Chapter 4

The Mechanics of Modern Money

-

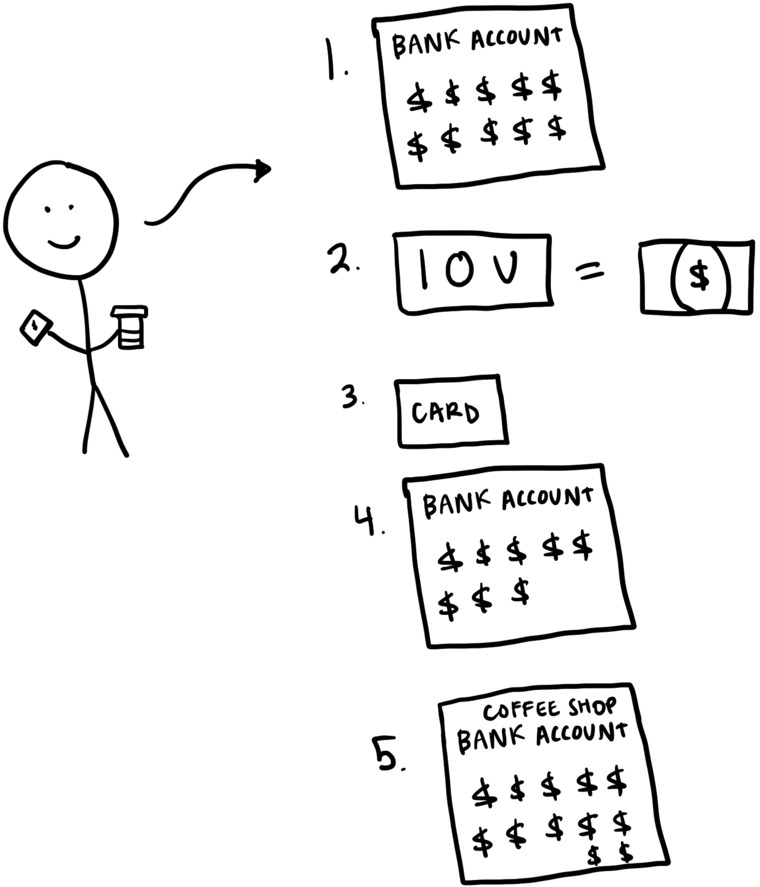

You have a bank account, which holds your bank deposit.

-

Your money on deposit at the bank is actually an “Oh, man, I owe you money” note from the bank. It’s a promise that you will be paid from your account when you go to the bank and ask for money.

-

You swipe your card for coffee.

-

The bank processes the payment by taking money out of your bank account, thereby reducing your deposit (or, if you use a credit card, adding the amount to what you owe your credit card company).

-

The bank transfers the money to the seller, thereby increasing the seller’s bank deposit.

Banks are the gatekeepers of money. They are the money business model. The U.S. government is the creator of the money, the ultimate facilitator of what the banks are able to do. The government “creates” money in two ways:

-

By issuing coins and notes. The U.S. Treasury (specifically the U.S. Mint and Bureau of Engraving) creates currency notes, whereas the Federal Reserve issues them. The money goes into the bank system right away—so banks still are running the ring of money, facilitated by the government.

-

Through credit markets. The government issues bonds, promises to pay money back at some point in the future. The markets (made up of foreign governments, asset managers, and the Federal Reserve at present) say, “Ah, yes, we will buy those from you,” and with the money gained, the government is able to execute on public infrastructure, social spending, insider trading, and other activities. Corporations do the same thing: They issue bonds, which serve the same functionality but have a different interface (which I will talk about later).

The government doesn’t really control the money supply; it can nudge it around via all sorts of mechanisms that I will get into later, but it’s really the Big Boi Banks that are in charge. If all of this seems abstract and convoluted, that’s because it is. You’re not crazy! And there are times when collective trust can go poof, and money is no longer money.

