Chapter 10

The Housing Market

The American Dream

The American Dream, as defined by James Truslow Adams, is “the dream of a land in which life should be better and richer and fuller for everyone, with opportunity for each according to ability or achievement.” It’s no secret that the American Dream (at least the way Adams saw it) is no longer what it used to be.

A lot of younger people think that we need a total market reset so they can get access to a home—otherwise, that dream (or, let’s be real, any shred of stability) will never be theirs. Jerome Powell, the chair of the Federal Reserve during the 2020s housing bubble, even said that a housing market recalibration of sorts was necessary! A few things are going on with the housing market, including soaring home prices, a lack of housing in major cities, and private equity snapping up homes, leading to a housing crisis and, subsequently, a crisis for the American Dream.

The Housing Cycle Is the Business Cycle

Currently, a house costs 4.5 times the median family income, whereas, historically, it was 3 to 3.5 times the median family income. Housing has now become unaffordable.

This is a supply and zoning issue. Edward Leamer, an economist at NBER, argued in his brilliant paper titled “Housing Is the Business Cycle,” “Housing is the most important sector in our economic recessions and any attempt to control the business cycle needs to focus especially on residential investment.” Weakness in housing sales is a core indicator of a recession, mostly because the world is driven by consumers, who are directly impacted by the cost of housing! As Leamer wrote, “it’s a consumer cycle, not a business cycle.” Residential investment (expenditure on constructing, renovating, or purchasing residential properties such as homes and apartment buildings), a key part of GDP, is important because people are important. But we forget that the world is made up of people and that capital appreciation (the increase in the value of something over time) isn’t the core point of everything, ever.

How to Buy a House

There are two ways to buy a home:

-

Put down all cash. (In July 2022, nearly one-third of all home purchases were made in cash up front.)

-

Finance the home through a mortgage.

If you finance a home, the total cost of the home is a function of the price you pay for it plus the mortgage that you have to pay off.

A mortgage is a loan specifically for buying real estate, requiring some cash up front (usually about 20 percent of the home price), known as a down payment. The rest of the house is covered by a mortgage payment. A mortgage allows you to borrow the money necessary to buy the house, and you repay it over time with interest, usually through monthly installments.

