Chapter 7

Commodities

Commodities are the raw materials that create the building blocks of our economy. They are the common denominator of everything we interact with. On the surface, they may seem incredibly simple—of course, it seems like oil will always come out of the ground and copper will always be mined (until it runs out). These are commodities! They are the foundations of life.

Globalization and Commodities

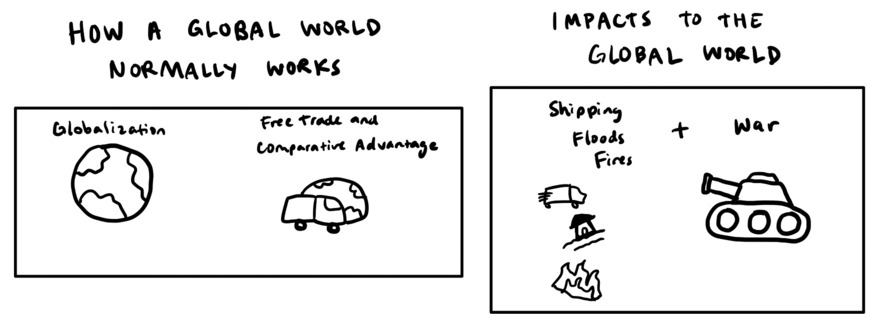

Globalization is a core component of how our world works, and it has arguably helped create the standard of living we have today. A lot of countries rely on imports for the majority of their consumption, and that isn’t a bad thing! Comparative advantage allows countries that are theoretically “better” at producing certain goods and commodities to produce them and, theoretically, the utilization of resources should be more effective across the board. For instance, warm and humid Mexico is much better at growing oranges than cold Canada is—so Mexico, based on its climate, should have a comparative advantage in orange production.

However, wars, pandemics, and natural disasters such as floods and wildfires can massively disrupt global supply chains, destabilizing industries and even entire economies. Recently, the supply of wheat, fertilizer, oils, and other products from major producers such as Russia and Ukraine basically disappeared due to the war, reverberating down the entire supply chain.

Other downsides of globalization are well established: Greater benefits are reaped by multinational corporations and the extremely wealthy than the general population; the environmental impact from the emissions generated by the planes, trains, and trucks transporting goods around the world; and increased interdependency among countries that have begun to rely more and more on one another in an era of increasing geopolitical instability.

External Factors and Commodities

These effects are compounded by the fact that most products we buy require inputs from other products—that are often imported—to manufacture them. Natural gas and potash go into fertilizer, fertilizer goes into crops, and so on. Grain represents the number one cost of feeding cattle, so when grain prices increase, the cost of cattle and therefore meat is going to increase, too. If one of the commodity dominoes tips, the entire line begins to topple.

A good example of this was what happened to Pakistan during the start of the European energy crisis in 2022. As Bloomberg reported, Pakistan State Oil Company wasn’t able to buy diesel fuel from Kuwait Petroleum Corporation because at that time “product [was] moving toward the west.” Pakistan wanted to buy, but the European countries captured the available supply because they could pay a premium over what Pakistan was willing to pay. This kind of situation has a lot of ramifications—specifically, exacerbating inequality between the developed and developing worlds and making it so those who can pay more might be the only ones who can stay alive. It’s a “those who pay can play” situation.

Commodity crises are a great reminder to pay attention. This stuff feels so simple, so easy, but when it’s gone, a process that will only be accelerated by climate change, the fallout is calamitous.

Common Commodities

Agricultural Products

Energy

Indices

Metals

Oil

For better or worse, oil is a crucial commodity, and its markets are some of the most closely watched in the world. The price of crude oil is a broad indicator of the entire economy’s health, impacting everything from the cost of transportation to what we pay for the petroleum-based plastic food containers at the grocery store.

Oil prices are volatile because of geopolitical realities. Recently, Saudi Arabia and Russia have drawn closer together, which could elevate oil prices more in coming years as the two countries work in cahoots. The two countries set oil production levels together—as the top two oil exporting countries in 2023—and this decided supply of oil is what determines the price of oil. However, oil supply is tenuous. Shale oil producers and OPEC underinvested in production for many years, making it more difficult to produce oil, thereby making it more expensive.

Gas Prices

Gasoline prices are a direct way that consumers feel the impact of changing oil prices, particularly in the United States. While one might expect that oil and gasoline prices have a linear relationship, they do not! When oil prices increase, gasoline prices increase, too; but when oil prices decrease, gasoline prices…don’t. Which is cute!