The Banking Blueprint

The banking business model is built on trust, but it’s also built on their ability to borrow short (mostly through customer deposits) to lend long (through longer-term loans such as mortgages); that is their business model. They collect deposits from people like you and me and usually pay us interest on those deposits so that we’re incentivized to keep our money with them.

Banking is akin to an arrangement in which the government says, “Banks, you can earn big bucks by distributing money to the public on behalf of us, the government, and the public will believe in you because we believe in you.” For a super-simplified example: Imagine you’re at a carnival, and there’s this mega-popular game booth. The carnival organizers (that’s our government in this analogy) aren’t really interested in running the game themselves, so they let specific chosen ones (our banks) set up shop and run that game.

It’s like the carnival bosses saying, “Hey, you banks. You won. All you’ve got to do is distribute these prizes (money) to the winners (public). We’re not going to give these rights to just anyone, just you. This is trust.”

In essence, the “franchise” part here means the exclusive right or privilege given by the government to banks to handle and distribute money. Just as a franchisee in the business world gets rights to sell a product or service under the brand name of a bigger company, banks get the “franchise” from the government to be the primary handlers of our monetary system. And because of this official stamp of approval, people trust banks with their hard-earned cash. The banking business model’s success relies heavily on a key concept known as fractional reserve banking. This concept plays a pivotal role in how banks operate and contribute to the broader economy.

Fractional Reserve Banking

Of course, as a bank, you’re getting money from deposits and interest payments, so you can loan out more than you have—the fundamental concept of fractional reserve banking! Banks are allowed to loan out the majority of the deposits on their books, the theory being that not all their depositors will want to withdraw their money at the same time. If you deposit $100, the bank doesn’t have to keep the whole amount in the bank. It can loan that money out! That is how it makes money! If it does not lend out deposits, it is going to have trouble making money and continuing to operate as a bank.

But it also has its own money, called its reserves—all the cash it holds plus any money it is holding at the Federal Reserve. It must keep a fraction of those reserves on hand, but the rest can roam wild and free.

Where did this business model of borrowing come from?

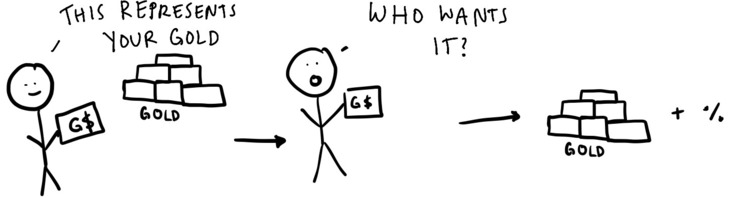

For a long time, gold was the primary medium of exchange. But no one wanted to carry around large quantities of gold, so they started leaving their gold with a goldsmith. The goldsmith was like, “Sure, I will hold on to these for you. Here’s a piece of paper representing your gold.” Then people started trading their gold receipts and the goldsmiths started lending out gold with interest.

This is fractional reserve banking: lending out more than technically exists, making it so that not every dollar can be given back all at once.

So the banks take the money, invest it in securities that earn maybe 2% to 3%, and keep the spread between the interest they’re being paid and the interest they’re paying to their customers, or the net interest margin. Understanding the principles of fractional reserve banking sets the stage for exploring the next crucial aspect of banking: the process of making loans.

The Art of Lending

Banks take a variety of factors into account when making decisions about loans and investments, including the movements interest rates are expected to make. This is a function of expected loan demand and risk assessment: If rates are expected to rise, banks will charge higher rates on the loans they issue and prioritize shorter-term loans to reduce any potential losses of long-term assets due to those higher expected borrowing costs.

Once the loans are made, money is created because the banks are essentially creating new money through loaning out deposits.

To understand this better, we can take a look at a bank’s balance sheet.

A balance sheet is composed of assets and liabilities—what a bank owns and what it owes.

