Chapter 14

Recessions

Recessions and Economic Downturns

Recessions occur when the economy shifts from a period of expansion to contraction, and it can be a technical nightmare to figure out if we are in one.

Even when the economy is technically not in a recession, high gas and food prices can make it feel like one. Recessions, an unfortunate economic reality, are some of the scariest things we have to deal with. They’re one of those economic maladies that plague us because of the boom-bust cycle of our economic systems.

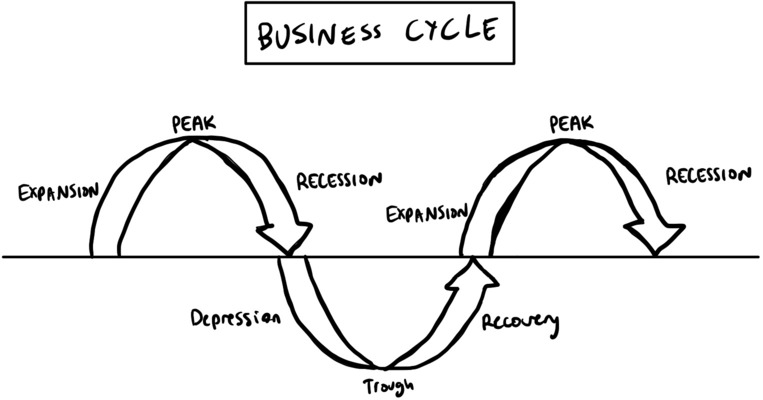

The world is cyclical, and the economy fluctuates between periods of economic expansion and contraction due to changes in government policy, consumer sentiment, spending, and business investment. The markets love “line go up,” which creates a lot of incentives for things to go up in the broader economy! And to go up way too fast! Eventually, all of it—the economy, markets, and everything in between—will come crashing down.

The Semantics of a Recession

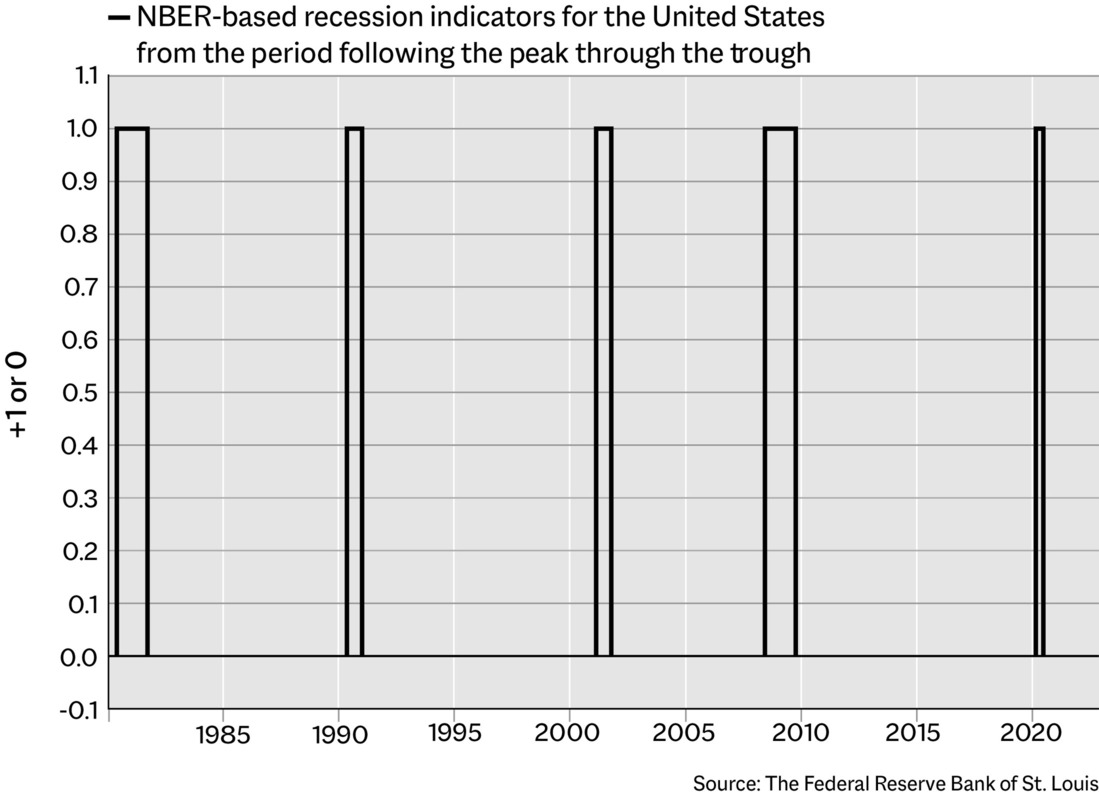

The strangest thing about recessions is that we usually don’t know if we are in one until after it’s happened. In the United States, recessions are determined by the National Bureau of Economic Research (NBER), a nonprofit organization that uses various metrics to figure out where we are in the economic cycle. They take into account a whole slew of economic data, including:

