Chapter 2

The Vibe Economy

Economics can be seen as the ultimate tool for decoding our collective decisions. It’s about understanding the whys and hows of our resource use—the choices we make in the corridors of legislation and regulation and in our everyday lives.

It isn’t just a dry collection of figures and theories; it’s a dynamic map of human behavior, a guide to navigating the complex networks of supply, demand, and market forces, and a primer on the policy and perspectives that guide our societal wants and needs.

Moods and Markets

Living in an uncertain world is challenging. We have animal brains, and our animal brains like to know what is happening. Our brains are built to process the negative first because it helps us plan for future survival.

It’s tempting for talking heads to point to economic data and say, “Look at these industrial production metrics; you should feel optimistic right now.” But let’s be honest—that doesn’t reflect many people’s everyday experiences. In this chapter, I will focus on how expectations, theory, and reality create the vibes of our economy.

The Economic Circle of Life

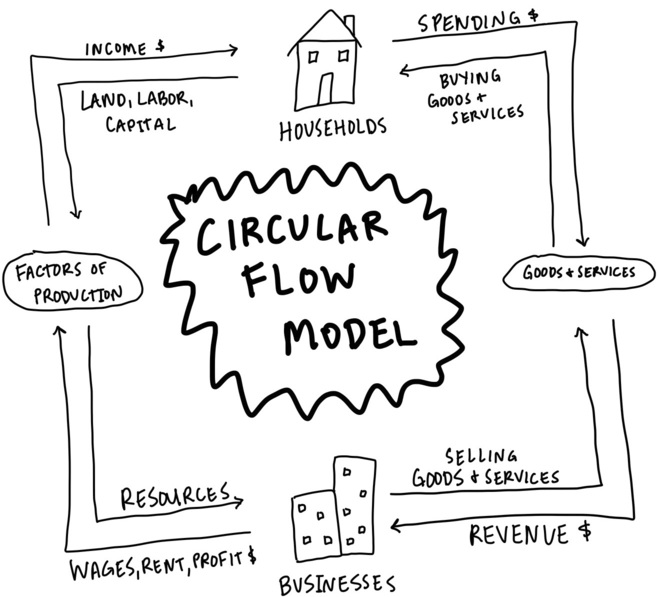

The circular flow diagram helps to chart the flow of resources and money. It’s a blueprint that illustrates the interactions between two key players: households and businesses. Households provide labor to businesses and, in return, get compensated with wages and salaries.

They then use this income to purchase goods and services from businesses. Businesses depend on households not only as a source of labor but also as consumers who buy their products.

The government is there, too, of course, collecting taxes and redistributing income, which has a ripple effect in impacting how much households can spend and how businesses plan their investments. The financial sector manages the flow of savings and investments and conducts external trade with other countries.

The diagram is just one model of the economy, but it shows how many moving parts there are. There’s a lot of complexity in the way the economy works, and this is why there’s such a gap between the data and lived reality sometimes.

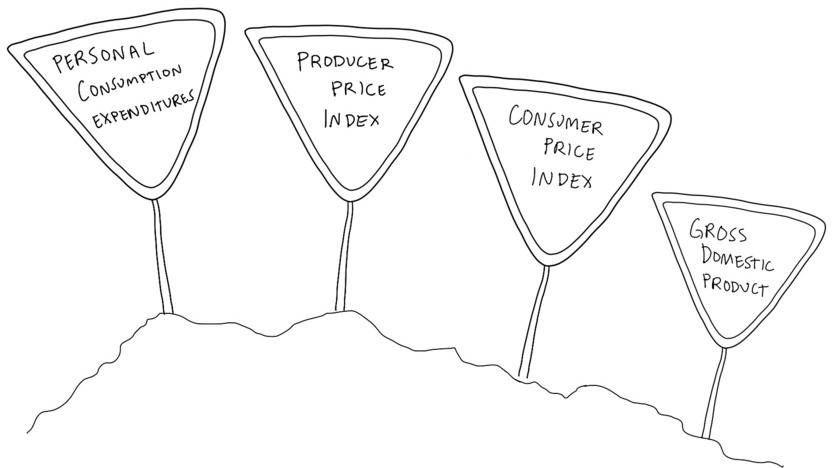

Navigating the economy’s twists and turns can feel like decoding a secret language of acronyms and figures. While these metrics—think GDP, CPI, PCE, and PPI (terms that will all get explained later on)—are pivotal in measuring economic health, they often miss the mark in reflecting people’s day-to-day realities.