-

The bank’s assets: what it owns, including loans extended to customers, government securities held, deposits maintained at the Federal Reserve, and other holdings.

-

The bank’s liabilities: things that it owes, which are the checking and savings accounts that people have with it, certificates of deposit issued by the bank, and loans taken by the bank.

-

There is also net worth, which is owner’s equity, or how much would be left after the bank pays off all its liabilities.

This ties in to something known as the accounting equation: Any company’s total assets—everything it owns or controls—must be equal to its liabilities—its financial obligations and debts, shareholders’ equity, the initial investment made by shareholders, and retained earnings generated over time. This is what makes the balance sheet balance. So the bank has to ensure that its assets match its equity and liabilities.

Decoding Bank Balance Sheets

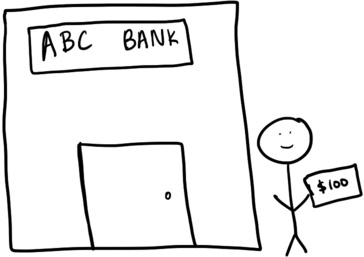

Let’s say you go to ABC Bank and deposit $100 into your checking account. That money now becomes part of the bank’s reserves as an asset, whereas the deposit in your checking account becomes a liability. When you deposit money, the bank makes a promise to you that it will pay you back. The dual nature of bank deposits is a fundamental principle of banking. When you deposit money, the bank makes a promise to you that it will pay you back. Deposits come with costs to the bank: the bank branches that seem to haunt every corner of cities, the apps we use to access our accounts, and the interest you are paid on the deposit are all things that the bank has to pay for.

Depending on the current macroeconomic environment, banks’ reserve requirements can vary widely. During 2020, it was dropped to 0 percent because everyone was like, “Banks, please lend all your money right now and save the economy.” Before then, it was 10 percent for a long time and should eventually tick back up as the Federal Reserve imposes a tighter monetary policy.

Returning to ABC Bank, it would be required to hold reserves of $10 on your deposit ($100 times 10 percent) to be kept on hand just in case the bank implodes, and it takes the $90 in excess reserves, the amount it’s allowed to lend out, and does exactly that. To the bank, the $90 loan is an asset and the checking account of whoever borrowed it is a liability. The books are still balanced!

The Invisible Sheriff

Excess reserves are like the secret sauce in the banking world, particularly when it comes to lending, snapping up government securities, and ensuring that the folks who’ve stashed their cash in banks can get it back when they want. These reserves are what banks have tucked away above and beyond what the rulebook says they need to keep on hand. They’re super important because they give us a sneak peek into how banks might influence the whole money game through something called the money multiplier effect.

Now, when it comes to the money banks can lend out, the rule of thumb is usually tied to how plump their reserve cushion is—assuming there’s some kind of minimum reserve requirement. But let’s say this requirement is zero, like it was in 2020.

In theory, banks could go wild, lending out as much money as they’ve got in deposits. But here’s the catch: If they get too loan-happy, they could end up with severe liquidity issues (translation: not enough quick cash to meet immediate demands). So even if we’re thinking, “Yeehaw, let’s go full Wild West with banking,” there’s still this invisible sheriff in town—the unspoken rule that going overboard with loans could cause a major freak-out. Banks need to keep enough in reserves to keep their depositors from panicking.

In the past decade, things went pretty well for banks. Interest rates were basically zero, so they didn’t really need to pay much of anything to their depositors—around 0.01% on average. That was good for the banks! They were earning 2% to 3% on all the money people put into them. But if the Fed raises interest rates, the banks are going to need to pay more on deposits, meaning that they aren’t going to be making as much money as they used to. That’s well and good, but if banks are caught way off guard—say, they need to start paying 4% on deposits but are earning only 3%—they are going to be in trouble.

