Chapter 5

Supply and Demand

Introduction to Supply and Demand

Ever wonder why your favorite coffee brand gets pricier or airline tickets fluctuate in price? It all comes down to the seesaw of supply and demand—balancing what we have versus what we want.

Supply and demand is a pretty intuitive theory that we use almost every day without knowing it! There are a lot of complicated graphs that explain it in granular detail, but the general idea is that the price we pay for things is determined by how many people want it (demand) and how much is being produced and sold (supply).

When demand is low (no one wants a thing) and supply is high (there is a lot of a thing being produced), that will push prices down. Conversely, when demand is high (a lot of people want a thing) and supply is low (not a lot of the thing is being produced), that will push prices up.

In 2021, the Pokémon Company printed 9 billion Pokémon cards to stop speculators from making a bunch of money selling rare cards. It was able to stop people from making a bunch of money on the demand for rare cards by simply managing supply and producing more cards. Turn on the supply faucet, and prices usually tend to go down.

Think about Taylor Swift concert tickets in 2023. A lot of people wanted tickets! However, there was not enough space in most of the arenas to hold all the people who wanted to attend the concerts. So, the ticket prices were pushed up to test how much people really wanted tickets—a reflection of the high demand for tickets and the limited supply.

Taylor Swift tickets show the influence of corporations and how sometimes price fluctuations are not just about supply and demand. There was a huge controversy about Ticketmaster price gouging and using weird selling mechanics that kept the prices from being determined by the market. Sometimes corporations, especially those that have a monopoly over what they sell, can set prices regardless of the level of supply and demand.

Supply and demand—it’s everywhere and everything.

The Economics of Banana Bread

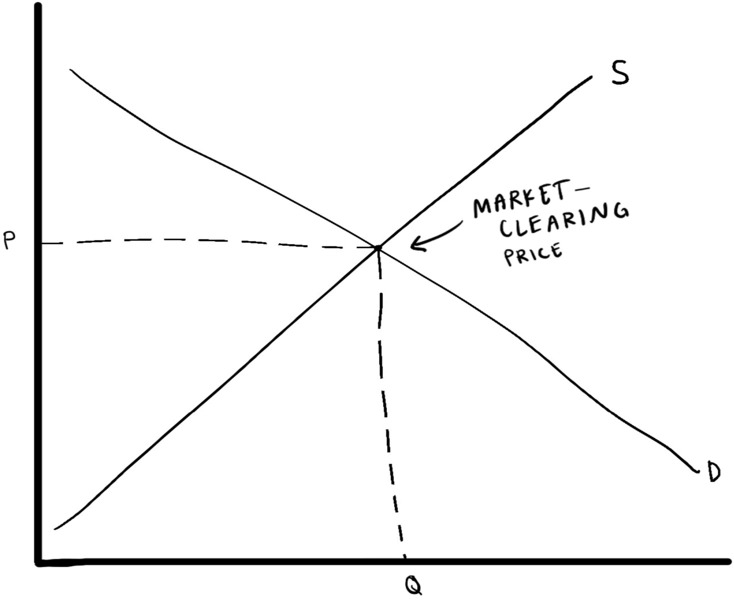

In every marketplace, whether it’s global commodities or a local bake sale, the principles of supply and demand are at play. Anyone familiar with planet Earth knows that sellers try to sell their goods and services at the highest price possible, whereas buyers try to buy things at the lowest price possible. The market price is where supply and demand meet: the lowest price a seller will accept and the highest price a buyer will pay.

When supply and demand are balanced, there is a state of equilibrium in which they meet. That is when the market price is reached!

-

A price above equilibrium is a price at which people want more things than are available.

-

A price below equilibrium is a price at which there are more things available than people want.

Let’s visit my grandma’s kitchen to see this in action. She’s been baking banana bread for the past thirty years, and it’s a perfect example to illustrate these concepts.

