Chapter 12

Bond Market

The Bond Market

The bond market and stock market are sort of similar; both are platforms for companies to raise money and allow people like you and me to participate in the process.

Bonds are a vast, complex network of financial instruments that form a cornerstone of modern finance, but outside Wall Street, they aren’t really talked about a lot! Bonds are the undercurrent of the rivers we all wade through, the backbone of the stock market, and the support system of most of the businesses we interact with every day.

Most people who want to buy a car, a house, or anything else that is big and expensive need to take out a loan. Companies, as well as governments and financial institutions, have to do the same if they want to finance a really big project. But rather than going to a bank, they go to the bond market.

What Are Bonds?

Bonds represent the debt of a company, government, or municipality. When you buy a bond, you are lending money to one of those entities for a certain amount of time so it can carry out various projects or finance certain activities, and in return it pays you interest over that time period. Bonds tend to have a lower risk than stocks because they have regular payments called coupon payments that they pay out to investors on a set schedule—and bond investors are paid before shareholders if the company ends up going under.

The bond market facilitates the flow of money between entities that need it (borrowers) and those that have it (lenders). For example, Kansas City, Missouri, approved an $800 million infrastructure repair program, financed by General Obligation bonds. The goal was to repair streets, bridges, sidewalks, and more as part of their GO KC Program. It would normally enlist a broker/dealer to help sell these bonds to investors such as mutual funds. Bonds have a lot of complex components.

Bonds Between Friends

For now, think of it as being like borrowing $10,000 from a friend. “I’ll pay you back in two years,” you promise them; they become the lender and you the borrower. To make sure they know that you’re not going to dip out before paying them, you tell them that you’ll pay an annual interest rate of 1% with semiannual payments: $100 a year, paying $50 twice a year. The yield (the return generated by the investment over a period of time) on the bond is 1%; because the bond isn’t trading on the open market, the market value and the face value are the same. This is a simplified example—and bonds are different from regular loans. Bonds are issued by governments, municipalities, and corporations (not by regular people) and are often traded on markets (loans usually aren’t, unless they are packed into the MBSs or CDOs I talked about before).

This underground bond sale that you and your friend are entering into has a few components:

-

Maturity date. This is the two-year time frame that the two of you entered into, the time in which the face value, or total value of the bond ($10,000) will be repaid.

-

Coupon rate. This is the 1% interest that you’re paying annually. This is usually a fixed percentage of the face value of the bond, which is $100, or $50 twice a year.

-

Number of periods. You entered into a two-year agreement by which you’re going to be paying your friend four times (semiannually ends up being four payments over two years), so this is four.

-

Yield to maturity. The future value of coupon payments is discounted via this rate—the rate of return investors would get if they reinvested every coupon payment from the bond at a fixed interest rate until the bond matures, which is quite a chore to calculate. To simplify, we can just assume that it is 2%.

This is where things get mathy, but that’s okay!

First, let’s calculate the present value of the semiannual payments:

50/(1.01)1 + 50/(1.01)2 + 50/(1.01)3 + 50/(1.01)4 = $195.09

Now we’ll calculate the present face value of the bond:

10,000/(1.01)4 = $9,609.80

Added together, we get the total value of the bond = $9,804.89.

So if you want to trade your bond on the market (or if your friend wants to trade it on the market after they buy it), this is what it would trade for. We calculated the present value of the bond’s expected value based on the coupon payments you promised your friend for sticking around.

Stocks are valued in sort of the same way—the net present value of future cash flows—but bonds return interest payments, plus the loan principal when the bond finally reaches maturity, so the valuation model for bonds and stocks is actually quite different.

There are two more important things to know about bonds:

-

Bond prices and interest rates are inversely correlated. That means when interest rates go up, bond prices go down, because they usually were issued with a lower rate. So if you have a bond paying 2% and then interest rates tick up and all the new bonds are paying 3%, your bond is going to fall in value because people are like, “There is no way I am paying a lot to take on that lower yield!” It’s the opposite when interest rates decrease. If rates fall and all the new bonds are paying 1%, your 2% bond is going to look superhot, leading to it trading at a premium because everyone is like, “Please give me the yield.”

-

Duration determines bond movements in relationship to outside factors. Duration is how a bond’s price sensitivity to a 1% change in interest rates is measured. When you have a longer-term bond, like thirty years, it’s going to be pretty sensitive to changes in interest rates because it has to exist for such a long time, with a lot of future cash flows. A shorter-term bond has less exposure to interest rate fluctuations because it isn’t around as long.