-

Total nonfarm employees

-

Employment level

-

Industrial production

-

Real manufacturing and trade-industry sales

-

Real personal income excluding transfers

-

Real personal consumption expenditures

-

Gross domestic product (GDP)

-

Gross domestic income (GDI)

-

The average of GDP and GDI

There isn’t a fixed rule to determine when recessions happen; it’s just a combination of the above data points and the general vibe that NBER gets from the economy. It looks at depth, diffusion, and duration (the three D’s).

-

Depth: how much economic indicators deteriorate

-

Diffusion: how broad that deterioration is across the economy

-

Duration: how long the deterioration lasts

For example, we had a recession from February to April 2020 when the covid-19 pandemic began. Twenty-one million jobs were lost in two months—the depth was there, as production levels, employment levels, retail sales, spending, and personal income all collapsed. The diffusion was there, too, with economic weakness across almost every single industry. Duration was a little different, as the recession was only two months, but it was so deep and widespread that the amount of time didn’t matter.

However, there is an element of subjectivity in determining if we are actually in a recession. As James Hamilton of the University of California at San Diego wrote:

The NBER’s dates as to when U.S. recessions began and ended are based on the subjective judgment of the committee members, which raises two potential concerns. First, the announcements often come long after the event. For example, NBER waited until July 17, 2003 to announce that the 2001 recession ended in November, 2001. Second, outsiders might wonder (perhaps without justification) whether the dates of announcements are entirely independent of political considerations. For example, there might be some benefit to the presidential incumbent of delaying a declaration that a recession had started or accelerating a declaration that a recession had ended.

NBER is pretty subjective—it takes its sweet time and isn’t immune to politics (just like any other institution).