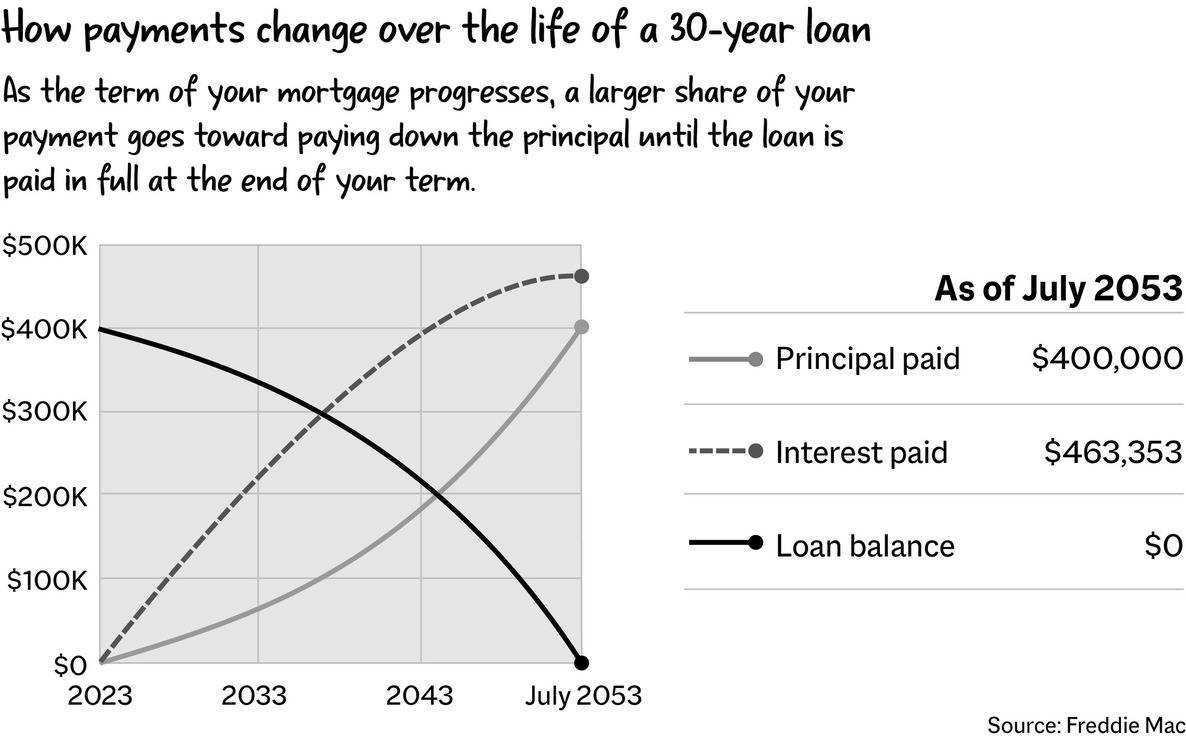

In the United States, most mortgages are thirty-year fixed-rate mortgages, so if you’re able to lock in a low interest rate, the payments won’t be that bad. But if mortgage rates skyrocket, it can make it impossible to finance a home.

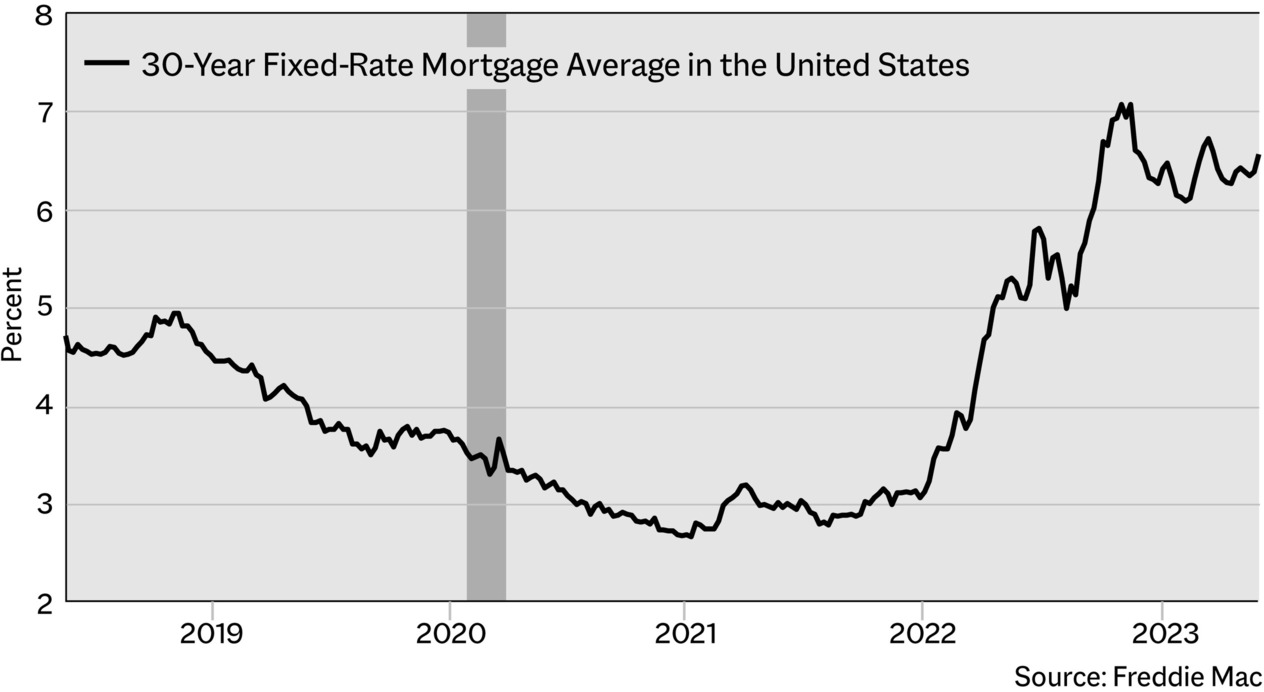

Mortgage Rates Over the Past Two Years

Mortgage rates were really low for a long time, which enabled a lot of people to enter the housing market. But then the Federal Reserve started hiking rates to fight inflation.

Rates bottomed out around 2.5% in 2021 and then shot up to over 8 percent in 2023—a huge and painful move. Mortgage rates wield significant power, pricing some prospective home buyers who would have previously been allowed in out of the market. That also gave all-cash buyers, who are usually older and already have accumulated wealth, an advantage.

