Chapter 15

Fiscal Policy

What Is Fiscal Policy?

Fiscal policy, the mighty tool wielded by governments, utilizes federal spending, taxation, and borrowing to influence individual and corporate financial decisions, maintain the economy’s delicate balance (or attempt to), and ultimately, shape the destiny of nations. This chapter will walk through how the government wields its financial power through spending programs and tax policies to manage the country’s overall economic stability. Let’s start by getting a few misconceptions out of the way.

-

Government spending is to blame for inflation. Productive government spending is quite good for the economy. Think public transit (not the one more lane bro for highways but actual investment in subways and light rails), education, healthcare, environmental protection, and scientific research. If the government is spending on things that aren’t useful (say, sending billions of taxpayer dollars toward maintaining empty buildings), that’s another story.

-

Government deficits are always irresponsible. It’s okay for the government to spend more than it makes, or run a deficit, especially when it is spending on the aforementioned productive investments. Think of it as investing in a class to become a certified electrician—a necessary up-front expense for a benefit that will pay off down the road.

-

Trade deficits are bad for the economy. Again, it’s not inherently bad for a country to import more goods than it exports—to buy more things from other countries than it sells to other countries. What’s important are capital flows. As long as a country with a trade deficit continues to attract investments in its stock and bond markets, the overall balance remains in check.

When we are in an economic downturn or are anticipating a recession (basically when things look dicey), the government’s go-to move is to spend money—pouring funds into infrastructure projects or education or dispersing stimulus payments as we saw in 2020, accompanied by tax cuts and strategic borrowing of bills, bonds, notes, and more. This should unleash a wave of economic energy, creating jobs and fueling the demand for goods and services. The atmosphere transforms, consumer confidence rises, and the economic vibes grow stronger. The party is in full swing. But if the government borrows too much—and isn’t careful with how it spends the money—it can lead to high inflation, which we know can be a problem!

When the government tightens its purse strings (its default response to high inflation), through either tax increases or a slowdown in borrowing, the once lively gathering loses its momentum, bringing an abrupt end to the festivities. The flow of money, which is vital for people and businesses, becomes restricted, affecting their spending capacity.

What Does the Government Spend Money On?

The government spends money on a lot of things, including:

-

Social programs. These include social welfare programs such as housing assistance, unemployment benefits, educational programs, food assistance, and other forms of social safety nets.

-

Defense and security. This is all about military, national defense, and homeland security. It covers the costs of maintaining armed forces, defense infrastructure, weapons, and equipment, as well as funding military operations and initiatives.

-

Infrastructure development. This includes spending on public assets, including roads, bridges, airports, railways, public transportation systems, water supply networks, and other critical infrastructure.

-

Public services. This covers the cost of government operations and services to the public including government agencies, administrative functions, law enforcement, and firefighting.

-

Debt interest payments. These are funds to service government debt obligations. This spending includes interest payments on outstanding government debt issued through bonds and other securities, financial instruments used to help fund various operations.

-

Research and development. This includes investment in research and development that supports scientific advancements, technological innovations, and initiatives to address societal challenges that are meant to encourage innovation.

-

Subsidies and grants. These support specific industries, businesses, and individuals to promote economic growth and job creation and to foster specific sectors and projects.

-

Foreign aid. This is financial assistance or resources to other countries to support their development, address humanitarian crises, and foster good diplomatic relations.

All of these things are partially funded by taxes.

Taxes

In the United States, the tax system, like the monetary system, is based on the full faith and credit of the United States. In other words, people are going to pay taxes only if they believe in the system collecting them. There would have to be a catastrophic level of loss of faith for them not to, and there is a reason that the government has to maintain the trust of the people it serves! Democracy fundamentally depends on the belief and engagement of its citizens; without their trust and active participation, it risks transforming into a different system entirely, where power is concentrated in the hands of a few. Without public belief in the integrity and ability of the government to serve the nation’s best interests, the foundation of democracy becomes shaky. When people stop believing in the government’s ability to make responsible decisions, there is a risk of widespread disillusionment, political apathy, and social unrest. So taxes are more than just a tool to raise money; they are a social consensus mechanism that enables civic engagement and shapes societal priorities (sort of).

Unlike the United States, which pulls in most of its money through income taxes, more than 170 countries, including all those in Europe, collect a value-added tax, or VAT. It’s seen as a way to generate money for the government without all of the burden falling on individual taxpayers; it also simplifies income tax filing, provides a consumption-based tax versus income-based tax, and is an evenly distributed burden because the tax is added to the price of goods and services at every stage of production and distribution.

