Chapter 3

The Weird World of Money

The Weird World of Money

Money is an ever-present aspect of our daily lives, serving a crucial and complex purpose. Despite its significance, it’s difficult to talk about it. In a room full of people, you might have an easier time talking about bowel movements than feelings about money.

But what is money, really?

Mostly, it is a social construct that relies on people’s trust. Money is a commodified product, a promise. It’s the glue that holds society together because it facilitates transactions, enables growth, and expresses convictions.

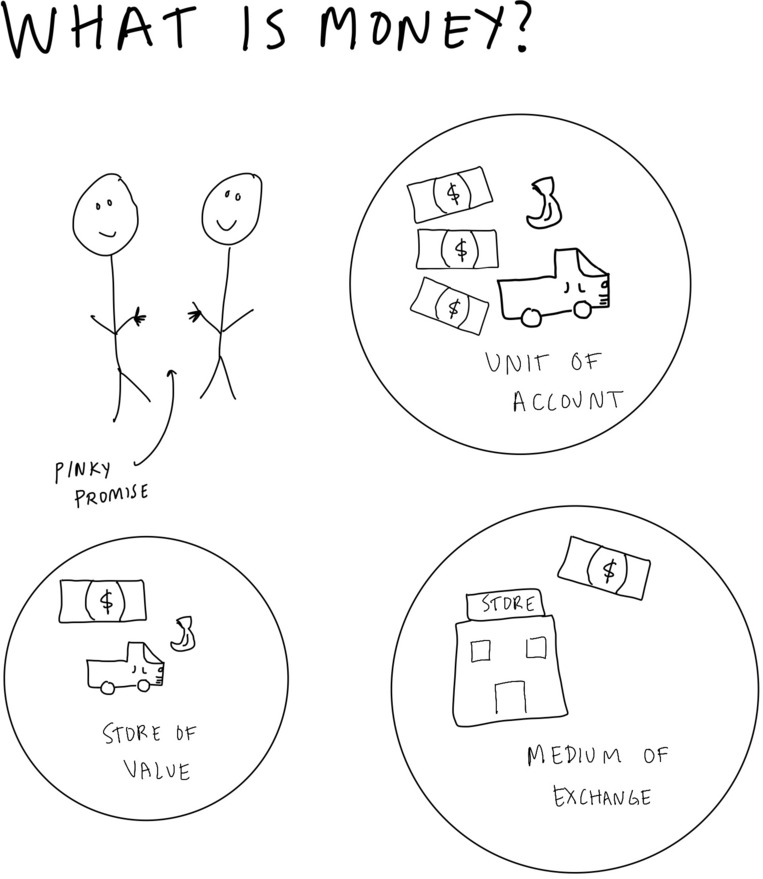

Dollars and Sense: What Makes Money, Money?

Money has three core attributes, and we can talk about them through the analogy of bananas and trucks. It is:

-

A store of value. It holds value over time (however, inflation does complicate this). One dollar today will buy the same number of bananas or trucks tomorrow.

-

A unit of account. It can be used to compare the values of goods and services, so one dollar can buy one banana, whereas many dollars can buy a truck.

-

A medium of exchange. You can go to the grocery store or truck dealership with your dollars, and both will accept your dollars as valid payment for whatever you are trying to buy.

The concept of money is broad and can be pretty much anything that people believe in.

Through the Ages: The Evolution of Money

To understand how money functions in our day-to-day world, we need to look back—way back.

A long time ago, people used things like seashells or mineral chunks as means of exchange. Really, anything that can meet the three pillars—medium of exchange, store of value, and unit of account—can technically be money. For example, if our ancestors had collectively agreed and trusted that toenail clippings had value and could be used reliably for transactions, savings, and accounting, then technically, toenail clippings would have been money in their society (though not a formal currency, which is money that is printed and minted by a government).