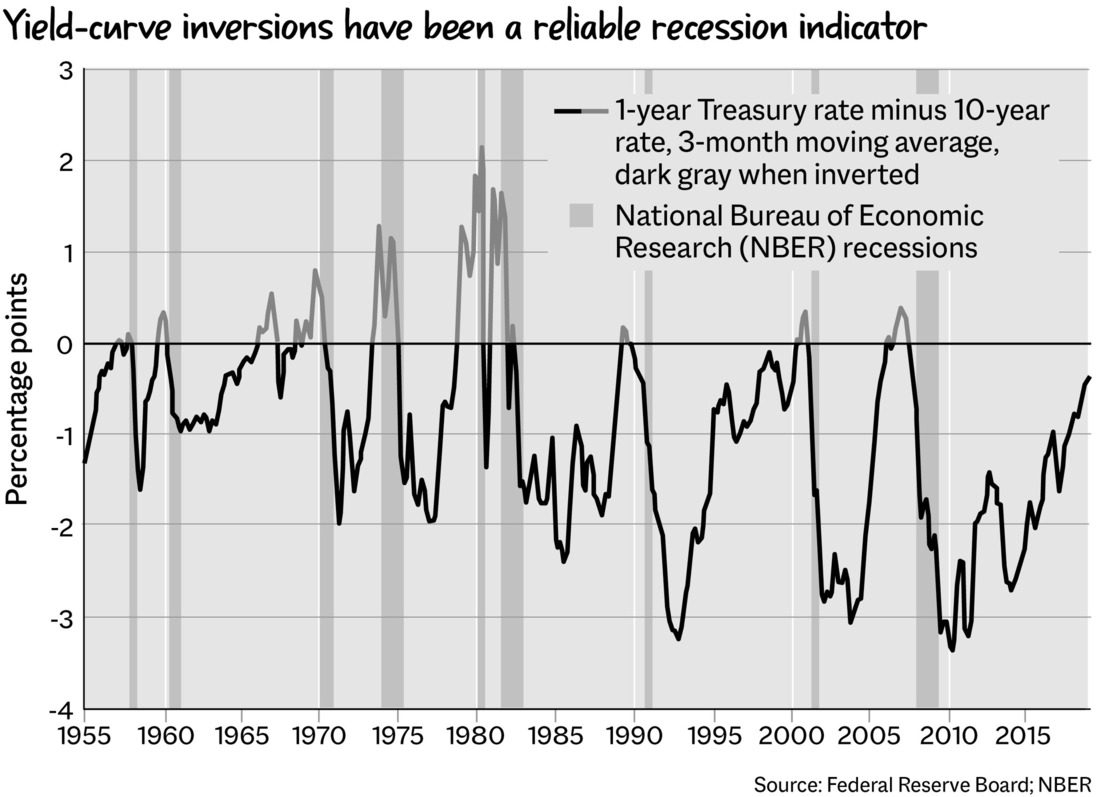

The crucial thing about all this is how people perceive and experience their circumstances. If we are in an economic slowdown, it doesn’t make it any better by defining it as a recession or not. The most important thing is how we move forward. The lens through which we view our world quantitatively is archaic. For example, the inverted yield curve is one way that markets will attempt to signal if we are in a recession. However, the yield curve is not always accurate and works only within a pretty small sample size.

The term recession is largely semantic. This might sound silly, but recession is a label more than anything else. It’s good to know when and why a recession happens, but when we are in one, we could call it a potatocession and it would still have the same impact. What really matters is wage growth, unemployment, opportunities, and so on.

In the words of the gaming expert known as Cheesemeister on Twitter, “Mario games teach us that even if something is essentially the same, psychologically it can be completely different. This example is very easy to understand.”

We live in a world where everything is not what we thought it was going to be (which I think is just life), so the differentials described above matter because they influence how we experience the world. You can be at the same height with a stack of blocks beneath you or just one block floating—it’s the same height, but a completely different way to get there.

The economy, despite its wide-ranging reach, is an incredibly personal experience. For example, 5 percent inflation can be the “same” for everyone but is actually completely different because 5 percent means a lot of different things to different people. If you read that inflation is at 9.1 percent but feel as though it’s more than 20 percent because of your experience of shortages at the grocery store and your rent going up $1,000, that creates pain. This can feel like a recession, but it isn’t. Technically.

What Does a Recession Look Like?

A recession could take place based on anything from a slowing down in the labor market, the Fed’s rate hikes hitting the economy in a big way, or any combination of business and consumer activity coming to a halt. If a recession did happen, a few things would take place:

-

Retail: Consumers usually cut back on discretionary spending during economic downturns, leading to reduced sales for retailers, impacting everything from grocery stores to furniture goods.

-

Restaurants: In recessions, people often cut back on dining out to save money. Fast-casual, like Panera Bread, and luxury dining establishments, like Salt Bae’s restaurant in Las Vegas, might be particularly vulnerable, though fast food sometimes proves more resilient.

-

Travel/Tourism: This industry is highly sensitive to economic downturns. Business travel can decline when companies look to cut costs, and leisure travel drops as households tighten their belts. The 2020–2021 period really highlighted the vulnerability of this sector to external shocks (like the covid-19 pandemic).

-

Leisure/Hospitality: This sector, closely related to travel and tourism, would likely see reduced revenues. Hotels, resorts, and other destinations would experience declines in bookings, and entertainment venues, like cinemas and theaters, might see fewer patrons as everyone tries to save money.

-

Service Purveyors: Professional services, especially those deemed non-essential, could see decreased demand. For instance, luxury services or elective medical procedures might see reductions.

-

Real Estate: Housing markets can be impacted in several ways during a recession:

-

Residential: Potential homebuyers might delay purchasing due to economic uncertainty, leading to a decline in sales and potentially in prices.

-

Commercial: As businesses contract or shut down, demand for office and retail spaces might decline (exacerbating the already strange state of commercial real estate due to people working from home).

-

Manufacturing/Warehouse: These sectors are closely tied to consumer demand. As people buy less, there’s less need to manufacture goods or store them in warehouses. Also, global disruptions can impact supply chains, affecting manufacturing operations.

-

Historic Recessions

There are real economic downturns that have lasting, devastating consequences. The recessions of 2008 and 2020–2021 are two such examples. Both downturns greatly impacted people’s lives and left lasting scars, but they were completely different from each other.