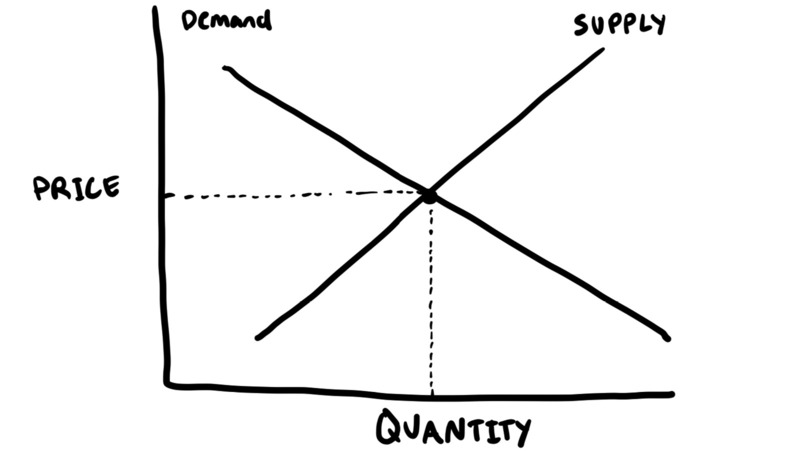

The demand for Grandma’s banana bread is the quantity of bread that customers would buy at all possible prices and is represented by a downward-sloping curve, as shown in the graph on this page. If Grandma decides to hike up the price of her banana bread, people aren’t going to buy as much. But if she lowers the price, they are likely to buy more.

A change in demand might also occur if, for example, a new study comes out that says eating banana bread is healthy for you. Suddenly, more people will want to buy Grandma’s banana bread, because they have more incentive to eat it, and the demand curve will shift upward.

On the other hand, the supply of Grandma’s banana bread is the quantity that Grandma is willing to produce and sell at all possible prices and is represented by an upward-sloping supply curve.

If the price of the ingredients goes up, it will become more expensive for her to make the bread, so she may produce less. Grandma is willing to sell at each price point along the curve. If prices go up, the quantity supplied of banana bread will increase, and if prices go down, the quantity supplied of banana bread will decrease.

However, if the price of flour goes up—an input to her good—Grandma may have to raise the price of her banana bread or produce less bread to maintain her profit margin. This would result in an upward shift of the supply curve.

The market price of my grandma’s banana bread is determined by the intersection of the supply and demand curves—the equilibrium. These are not just abstract economic theories; they’re everyday realities impacting how goods (like banana bread) are priced and sold. Supply and demand plays out on a global scale in a more complex and far-reaching system through the intricate and expansive world of supply chains.

Supply Chains

While the principles of supply and demand in Grandma’s kitchen might seem a world away from global trade, they are indeed connected. The history of supply chains can be traced back to ancient civilizations, where horse-drawn carts moved silks and other wares along newly established trade routes. The early trade networks such as the Silk Road made it possible for global trade to be conducted. The Industrial Revolution was when modern supply chains truly came into existence, with steam-powered ships moving across oceans and railroads crisscrossing nations. Ever since then, supply chains have become increasingly complex—and delicate.

