. This difference in prices is known as the “repo rate.”

-

By setting the repo rate, the Federal Reserve can change short-term interest rates in the financial markets. A higher repo rate encourages financial institutions to participate in repo agreements with the Federal Reserve rather than lending to other banks or entities in the private market—which means they have less money available to lend to others in the market and therefore the economy slows and short-term interest rates rise. Conversely, when the repo rate is lower, financial institutions may find it more attractive to lend to other market participants, increasing the supply of funds and potentially lowering short-term interest rates.

The advantage for the financial institution is that it gains immediate access to cash or liquidity by selling the securities to the Federal Reserve. This additional funding, often referred to as “extra green,” can then be used by the financial institution to provide loans to individuals and businesses, supporting economic activities.

Types of Repo Agreements

It’s important to note that there are two types of repo agreements: term and overnight.

-

Term repo agreements have a longer duration, lasting a few days or weeks.

-

Overnight repo agreements are very short term, lasting only one day.

Institutions use repo agreements to meet daily liquidity needs—if they don’t have enough money on hand, they can enter into an overnight repo to cover the deficit. Term repos are used for longer-term liquidity need or project financing.

The Fed also has a tool called the Standing Repo Facility (SRF), which helps keep the money market stable. It provides liquidity to banks if they need it, giving them access to short-term funding through repurchase agreements (repos) with a central bank. This ensures that markets can function properly and provides money in case any banks need it. This is really important because if the money market goes haywire, it can cause big problems for the broader economy. The SRF helped keep things under control during the financial crisis of 2008, when lots of people were pulling their money out of money market funds—short-term investments that are supposed to be low risk. Basically, the Fed acts as the firefighter of the economy, putting out financial blazes before they turn into infernos.

The Discount Rate

The discount rate is the interest rate that the Fed charges on loans made through the discount window. It’s set above the fed funds rate to discourage borrowers from using it. Institutions normally borrow from the discount window if they desperately, desperately need money—it serves as a safety net for stability, particularly during times of financial stress.

But the discount rate is more than just a way for the Fed to make money off loans; it’s actually a signal that tells us what the Fed is thinking about the economy. Think of it as a traffic light for the economy.

-

When the light is green (the discount rate is low), banks are free to borrow and lend money more easily, and the economy can speed along.

-

But when the light turns yellow (the Fed raises the discount rate), banks know they need to chill out because borrowing money just got more expensive.

-

And when the light turns red (the discount rate is really high), banks know they need to stop and reevaluate their strategies because borrowing money is just too costly.