2008 Recession

The 2008 recession played out over many years. A slew of bad decisions compounded to create a massive tower of financial instability. The housing market boom was the best-known part of this. Lenders were like, “Oh, yeah, this is what I want. I am going to lend to anyone and everyone,” leading to a series of loans to people who were likely to be able to pay them back as well as loans to people who were unlikely to pay them back. The biggest problem in 2008 was that people expected home prices to go up forever. As Antoinette Schoar, an economist at the MIT Sloan School of Management, saw it:

The problem with the banks was less a misalignment of incentives or deliberate misselling of loans to people who couldn’t afford it, and more, if you want, stupidity. It was this belief that house prices could only go up, and so it didn’t matter whether the person who was buying a particular house might lose his or her job and default on their payments. The bank would be holding valuable collateral and everything would be fine.

The problem was the belief in “home prices go up forever”: optimism about the cyclical housing market on the part of the banks and people buying homes.

The mortgages were packaged into financial products known as mortgage-backed securities (MBSs). The securities were then sold to investors worldwide, who were like, “Let’s get some exposure to the very strong housing market in the United States and the American Dream! That’s always been a good and stable thing!”

It was not a good and stable thing! The housing market started to cool off, home prices began to decline, and everything began to fall apart. A lot of borrowers found themselves unable to repay their loans, leading to a bunch of foreclosures on homes across both prime and subprime mortgages. That was devastating, not only for the people who were being foreclosed on but also for the value of the mortgage-backed securities, which became essentially worthless.

To make things worse, a lot of the mortgage-backed securities were insured through credit default swaps, a type of financial instrument. By protecting investors from the risk of people defaulting on debt obligations, they were supposed to insure the investments against loss—so if they did become worthless, investors would still be okay. But because everything went so bad so quickly and so many people were affected, the insurance companies couldn’t meet all the claims.

Everyone freaked out. There was a credit crunch, when the banks were too spooked to lend money, which is necessary to boost business investment and consumer spending; that made it hard for the economy to function. A global recession ensued. No one could really do anything because the intricate, delicate financial system was cratering.

2020 Recession

The recession of 2020–2021 was a little bit different; it was due to a global pandemic. When covid-19 began to spread around the world, lockdowns followed, with social distancing put into place. No one could go anywhere. Global supply chains broke. Nothing could get anywhere. There were all sorts of shortages, from toilet paper to lumber. Prices skyrocketed for certain goods because nothing was where it needed to be. That all happened in a matter of weeks! The financial crisis of 2008 played out over months before it became severe, but the effects of the pandemic were immediate.

In April 2020, the price of oil went negative as oil demand plummeted due to the lockdowns (no one and nothing were going anywhere). There was a shortage of places to keep the oil, so oil producers were like, “Someone has to take this off our hands!,” and they ended up paying buyers to buy the product. It was a very weird supply-and-demand situation, and it highlighted the new world that the pandemic had catapulted us into. Financial assets sold off across the board, with all sorts of liquidity issues as people tried to figure out what was going on. E-commerce, healthcare, and technology all did great during that time, but airlines, travel, and energy were brutally beaten up due to uncertainty and fear.

The recovery after the 2008 recession was also different from the recovery after the 2020 recession. In 2008, the government created the Troubled Asset Relief Program (TARP), and in 2009, Congress passed the American Recovery and Reinvestment Act (ARRA), which helped stabilize the financial sector and stimulate the economy (at a cost). TARP was all about bailing out the banks and taking toxic assets off their balance sheets. But soon it was pouring money into banks and bailing out General Motors. People got pretty mad about that! The ARRA was meant to help create jobs and provide infrastructure spending to try to spur the economy in the right direction, but it was slow to work. And TARP was so big.

They were tactics of bailout capitalism and initiated much of the action we see today. There is a lot of support for businesses, and this makes sense! Businesses employ people, and people are the economy, so it makes sense to support people where they work. But businesses don’t always distribute the help.

If businesses become reliant on government interference, it creates all sorts of problems, such as zombie companies—companies that should die but don’t because there is always support for them!

Zombie Companies

Zombie companies, as defined by Ryan Niladri Banerjee and Boris Hofmann in their paper “The Rise of Zombie Firms: Causes and Consequences,” are firms that are “unable to cover debt servicing costs from current profits.” They don’t make enough money to be successful but remain afloat mostly through borrowing money and seeking government aid. Think of WeWork, which seemingly stays afloat out of sheer willpower, and GameStop, which subsists on meme fumes, Reddit posts, and rocket ship emoji.

But zooming out here, targeted government intervention can sometimes prevent systemic collapse (as we saw during March 2020), preserve jobs, and provide economic stability during times of crisis.