But let’s talk about the burden facing the individual taxpayer. If you’re American, you pay a percentage of your income to the government, collected by the Internal Revenue Service (IRS). The government uses a progressive income tax system, which means that the more money you make, the higher the percentage of your income you pay in taxes (usually, that is; some people know how to do some fancy accounting so that they pay less). There are seven tax brackets, with rates ranging from 10% to 37%. How much each individual pays is a bit complicated—but it’s all about margins. You don’t pay 37% on all of your income, just on the amount above the previous tax bracket. Here is the tax table for 2023:

Marginal tax brackets for tax year 2023, single individuals |

|

Taxable Income |

Taxes Owed |

Marginal tax brackets for tax year 2023, married filing jointly |

|

Taxable Income |

Taxes Owed |

|

Credit: Table: Gabriel Cortes/CNBC Source: IRS |

|

In Canada, the federal government also uses a progressive income tax system, but the tax brackets and rates are different from those in the United States. There are currently four federal tax brackets, with rates ranging from 15% to 33%. Similarly to the United States, it’s tiered, so if you make $70,000, you’ll pay 15% on the first $50,197 and then 20.5% on the remaining.

Finally, in the United Kingdom, the income tax system uses a progressive system with various tax brackets and rates. There are currently four tax bands, with rates ranging from 20% to 45%. In March 2023, Chancellor of the Exchequer Jeremy Hunt froze the personal allowance until April 2028. The idea is that pay raises will move people into the higher tax brackets. But taxpayers in the United Kingdom still pay a decent amount in national income, VAT, and council tax and rates.

How income tax levels in England, Wales, and Northern Ireland* will change from April |

|||

Band |

Current |

New |

Rate |

|

*Scotland sets its own bands and rates **Reduced by £1 for every £2 earned between £100,000 and £125,140 |