How Banks Hedge Risk

This is why banks employ strategies such as hedging, a risk management strategy that can protect against unexpected fluctuations in interest rates. Hedging is similar to planning a beautiful party in the park, complete with non-weatherproof snacks and drinks, and having a backup plan in case it rains. Banks use similar backup plans to protect themselves against sudden changes in the financial weather. A common practice is using interest rate swaps, which involve swapping interest rates. Let’s say Institution A has a variable-rate loan (the rate moves when the financial market moves) and Institution B has a fixed-rate loan (the rate stays the same regardless of financial market movement).

-

The two institutions can enter into an interest rate swap agreement, in which they agree to pay each other’s interest rate obligations.

-

In this scenario, if rates rise, Institution A might face steeper loan payments. But here’s where Institution B steps in, saying, “No sweat, we’ll cover the fixed interest rate to balance out your increased payments.”

-

Conversely, if rates fall, Institution A will pay less on the loan and will say, “Okay, Institution B, I’ll pay you the lower variable interest rate.”

-

This way, both are hedged against fluctuations that may occur either way as they have the other institution there to bail them out.

When banks don’t have such protective measures in place, things can get messy. While hedging strategies are crucial for managing risks, it’s important to recognize that even with these measures, banks can still face significant challenges—like complete failure.

How Banks Can Fail

A bank can fail for a number of reasons, such as insolvency, in which it runs out of money due to making risky loans. They can also fail due to illiquidity. If all of a bank’s customers panic and line up (or click a button) to try to get their money back at the same time, the bank will not be able to give every dollar deposited back to every person who wants it, leading to a bank run—like with what happened with the Silicon Valley Bank (SVB) failure in 2023.

SVB had constructed its banking business model perfectly well, borrowing short to lend long. That would have been fine, except that it had no hedges on to protect against downside risk, so when the Fed started raising rates and defining a new normal, its soft underbelly was exposed to the vicious elements of the cruel, cruel world.

Imagine this: The bank’s in hot water, losing money left and right. Then the drama unfolds on social media, sparking a digital-age bank run. Ultimately the Federal Deposit Insurance Corporation, or FDIC (which insures consumers’ bank deposits), and the Treasury went in to save the bank via coverage with three tools:

-

The FDIC’s Deposit Insurance Fund

-

The new Federal Reserve Bank Term Funding Program, which provides loans to banks and other financial institutions

-

A $25 billion backstop from the Treasury’s Exchange Stabilization Fund

In 2008, the 10 percent reserve requirement was in place. Banks needed to hold on to money. But they were offering subprime mortgages to high-risk borrowers (people who do not have strong creditworthiness and who will likely be unable to pay back the loan) and then bundling the mortgages together into mortgage-backed securities, or MBSs (a pool of mortgages with similar characteristics that represents fractional ownership of the entire pool and pays the MBS holders money through the principal and interest rate payments the borrowers make), and selling those time bombs to investors.

The banks found a way around the reserve requirement by using something called a collateralized debt obligation, or CDO, a complex financial instrument that packages all types of debts, such as bonds, loans, and mortgages, into a single security that is sold to investors. Similar to the MBS, the cash flows from the debt payments are what make these things juicy to hold on to. They are divided into senior tranches, which hold the least risky debt, and junior tranches, which hold the more risky debt. It’s all about redistributing risk. But during 2008, CDOs held some of those subprime mortgages. Their issuers took the risky mortgages and other risky loans and piled them into CDOs to sell even more time bombs to investors. But because they were backed by a pool of all sorts of assets, they achieved an AAA rating, meaning that everyone was like, “No problems here, fellas, this is safe and good.”

There were definitely problems here, fellas.

The housing bubble burst. Mortgage payment defaults began to rise. The time bomb blew up. And because the banks had been sneaky and had gotten around the reserve requirement via CDOs, they needed help. They began to fail. Then the Fed had to step in, and the economy has never really recovered, resulting in the decline in economic growth, the high unemployment rate world that Millennials graduated into, the slowdown in investment in housing (leading to the housing crisis that we have right now), the sovereign debt crisis that echoed across other nations, and the complete erosion of trust and confidence that people had in our systems—and of course the decade-long zero-interest-rate policy, or ZIRP, world that we lived in up until mid-2022.