A research paper titled “Do Gasoline Prices Respond Asymmetrically to Crude Oil Price Changes?” made a key observation:

-

When crude oil prices increase by a certain amount, the corresponding increase in gasoline prices at the pump tends to be even greater, costing consumers more than the increase in crude oil prices.

-

On the other hand, when crude oil prices decrease, the corresponding decrease in gasoline prices at the pump tends to be smaller, saving consumers less than the decrease in crude oil prices!

In other words, the relationship between crude oil price changes and gasoline price changes is not equal in both directions. This phenomenon is known as asymmetric price transmission or “rocket and feathers.”

-

When oil prices increase, gas prices go up, too—like a rocket shooting into outer space!

-

But when oil prices fall, gasoline prices also fall—but at a slower rate. Like a gracefully falling feather, weaving its way across the sky.

This is why gas prices can stay high, even as oil prices drop.

This asymmetry in price changes is annoying and means that regardless of the volatility and variability of oil prices, they will have a negative impact on people’s wallets. Even though consumers might benefit when crude oil prices decline, they do not fully reap the savings that might be expected based on the magnitude of the drop in crude oil costs.

Variability is bad! And that’s what we have had a lot of as a world during the past few years.

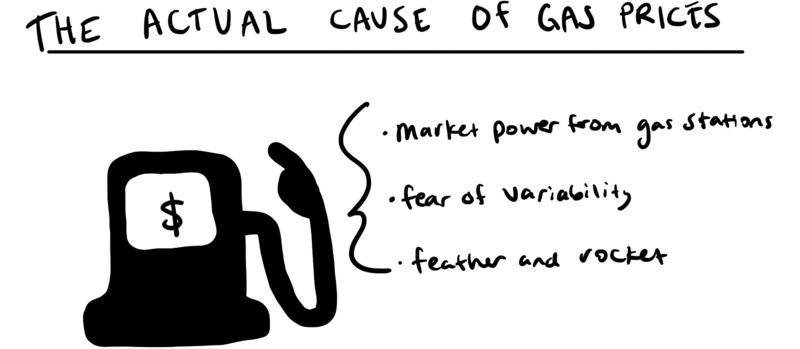

The rocket-and-feather world of gas prices is determined by a combination of:

-

The market power of gas stations. Gasoline is what’s called an inelastic good; most of us have to buy it even if the price goes up. Refiners acquire crude oil and turn it into fuel, and then it’s sent to service stations and distribution facilities, which all costs money.

-

Fear of price variability. If oil prices go up again, gas stations don’t want to be caught on the wrong foot. It’s much easier to keep gasoline prices high to hedge against that.

The problem is that gasoline prices are a political hot potato in the United States. If they are high, people are not happy with their politicians. Thus, a lot of “friendships” (trade partnerships) are forged by the price of gas. The energy trade is sort of the world’s balancing act. We know that we all have to get along, because if we don’t, there goes the functionality of everything we interact with.

Metals

Metals play a crucial role in our daily lives and in the global economy. Steel, copper, aluminum, and other metals are the foundations of the objects we interact with every day.

-

Steel is used in construction, infrastructure, cars, appliances, and many other products.

-

Aluminum is a lightweight metal used in airplanes, bikes, tech products like phones, and cans and is tightly tied to transportation and packaging.

-

Copper is used in electrical wiring, electronics, plumbing, and coins and is an indicator of the broad health of the global economy because it’s used in so many different products.

If the supply of one commodity goes bonkers, so does that of all the others. Rare earth metals, with names like neodymium, lanthanum, and cerium, are becoming increasingly important. They are pivotal in manufacturing high-tech devices, from smartphones and electric vehicles to advanced military systems. They are what make our gadgets smaller, batteries last longer, and electric motors more efficient.

But, of course, it’s a geopolitical hot potato. Most of these metals are mined and processed in a handful of countries, with China being the dominant player. Supply-chain concentration and environmental costs are headwinds, as we increasingly grapple with the idea that our current path of technological advancement hinges on us having the real world figured out.

The Rise of U.S. Shale Oil Production

The rise of U.S. shale oil production is an excellent illustration of the dysfunctional dynamics of the commodities markets. In the late 2000s and into the 2010s, cheap ways to get hydrocarbons from shale rock formations were discovered, and shale oil extraction technology improved so much that U.S. shale producers were able to produce more oil than the traditional producers such as Saudi Arabia and Iran.

When the United States began producing shale oil, all of a sudden the proverbial geopolitical table turned; there was a new oil king in town. It also changed U.S. employment patterns, increasing jobs in the oil industry and creating a reduced reliance on oil imports. OPEC and other producers had to adjust their output (and economic growth projections) to maintain prices.