In 2020, trillions of stimulus dollars were injected into the economy, including direct payments, expanded unemployment, small-business loans, and more. People were mostly okay. They were not okay during 2008.

The pandemic was, of course, global. The rapid spread of covid-19 impacted every country on Earth, triggering a global recession and impacting businesses on all continents. India went through a severe downturn, with millions of workers losing their jobs. The United Kingdom experienced a notable decline in GDP. In Brazil, the already existing economic challenges of high unemployment rates and income inequality were exacerbated. Germany experienced a large contraction in industrial production and export volume. Every nation had to grapple with bankruptcies, layoffs, and supply chain disruptions. Governments and central banks had to step up quickly with giant stimulus packages and monetary intervention.

But the world emerged from the 2020–2021 recession rather rapidly due to governments and banks doing so much. In the United States, the recession officially ended in April 2021, according to the NBER overlords. But for the rest of 2021 and into 2022, we were flirting with a different kind of recession: a vibecession.

The Vibecession

A vibecession is a period of temporary vibe decline during which economic data such as trade and industrial activity are okay-ish. There is, of course, an element of reality to our existence: policy decisions, manufacturing output, gas prices, and other factors that cannot be modified by our feeble human minds (at least right now).

But those decisions do affect normal, everyday people who generate the vibes that do most of the work in determining how we feel. We take experience and evidence and shape our expectations, which warps our perception and acts as a forcing function for interpretation—and that is how you feel (in the most simplistic sense possible).

That feeds back into discourse and discussion, which also influences vibes and thus feelings. How you feel compounds into how everyone feels, and that is consumer sentiment. Of course, consumer sentiment is everything because consumer spending is such an important component of GDP growth.

Experience and evidence shape perceptions, which end up molding an interpretation of the future, which results in our collective reality, as discussed in the Vibe Economy chapter. Another hurdle that we are running into is language—we don’t have the words to describe what is going on, especially with the advent of digital technology.

We speak to one another using words that have evolved over and through time, so that we know what one is talking about when they reference a doorknob or a pencil. But there is currently a battle between words and concepts.

For example, the number of Americans that support “spending on the poor” is 71%, but if you call it “welfare” that number drops to 30% according to the National Opinion Research Center at the University of Chicago. There is no difference beyond that of words! Yet that makes all the difference. We have three different definitions of what it means to live “paycheck to paycheck” as reported by Matt Darling, senior employment policy analyst at the Niskanen Center, yet endless headlines proclaim that x percentage of people are living paycheck to paycheck.

There is a tension between definer and definition which also creates a phenomenon where the words we say no longer mean what we think they do, especially regarding the economy. No wonder the sentiment is off! No wonder people are confused! It’s hard to understand what’s happening, and that makes all of this so much harder.

I mean, just look at GDP and GDP headlines. It clearly doesn’t really capture happiness or whatever, but it does capture consumer spending. Is that the same thing? Is a growing economy happiness, numerically speaking?

And then the interpretation gets confusing.

What sort of data do we need to understand the economy better and how can we make that data as understandable as possible? And then, what would it look like when people do understand the economy? How can we help people make better decisions?

Of course, as I have talked about throughout the book, there are many real problems with the economy. We have a structural affordability crisis. A housing crisis. A healthcare crisis. A childcare crisis. The list is endless and nothing can hide anymore. The things to be anxious about are numerous. The geopolitical warfare. The walls of any sense of economic safety caving in. The endless political theatrics.

But we don’t even have the words to talk about it with one another.

The Benefits of Recessions

With all that being said, recessions suck. But there are also opportunities! A lot of companies actually experience growth during downturns—Amazon, Netflix, Walmart, McDonald’s, and others all grew during the 2008 financial crisis because of strategic business decisions:

-

Walmart (2008 financial crisis): As the world’s largest retailer, known for its low prices, Walmart benefited during the 2008 recession as consumers became more price-conscious. Walmart’s sales and earnings grew during this period.

-

Netflix (2008 financial crisis): As consumers cut back on more expensive entertainment options, such as going to movies or taking vacations, many turned to affordable at-home entertainment. Netflix saw subscriber growth and solid performance during the recession.

-

Amazon (2008 financial crisis): While many retailers suffered during the downturn, Amazon’s emphasis on low prices, convenience, and a broad selection helped it capture market share.

-

McDonald’s (2008 financial crisis): McDonald’s is often seen as a recession-resistant company because people turn to cheaper dining options during economic downturns. The fast-food giant posted strong sales during the 2008 recession.