The central banks and physical cash provided by the government help support the banks, but the banks are really the P. T. Barnums running the circus.

Banks influence markets and people and the economy across the board, but what they influence most directly is credit availability for consumers, the money supply, interest rates (they are de facto members of the Federal Reserve!), and payment systems, which gets into the cross currents of the economic kingdom—the U.S. dollar!

The Dollar’s Reign

Think of the U.S. dollar as more than just paper and coins; it’s a powerhouse of economic strength. The U.S. GDP (Gross Domestic Product, which is the total economic value that a country is producing during a specific time period) is giant, making up over a quarter of the global economic pie. This dominance lends immense power and stability to the dollar, making it the world’s principal reserve currency. Countries worldwide hold the dollar in their reserve, use it for international trade, and rely on its value to stabilize their own economies.

That’s why when the world gets weird, the dollar usually becomes stronger. During periods of global economic uncertainty, more people demand the dollar because of its perceived stability, which (usually) results in its value increasing relative to that of other currencies—more demand, more value. When we say that the dollar increases in value, it means that the exchange rate of the U.S. dollar has increased against other currencies and each dollar can be exchanged for more units of another currency. Let’s say that $1 used to equal 0.85 euro but now equals 0.95 euro. If you want to take a trip to Paris, $1,000 used to be equal to €850, but now it’s equal to €950.

Stronger U.S. Dollar |

Weaker U.S. Dollar |

|

If you’re a U.S. tourist abroad you love the stronger dollar. You can buy more things in other countries because the dollar is worth more. But if you’re an international corporation, it’s a bit of a different story.