|||

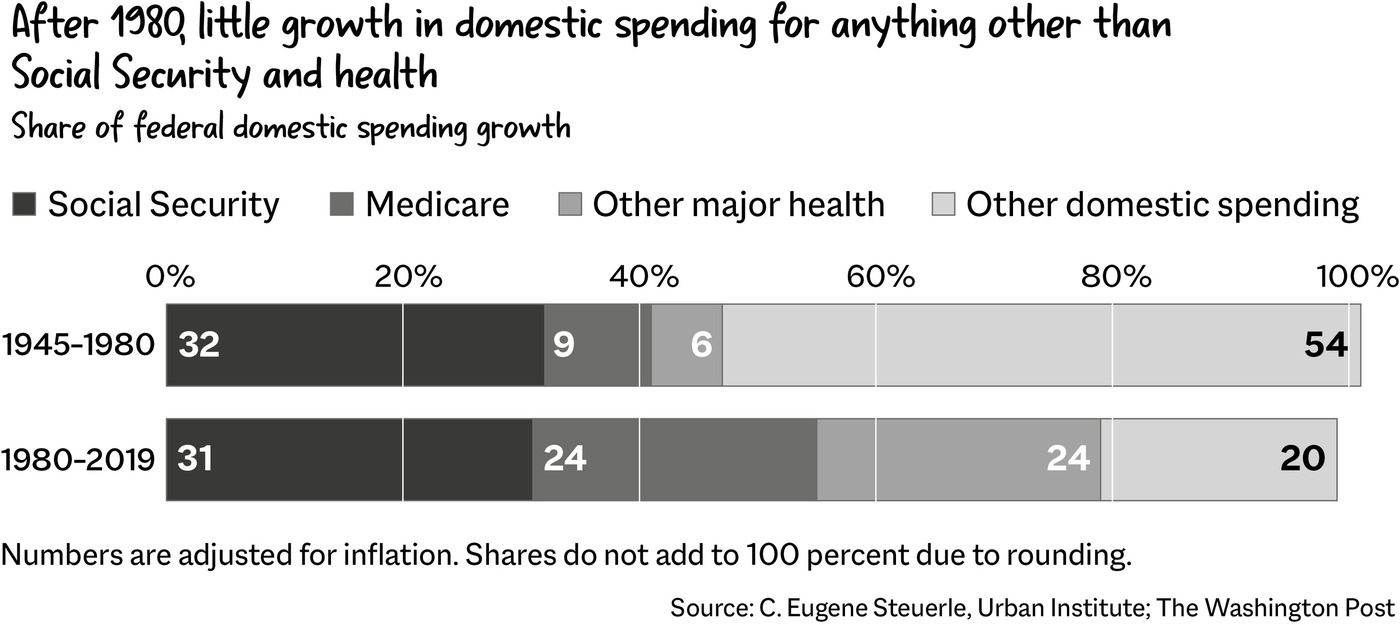

Each of these tax systems has pros and cons. The United Kingdom’s tax system funds the National Health Service, providing free healthcare, and contributes to a substantial social safety net and public education. But the tax rates are high, and the entire economy has been funky since Brexit. In Canada, the healthcare benefit situation is similar, and tax revenue is also used to help combat climate change. But Canada also has regional disparities and a housing crisis. United States taxes fund healthcare, with an increasing percentage going toward Medicare and Social Security.

Bonds

The government makes the lion’s share of its money through individual income taxes (federal, state, and local), with a healthy stream coming in from payroll taxes for Social Security and Medicare, corporate income taxes, and a trickle coming from fees, fines, and assets it sells off (lighthouses, seized homes, and other property). But usually, taxes, fees, and fines don’t quite cover what the government needs to fund its programs, so it issues bonds.

Bonds, as discussed in the Stock Market chapter, are a promise to pay money back at some point in the future, and markets (usually made up of foreign governments, like China’s and Japan’s, mutual funds, depository institutions, state and local governments, pension funds, insurance companies, and others, like individuals, banks, and corporate businesses) say, “Ah, yes, we will buy that from you.” The government is then able to execute on public infrastructure, social spending, and other projects.

There are different types of government debt. Bonds, known for their stability and low risk, are backed by the full faith and credit of the U.S. government. Municipal bonds are issued by state and local governments to fund projects such as schools, highways, and utilities. Corporate bonds, which enable companies to raise money by borrowing money from investors, provide varying levels of risk and return potential for investors, depending on the creditworthiness of the issuing corporation.

Type of Bond |

Issuer |

Primary Purpose |

The Debt Ceiling

This brings us to the debt ceiling, a cap on how much the government can borrow to pay for things such as roads, public schools, and the military. It’s set by Congress and is often compared to a credit limit, but for the government. In 2023, Congress fought the battle again—and the government narrowly evaded collapse.

It’s stressful to have the government almost collapse every few months because it can’t pay its bills. People are furious, and they should be. Why are our elected officials allowing federal workers to be repeatedly threatened with mass furloughs and hiring freezes, and endangering crucial programs and services like WIC, the special supplemental nutrition program for Women, Infants, and Children? It’s stupid. But that’s why we need to understand it.

The goal of the debt ceiling is to give Congress more control over government spending. It was intended to limit the amount of debt the government could take on, but over time, it has become more of a political football than a useful tool for moderating government spending—something used to try to extract political concessions or virtue signal to legislators’ bases in an era of dysfunctional bipartisanship (not to mention of wasting everyone’s time and money).

The original intention of the debt ceiling was to promote fiscal responsibility, but we have strayed far from that. It’s a flawed mechanism that exacerbates partisan gridlock and threatens the nation’s financial stability. Rather than fostering prudent fiscal management, it has turned into a tool of political posturing, with politicians using it as leverage to advance their own agendas, often at the expense of the nation’s well-being.

Abolishing the debt ceiling would be a step toward restoring fiscal sanity and promoting rational decision-making! By eliminating this arbitrary limit on government borrowing, Congress could focus on more substantive debates about spending and revenue without having to resort to brinkmanship and theatrics. The debt ceiling is also ineffective at controlling government spending; it doesn’t even look at the underlying causes of deficits or encourage long-term fiscal planning.

The debt ceiling’s original purpose has been overshadowed by its adverse consequences, making it a detrimental relic of the past. Abolishing it would signal a commitment to pragmatic governance and demonstrate a willingness to tackle the nation’s fiscal challenges with seriousness and deliberation. By doing away with this counterproductive mechanism, Congress could pave the way for a more stable, transparent, and effective fiscal policy.

Congress is almost always battling over the debt ceiling; it has moved the debt ceiling seventy-nine times since 1960, and every time the government approaches the limit, anxiety spikes about the prospect of its hitting it and being unable to meet its financial obligations. In recent go-arounds, conversations have sounded approximately like this:

Republicans do not like the level of spending Democrats want for programs to improve education, transportation, housing, scientific research, and environmental protection (which is what the government is designed to do at a base level). Both parties are guilty of trying to score political points at the absolute worst moment, because there is a potentially severe fallout from not solving the debt ceiling problem.

What would the consequences of breaching the debt ceiling be?