The Fed Funds Rate

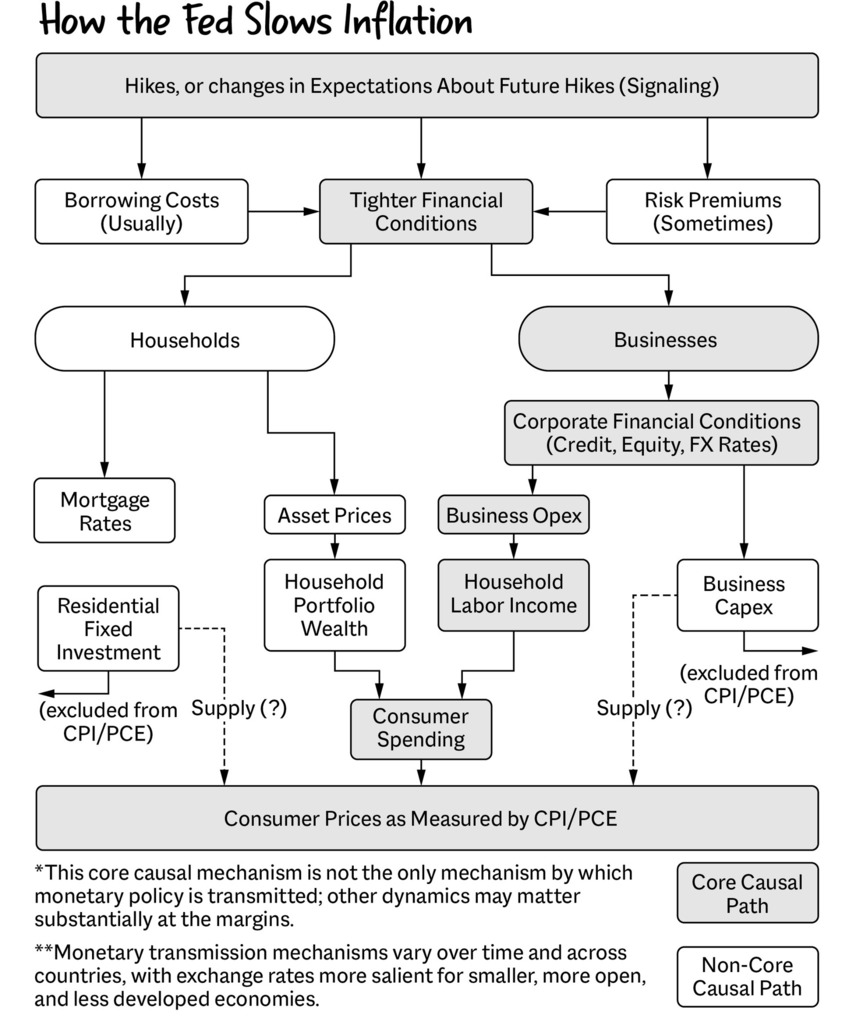

The point of this rate (referred to as the bank rate in the United Kingdom, the refinancing rate in the European Central Bank, and other names in other nations) is to make it more or less expensive to be alive—to change the cost of money. Central banks set a target range for the interest rates that depository institutions charge each other for overnight loans to meet reserve requirements when one has a shortfall and another has an excess at the end of day (EOD). Though we say the Fed “sets” the fed funds rate, it is really using other tools, such as open-market operations, to make borrowing more expensive. When inflation is really high, the Fed wants people to chill out and stop spending money. So it nudges the fed funds rate upward, and banks then pass the cost along to consumers in the form of higher interest rates on everything from car loans to credit card payments. Everyone says, “Okay,” and stops taking out financing, which slows the economy down, which eventually slows inflation.

When the economy isn’t doing so hot, it’s the opposite: The Fed wants people to spend money. So the people at the Fed push the funds rate downward—or slash it to zero, as they did in December 2008 and March 2020—making it cheaper to finance cars, homes, anything that you have to get a loan for. Everyone says, “Okay!” and starts taking out financing, speeding the economy up, which eventually speeds inflation up.

Being a Central Bank Is About Belief

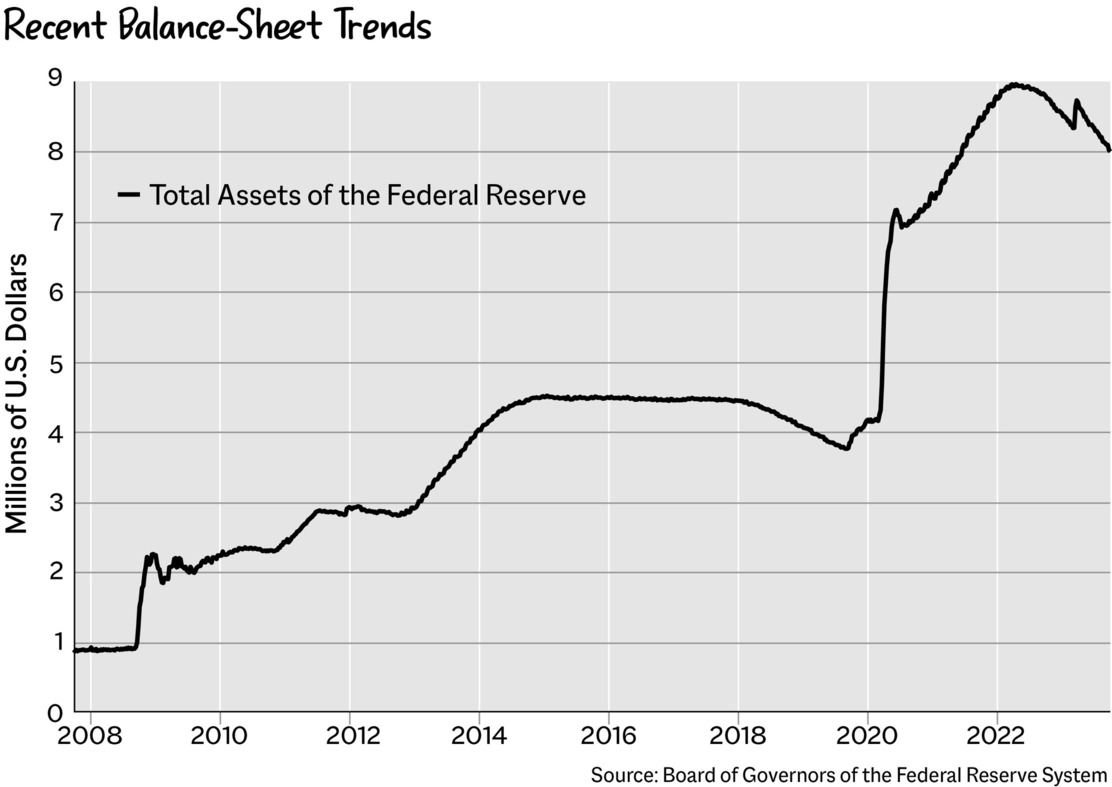

When the financial system started melting down during the 2008 Great Financial Crisis (GFC), the Fed had to implement new tools, as its existing playbook was no longer working. That was when quantitative easing (QE) came on the scene, similar to open-market operations, except that central banks buy long-term bonds and securities, such as mortgage securities, rather than just short-term Treasury bills, with the goal of impacting various interest rates and getting specific parts of the economy rolling again.