Of course, as when anyone owes anyone else money, there is risk! The risk here is that bondholders might not be able to make their payments to you; this is known as the default risk.

A bond rating is the measure of the creditworthiness of a corporation, organization, or institution based on its profitability and the stability of various projects it is working on.

Bond Ratings

Starbucks, for example, has a rating of BBB+ from Standard & Poor’s (one of the two main ratings agencies) and a rating of Baa1 from Moody’s (the second main rating agency), which is an assessment of Starbucks’ credit risk and ability to pay back the bond. Both of those ratings are low investment grade, meaning the agencies think that Starbucks can pay its loans back perfectly fine and isn’t at too high a risk of default but may be susceptible to adverse economic conditions or changes in the business environment.

Companies with a higher credit rating (usually those that are better able to repay their debts) are going to have a tighter spread than companies with lower credit ratings. There are other things that influence credit ratings, including the amount of collateral a bond issuer puts up. Bond issuers love when they can possess collateral in the case of default—so if a borrower can put up an asset to make sure everyone is feeling good, that helps a lot.

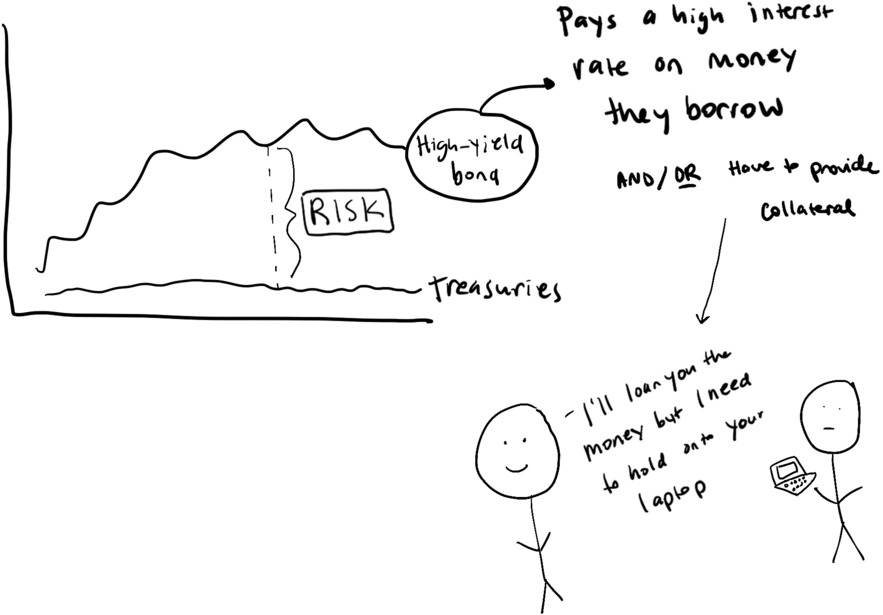

AAA bonds have the most immaculate vibe, are “investment grade,” and pose the lowest risk to investors. “High-yield” bonds (those rated BB and below) are riskier, but they also (usually) pay higher rates of return because of that risk.

High-Yield Friend

Let’s say you have a friend who is a bit loose with their budget. They’re constantly asking you to loan them a little money, and they don’t always come through on their promise to pay it back. So you wise up and become more hesitant to lend them money—maybe even charge them interest on the money they still need to repay you. They are risky relative to your other friends. The friend spread is wide.

That same story plays out in the bond market!

If the spread is wide—meaning that the company is wildly risky relative to government securities—lenders will begin to demand higher interest rates.

If your friend said, “Hey, I need to borrow a hundred dollars, and I will give you my laptop as collateral,” that’s even better. You might even charge them a lower interest rate because if they don’t repay you, you get to keep the laptop.

What Is a Spread?

Treasury Bills, Notes, and Bonds

U.S. government bonds are usually considered to be risk free, because historically, and in an ideal future world, the U.S. government is very unlikely to default on its debt. One of the most critical ingredients of asset prices is the price of safety, or the assurance of risk-free investments, which is represented by the yield on risk-free assets such as three-month Treasury bills, which are assumed to have very little (if any) default risk. You might say, “The U.S. government seems pretty risky to me!” Risk is relative. The term risk free implies three main things:

-

SAFE: The U.S. government is unlikely to default on its debts.