-

The Treasury would stop functioning. If the Treasury can’t keep money flowing back and forth and the government shuts down, payments to federal workers, agencies, Social Security beneficiaries, and Medicare providers would be delayed, financial markets could panic, and public confidence in our political institutions would be (justifiably) shaken. Even though the government has technically hit the debt ceiling limit before, the Treasury has always bought enough time for Congress to strike a deal by using cash on hand (a limited supply of money that’s ideally supposed to be kept on hand) and what it calls “extraordinary measures” (aka creative accounting maneuvers). If the government does default, lenders will become highly reluctant to lend to the United States, and those who do will demand higher interest rates. This would result in even more of the government’s budget allocated toward interest payments.

-

The United States could go into default. This would be unprecedented, and the cascading effects would be catastrophic—including a downgrade by credit rating agencies, higher borrowing costs, and a recession, creating problems both for everyday consumers and for the United States as a global power. For the time being, the U.S. dollar is the premier reserve currency of the world (meaning that it’s the currency most commonly held by central banks and major financial institutions around the world) because the United States is currently King Daddy of the world and has the biggest economy. A default would shatter global trust in the U.S. government at a very delicate geopolitical moment—and make everyone question the strength of the United States and the dollar.

The United States is one of the only countries that has a debt ceiling; Denmark does, too, but it isn’t weird about it like the United States is. Other countries are concerned about their debt loads (Switzerland and Norway have virtually no debt, so not them), but the United States is the only one that uses it as a political football and puts the fate of the country at risk every few years. Other countries, including Germany, Italy, Poland, and Switzerland, have balanced budget provisions. Germany has a debt brake, or Schuldenbremse, which puts a limit on the structural deficit the government can run. France has a fiscal rule called the “golden rule,” which sets a limit on the structural budget deficit.

The debt ceiling is bad. It is simply, objectively, bad. Not only because it’s glorified paper pushing, but also because it undermines confidence in the U.S. economy, makes market expectations go haywire, and creates unnecessary stress for us all—especially federal employees, who have to worry about whether they’ll be paid if there is an extended impasse and the Treasury runs out of cash to fulfill its obligations. The debt ceiling comes into conversation only because the government is funded by us, the taxpayers.

The United Kingdom Shows That Fiscal Policy Is an Art

How the government decides to handle taxes, government spending, and borrowing is key. The United Kingdom ran into this head-on with Prime Minister Liz Truss, who in September 2022, during a period of inflation, announced a “minibudget.” The budget included increased tax cuts and a lot of government spending, which was very fiscally loose. Misplaced tax cuts, just like loose monetary policy, are inflationary, and the inflationary pressures contributed to Truss famously having a shorter shelf life as PM than a head of iceberg lettuce from the supermarket.

The introduction of the minibudget (and subsequent market reaction) caused the price of government bonds (called “gilts” in the United Kingdom) to collapse. The market deemed the minibudget irresponsible because in the inflationary environment, it was very much not the time to be cutting taxes! People were like, “It’s insane to be doing fiscal easing in the middle of an inflationary crisis because you’re going to cause more inflation.”

Once the sell-off began, it was assumed that the Bank of England would step in and fix everything: do an emergency rate hike, buy bonds, anything. But it didn’t. In one example of the extremity of market moves, the yield on thirty-year U.K. inflation-linked bonds jumped by more than 250% (meaning that they fell 250% in price) after the Bank made the announcement that it was not going to intervene.

The reason that the Bank ended up going all in was that there was a liquidity crisis in liability-driven investment (LDI) funds that were very invested in gilt-edged securities, the government Treasuries. Gilts, of course, were selling off. So the LDIs were not doing that well. And it turned out that pension funds, which people use for support in retirement, owned a lot of LDIs. So the pension funds were at risk of blowing up.

The Bank had to do something. So it stepped in. It bought bonds! However, the move was ineffective because it functioned as a quantitative easing program about a week after the bank had announced quantitative tightening (I will discuss the specifics of that later) with almost 10 percent inflation as the backdrop.

There were so many things going on! The U.K. government had an expansionary fiscal policy that was largely inflationary, freaking everyone out because inflation was already so bad. Then the Bank of England had to step in to save the government from itself!

That crisis revealed the political limits of fiscal policy, at least during times of high inflation. It threw the United Kingdom into austerity, constraining both bad and good economic plans. It also underscored the power of monetary policy—and how influential our central banks have become.