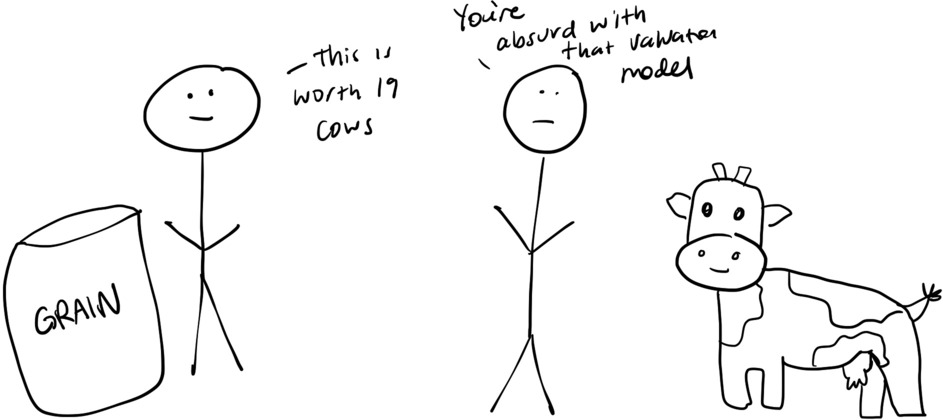

A lot of the ancient systems depended on bartering, the exchange of goods and services without the use of money. But as society kept evolving, it became more complicated to carry around a herd of cows in an attempt to trade them for some grain.

Anthropologists like David Graeber, author of Debt: The First 5000 Years, suggest that early societies operated on the principles of communal sharing rather than strict bartering. However, as societies grew and contact with other civilizations happened, there was a need for a standardized medium of exchange.

Some people thought a certain amount of grain was worth only fifteen cows, some thought it was worth maybe nineteen cows, and that was frustrating for both sellers and buyers to deal with.

Around 3500 b.c.e., Mesopotamia was the first region to establish a monetary system, using clay tokens that represented goods and services. These tokens were one of the first forms of currency, and merchants recorded transactions on clay tablets, a process developed around 3200 b.c.e. As Edward Chancellor wrote in The Price of Time, “We do know that the Mesopotamians charged interest on loans before they discovered how to put wheels on carts.”

Around 600 b.c.e, coins were developed in Lydia, an ancient kingdom in Asia Minor. The coins were made from electrum, a natural alloy of gold and silver, and were much easier to carry around than cows. The coins were a significant advancement, providing a stable, standardized medium of exchange and unit of account.

The coin-based monetary system financed empires for thousands of years, and helped to develop trust in the underlying economic system. Markets were formed, society advanced, and economies continued to grow.

In modern times, most societies have now transitioned to fiat currency, which is money that derives its value not from physical commodities, but from government regulation and public trust. Unlike gold- or silver-backed currencies, fiat money, such as the U.S. dollar, is valued based on the government declaring that it is valuable rather than on its material worth—it’s just made of linen and cotton.

The American Currency Story: Revolution to Recognition

The story of how money evolved in the United States can tell us a lot about the function of money and the monetary system it exists in. In the early 1700s, the American colonies relied mostly on European currencies such as the Spanish piece of eight—though those were in short supply—and barter (want to trade some dried fish for pewter dishes?) as a way to maintain a functioning economy. To help finance the Revolutionary War, the Continental Congress issued a currency called continentals that was backed by the anticipation of future tax revenues, which was a pretty ballsy bet on the projected new country.

Funnily enough, this is actually pretty similar to the way the U.S. currency works now. The U.S. dollar is backed by “the full faith and credit of the U.S. government,” which essentially equates to the value of all the drones, tankers, and military bases that are waiting to pulverize anyone who dares question its status.

Sure, the U.S. government has come a long way in the past 250 years. We’re still using the same foundational document, the Constitution, in an era where technology like an iPhone would have melted a Founding Father. But the method of currency in the 1700s was unstable and inefficient. The fledgling United States required something different if it wanted to grow. The continental was the first currency, but it was plagued by excessive inflation during the Revolutionary War and lack of trust because of that. So in 1785, the Continental Congress dropped the continental, adopting the dollar as the national currency, and five years later the Constitution was ratified.