The pinch of escalating food costs, the sting of rising rent, and the stress of mortgage payments don’t always sync up with the so-called success stories these numbers narrate. This discord between hard data and the lived experience is the core of the “vibes economy.”

Fueling Feelings

When gasoline prices increase in the United States, consumer sentiment tends to decrease, and this can shape how the economy works. High gas prices make us feel bad—and it’s not hard to see why.

-

High gas prices impact everyone who owns a car, and also affect the prices of goods that require transportation, which is basically everything we buy—not to mention the cost of heating homes and producing electricity. Oil is the common denominator to the economy—and everything is swayed by its cost.

-

We are swayed by prices, and if prices are high, we feel bad.

-

If we feel bad, the economy feels bad.

Bright neon signs on every street corner remind us of how expensive it is to be alive. High gas prices do not a recession make. But they sure can feel like one.

What Is OPEC?

The oil market is influenced by how much oil is being produced by the Organization of the Petroleum Exporting Countries, or OPEC (as well as other producers, including the United States) and how many people are consuming that oil—supply and demand! It balances international relations, is affected by domestic politics and policies, and manages the extensive network of supply chains that gets oil from the ground into basically everything. Oil prices are just one example of how our feelings can shape the economy—and how important it is to manage sentiment.

Vibe-Ology and Emotion Economy

There is nothing new or unique about the concept of sentiment driving the economy. John Maynard Keynes coined the term animal spirits to describe how emotions can influence people’s decisions and market behavior. Concepts like irrational exuberance, herd mentality, and risk appetite all fall under this sentiment-driven economic umbrella.

Economic Theory |

The Role of Emotions |

One theory worth studying more closely is reflexivity, the legendary trader George Soros’s theory that there’s a feedback loop between what people think and what actually ends up happening, which in turn changes the way people think. The internet bubble is a key example of this—

-

Initial Perception/Belief: In the late 1990s, there was widespread belief that the internet would revolutionize businesses (which it did!) and that traditional valuation metrics didn’t apply to internet-based companies (which they…did). This belief led to increasing valuations for tech startups, many of which were making no money.

-

Market Action Based on Belief: Investors began pouring money into technology stocks and internet startups, driving their prices up. This was partly based on the notion that the internet’s potential was so vast that even high valuations were justified.

-

Reflexive Feedback Loop: As more money flowed into the tech sector and share prices rose, it reinforced the belief that the internet was fundamentally transformative! And that these high valuations were justified. The rising stock prices attracted even more investors, further driving up prices.

-

Bubble Bursts: Eventually, when the realization set in that many of these companies wouldn’t be profitable for years (if at all), the bubble burst. Stock prices plummeted, leading to the dot-com crash in the early 2000s.

Soros argues that highly valued companies that have attracted significant investments based on the expectation of their future profitability—often due more to narrative than to objective analysis—gain a critical edge in hiring and get the best talent in the field. Who doesn’t want to work for the new hot startup, which could be the next Google or Apple or Microsoft? Then their valuation (based on expectations) brings in more investors, more money, more growth, and even better talent. This example highlights the blurred line between perception and reality: Is the stock price high because the company is growing, or is the company growing because the stock price is high? Perhaps worst of all, is the company stagnant with a high stock price—overvalued, a bubble, not reflective of reality?

This passage from the economist Fischer Black’s 1986 paper “Noise” also discusses the same concept.