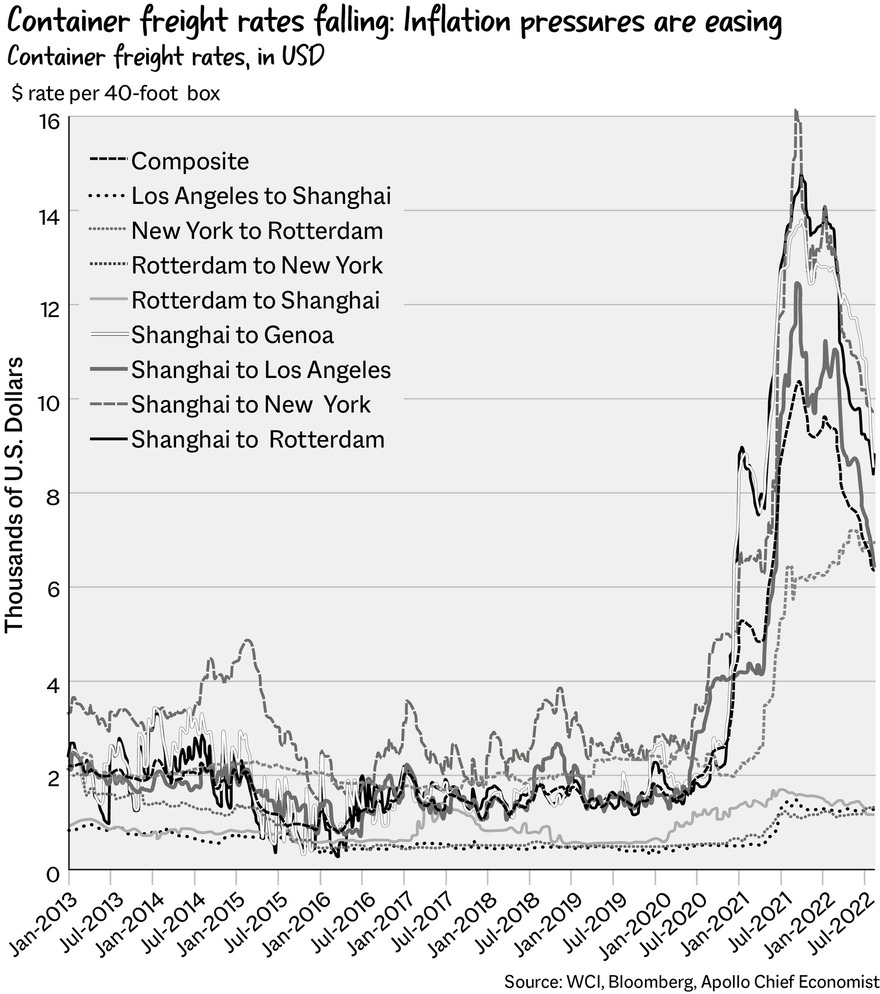

Suppliers use ships, planes, trains, and trucks to rapidly move goods around the world, winding through farms, manufacturing sites, warehouses, distribution centers, retail shelves, and more. However, due to the numerous links in these networks, they are easier to break than to improve, as seen during the covid-19 pandemic, when the global supply chain was disrupted. Planes were grounded. Shipments were delayed or halted, causing a buildup of container ships outside major ports such as Los Angeles. As a result, shipping rates soared, reaching levels not seen in twenty-five years. The already overwhelmed supply chain struggled to cope with the influx of goods and the limited number of available transportation routes, as well as a shortage of personnel and equipment to move the goods.

There are various metrics used to measure the performance of supply chains, such as the Global Supply Chain Pressure Index and the Manheim Used Vehicle Value Index. This 2022 chart from Apollo shows the decline in container freight rates across the board. It became very expensive to ship things during the pandemic—but then it wasn’t expensive as supply chains began to normalize.

In 2020, the global supply chain fell apart because so many companies had shut down. But the world still had to function, despite the disruptions and challenges that were occurring on an unprecedented scale. The main lesson learned during that time was that supply is not infinite. The early 2020s were when things stopped “thinging.” They exposed our fragile reliance on something that powers almost everything in our daily lives and is constantly exposed to natural disasters, geopolitical tensions, and the rickety nature of the physical world. The backbone of our global economy became a question mark rather than a foundation.

Semiconductors

Remember those teeny chips that had supply and demand going bonkers? Semiconductors are an electrically conductive material that are the building blocks of modern technology. They’re basically the brain of electronics, playing a crucial role not only in cars and computers, but also in a wide array of household devices like toasters, laundry machines, and much more. Most of our ways of living would not be possible without semiconductors. For example, the two-minute timer that you use to brush your teeth? It’s reliant on a semiconductor. What happened with semiconductors in 2021 and 2022 was a perfect supply-versus-demand storm.

-

In 2020, the covid pandemic shut down factories. Semiconductors can’t be produced if the factory isn’t running! Factories were also plagued by natural disasters that forced some plants to stop production. In Texas, there were ice storms (a complete anomaly and very representative of the anomalous times we seem to be living in). Taiwan was going through a series of droughts that made it hard for the water needed for chip production to be supplied.

-

There was also the constant backdrop of geopolitical tension. China was circling Taiwan during that time, which was stressing everyone out because if China invaded Taiwan, that would greatly increase the probability of a global conflict. Taiwan is the world’s leading semiconductor producer, so that created a pressure-cooker situation.

-

The pandemic also shut down ports. Chips can’t be delivered to manufacturers if they can’t be landed! So even when the factories did produce chips, the chips did not go anywhere.

-

Later on, demand came into play. The supply chain went into chaos because people were emerging from lockdown and wanted more things, and all those things contained semiconductors.

Various supply issues and outsized demand, coupled with breakdowns in semiconductor production and delivery, produced a perfect storm of not-enoughness. Car companies were reducing production over chip worries, Apple warned that the shortage would impact iPhone production, and there were doubts that the semiconductor supply would ever recover.