Lessons from the Eurozone

The eurozone debt crisis, which began in 2009, is a good example of the importance of a certain level of debt management. Several countries using the euro as their currency, including Greece, Ireland, Portugal, Spain, and Italy, faced severe financial difficulties, with high levels of public debt, soaring borrowing costs, and struggling economies. The crisis led to concerns that the eurozone might break up, which could have had profound consequences for global financial markets and the world economy. Ultimately, the eurozone was saved by the creation of the European Financial Stability Facility (EFSF) and the European Stability Mechanism (ESM), the European Central Bank (ECB) intervening with liquidity support, a banking union, bailout packages provided by the IMF, and, most important, by Angela Merkel, the German chancellor, agreeing to support the euro.

Basically, Germany needed to run a deficit to help save all the other European countries, specifically Greece (George Papandreou, its prime minister at the time, had agreed to a massive sovereign default that had sent the country’s economy into a downward spiral) and Italy. Merkel wanted nothing to do with it. When asked by U.S. president Barack Obama and French president Nicolas Sarkozy to increase contributions to the eurozone “firewall,” “to the astonishment of almost everyone in the room, Angela Merkel began to cry. ‘Das ist nicht fair.’ That is not fair, the German chancellor said angrily, tears welling in her eyes. ‘Ich bringe mich nicht selbst um.’ I am not going to commit suicide.”

Germany ended up contributing, saving the euro. There were lessons in there about the balance of austerity— the fact that some government spending is important and, as Mark Dow of Behavioral Macro, put it, “There should be no doubt by now that markets, economists, and pretty much everyone for the past generation has underrated the power/utility/capacity of fiscal policy, and overrated the power/utility/capacity of monetary policy.”

Can the Government Survive?

A government’s decisions on spending, taxation, and borrowing not only have immediate effects on the economy but also shape the trajectory of society over time. Policymakers have an ethical responsibility to consider the interests of both present and future generations when formulating fiscal strategies.

There are a lot of questions about what is going to happen with entitlements, support, and deficits at a certain point, especially considering all the noise about Social Security running out by 2030 in the United States, pensions potentially drying up in the United Kingdom, and so on.

It makes sense to worry about this stuff. My grandma worked at one company her whole life (and worked very hard), retired in her sixties, and is still living off her pension in her nineties. That is likely not going to happen for the younger generations. Populations are aging, and life expectancies are increasing. In 1940, there were forty-two workers per retiree, but that number has fallen to three to one, meaning that there are not nearly enough workers to support Social Security beneficiaries.

Japan is a good example of a real-time fiscal and monetary experiment in the face of challenging demographics. Japan has one of the world’s most rapidly aging populations. This demographic trend has resulted in a declining workforce and a rising number of retirees. As a result, Japan’s public debt–to–GDP ratio is among the highest in the world as the government has run a huge deficit over the years in an attempt to support the population. So it has passed various fiscal stimulus packages to boost demand, mainly through spending on infrastructure projects and social programs, as well as a lot of support from their central bank, the Bank of Japan.

Basically, governments are running a lot of fiscal experiments in real time.

Fiscal Policy Is Good, Actually

Alex Williams, an economist at EmployAmerica, developed something he called a “Frying Pan Chart” to describe the idea that the 2010s are over or the concept that fiscal spending is not always a bad thing. The chart that follows looks like a frying pan—you can see the dip during 2010, when fiscal austerity, the government spending less, was a popular ideology. But during both the Trump (mostly in the form of tax cuts) and Biden administrations, government spending was big, including the CHIPS Act of 2022, the Inflation Reduction Act of 2022, and the Infrastructure Investment and Jobs Act of 2021.

The Frying Pan Chart bolsters the idea that the government can—and should—spend money. The fact that we didn’t during the 2010s because of the idea that governments shouldn’t spend money was net harmful.

As the early-twentieth-century economist John Maynard Keynes said, “Anything we can actually do, we can afford.” Governments exist to spend money.

Borrowing money is okay! It really is! A lot of people scream about deficits, but red ink in the federal budget isn’t cause for alarm the way it would be in say, a family’s budget, especially if the borrowing is being spent on productive things such as infrastructure or education. Olivier Blanchard, a former chief economist at the International Monetary Fund (IMF), argued that there are benefits to high levels of government debt in a low-interest-rate environment—not an argument for more public debt, just an acknowledgment that debt isn’t always a bogeyman.

That being said, interest rates skyrocketed in 2022 and 2023 as the Fed raised them to fight inflation, creating higher interest payments for the U.S. government. But the real problem comes when a country borrows money to pay for the money that it’s already borrowed—that’s a real debt-death-doom loop.