I think that the price level and rate of inflation are indeterminate. They are whatever people think they will be. They are determined by expectations, but expectations follow no rational rules. If people believe that certain changes in the money stock will cause changes in the rate of inflation, that may well happen, because their expectations will be built into their long-term contracts. (Author’s emphasis.)

Of course, our expectations influence our reality. What we think will happen ends up happening, which influences what happens later. Emotions (vibes) are the key driver of a lot of the decisions that we make.

All of this, coupled with our personal experiences in the world, influences our perception and interpretation of the world and our subsequent discourse about it. This is how we feel. This is vibes.

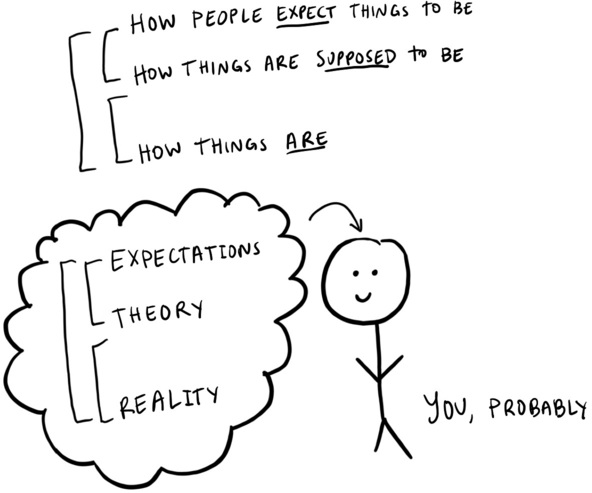

The Uncertainty Cake

When we’re worried about the economy, we are usually worried about our own money. This creates the perfect recipe for a cake of uncertainty, composed of expectations, theory, and reality, based on:

-

Expectations: How we expect things to be

-

Theory: How things are supposed to be

-

Reality: How things are

Our vibes are multiplied across the economy. Your vibes compound with everyone else’s vibes, and that, at a very basic level, creates consumer sentiment. As I talk about in the GDP chapter, consumer sentiment is everything because it drives consumer spending, the central driver of GDP growth.

When expectations, theory, and reality diverge, that’s when the vibes get really weird. Economic theory is the perfect example of this. There is a gap between what textbooks say is going to happen and what companies actually end up doing. Economics is known as the dismal science, but it really should be known as the dismal art. Most stock valuation models are an educated guess about the future; most economic theory is measurable, but on the basis of loose facts. As the English author Hilary Mantel wrote in a 2017 Guardian piece on facts, history, and truth, “Evidence is always partial. Facts are not truth, though they are part of it—information is not knowledge. And history is not the past—it is the method we have evolved of organising our ignorance of the past. It’s the record of what’s left on the record.”

Random facts may not always tell the whole truth! This creates cognitive dissonance as it makes us hold conflicting beliefs, because like, hello! What do you mean nothing ever really makes sense and no one really knows what is going on?