The Fed slashed rates in 2008 and did three rounds of QE (2008–2010, 2010–2011, and 2012–2014) as well as Operation Twist, selling short-term Treasury securities and buying an equivalent long-term to try to lower long-term rates without increasing the balance sheet. They also developed the Term Auction Facility and several other facilities to try to provide money to markets.

After letting the balance sheet grow substantially after 2008, in 2018 the Fed began to reduce the size of the balance sheet (an unprecedented move at the time!) in response to rising interest rates. It imposed a $10 billion cap on monthly runoff, increasing it to $50 billion over the course of a year.

As the Fed began to increase the use of reverse repos to reduce its balance sheet, the demand for these transactions surged. Banks were stoked to lend money to the Fed, because what could be a safer and more reliable borrower than the Federal Reserve? But because the demand spiked, the interest rate on reverse repo transactions fell. At one point, it went negative, with banks paying to transact with the Fed.

Soon enough, there was a shortage of cash in the financial system. In September 2019, the U.S. overnight money market (financial markets in which short-term, low-risk debt securities are traded) experienced some wild volatility. There were two main causes: first, corporate tax payments were due September 16, so money left money market mutual fund accounts and banks and was sent to the Treasury, and second, $54 billion of Treasury debt was due. So a bunch of cash was drained.

Like $120 billion worth.

The rate movements were huge, and the Fed had to reverse its QT process in order to stabilize the financial system. Of course, that was a statistically wild event, but it was underscored by the ridiculousness of financial systems. It was a nightmarish mess and one that spooked people about monetary policy yet again.

Zero interest rates are a lot easier to deal with than “normal” interest rates are. This is known as zero interest rate policy, or ZIRP, and it brought a lot of excess in the years following the GFC. It indirectly led to many speculative bubbles, including meme mania.

There was a particularly grand spree of QE in 2020 after the covid-19 pandemic hit.

Monetary Policy in 2020

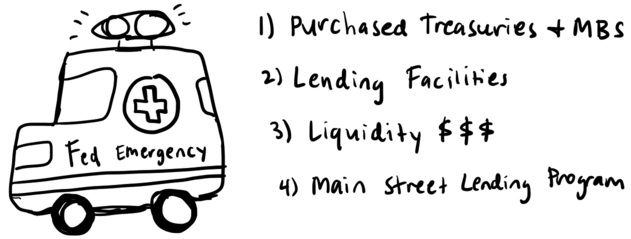

The Fed wanted people to SPEND—to go buy homes, cars, and groceries to fill their fridge (and maybe even the fancy kind of pickles!). So it dropped the reserve requirement in the hope that banks would lend more, credit markets would get their groove back, and borrowing would be cheaper across the board for businesses and households.

It went on a shopping spree! It purchased a ton of Treasury securities and mortgage-backed securities (MBS), bundles of home loans and other real estate debt obligations that can be passed from the bank that issued them to other parties in large quantities to inject some cash into the financial system.

It implemented lending facilities. Think of these as being like support systems for credit markets, helping out businesses and even local governments. It was like giving them a helping hand to access the funding they needed during those tough times. Things like the Primary Dealer Credit Facility provided short-term loans to dealers (firms that trade directly with the Federal Reserve and U.S. Treasury), and the Commercial Paper Funding Facility facilitated the issuance of commercial paper to companies to help support credit flow to households—basically, they got money to people.

It also made sure that money market funds didn’t freeze up, by providing them some liquidity injections.

It created the Main Street Lending Program, which was all about supporting small and midsized businesses. It wanted to make sure that mom-and-pop shops and growing companies got the help they needed to survive the economic downturn.

Those moves did much to stabilize the markets and probably helped us avoid another Great Depression. As Nick Timiraos of The Wall Street Journal wrote in Trillion Dollar Triage, a chronicle of the Fed’s action during the pandemic: “The central bank can help boost demand when the economy slumps; there was no precedent for what policymakers would soon face—the equivalent of an economy placed into a medically induced coma. And rash action risked panicking the markets further. As he disembarked from the plane, Powell already knew one thing: doing nothing was not an option.”