However, shale oil producers got a little too excited and produced too much shale oil. That caused a glut of oil and gas, putting downward pressure on prices and making everyone pretty mad. Especially the investors in the shale industry! The shale oil industry burned through enough cash during that time to make those people very upset—to the point where “capital preservation” became a key part of the energy industry.

After Russia invaded Ukraine, there was an energy crisis in Europe, because both Russia and Ukraine are suppliers of oil to the European energy market. Ideally, U.S. shale oil production should have been increased during that time to make up for the lost supply, but investors in the industry were still not happy. The industry had lit its investors’ money on fire a few times during the past several years (to the tune of $600 billion), and now investors are being very conservative. They say, “Shale, please focus on giving us money! Thanks! No more expansion, no more rapid growth, just free cash flow and dividend yields, and that’s all.”

So the shale people are like, “Ah, okay, no problem, sugar dad—I mean shale daddy.” They remained focused on providing returns to investors instead of meeting the European demand for oil that Russia and Ukraine can’t supply because of the war and OPEC can’t supply because of misaligned incentives. This created value for shareholders at the expense of the global energy market as demands were not met with supply, even though the market demanded it!

The Rise of Renewables

Many might be asking, “What about renewables? Surely we have made great progress there?” We have! But unfortunately, green energy policy cannot be carried out without green energy investment. We have to deal with the “oil spill” before we can make a full transition to more sustainable resources. But everyone is like, “What if we just drive electric vehicles? That will show Big Oil!” Electric vehicles (EVs) are great, but the raw materials and metals needed to produce EVs and their batteries are all increasing in cost due to their increased demand—and there is not enough manufacturing capacity. For instance, lithium, crucial for battery production, has gone exponential in price. And it just gets back to the idea that we can’t have green energy without dirty energy. We need oil to build out the infrastructure to make EVs, solar panels, and nuclear reactors.

The shift to renewable energy isn’t just about technological advancements—it hinges crucially on global cooperation. Climate change, after all, doesn’t care about borders. To effectively transition to renewables, countries must transcend their individual interests and work together. This means wealthy nations aiding less developed ones through technology transfers and financial support. It’s about more than just signing international agreements like the Paris Climate Accord. It’s about actual, tangible actions.

We’re talking about easing trade barriers to allow the free flow of renewable tech, sharing breakthroughs in energy storage and efficiency, and truly committing to a collective approach. However, the challenge lies in aligning disparate economic interests and political agendas. It’s a delicate dance of diplomacy and mutual understanding as the world tries to balance national priorities with the pressing need for a sustainable future.

The green energy transition isn’t a clean break; it’s a complex, winding road toward progress. It involves balancing our current energy needs with the goal of a more sustainable future. As we navigate this path, both at the domestic and global level, we must be mindful of the economic, environmental, and logistical challenges that come with such a monumental shift in how we power our world in a more sustainable way.

Artificial Intelligence and Commodities

There is a world in which AI helps us manage our crops, sow them in the perfect temperature, and provide them with the perfect amount of water, but it is dependent on an electrical grid! Similarly, in the mining industry, AI can significantly enhance the extraction of the key commodities like steel and copper that I mentioned. By using machine-learning algorithms, mining operations can predict and locate resource deposits more accurately, improving efficiency and reducing environmental impact. But it all required a foundation. AI requires massive computational power and servers that run constantly. That is a risk!

We need food. We need copper and steel and wheat and corn and lumber. The maintenance of the real world outside the vast and deep void of the internet is important! Commodity shortages remind us that, as the evolutionary biologist Lynn Margulis put it, “We abide in a symbiotic world.” She wrote about lichen, a partnership of algae and fungi, as a metaphor for the interdependence of all living things, surviving through collaboration rather than competition:

Like a farmer tending her apple trees and her field of corn, a lichen is a melding of lives. Once individuality dissolves, the scorecard of victors and victims makes little sense. Is corn oppressed? Does the farmer’s dependence on corn make her a victim? These questions are premised on a separation that does not exist. The heartbeat of humans and the flowering of domesticated plants are one life. “Alone” is not an option.

The brilliance of AI’s computational power is linked to the raw, tangible materials it helps to produce and manage. It’s a symbiotic relationship where each domain—the digital and the material—enhances and enables the other, illustrating that our digital-driven world and journey toward a more AI-integrated future is as much about the resources we extract from the earth as it is about the data we extract from our algorithms.

Nature is part of us, and so are commodities—because they are part of nature. We need to respect that fact in our pursuit of survival.