-

LIQUID: The Treasury market is liquid, meaning that there are usually a lot of willing buyers of government debt: foreign governments, investors, and others.

-

STABLE: The short term minimizes rate movements, meaning that over the short term (say, three months), rates aren’t going to bounce around too much.

The risk-free rate is crucial because it’s used to value all other assets, including stocks, bonds, and the rates people pay on their mortgages. For example, an increase in the risk-free rate puts pressure on stock valuations because it raises the discount rate I talked about earlier, which bites into the expected market return because future cash flows will be worth less. The term risk-free rate in the bond world is somewhat like the North Star of the finance world. When the risk-free rate moves, it’s like a domino effect: Everything from stock prices to corporate bonds and even your neighbor’s mortgage rate feels the impact. It’s a baseline that tells investors what they can expect to earn without taking on excess risk.

Treasury Market

So Treasuries are meant to be the safest asset in the world. These are the underlying forces powering the global market ecosystem because they are the bonds that the U.S. government sells in order to raise money and finance its activities. There are three types of Treasuries:

-

Treasury bills. These range in maturity from one month to one year.

-

Treasury notes. These have two-, three-, five-, seven-, and ten-year maturities.

-

Treasury bonds. These mature in twenty to thirty years.

Treasury yields, particularly the ten-year yield, are seen as a useful indicator of how people are feeling about the economy. The relationship between Treasury yields and investor sentiment is complex—but higher yields on long-term Treasuries can sometimes be associated with positive investor sentiment and optimism regarding economic expansion and increased business profitability.

What is really important is how yields relate to one another across something called the yield curve, the relationship between bond yields and maturity dates.

-

The yield curve should generally be upward sloping; you should be compensated more for holding thirty-year bonds than ten-year bonds because there is more uncertainty (and hopefully economic growth) on the thirty-year horizon.

-

However, sometimes the yield curve flattens. This means that investors in the bond market don’t see a lot of economic opportunity over that timeline; essentially, they feel, the market in ten years will be relatively the same as the market in thirty years.

-

Also, sometimes the yield curve inverts. This is bad. This means that the bond market is not happy—investors don’t expect economic growth in the future. An inverted yield curve normally signals a recession.

But as economists at the Federal Reserve wrote, “It is not valid to interpret inverted term spreads as independent measures of impending recession. They largely reflect the expectations of market participants.” (Author’s emphasis.)

What the heck, right? Expectations manifest reality! And before you ask, “Isn’t this book about economics, not astrology?,” let’s just say that economics and astrology have more in common than not.

The basic takeaway is that the yield curve reflects economic vibes. When it inverts, vibes are bad. When it’s upward sloping, vibes are good. But sometimes the vibes are confusing. Inversion of the yield curve does not always mean that a recession will follow; it just means that things are not looking hot.

The inverted yield curve has preceded recessions in the past, but it isn’t a foolproof oracle of what is to come; nothing can be. We must understand why things go up, because that will tell us why other things go down. Treasuries are the foundation our economy rests on. Most countries hold them, most investors hold them, and they’re the support beams of the entire U.S. economy.

So in the world of government bonds, U.S. Treasuries are often the poster child for stability and low risk. Each country usually issues their own sovereign bonds, with a different profile of risk and return. Some, like German Bunds or U.K. Gilts, are pretty stable. Others, from countries with less stable economies, like Argentina or Zambia, are much riskier. Just like U.S. Treasuries, these sovereign bonds are a reflection of a country’s economic health and a good gauge of global financial currents.

Markets as Vibe Reflectors

In his book Reminiscences of a Stock Operator, a lightly fictionalized account of Jesse Livermore, a legendary trader in the late 1800s who knew the game of market psychology and emotions all too well, Edwin Lefèvre wrote:

Nowhere does history indulge in repetitions so often or so uniformly as in Wall Street. When you read contemporary accounts of booms or panics the one thing that strikes you most forcibly is how little either stock speculation or stock speculators to-day differ from yesterday. The game does not change and neither does human nature.

Livermore was incredibly good at predicting market movements and trends, shorting the market (betting that it would go down) before the 1906 San Francisco earthquake and the 1929 Wall Street crash. There’s a list of investing rules published by Martin Zweig, another incredible investor and analyst, that echoes Livermore’s credo, “There is nothing new on Wall Street.”