There has been a lot of criticism of what the Fed did during the pandemic, with some saying that it overstepped its authority and did too much, but it’s also true that they (and everyone) were dealing with impossible circumstances.

Oil prices had suddenly gone negative, meaning that traders were paying buyers to take barrels off their hands—a historic quirk in the market that should never have happened. We’re talking about our most traded commodity here! The head of oil markets at Rystad Energy, Bjørnar Tonhaugen, described it as an oil Everest but in reverse: “Oil prices not only hit rock bottom, but they also broke the rock.” That goes against all the economic laws of the known universe.

Meanwhile, high-yield debt (high-risk, potentially high-reward bonds, also known as junk bonds) was blowing out, meaning that yields were skyrocketing, because no one wanted to own anything risky. And people were losing their jobs. Central banks around the world did what they thought was best—and doing too much was probably better than doing too little. If the central banks hadn’t intervened, the world likely would have experienced a worldwide depression, as it did in 1929. The world was shutting down. It was a once-in-a-lifetime event, and it needed once-in-a-lifetime support. The following factors had to be taken into consideration.

-

People are the economy.

-

Monetary policy exists to stabilize the economy.

-

Monetary policy is meant to help people.

-

Does it always? No, of course not.

People really like policy only when the car is driving forward (cutting rates and quantitative easing) versus driving in reverse (raising rates and quantitative tightening). QT policies aim to shrink the Fed’s balance sheet, reduce their bond holdings, or raise interest rates. The Fed begins QT with a process known as runoff, which allows bonds to mature without reinvesting the proceeds.

These contractionary policy tools are a bit slippery to pin down, as are most aspects of monetary policy, because, as much confidence as the Fed may project, no one really knows how they work. No one really knows what the best interest rate is or how shrinking the Fed’s bond holdings will impact the economy. It’s a guess.

For example, the 2022–2023 balance sheet runoff: its pace was much faster than in 2018. The Fed let $95 billion in securities mature every month, $60 billion in Treasuries, and $35 billion in mortgage-backed securities (a financial product in which banks sell debt obligations—in this case, home and real estate loans—to investors who take their place in waiting to collect repayment). This is a huge number, compounded by the Fed raising rates quickly.

But there was a Repo Crisis 2.0—kind of!

Silicon Valley Bank (SVB) failed in 2023 because it had no hedges and no protection on the bonds that it owned. It owned a lot of Treasury securities, and when the Fed started raising interest rates, those securities lost a lot of value. When the rates went up, the prices of the securities went down.

Silicon Valley Bank was caught in the crossfire of the fast and furious Federal Reserve moves. State regulators in California and at the Federal Reserve Bank of San Francisco had been aware of excessive risk-taking and poor internal management at SVB in the years leading up to its demise. Eyebrows had gone up, and reports had been issued, but oversight teams didn’t apply enough pressure for the bank to get back onto the straight and narrow.

SVB was just one casualty of monetary policy. What the Fed did in 2023 also contributed to the downfall of Credit Suisse, a 167-year-old organization, causing distress in regional banks and showing the power of social media to create a bank run (the relationship between social media and bank runs could be a book in itself). The Swiss investment bank UBS acquired the remains of Credit Suisse and will likely downsize some parts of it and sell off others.

Fed Cred

Being a central bank is hard. The Fed, for instance, has to rely on a few things that are technically outside its control to achieve the goal of slowing the economy down:

-

People have to believe it can do it. A lot of what the Fed does hinges on its credibility—which it arguably still has. But if all of a sudden, the market is like, “Ha-ha, Fed is lame and can’t do anything,” it makes its policy actions more difficult. If people expect inflation to rise, they are going to hurry up and buy things before they get more expensive. Employees also might be more aggressive about negotiating higher pay, and companies may preemptively raise prices to make up the difference (or just because everyone else is doing it and they can get away with it!). The central bank cares about what people think is going to happen—because that’s usually what ends up happening. That’s why Fed cred—or the lack thereof—can be the downfall of monetary policy.

-

The tool kit has to work. The Fed bankers can push their levers of open-market operations, reverse repo, the discount rate, and attempts to project gravitas and credibility, but ultimately, all of these instruments are somewhat indirect. They don’t have a 100 percent success rate. In the 2010s, for instance, the Fed wasn’t able to boost inflation (and with it, economic growth) the way it wanted to.

It’s impossible to predict the future accurately, yet that is what we ask central bankers all over the world to do. So how do they do it?