In 2020, the thirty-year mortgage rate was 2.87% and the average new home price was $405,000. By 2022, the thirty-year mortgage rate had risen to 6% and the average new home price was $547,000. That resulted in a $28,000 increase in the necessary down payment, assuming that a prospective buyer put 20 percent down, and a 96 percent increase in average monthly payments from $1,343 to $2,628—and this comparison doesn’t include property taxes, insurance, utilities, and home repairs!

Over two years, monthly payments increased by almost $1,000 for a thirty-year fixed-rate mortgage. Eighteen million people were knocked out of the housing market because affordability disappeared so quickly.

Those who were able to get in won the game. Nearly two-thirds of outstanding mortgages in the United States have an origination interest rate of 4% or less—and 39 percent of homeowners have no mortgage, equating to roughly 32 million people (mostly boomers) who are free and clear.

This creates issues across the board.

As interest rates have gone up, fewer people have wanted to invest in mortgage-backed securities, because the risk of defaulting (being unable to pay) on real estate loans has also gone up—not an attractive proposition. The effect? Mortgage providers are charging higher interest rates!

The flip side of 18 million people unable to afford owning a home is that they have to rent, which pushes rental prices up. Compound that with Millennials forgoing homeownership, and the demand can easily outpace the available supply of rental spaces—exacerbating the housing crisis more.

Well, Why Don’t We Have Enough Homes?

So, yes, we do not have enough housing. For a few reasons (note: this list is not exhaustive):

-

Regulation: Zoning policies and obstructions to construction put into place by state and local governments make it much more difficult to build homes.

-

Types of homes: One in twenty new homes are now built for the purpose of rental living rather than homeownership (it was closer to one in fifty during the early 2000s). According to research by CoreLogic, the percentage of new single-family homes less than 1,400 square feet dropped from 70 percent of builds in the 1940s to less than 10 percent in 2020, so if you want to buy a starter home, tough luck. Sales of houses priced under $300,000 have fallen substantially since 2010, when they made up 70 percent of sales, to less than 10 percent in 2022.