Ultimately, the issue was solved mostly through policy and technology (although supply chains are never completely perfect). Apple began to make its own chips in-house, switching from Intel to M1; Tesla announced the Dojo supercomputer; and the Taiwanese company TSMC, the world’s first and largest semiconductor foundry, announced plans to build factories in the United States. The semiconductor crisis, which rattled the core of global technology and manufacturing industries, extended into the auto market, which was its own peculiar supply-and-demand situation.

Used Cars

Used cars are an essential part of the automotive market, usually providing a very affordable option for those who don’t want to buy a new vehicle. But during the pandemic, used cars were more expensive than new cars, which is bonkers! The problem was, of course, caused by supply and demand. Supply chain disruptions, a semiconductor shortage, and a raw materials gap led to issues in producing new cars, and, therefore, car buyers had to buy used cars. Just to make things extra spicy, there was a shortage of used cars, too. There just weren’t enough cars anywhere!

That of course led to a wild spike in car prices. January 2021 was the beginning, with the average used-car price reaching a peak of $25,000 in February 2022. In comparison, the median price of used vehicles had been $17,500 in July 2019—a 40 percent jump!

Cars with hundreds of thousands of miles on them were selling for well north of $10,000. This is opposite to how we think the used-car market should work! A new car depreciates by almost 20 percent as soon as you drive it off the lot. A vehicle that has been driven to near nonusability should be inexpensive! Not cost $10,000!

It gets even weirder. Older cars were actually more expensive than younger cars, completely throwing aside any rational market model of pricing. A 2009 Camry went for roughly $8,000 in 2019. The price skyrocketed to $16,000 in 2022. A 2016 Camry going for $22,000 in 2019 sold for $33,000 in 2022. Both cars got more expensive. The price of the 2016 Camry went up 50% but the price of the 2009 Camry doubled—something that doesn’t really make a lot of economic sense.

That showed the power of supply and demand. There weren’t enough new cars to satisfy the demand, so people turned to used cars. They wanted sedans because they were (theoretically) cheaper. It also showed the pricing power that companies have. Manufacturers’ profits surged, as reported by Axios, despite less car production and fewer cars being sold. The whole thing was a mess. It flipped what we understood about markets and pricing dynamics and gave it all a big middle finger.

Used-car prices were a clear example not only of pricing mechanics but also of the importance of supply and demand. In most cases, a supply chain breakdown is the result of policy failure. And policy will be required to repair it.

So let’s talk eggs.

Eggflation: When Eggs Come in Short Supply

For a few weeks in late 2022, eggflation was a big topic of discussion. People who were used to buying ten dozen eggs a week for bodybuilding purposes were in shambles.

If you were even able to find eggs, they were likely going to cost $3 to $4 more per carton than before. Eggflation was an economic phenomenon that impacted breakfast tables and restaurant chains alike. But how did it happen?

There were quite a few culprits. February 8, 2023, marked the one-year anniversary of when the highly pathogenic avian influenza, or HPAI, was found in commercial chicken flocks in the United States. The infection had begun in Dubois County, Indiana, and spread quickly across the country, decimating chickens and thus the egg supply. In 2022, almost 60 million birds were lost to HPAI. There were roughly 300 million egg-laying hens left at the end of the year, far fewer than normal.

Supply chains also played a role. Chickens eat a lot of corn and a lot of soybeans. Not only did the cost of chicken feed spike, but breaches in the supply chain made it much more difficult to get the feed to the chickens. (There are still breaches in the supply chain, with millions of chickens starving in California because corn wasn’t delivered on time due to delays on the part of the Union Pacific railroad.) Egg suppliers are very reliant on railroads, which means that the supply of eggs can get very volatile very fast—and add to egg price concerns. Compound that with a very cold, wet winter, and the feed supply chain was in shambles.

Then there’s demand. We eat way more eggs than we used to! Per capita annual consumption is forty eggs more now than it was in 2012. A greater demand for eggs and not enough egg production due to a lack of laying hens was a recipe for distress.

The egg crisis was bad. Prices shot up quickly and aggressively. But the outrage we saw was largely a function of the media and the story behind why eggs were going up in price. When news reporters started complaining about the price of eggs, there actually wasn’t much of a markup! Stores were selling eggs for roughly the price at which they were buying them from producers. But once people get freaked out, just as they did about toilet paper during the pandemic, it can lead to an insane price spiral, which was partially what we saw with eggs because the news was like “there are no eggs go panic mode everyone.” So of course, people went into panic mode. That put even more pressure on the supply chain because people tried to buy extra eggs and hoard them, which exacerbated the shortage, and so on and so forth.