Economic Mood Rings

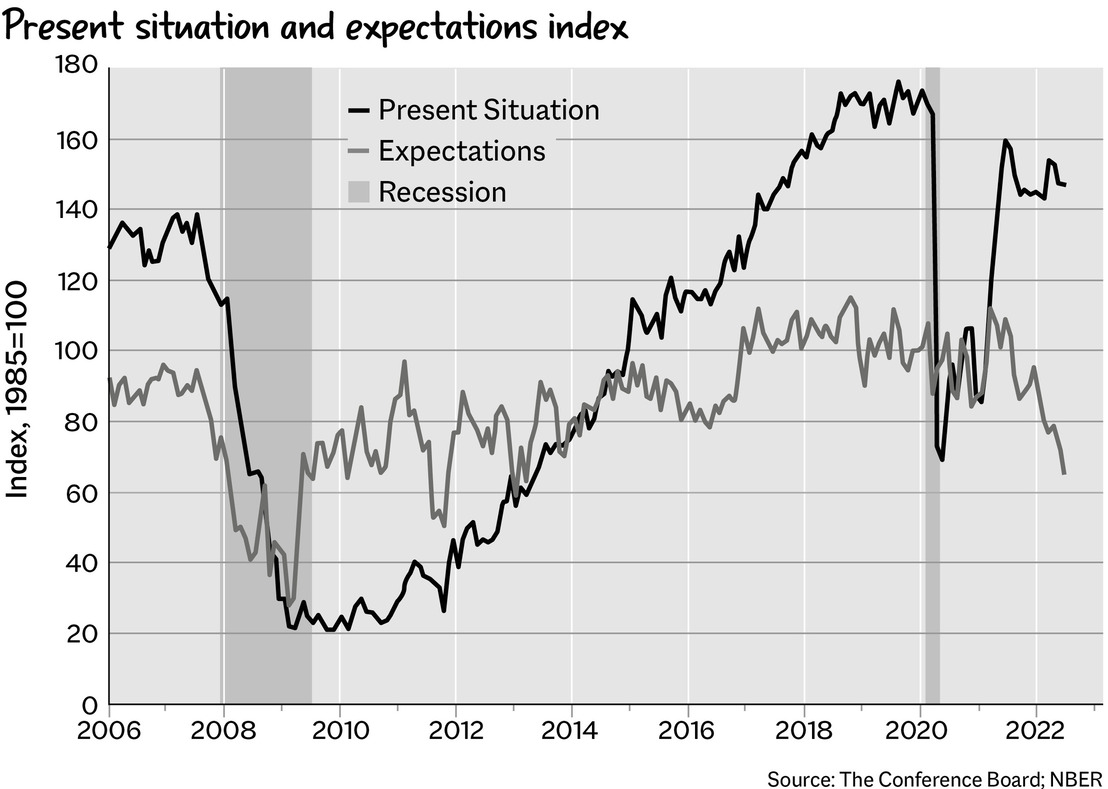

We can look at certain metrics to gauge this element of cognitive dissonance. The Consumer Confidence Survey, for example, is a measure produced by the Conference Board that provides key insights into consumer confidence. Other measures of global consumer confidence, including the Conference Board Global Consumer Confidence Index, and survey firms such as Nielsen, Ipsos, and GfK, give us insight into consumer attitudes, economic expectations, and labor market perception, providing a general sense of how people feel about the present situation and their expectations. When there is a gap between the present situation and people’s expectations, that’s not good, because that means people are like, “Wow, things are really bad and they are about to get a whole lot worse.”

Of course, the feeling of things being bad compounds. There is a gap between confidence measures, so we aren’t even that confident in our confidence! But when there is a divergence between reality and expected reality, that is not good.

We can apply the vibes-based model to our world pretty easily. When people are feeling bad, they often run their actions through this vibes-based model subconsciously. If people are feeling uncertain, they might stop spending money, which impacts the entire economy. That’s the power that people—including you—have in shaping our economic reality. This applies to all sorts of economic data points, too. As Josh Zumbrun in The Wall Street Journal put it, “Expected inflation is, in some sense, a self-fulfilling prophecy. If people expect it to continue, they might raise prices for their business or ask for raises at their jobs, fueling continuing price increases.”

Think about how vibes based that is: Inflation is entirely dependent on what people expect to happen! Experience, evidence, expectations, perception, and interpretation are all key economic variables—and it can be tough to manage the economy when all the vibes are off. So, of course, the obvious solution is to have people manifest the right vibes, right?

Ha-ha, I wish. Vibes are just one part of the equation. When it feels like everything is falling apart, people want to point fingers, place blame, and say, “This is not how things should be!” And the problem is that they are right; this isn’t how things should be. Everyone is searching for broader freedoms in a world dominated by corporations and advertising and also if you have a feeling just medicate it and also student loans and also the housing crisis and also hyper-individualism and also the Earth is burning so there is nothing left to do but try to save it.

In an ideal world, problems would be simple and solutions would be easy. But as James Baldwin once said, “The hardest thing in the world is simplicity.” We live in a complex universe, which makes it incredibly difficult to point at any one thing as the Number One Problem.