-

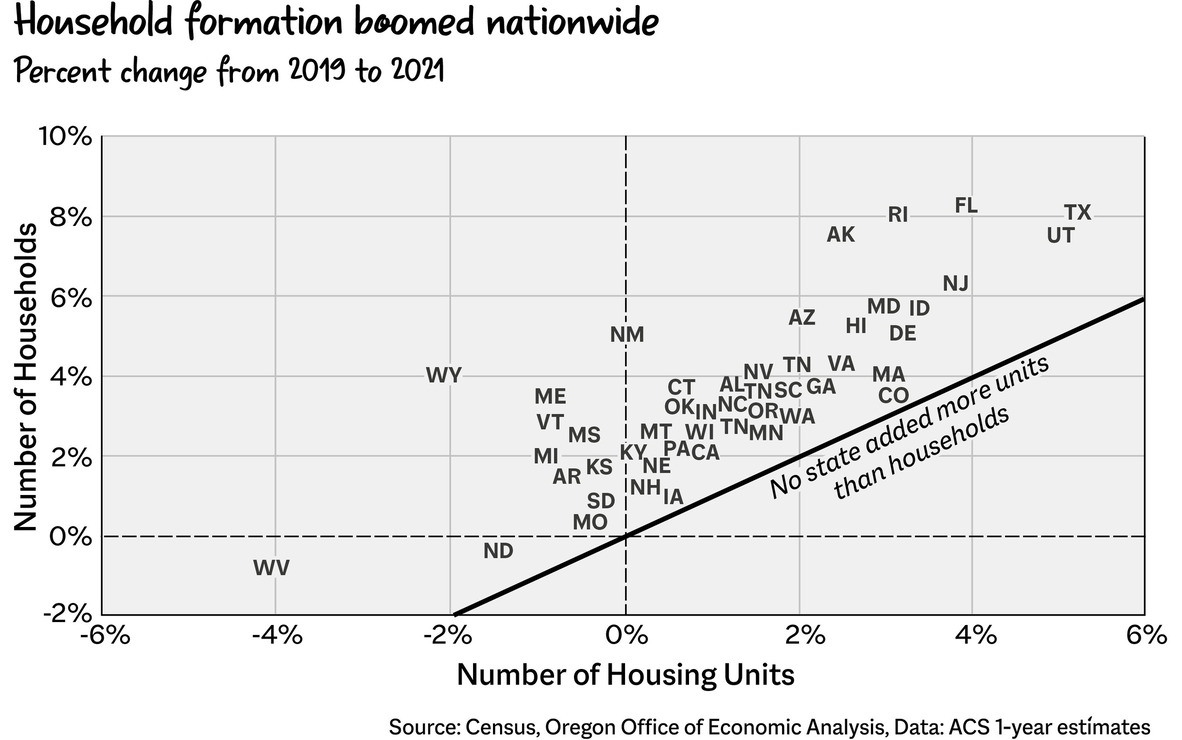

Supply chains: During the early 2020s, there were also significant issues in supply chains and labor resources, with many homes sitting idly, waiting to be finished. Paint, coating, and adhesives were in short supply due to overseas production challenges (globalization!), making building and decorating homes incredibly difficult. During the pandemic, not a single state added more housing units than new households, as reported by the American Community Survey.

-

Money: Investors, mostly private equity firms, buy up a significant amount of real estate; according to ProPublica, they accounted for 85 percent of the biggest apartment deals by the Federal Home Loan Mortgage Corporation, also known as Freddie Mac, over the past decade. Investors have bought more than one in every ten homes sold over the past decade—twice the number before the 2008 housing crash. Capital allocators (the private equity firms and other institutions that are buying up real estate) decide how homes are built and who they are sold to, both metaphorically and literally.

-

Zillowification: Companies such as Opendoor and Zillow were pioneers of home flipping during the housing boom of the early 2020s, but when mortgage rates skyrocketed, they lost a lot of money (up to $175 million, according to Opendoor).

-

Airbnb: Over half of Airbnb’s current listings have been added since 2020, further limiting the housing supply via short-term rentals.

-

Pandemic overhang: Much of the surge in home prices is attributed to the work-from-home era of covid-19, which accounted for more than 60 percent of the overall increase in house prices from November 2019 to November 2021, according to research by the Federal Reserve Bank of San Francisco.

So it becomes a vicious cycle that ultimately circles back to the fact that we need more housing—and the United States is not the only country struggling with this.

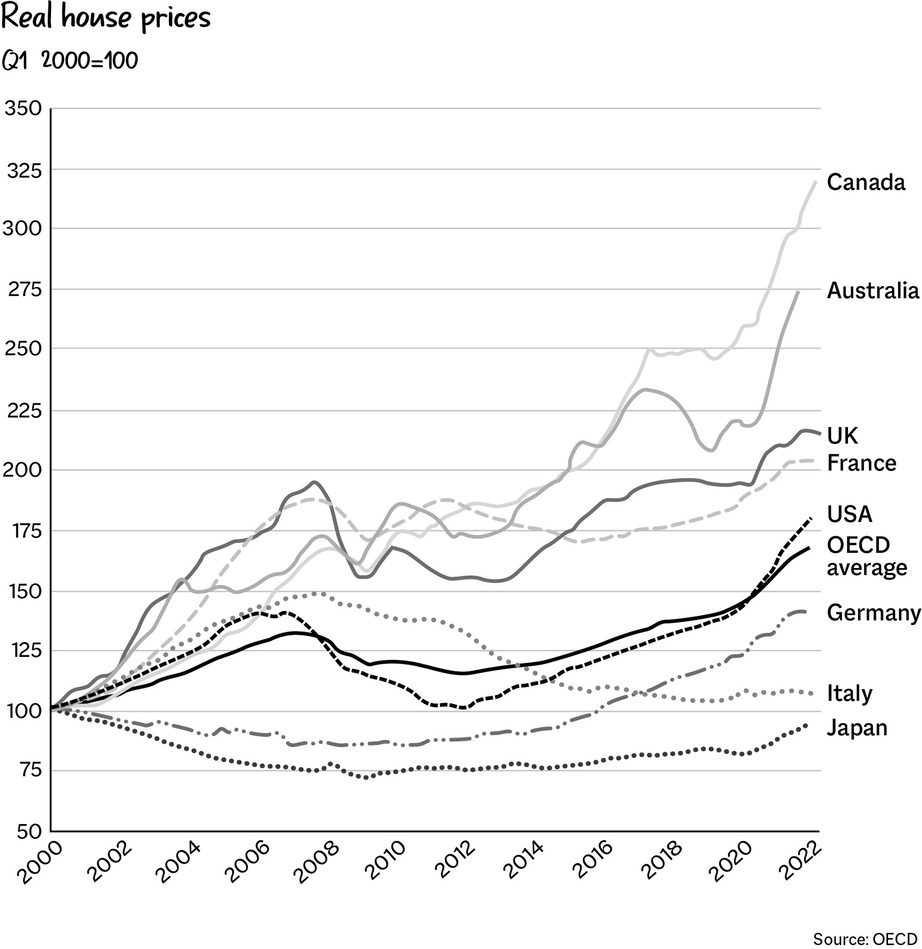

Housing in Other Countries

The crisis is actually worse in other developed nations for several reasons. The most common form of mortgage in the United States is now a thirty-year fixed-rate mortgage, but in the United Kingdom, variable-rate mortgages are often available—meaning that if the Bank of England raises interest rates, a buyer’s monthly mortgage payments will increase!