-

General Mills (2008 financial crisis): People often eat at home more during recessions to save money. Companies that produce consumer staples, like General Mills with its cereal and other products, can and did see stable or increased sales.

-

Microsoft (2001 dot-com bubble burst): Despite the tech sector being hit hard by the dot-com bubble burst, Microsoft, with its diversified products and strong balance sheet, navigated the period effectively.

-

Dollar Tree & Dollar General (2008 financial crisis): Discount stores generally do well during recessions as consumers look for bargains. Both of these chains expanded and saw increased sales during the recession.

-

Procter & Gamble (various recessions): As a producer of consumer staples, such as laundry detergent, toothpaste, and toilet paper, P&G often maintains steady sales even in economic downturns.

-

Ross Stores & TJX Companies (2008 financial crisis): These discount apparel retailers saw strong sales and expanded their store count while other retailers struggled, because they are a discount option for apparel and other goods that people like buying (and people always really like buying goods!).

There is always opportunity, even in the scariest times. As Aristotle said, “It is during our darkest moments that we must focus to see the light.”

It’s human nature to want to assign blame, to identify a definitive, central cause behind a problem. It’s easier that way! Of course, it’s easy for me to say, “Ah, yes, many are at fault, therefore we must be kind in distributing the blame.” But that’s the reality of the strange era we live in. People often want validation of their feelings that things are bad, and this can lead to a sort of vibes-based recession (the aforementioned vibecession).

This is why the debate over what a recession is or is not can become just a matter of semantics. If people are feeling bad about their economic prospects, that’s a real data point. If people aren’t happy with the economy, we risk spiraling into some sort of vibes-based recession as a result of the vibes-based model influencing the vibes-based narrative that influences the vibes-based economy.

As former Secretary of Defense Donald Rumsfeld once said, “There are known knowns: these are things we know we know. We also know there are known unknowns: that is to say we know there are some things [we know] we do not know. But there are also unknown unknowns—the ones we don’t know we don’t know.”

No one really knows what is going on.

The only certainty is uncertainty, the only conviction is lack thereof, and the only path forward is blindfolded.

We may simply be consuming far too much information for our brains to process. We are not built to be bombarded by all of the news, all of the time. But we are, and the resulting overwhelm becomes the narrative.

The answers we have about the economy oftentimes just lead to more questions. And I think that inquiring tone at the end of a sentence as people ask what’s going on tells us more about the economy than any report ever will. The worry of a recession should not be discounted, especially considering how fast the economy can turn, given things like geopolitical conflict and global pandemics. There are also lagged effects. So if the Federal Reserve or the U.S. government does something, like raise rates or cut taxes, that impact will take time to show up.

However, Bloomberg Economics predicted a 100 percent chance of a recession by the end of 2022, and that never happened. But that doesn’t mean it never could happen…. And in general, the tension is thick (something I’ll get into in later chapters) and it rings of Toni Morrison’s words in The Source of Self-Regard:

Fascism talks ideology, but it is really just marketing—marketing for power. It is recognizable by its need to purge, by the strategies it uses to purge, and by its terror of truly democratic agendas. It is recognizable by its determination to convert all public services to private entrepreneurship, all nonprofit organizations to profit-making ones—so that the narrow but protective chasm between governance and business disappears. It changes citizens into taxpayers—so individuals become angry at even the notion of the public good. It changes neighbors into consumers—so the measure of our value as humans is not our humanity or our compassion or our generosity but what we own. It changes parenting into panicking—so that we vote against the interests of our own children; against their health care, their education, their safety from weapons. And in effecting these changes it produces the perfect capitalist, one who is willing to kill a human being for a product (a pair of sneakers, a jacket, a car) or kill generations for control of products (oil, drugs, fruit, gold).

There’s a scene in the movie Before Sunrise in which one of the characters says:

I believe if there’s any kind of God it wouldn’t be in any of us, not you or me but just this little space in between. If there’s any kind of magic in this world it must be in the attempt of understanding someone, sharing something. I know, it’s almost impossible to succeed, but who cares really? The answer must be in the attempt.

The answer must be in the attempt. We get so caught up in what happens at the end that we forget to simply exist. And maybe availability and optionality could both be solved if we were just more present in the moment. More reflective. More there for one another.

Of course, the thing we have to remember is that people are the economy. As we try to figure out how to integrate AI into our lives, manage wealth inequality, and try to maintain our labor market, we have to remember that people are everything.