Shearson Hutton

Shearson Lehman Taxable Fixed Income

Technical Analysis

The Market Technician’s Association

Monthly Meeting 4/11/90

Marty Zweig’s Investing Rules

-

The trend is your friend, don’t fight the tape.

-

Let profits run, take losses quickly.

-

If you buy for a reason, and that reason is discounted or is no longer valid, then sell!

-

If the values don’t make sense, then don’t participate. (2+2=4)

-

The cheap get cheaper, the dear get dearer.

-

Don’t fight the FED (less valid than #1).

-

Every indicator eventually bites the dust.

-

Adapt to change.

-

Don’t let your opinion of what should happen, bias your trading strategy.

-

Don’t blame your mistakes on the market.

-

Don’t play all the time.

-

The market is not efficient, but is still tough to beat.

-

You’ll never know all the answers.

-

If you can’t sleep at night, reduce your positions or get out.

-

Don’t put too much faith in the “experts.”

-

Don’t focus too much on short term information flows.

-

Beware “New Era” thinking, i.e., it’s different this time because…

All seventeen rules are based on managing emotions. That’s been the schtick of this whole book, right? Vibes and feelings are much more important to how the economy (and stock market) functions than we give them credit for. The reason we tend to ignore the emotional aspects of these things is that they sound sort of silly. They make it difficult to plan policy. And of course, as Morgan Stanley wrote in an investor letter in 2023, “Price has driven narrative for generations…. Strong US growth, persistent EU inflation & a disappointing China reopening are all recent narratives supported by prices. But for all 3, the fundamentals look more complicated and face key near-term tests.”

Price drives narrative. So parts of how we interact with the economy and markets are emotion, influenced by price, but it’s very much which came first—the chicken or the egg? The price or the story?

Wasteland Capital, a popular Twitter account, tweeted in November 2022, “It’s fascinating that finance professionals can look at exactly the same product, financials, data set, management team, facts and events, and draw completely opposite and entirely conflicting conclusions.” The stock market is bizarre, because, as Wasteland Capital pointed out, no one really agrees with what is going down at any given point. The industry is based on making money off people disagreeing on what will happen and why.

There is a lot of speculation in markets. They haven’t done what they need to do. As Martin Sandbu, the Financial Times’ European economics commentator, wrote in July 2022:

Yet these past 20 years have been the era of lower-than-ever financing costs, first because of market exuberance, then thanks to central banks’ ultra-lax monetary policy. And what do we have to show for all that cheap credit? Two lost decades for investment…. I think our failure to invest is profoundly political…. That is true in good times, when transfer payments, tax cuts and immediate public goods are all politically more attractive than capital investment. (Something equivalent is at work in the private sector: witness companies’ choice to return cash to owners through share buybacks rather than invest in their own growth.) It has also been true in bad times, when investment is the easiest expenditure for belt-tightening governments and companies to cut.

Society at large has gotten a bit lazy. We have sacrificed tomorrow for today, and the markets are a prime example of that. Sandbu highlighted companies that are conducting share buybacks, or buying shares to boost their stock price, rather than saying, “Maybe we should invest in our company for longer-term growth.” That isn’t great.

Market blowups, such as the 2008 financial crisis and the dot-com bubble, occur when people forget that they actually exist in reality, with real-world constraints that need risk management, and money becomes a religion of sorts. We get caught up in the game, and the game becomes us. We become defined by the money we make—the gains. When losses come, so does the loss of faith.

Markets are a pressure cooker, too. In 2023, a writer at Bloomberg published an article titled “Corporate America’s Earnings Quality Is the Worst in Three Decades,” which basically took the stance that corporate America was engaging in a little bit of accounting embellishment to make the numbers look better than they are. As Gregg Fisher, the founder of Quent Capital, said in the article, “The pressure on these leadership teams is intense. If you’re getting ready to release your earnings and you can move a penny around somewhere from left to right, it just might tell a better story that as long as it’s legal, they do it.”

Part of the market dance is that hedge fund assets have gone parabolic, part of the dance is trying to appeal to markets, part of the dance is just to stay alive as a company—it’s all a very delicate balance.

We repeatedly learn the same lessons regarding markets, risk taking, and making educated decisions relative to what has happened historically, but it seems that each time we must process the knowledge differently. Things sort of change, but there is always the same underlying problem of exuberance or zero risk management, and because markets are based in human nature, we repeat the same errors over and over again.