In Australia, housing affordability is a big challenge due to zoning laws, land release, planning regulations, and other factors. These problems also exist in other nations. The perfect storm of climbing interest rates and expensive housing, exploding demand, and not enough housing is reverberating across the global economy.

Canada is in a league all its own. Its banks issue variable-rate mortgages. This differs from those in the United Kingdom in that U.K. banks provide more flexibility in prepayment options, while Canadian banks impose stricter penalties and Canadian borrowers have more options for longer-term fixed-rate mortgages. This means that borrowers’ mortgage payments vary as the Bank of Canada raises or lowers rates, unlike payments on the United States’ typical thirty-year fixed-rate mortgage—with fixed being the key word here.

Fixing the Problem

We see home equity as the way to a comfortable middle-class life. That’s problematic! People shouldn’t have to become real estate speculators in order to live a comfortable life. The Argentinian economics blogger Maia Mindel has written extensively about how housing is an investment opportunity—and the perceived catastrophe of home prices going down in developed nations: “By allowing the already rich to prevent the value of their [housing] investments from ever going down, the developed world has sleepwalked into an unenviable situation: one of stratified incomes, reduced opportunities, and worse outcomes for everyone.”

Using a home as an investment vehicle isn’t great, because it creates a vampiric housing market built on value extraction. When it gets bubbly, it gets inflationary, too. According to a report from the Federal Reserve, home price gains in the early 2020s created $9 trillion in wealth, and could have driven roughly a third of the increase in inflation during the 2020–2022 time frame.

Making sure that everyone has a place to live should be a high priority across all countries. If more people have a place to live, the economic wheels will turn more smoothly, the economy will run better, and we will have less fear and worry haunting our everyday actions.

Of course, some people will mutter, “But the world is unfair. How can you say everyone should have a place to live?” Of course the world is unfair, but that doesn’t mean we shouldn’t try to make it better. As Barbara Alice Mann of the University of Toledo wrote, “Westerners are fond of the saying ‘Life isn’t fair.’ Then, they end in snide triumph: ‘So get used to it!’ What a cruel, sadistic notion to revel in!”

Fairness is subjective, and the balance of equality and equity is a delicate dance. But in regard to housing, supply has always been the problem. The core fact of the housing issue is that we need more of it, but there needs to be an evolution of regulations in order to make that happen.

So to solve the housing crisis, we need to do a few things.

Zoning laws need a serious revamp, allowing more mixed-use spaces combining residential areas with commercial and light industrial areas. It’s time to transform these areas from single-purpose zones into dynamic, multifunctional spaces. Streamlining the building permit process so it’s more transparent can make the journey from plan to reality smoother and accelerate the pace of building homes.

More prefab homes—they’re the fast track to building more homes quickly and efficiently, blending modern aesthetics with practicality. Moreover, various cities are enacting policies to help expand their housing supply. For example, South Bend, Indiana, offers preapproved house plans that can easily be built to produce more supply and support neighborhood infill. This is great!

How Do Monthly Payments Work?

Cities are peppered with underutilized spaces—let’s transform these into vibrant residential areas. Offering incentives for infill development can turn these urban voids into thriving communities.

Finally, green building practices are the need of the hour. Encouraging developers to adopt sustainable methods can lead to homes that are kind to both the environment and the economy. It’s not just a “green trend” but a necessary evolution in the way we think about and construct our living spaces, ensuring that they are in harmony with our environment—ecological responsibility and economic sensibility go hand in hand.

By weaving together these strategies, we can craft a future where housing is not just a commodity but a right accessible to all. It’s about creating spaces that are more than just shelters—they’re sustainable, affordable, and integral parts of vibrant communities. The goal is clear: to not only build more homes, but to build them smarter, more sustainably, and with a vision for the future. Let’s make the dream of affordable, sustainable housing a reality for everyone.