Alexander Hamilton came along with a plan for banks. There weren’t any banks making loans, so there wasn’t really any way to start a company. The ultrawealthy personally controlled most lending, which isn’t really the best way to distribute scarce resources. Hamilton wanted a federal bank that would provide credit to the government and businesses, issue a national currency, and be a place for people to safely store money. But soon, Thomas Jefferson rolled up, saying that the bank was a bit too central and that the newly created Constitution didn’t give the government power to have anything to do with a national bank or a currency.

The two went to battle, Hamilton won, and the First Bank of the United States was created in 1791. However, it failed to be rechartered twenty years later, for a variety of reasons including the worry that a national bank was an encroachment on states’ rights (and state-chartered banks) and served only commercial and industrial interests. States took matters into their own hands and issued their own currencies, which was an absolute nightmare.

We can make a comparison to the modern-day eurozone, a monetary union of twenty of the twenty-seven European Union countries. These nations have adopted the euro as their shared currency and legal tender, facilitating easier trade and financial transactions across borders. However, this union has faced its challenges, notably during the eurozone crisis that began in 2009. The crisis was primarily fueled by high sovereign debt levels in countries like Greece and Spain, economic imbalances within the zone, and vulnerabilities in the banking sector, all exacerbated by the constraints of a shared monetary policy without a corresponding fiscal union and the spillover effects of the 2008 global financial crisis. The union is a tricky thing to balance with so many countries and the volatile financial climate! But just imagine how difficult it would become if, all of a sudden, some of the member countries stopped accepting the euro and each of them tried to do business and buy things across borders with twenty different currencies. It would be a nightmare! It would be confusing, scattered, and a breeding ground for conflict—which, sure, can be functional, but not really great for long-term growth, stability, and EU unity.

In 1816, when people’s eyeballs were melting out of their skulls from exasperation with the monetary system, Congress chartered the Second Bank of the United States. That lasted twenty years, until Andrew Jackson said, “Absolutely not.”

The Free Banking Era began—when, again, each state made its own rules and created an absolute mess with little to no regulation from the government. It was called the “wildcat” era and for good reason: There were eight thousand state banks, each of which issued its own notes that were denominated in dollars but represented claims on the bank’s assets. Because they were issued by state-chartered banks, the value and stability of the banknotes were variable, depending on which bank had issued the note; some banks were reliable, and others were not. That made it very difficult for customers to do what they needed to do at the banks: banking. The banks essentially became useless.

The government was ripping their hair out of their heads in frustration. So in 1863, the National Banking Act was passed, which created a uniform national currency and allowed only nationally chartered banks to issue notes.

For a long time, money in the United States was tied to the value of gold. For a myriad of reasons, the country went off the gold standard in 1971. Each dollar had a specific value in terms of gold and could be converted into gold at that rate. It’s pretty tough to maintain fixed exchange rates when economies are waffling as they did in the 1970s, so the fixed exchange rate system had to end. After the gold standard fell apart, money became an abstract way to keep score (the shift from money being a physical representation of value through gold, to it being a symbolic representation of value based on trust and shared agreement) and maintain a stable economy. Our money today is fiat money. It doesn’t have an intrinsic value, but it does have “the government says this is valuable and therefore it is” value.

Despite what some might say, it’s actually good that we aren’t on the gold standard anymore. The gold standard was restrictive, and switching to fiat has allowed greater flexibility in monetary policy, which is crucial for enabling governments to respond more effectively to financial crises, regulate inflation, and stimulate economic growth. To this day, the Federal Reserve helps enforce the promise and collective trust that we all have in money.

All central banks, including the Fed, are economic vibe setters, the guardians of the money. Central banks gained a significant amount of power in the nineteenth and twentieth centuries, such as the Bank of Japan being established in 1882 and Germany’s Bundesbank (a significant inspiration for the European Central Bank) in 1957, something we will discuss in a later chapter.

Money functions to get us onto the roller coaster of life: to stand in that long line, get buckled into the seat, and go for a ride over all the ups and downs.

But how does money work in the modern economy?