Hand-wringing headlines created a loop of people freaking out about prices, prices rising, and people freaking out more. As Mike Gauntner, a reporter for 21-WFMJ, wrote, “High consumer prices for shell eggs has [sic] caught the attention of the national media, raising consumer awareness and fueling a rising resistance.” That’s why Jerome Powell, the chair of the Federal Reserve, prefers rational inattention to inflation; if people are watching what is going on, they are more likely to respond to it, which can exacerbate the issue at hand.

What got less coverage was that, adjusted for inflation, egg prices were actually lower in 2022 than they had been in 2015. Prices peaked in December 2022, with a dozen eggs selling for around $5 on average. Egg supply and prices were already recovering in early 2023. Producer prices, the prices farmers charge grocery stores, began to fall. The retail price, the price consumers pay in the grocery store, fell sharply (by $1 in one week in early January!) and continued to fall into 2023.

The moral of the story is: We need more egg-laying chickens.

The eggflation story is emblematic of what could happen to the rest of the economy. We are dependent on fragile systems that can break when stressed.

Beyond Mechanics and into Policy

The basic idea is this: When there is more demand for a thing than there is supply, the number of people wanting it is greater than how much is available and the price will rise to sift out the people who don’t truly want the thing. If there is a greater supply than demand, more people are selling the thing than buying it and the price will drop. But we’ve seen one price distortion after another in recent years, thanks to the screams of the media, reflexivity, shortages of raw goods, supply chain disruption, and good old-fashioned price gouging. How can this be fixed? By fixing the bad policy that creates misdirected incentives.

Making Supply Chains Better

After what happened to supply chains in the first two years of the 2020s, businesses and local government bodies should be funneling money into capital investment: repairing or upgrading old equipment (such as installing air-conditioning units inside delivery trucks), buying new equipment (including new cranes and larger container ships), investing in new technology (such as a software system that doesn’t have employees tearing their hair out or logistics services that improve tracking and inventory management), building bigger warehouses and fulfillment centers (which are needed especially in the ecommerce industry), and more. All of this is done with the goal of helping goods, services, and information flow more efficiently and making workers less miserable.

Of course, putting money toward rebuilding supply chains isn’t as exciting as investing in the hot new thing, whether it be deepfakes, artificial intelligence, or cryptocurrency. One of the most crucial links in the supply chain was built on the premise that workers would provide labor for free. As Bloomberg journalists wrote:

Port truckers are typically independent contractors, without the benefits and protections of unionized transport sectors or even major companies with shipping divisions, such as Amazon. Their jobs require them to line up for hours to pick up cargo, and they’re paid only when they move it. “The port truck driver, for decades now, has basically been the slack adjuster in the whole system,” said Steve Viscelli, an economic sociologist with the University of Pennsylvania who studies labor markets and supply chains. The entire system, he said, is built around free labor from truck drivers as they wait for containers.

Essentially, companies tell their truck drivers and crane operators, “Hey, listen, we are going to underpay you, we are going to expect you to do more work than you should and thus create a completely misaligned incentive structure.”

In 2020, all the small details of our supply chains were highlighted: railroads, ports, and cranes; how long ships spend at the dock and the touch points for the RTG/RMG container crane operators, truck drivers, and clerks; how long containers sit without drivers available to drive them away; maintenance of yard equipment; package unloading. Each of these factors has a cascading, knock-on effect.

Policymakers aren’t directing dollars to where they need to go. When the 2020 financial crisis occurred, the government was able to solve the problem by providing monetary support—a lot of monetary support. But when ports shut down, they can’t be reopened the same way. Real-world solutions are called for. Anthony Lee Zhang, a professor at the University of Chicago, once tweeted, “As resources get cheaper, we find progressively dumber uses of them.”

Things like artificial intelligence, autonomous vehicles, 3D printing, virtual reality, and potential innovations like quantum computing will of course change how we interact with the world. But we have gotten very good at taking raw materials out of the earth and making things out of them. However, the cost of repairing things (labor) has skyrocketed, hence the “I’ll buy cheap things because they’re cheap rather than repairing those I already have” mindset.

That’s the thing about presumed infinity. Because we live in a time of abundance in most developed nations, it can feel as though we are always going to have everything, forever. But the reality is that we aren’t always going to have everything, forever.