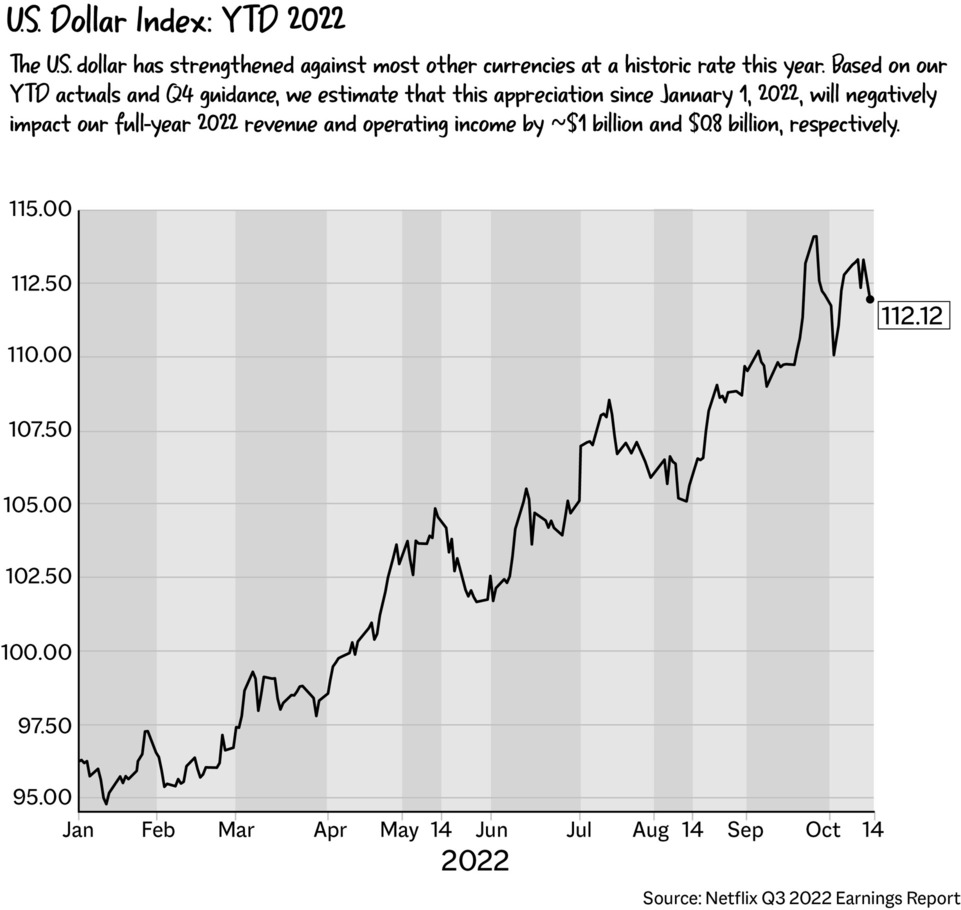

Netflix ran into the problem of a stronger dollar back in 2022. As Jack Farley, a macro researcher at Blockworks, explained, “Netflix says the rising dollar will cost them about $1 billion in revenue for the year.” The situation arose because Netflix conducts business overseas. Its subscribers pay in local currencies, and when those local currencies are converted to U.S. dollars—and the dollar is strong—it diminishes how many dollars those local currencies turn into. So Netflix was walloped by the strong dollar in 2022.

A stronger dollar is a wrecking ball in a lot of ways—but funnily enough, the dollar is the only real hedge against inflation. Xiang Fang, Yang Liu, and Nikolai Roussanov published a 2022 paper titled “Getting to the Core: Inflation Risks Within and Across Asset Classes’’ that explored this. As they explained:

The only “real” hedge appears to be the U.S. dollar which is contrary to much conventional wisdom, but entirely consistent with our historical evidence! Why does USD strengthen when US Core inflation is up? One obvious reason is the expected tightening by the Fed, which makes dollar interest-bearing assets more attractive. A more subtle reason that we point to in the paper is the real exchange rate appreciation—core goods, which are inherently less tradable than energy, become more valuable, driving up consumers’ “marginal utility” of consumption.

The dollar is an inflation hedge, backed by nuclear bombs, F-22 fighter jets, aircraft carriers, and millions of American military personnel. All the talk about the United States being a really stable place is essentially a big red arrow pointing to the power of the U.S. military and its allies. European Union countries, Japan, Korea, Mexico, Australia, and other countries all say, “Yes, the U.S. dollar is the way to go.”

As Karthik Sankaran once tweeted, “The most important aspect of USD centrality is not its role as the dominant international reserve asset, but rather its role as the dominant denomination of cross-border liabilities. Here I stand, I can do no other.”

Recently, there has been a lot of worry over the dollar maintaining its status as the reserve currency because of the potential reallocation of economic interest and influence, mostly due to the rise of countries such as China and the issues in the U.S. political system (a bipartisan issue!). There is speculation that often sounds like “We are going to have hyperinflation [implying an infinite number of dollars being printed] and the purchasing power of the dollar will go to zero [be worthless].”

All countries’ debts to other countries are denominated in dollars, so the currency won’t blow up anytime soon. When people—whether they be policymakers or posters on social media—talk about the dollar being printed into oblivion, it’s really important to talk about the fact that the dollar is a symbol and a transactional tool. It’s the means by which we buy goods and services, but it’s also used to conduct trade deals and international negotiations. As such, the U.S. foreign policy establishment is always working to defend the value of the U.S. dollar.

The most notable trend in recent decades has been the rise of nontraditional reserve currencies—the currencies of countries without the economic scale and volume of cross-border transactions that distinguish traditional reserve currency issuers.

If the dollar dominance comes to an end (a scenario, not a prediction), the greenback could be felled not by the dollar’s main rivals but by a broad group of alternative currencies. So it’s sort of as though the dollar will remain the dollar until money fragments into many other currencies—but there probably isn’t another currency that is going to take its place for a while.

Rethinking the Dollar

Michael Pettis, an expert on the Chinese economy, has written extensively on how hard it would be for us to dedollarize—it’s not just countries deciding to not use the dollar anymore (although that is the beginning of a worrying pattern). And here’s why we won’t see dedollarization anytime soon (probably):

-

The dollar is the best of the lot. The dollar is the best thing out there—clear, liquid financial markets, transparent corporate governance. It’s the least nasty alternative.

-

Structurally. Surplus and deficit national economies exist. What the United States is doing right now is absorbing the world’s surplus from countries such as China, Russia, and Saudi Arabia. Export-oriented economies rely on the dollar to stabilize their own currencies!

-

Even more structurally. There is also a balance of payments to be considered! Current and capital accounts! The United States has a surplus in its capital account, a deficit in its current account. In order for another currency to take on the role of reserve currency, it would have to take on the same structure, which would require a bit of a sacrifice from China (assuming it would go along with that!).

Structure is hard to erode quickly. The IMF sees the shift out of dollars as a shift into currencies of smaller economies—not a shift to one main currency—and one that’s happening slowly, not quickly. That makes sense, right? This ties into the broader themes of domestic protectionism, onshoring, and deglobalization; everyone is going to try to protect their own space.

People have all sorts of incentives for dollar doomerism, such as making money off a newsletter or an investing subscription service to promote the narrative of the dollar losing its status as the reserve currency. And that circles back to detachment, accepting everything at face value, taking media as capital-T Truth.

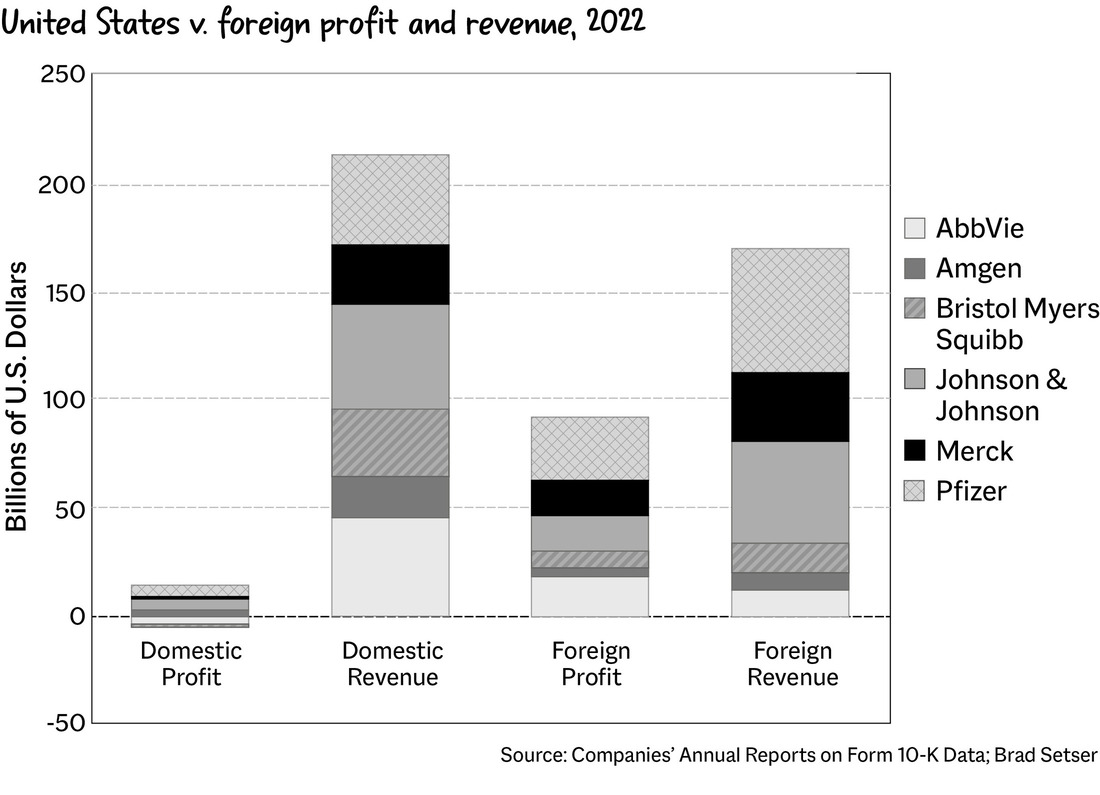

We spend a lot of time worrying about dedollarization, when we really should be worried about other economic woes. As the economist Brad Setser at the Council on Foreign Relations put it, “Waiting for the day when the tax avoidance strategies of US multinationals generate as much sustained attention as ‘de-dollarization’!” Setser did a presentation on tax avoidance by big pharmaceutical companies, and yep, most of their profits are offshore. That’s probably a bigger deal than the very low chance of the dollar losing its reserve currency status.

A lot of people feel that the dollar is not going to be able to maintain its reserve currency status in an increasingly polarized world. But because the dollar is the common denominator of the global economy, it makes everything complicated. If any country pivots away from the United States, the U.S. government can remove it from trade agreements, issue tariffs against it, decline military assistance to it, and basically hang it out to dry—as it did in 2022 after Russia invaded Ukraine.

People want to spend and they want the dollar, and it’s the only real inflation hedge we have, which is definitely counterintuitive. So when we ask, “Can the dollar be replaced?” the answer is, of course, “Maybe.”

There is no real yes or no answer. As we know, anything can happen. But as Perry Mehrling, a professor of economics at Boston University, said on an episode of Bloomberg’s Odd Lots podcast:

The logic of why it’s a good thing to have one currency for the whole country and par clearing for the whole country, the logic is just the same for why it might be a good idea to have one currency for the whole world. And that’s what people get out of it, is that it makes it easier to do trade, to do calculations, to unite the globe into a unified economy…. This notion of separate nation states with separate currencies. This is something that was inherited in our minds from World War II, when that system had all broken down. But that’s not the world we live in now. It’s a global dollar system. And it has a lot of advantages for now that does mean, which you were just coming to at the end, that basically there’s one monetary policy that matters. And that’s U.S. dollar monetary policy that then gets filtered out to the whole rest of the world. And that’s what’s happening now.

The dollar is a global unifier.

Money is a tool, but it’s also a symbol. It’s sort of like the luxury wine sector, which is a trillion-dollar-a-year industry even though many people can’t taste the difference between low- and high-quality, cheap and expensive, red and white wines.

As Samuel Hammond, a senior economist at the Foundation for American Innovation, tweeted, “Wine seems to just be a well-studied microcosm of how human beliefs and desires work more generally. Namely, that they’re socially mediated, easily falsified, unconsciously influenced by cues of status and distinction, and relatively impervious to rational self-reflection.”

How we interact with the world around us is all social! It’s almost unconscious, and it’s all a little silly.

Hammond continued, “If a bottle of aged grape piss can sell for thousands of dollars, what other trillion dollar industries and worldviews are constructed on a foundation of mass preference falsification and status driven self-deception? Almost all of them?”

Money, though seemingly as arbitrary as expensive wine, serves as the universally accepted tool that keeps our global economic engine running. It gets its value from a combination of economic, financial, and political factors, as well as collective trust. The only reason it works, like many things in the economy, is because we believe that it does—it’s all about the people’s faith.

Final Thoughts

It’s a symbol, a tool, and a reflection of our collective beliefs and desires. We’ve seen how money, in all its forms, from seashells to digital entries, shapes economies and influences global dynamics.

The next section is a deep dive into the world of how we measure, track, and analyze money. Money, after all, is not just about what it is, but also about how much of it there is and the stories of growth, challenge, and change that accompany it.